Interest Rates 2009

12

10

8

6

4

2

0

1

2

3

4

5 6 7

Month

8

9

10 11

Interest rate

The difference in USD/VND price is quite large, the domestic currency is devalued, people switch to depositing foreign currency to avoid the devaluation of the domestic currency.

Chart 2.5. VND deposit interest rates in 2009

Capital mobilized in VND in 2010 was the highest increase compared to previous years, reaching

734,160 billion VND (up 32.45% compared to 2009) mainly short-term from 1-3 months. Meanwhile, capital mobilized in foreign currency in 2010 reached 280,740 billion VND, up 20.64% compared to 2009. The growth rate of capital mobilized in VND is higher than that of capital mobilized in foreign currency converted to VND because the interest rate mobilized in VND is quite high compared to the interest rate mobilized in foreign currency, specifically:

Table 2.4. Average mobilization interest rate at some points in 2010

VND deposit interest rates for some terms at some points in 2010

(unit: %)

Day | 1 month | 2 month | 3 month | 6 month | 9 month | 12 month | 18 month | 24 month | 36 month |

12/31/09 | 10.29 | 10,289 | 10.35 | 10.37 | 10.36 | 10.37 | 10,367 | 10,387 | 10.38 |

06/26/10 | 11.19 | 11.28 | 11.38 | 11,468 | 11.47 | 11.51 | 11.29 | 11.32 | 11.32 |

12/31/10 | 13.68 | 13.69 | 13.65 | 13.34 | 13.05 | 13.38 | 12.32 | 12.34 | 12.35 |

Maybe you are interested!

-

Solutions to enhance capital mobilization at Lien Viet Post Joint Stock Commercial Bank - Hai Phong Branch - 9

Solutions to enhance capital mobilization at Lien Viet Post Joint Stock Commercial Bank - Hai Phong Branch - 9 -

Solutions to Improve Capital Mobilization Efficiency at Vietnam Foreign Trade Bank

Solutions to Improve Capital Mobilization Efficiency at Vietnam Foreign Trade Bank -

Research Results on the Relationship Between Exchange Rate Level and FDI Capital in Vietnam and Discussion

Research Results on the Relationship Between Exchange Rate Level and FDI Capital in Vietnam and Discussion -

Solutions to enhance capital mobilization at Lien Viet Post Joint Stock Commercial Bank - Hai Phong Branch - 8

Solutions to enhance capital mobilization at Lien Viet Post Joint Stock Commercial Bank - Hai Phong Branch - 8 -

Solutions to enhance capital mobilization at Dong Trieu Branch of Investment and Development Bank - Quang Ninh - 4

Solutions to enhance capital mobilization at Dong Trieu Branch of Investment and Development Bank - Quang Ninh - 4

“Source: Author's synthesis and calculation”

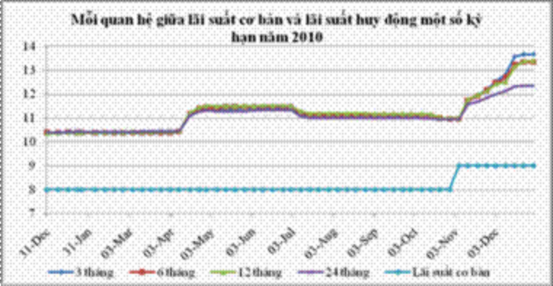

Chart 2.6. Relationship between base interest rate and deposit interest rate for some terms in 2010

The market has been “calm” for 11 months. On November 5, 2010, the State Bank issued a regulation to raise interest rates to 9%, and banks immediately increased their deposit interest rates to 12% per year. However, 12% per year was just a formality, and some banks lacking capital quietly increased their deposit interest rates in many forms, and by the end of November, the interest rate had reached 14%. In early December, the Banking Association announced a “consensus interest rate” of 12% per year.

On December 14, 2010, the Banking Association continued to issue a consensus interest rate, this time with a larger number of participating banks and stronger measures, accordingly the mobilization interest rate margin was raised to 14% including promotional forms.

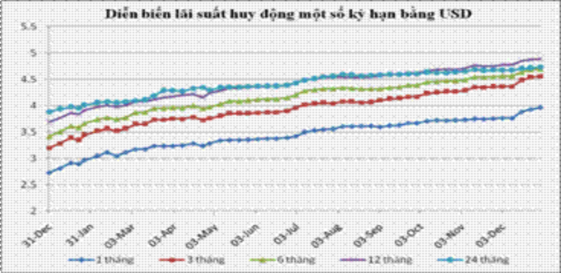

Regarding foreign currency interest rates : Foreign currency deposit and lending interest rates in 2010 continued to increase slightly throughout all months (as of the end of December, USD deposit interest rates increased by about 0.82 - 1.36% for all terms compared to early January 2010).

