LIST OF REFERENCES

Vietnamese Document Catalog

1. Huynh The Nguyen and Nguyen Quyet, 2013. The relationship between exchange rate, interest rate and stock price in Ho Chi Minh City. Journal of development and integration, No. 11 (21), pp. 37-41.

2. Nguyen Thi Ngoc Trang, 2007. Financial risk management . Statistical publishing house.

3. Nguyen Thi Ngoc Trang and Nguyen Huu Tuan, 2014. Monetary policy transparency and retail interest rate pass-through in Vietnam. Journal of development and integration, No. 15 (25).

4. Tran Ngoc Tho et al., 2005. Modern corporate finance . Ho Chi Minh City: Statistical Publishing House.

5. Truong Dong Loc, 2014. Factors affecting stock price changes: evidence from Ho Chi Minh City Stock Exchange. Can Tho University Science Journal, No. 33 (2014), pp. 72 – 78.

English Document Catalog

1. Akaike, H., (1974). A new look at statistical model identification, IEEE Transactions on Automatic Control , AC-19:716-723.

2. Bach, B., Ando, A., 1957. The redistribution of effects of inflation. The Review of Economics and Statistics , 3: 1–13.

3. Bollerslev, T., 1986. Generalized autoregressive conditional heteroskedasticity.

Journal of Econometrics , 31: 307–327.

4. Booth, J., Officer, D.T., 1985. Expectations, interest rates, and commercial bank stocks. Journal of Financial Research , 8: 51–58.

5. Chamberlain, S., Howe, J., Popper, H., 1997. The exchange rate exposure of US and Japanese banking institutions. Journal of Banking & Finance , 21:871–892.

6. Chance, DM, Lane, WR, 1980. A re-examination of interest rate sensitivity in the common stocks of financial institutions. Journal of Financial Research , 3:49–55.

7. Choi, JJ, Elyasiani, E., Kopecky, K., 1992. The sensitivity of bank stock returns to market, interest, and exchange rate risks. Journal of Banking & Finance , 16:983–1004.

8. Christian CP Wolff, HA Benink, 2000. Survey Data and the Interest Rate Sensitivity of US Bank Stock Returns. Economic Notes , 29: 201-213.

9. Dickey, DA and Fuller, WA, 1981. Distribution of the estimators for autoregressive time series with a unit root. Econometrica , 49:1057- 1072.

10. Dinenis E. & SK Staikouras, 1998. Interest rate changes and common stock returns of financial institutions: evidence from the UK. The European Journal of Finance , 4: 113-127

11. Elyasiani, E., Mansur, I., 1998. Sensitivity of bank stock returns distribution to changes in the level of volatility of interest rate: a GARCH-M model. Journal of Banking & Finance , 22: 535–563.

12. Elyasiani, E., Mansur, I., 2003. International spillover of risk and return among major banking institutions: a bivariate GARCH model. Journal of Accounting, Auditing, and Finance , 23: 303–330.

13. Engle, RF, 1982. Autoregressive conditional heteroscedasticity with estimates of the variance of United Kingdom inflations. Econometrica , 50:987-1007.

14. Engle, RF, Ng, V., Rothschild, M., 1990. Asset pricing with a factor-ARCH covariance structure: empirical estimates for treasury bills. Journal of Econometrics , 45: 213–238.

15. Fama, Eugene F., and Kenneth R. Frech, 1992. “The cross – section of Expected Stock Returns”. Journal of Finance , 47:427 – 465.

16. Fama, Eugene F., and Kenneth R. Frech, 1993. “Common Risk Factors in the Returns on Stocks and Bonds”. Journal of Financial Economics , 33: 3-56

17. Flannery, M., James, C., 1984. The effect of interest rate changes on the common stock returns of financial institutions. The Journal of Finance , 39:1141–1153.

18. Flannery, MJ, Hameed, AS, Harjes, RH, 1997. Asset pricing, time-varying risk premia and interest rate risk. Journal of Banking & Finance , 21: 315–335.

19. French, K., Ruback, R., Schwart, G., 1983. Effects of nominal contracting on stock returns. Journal of Political Economy , 70–96.

20. Gilkenson, J., Smith, S., 1992. The convexity trap: pitfalls in financing mortgage portfolios and related securities. Economic Review. Federal Reserve Bank of Atlanta , 4–27.