Chart 2.7 Interest rate developments for some terms in USD

Table 2.5. USD mobilization interest rates for some terms at some points in 2010 (unit: %)

Day

1 month | 2 month | 3 month | 6 month | 9 month | 12 month | 18 month | 24 month | 36 month | |

12/31/09 | 2.7 | 2.87 | 3.20 | 3.42 | 3.53 | 3,693 | 3.86 | 3,886 | 3.91 |

06/26/10 | 3.4 | 3.61 | 3.90 | 4.04 | 4.15 | 4.21 | 4.39 | 4.33 | 4.39 |

12/31/10 | 3.96 | 4.21 | 4.56 | 4.76 | 4.7 | 4.76 | 4.89 | 4,689 | 4.73 |

“Source: Author's synthesis and calculation”

Thus, the mobilization interest rate level is under pressure to increase during the year due to a number of main reasons: The demand for capital for investment, production, business and consumption continues to increase in the context of economic recovery; Under pressure from the inflation index due to the delayed impact of policies in 2009 (in 2010, the consumer price index only remained stable from March to August, the remaining months fluctuated highly, affecting many macroeconomic targets of the Government and monetary policy measures of the State Bank); Unhealthy competition of some credit institutions and the psychology and expectations of the people. Although the interest rate level has many fluctuations, it still ensures the interests of depositors in the context of inflation.

increased at the end of the year, so the capital mobilization speed in 2010 has improved significantly compared to previous years.

2.3.2. Capital use activities of some commercial banks in Ho Chi Minh City.

Table 2.6. Credit balance situation of some commercial banks in Ho Chi Minh City

Unit: Trillion VND

Year

Category

2008 | 2009 | 2010 | % compare next year to previous year | ||

2009/2008 | 2010/2009 | ||||

1. By currency | |||||

In VND | 360.41 | 536.91 | 640.08 | 48.97% | 19.22% |

In foreign currency (in VND) | 141.96 | 162.99 | 247.14 | 14.69% | 51.80% |

2. By type of credit | |||||

Short term | 280.96 | 405.80 | 508.50 | 44.43% | 25.31% |

Medium, long term | 221.72 | 294.20 | 380.50 | 32.69% | 29.33% |

Total outstanding loans | 502.68 | 700.00 | 889.00 | 39.25% | 27% |

“Source: Ho Chi Minh City Statistical Yearbook 2010” [55]

700

600

In VND

In foreign currency (converted to VND)

500

400

300

200

100

0

2008 2009 2010

Figure 2.8 Graph showing credit balance by currency.

600

500

400

Short term

Medium, long term

300

200

100

0

2008 2009 2010

Figure 2.9. Graph showing credit balance by debt term

After implementing the negotiated interest rate mechanism and along with the flexible monetary management measures of the State Bank at the end of 2010, the VND mobilization and lending interest rates of commercial banks have gradually decreased with the VND mobilization interest rate not exceeding 14%/year; the average lending interest rate is 15.27%/year. In addition, the difference between the lending interest rate and the average VND mobilization interest rate is only about 2.5%/year, lower than in previous years (this figure was 4.62%/year in 2008; 4.45%/year in 2007; 4.63%/year in 2006 and 3.42%/year in 2005). In particular, the USD deposit and lending interest rates by December 2010 increased by about 0.5%/year compared to the end of 2009, specifically, the average deposit interest rate was at 4.08%/year and the average lending interest rate was at 6.26%/year.

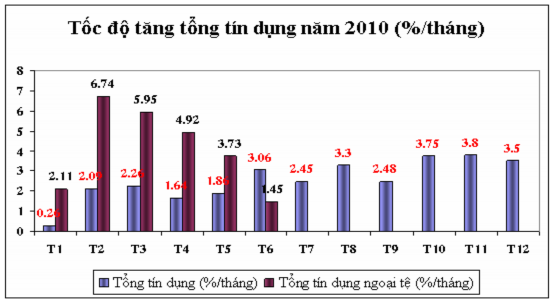

Chart 2.10. Total credit growth rate in 2010 (% month)

By the end of 2010: Total outstanding credit reached VND 889,000 billion, up 27% over the same period. Outstanding credit of commercial banks reached VND 506,730 billion, accounting for 57% of total outstanding credit, up 31.6% over the same period. Outstanding credit in VND increased by 19.22% over the same period, outstanding foreign currency reached VND 247,140 billion, up 51.80% over the same period. The reason for the strong increase in outstanding foreign currency credit is because foreign currency loan interest rates are much lower than VND loan interest rates, businesses will benefit more when borrowing in foreign currency.

In 2009, outstanding credit in VND increased quite high by 48.97% compared to the same period in 2008, reaching 536,910.4 billion VND. This increase was due to the difference in interest rates between VND and foreign currencies when implementing interest rate support in the Government's stimulus program. Outstanding short-term credit accounted for 57.97% of total outstanding debt, up 44.43% compared to the same period; outstanding medium and long-term credit increased 32.69% compared to the same period.

Regarding the loan capital structure, according to the table, short-term credit accounts for the main proportion, more than 50% of total outstanding debt and is increasingly increasing. If in 2008 the proportion of short-term credit outstanding debt accounted for 55.89% of total outstanding debt, by 2009 it was 57.97%. This comes from the fact that commercial banks are limiting medium and long-term loans, mainly short-term loans because the mobilized capital is mainly short-term. If short-term mobilized capital is used for medium and long-term loans

Commercial banks will face high liquidity risks when deposits mature and the banks have not yet recovered the loans.

2.4. Capital mobilization activities of some commercial banks in Ho Chi Minh City in recent times.

Interest rates for VND deposits from 1-12 months are higher than those for long terms from 13 months and up . Commercial banks have introduced many forms of capital mobilization such as regular savings, prize savings with many attractive prizes, issuing short-term valuable papers such as promissory notes, deposit certificates, etc., but capital mobilization still faces many difficulties. With a ceiling interest rate of 14% for VND and 2% for USD, depositors are not very interested in depositing money in banks because the interest rate is too low, while inflation is high (inflation in 2011 was 18.58%), the amount of interest received is not enough to ensure their lives.

The determination of the mobilization interest rate has led to the phenomenon of circumventing the interest rate ceiling in some commercial banks in the form of paying brokerage commissions, lending capital trust, paying the difference from other expenses while the mobilization interest rate set by the State Bank is still printed on the books, etc. Depositors have withdrawn money from commercial banks with low mobilization interest rates to deposit in commercial banks with higher interest rates, making the capital sources of commercial banks always in an unstable state, making it difficult to plan future business strategies. Some joint stock commercial banks have mobilized more than the ceiling interest rate of 14% such as HDBank and DongAbank, making it very difficult for the State Bank to operate monetary and financial policies.

The tightening of the deposit interest rate ceiling of 14%/year is also a reason for the narrowing of cash flow into banks and the imbalance between sources and use of resources. Specifically, the data published by the State Bank of Vietnam shows that, comparing October 2011 with December 31, 2010, the mobilization of the whole system increased by only 8.59% but credit increased by 8.61%, the balance between sources and use of resources has a significant difference. Since October 2011, some credit institutions have had temporary liquidity difficulties due to the imbalance in terms between short-term capital mobilization and medium- and long-term loans, due to the decrease in capital mobilization from organizations and individuals, capital mobilization on the interbank market

not enough to compensate, but has been supported by the State Bank through refinancing and open market operations. Foreign currency liquidity was low in the first 7 months of the year, but has improved since August after the State Bank implemented a number of measures to control foreign currency credit. This imbalance has left weak liquidity units with no other choice but to endure high interest rates on the interbank market. Some small commercial banks that could not mobilize capital had to borrow from financial companies with collateral being valuable papers (bonds). This is very beneficial for financial companies because they often undervalue (about 30-60%) the real value of valuable papers.

A shift in capital sources among commercial banks when there is a ceiling on deposit interest rates . If following the risk trend, with the same interest rate, the flow of savings will tend to shift to safer banks, meaning that the flow of money will shift from small banks to large banks, leading to a sharp decline in the mobilized capital of many banks. On the other hand, with the information that some small banks were merged in the restructuring plan of the banking industry (recently the merger of 3 banks: Saigon Commercial Joint Stock Bank, Vietnam Tin Nghia Commercial Joint Stock Bank and De Nhat Commercial Joint Stock Bank), depositors were afraid of losing money. Therefore, they divided their money into deposits in many different banks to ensure their money sources, because according to the Law on Deposit Insurance, only a maximum payment of 50 million VND is paid, even if the deposit of 100 billion VND is only paid 50 million VND.

Although the capital mobilized into the banking system has changed recently, the increase is quite low . Capital mobilization in the first 7 months of the year of local banks is estimated at 860,000 billion VND, up 17% compared to the end of 2010 and up 27.2% compared to the same period. Of which, mobilization in VND increased by 7.18%, in foreign currency increased by 3.33%. Total outstanding loans of commercial banks in the locality reached 790,000 billion VND, up 7% compared to the end of 2010 and up 2.13% compared to the same period. Of which, outstanding loans in VND increased by 2.44%, and in foreign currency increased by 19.18%.

According to the State Bank of Vietnam, Ho Chi Minh City branch, the difference in deposit interest rates between VND and foreign currencies (the difference is about 12%/year) is the factor that creates the opposite movement.