21. Grammatikos, T., Saunders, A., Swear, I., 1986. Returns and risks of US bank foreign currency activities. The Journal of Finance , 4: 671–683.

22. Hahm, JH, 2004. Interest rate and exchange rate exposures of banking institutions in pre-crisis Korea. Applied Economics , 36:1409–1419.

23. Hooy, CW, Tan, HB, Md Nassir, A., 2004. Risk sensitivity of bank stocks in Malaysia: Empirical evidence across the Asian financial crisis. Asian Economic Journal , 18: 261–276.

24. Kessel, R., 1956. Inflation-caused wealth redistribution: a test of a hypothesis. The American Economic Review , 3: 128–141.

25. Lloyd, WP, Shick, RA, 1977. A test of stone's two-index model of returns.

Journal of Financial and Quantitative Analysis , 12: 363–376.

26. Lynge, MJ, Zumwalt, JK, 1980. An empirical study of the interest rate sensitivity of commercial bank returns: a multi-index approach. Journal of Financial and Quantitative Analysis , 15: 731–742.

27. Mansur, I., Elyasiani, E., 1995. Sensitivity of bank equity returns to the level and volatility of interest rates. Managerial Finance , 21:58–77.

28. Merton, RC, 1973. An intertemporal capital asset pricing model. Econometrica , 41:867–887.

29. Ross, S., 1976. The Arbitrage theory of capital asset pricing. Journal of Economic Theory , 13: 314-360.

30. Ryan, Suzame K., Worthington, Andrew C., 2004. Market, interest rate and foreign exchange rate risk in Australian banking: A GARCH-M approach. International Journal of Applied Business and Economic Research , 2: 81-103.

31. Saadet Kasman, Vardar, G., and Tunc, G., 2011. The impact of interest rate and exchange rate volatility on banks' stock returns and volatility: Evidence from Turkey. Economic Modeling , 28: 1328-1334.

32. Saunders, A., Yourougou, P., 1990. Are banks special? The separation of banking from commerce and interest rate risk. Journal of Economics and Business , 42: 171– 182.

33. Scott, WL, Peterson, RL, 1986. Interest rate risk and equity values of hedged and unhedged financial intermediaries. Journal of Financial Research , 9: 325–329.

34. Song, F., 1994. A two factor ARCH model for deposit-institution stock returns.

Journal of Money Credit and Banking , 26: 323–340.

35. Stone, B., 1974. Systematic interest rate risk in a two index model of returns.

Journal of Financial and Quantitative Analysis , 9: 709–721.

36. Sweeney, R., Warga, A., 1986. The pricing of interest rate risk: evidence from the stock market. The Journal of Finance, 41:393–410.

37. Wetmore, JL, Brick, JR, 1994. Commercial bank risk: market interest rate, foreign exchange. Journal of Financial Research , 17: 585–596.

38. Yourougou, P., 1990. Interest rate and the pricing of depository financial intermediary common stock: empirical evidence. Journal of Banking & Finance , 14: 803–820.

APPENDIX: RESULTS OF RUNNING REGRESSION MODEL

RESULTS OF RUNNING DESCRIPTIVE STATISTICS AND ADF TEST

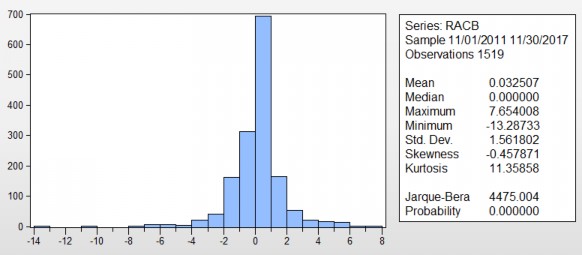

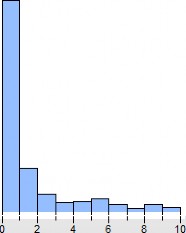

ACB

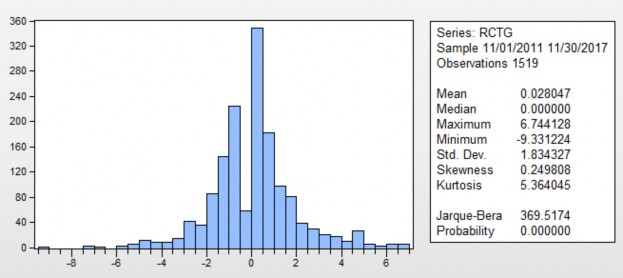

CTG

MBB

70 0

60 0

? 0 0

40 0

300

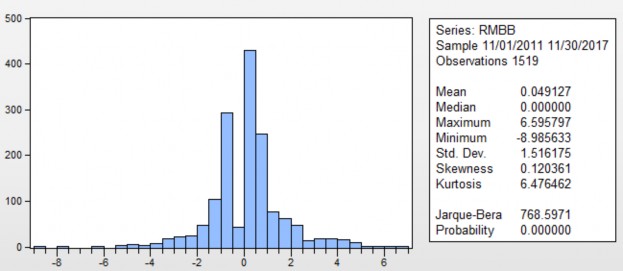

Mean | -0.003991 |

Median | 0.000000 |

Maximum | 9.531018 |

Minimum | -10.53605 |

Std. Dev. | 3.408486 |

Skewness | 0.057135 |

Kurtosis | 4.380374 |

Jarque-Bera | 121.4245 |

Probability | 0.000000 |

Maybe you are interested!

-

Current Status of Control, Monitoring and Reporting of Interest Rate Risk

Current Status of Control, Monitoring and Reporting of Interest Rate Risk -

CPI Fluctuations and Usd/VND Exchange Rate in the Second Half of 2011

CPI Fluctuations and Usd/VND Exchange Rate in the Second Half of 2011 -

Interest rate risk management at Vietnam Joint Stock Commercial Bank for Industry and Trade - 32

Interest rate risk management at Vietnam Joint Stock Commercial Bank for Industry and Trade - 32 -

Perfecting the interest rate management mechanism of the State Bank of Vietnam in the conditions of a market economy - 30

Perfecting the interest rate management mechanism of the State Bank of Vietnam in the conditions of a market economy - 30 -

Applying Taylor rule in the interest rate management mechanism of the State Bank of Vietnam - 28

Applying Taylor rule in the interest rate management mechanism of the State Bank of Vietnam - 28

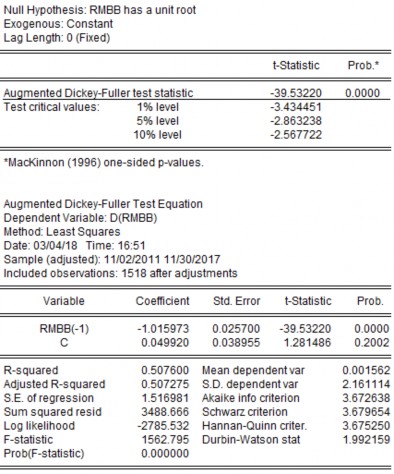

Null Hypothesis: RNVB has a unit root Exo genous: Constant

Lag Length: O (Fixed)

t-Statistic | Prob ' | |

.éuomented D ickeY-Fuller test statistic | -49.23271 | 0.0001 |

Test critical values: 1% level | -3.434451 | |

5% level | -2863238 | |

10 % level | -2.567722 | |

-

-

-

-

Series. RNVB

Sample 11.!01.!2011 11.!30.!2017

Observations 1519

* klacKinn on (1996) one-s ide d p-values.

.Aug mented D ickey-Fuller Te st Equation Dependent Variab Ie: D (RNVB)

I lethod: Le ast Squares Date: 04/03/18 Time: 16: 5 6

Sample (adjustment ): 1 February 1, 201 1 1 January 30, 2017 Included observations: 1518 after adjustments

Variable

coefficient | Std. Error t-Statistic | Prob. | |

RNVB(-1) | -1.230845 | 0.025001 -49.23271 | 0.0000 |

c | -0.005497 | 0.085179 -0.064533 | 0.9486 |

R-squared | 0.615215 | dependent variable | 0.002518 |

.Pdjusted R-squared | 0.614961 | SD dependent var | 5.348281 |

SE of regression | 3.318690 | .4kaike info criterion | 5.238334 |

Sum squared residue | 16696.77 | Schwarz criterion | 5.245350 |

Log likelihood | -3973.895 | Hannan-Quinn critic. | 5.240946 |

F-statistic | 2423.860 | Durb in-'.Watson stat | 2.02 9732 |

Prob(F-statistic) | 0.000000 |