In addition to continuously improving the product supply process, to meet the increasingly demanding needs of customers, Techcombank has also implemented many customer care programs, promotions and meaningful gifts for customers: "Lucky every day, billionaire luck", "Happy Tet Techcombank - Huge lucky money" with a special prize of 3.6 billion VND, "Win a Vespa LX from F@st i-bank online banking", "Send to Techcombank, win a Mercedes", "Super prize savings"...

2.3. Vietnam's macroeconomic context .

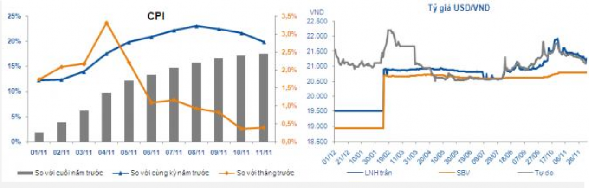

In 2011, facing many adverse impacts from both domestic and foreign sources, inflation and exchange rate instability were the two biggest challenges for the Vietnamese economy. The sharp devaluation of VND and the sharp increase in world commodity prices had a strong impact on the increase in the prices of imported and domestic goods. Along with the delayed impact of the loosening of monetary policy in the second half of 2010 and the policy of managing prices of essential goods such as electricity and gasoline according to market mechanisms, inflation in the first months of the year increased sharply and was always above 1.5%/month.

Chart 2.21: CPI and USD/VND exchange rate fluctuations in the second half of 2011

Currency market developments:

VND Market:

VND mobilization faces many difficulties, causing interest rates to increase: Due to the impact of the tight monetary policy, many banks have faced liquidity difficulties, causing interest rates in the interbank market as well as the residential market to increase sharply. VND mobilization interest rates were sometimes pushed up to 18-19% to attract depositors.

Slow growth in VND credit: In addition to liquidity difficulties of some banks causing limited credit supply, increasing mobilization interest rates pushing lending interest rates beyond the tolerance of businesses is one of the reasons.

causing credit growth to slow down compared to the end of 2010. On the other hand, under pressure from the credit growth ceiling, some banks that boosted credit from the beginning of the year experienced a situation of excess capital but could not disburse more.

In addition to the high interest rate that makes businesses not interested in borrowing from banks, the slow credit growth is also partly due to economic difficulties, slow consumption of goods, and high inventories, causing many businesses to go bankrupt or have to downsize. In the first 9 months of 2011 alone, the number of bankrupt or dissolved businesses was estimated at 4,700. Difficulties in production and business have caused many businesses to be unable to pay their debts. The bad debt ratio of the banking system at the end of August 2011 was over 3%, equivalent to about 76,000 billion VND, of which debt with the possibility of losing capital accounted for 37,000 billion VND.

Foreign exchange market:

Along with the monetary tightening policy, in 2011, the State Bank also took strong and decisive actions to limit the dollarization of the economy, thereby stabilizing the exchange rate. Specifically, in addition to tightening the inspection and handling of foreign currency trading on the free market,

Gold market:

2011 witnessed unpredictable fluctuations in world gold prices, which significantly affected domestic gold prices.

In the first 6 months of 2012, the capital market has had significant improvements compared to

with 2011.

Interest rates continue to fall across all markets

In the capital mobilization market, the interest rate of issuing Government bonds has been gradually regulated in a downward trend and continues to be oriented to reduce the general interest rate level of the whole market. As of June 21, 2012, the interest rate of issuing Government bonds has decreased by about 2.6 - 3% compared to the beginning of 2012.

In the market for mobilization from economic organizations and individuals, since the beginning of the year, the State Bank has adjusted the ceiling interest rate for mobilization four times, accordingly, the maximum deposit interest rate in VND for demand deposits and deposits with terms of less than 1 month has decreased from 6%/year to 2%/year, for deposits with terms of 1 month or more has decreased from 14%/year to 9%/year;

Interbank lending rates fall sharply to low levels

highest in recent years at most maturities.

With the current downward trend in interest rates on government bonds, the pressure on issuing government bonds will be reduced, creating conditions for reducing government bond interest rates, thereby contributing to the direction of reducing general interest rates in the market.

Stable Forex Market

The VND/USD exchange rate has remained stable since the beginning of the year. However, the exchange rate is forecast to increase in the coming time due to the continuous decrease in VND deposit interest rates and the possibility of further decrease, causing the VND to depreciate against the USD.

Total system assets decrease and bad debt increases

According to the State Bank, as of April 30, 2012: total credit in the entire system was

2,617,320 billion VND, down 0.59% compared to the end of 2011. The main reasons still come from: (i) the problem of business inventories has not improved much, so commercial banks are cautious in disbursing due to concerns about bad debt; (ii) the interest rate level is still high compared to the needs of businesses (75% of businesses accept a loan interest rate of 14% - 15%) while very few businesses can meet the conditions to borrow at preferential interest rates.

Total mobilization from residents and enterprises continued to increase slowly while total assets of the entire system tended to decrease. Bad debt of the entire credit institution system as of April 2012 was about 108.6 trillion VND, an increase of 28.18 trillion VND (35%) with an average growth rate of 8.6%/month, higher than the average growth rate of the same period in 2011.

2.4. Applying the SWOT model to evaluate the competitive capacity of Vietnam Technological and Commercial Joint Stock Bank (TECHCOMBANK)

In its strategy to enhance its competitiveness, Techcombank has gradually reformed the bank comprehensively in terms of corporate governance, risk management in developing products and services according to international standards, especially investment in technology. Techcombank's competitiveness can be evaluated in general through the SWOT model as follows:

Table 2.4: SWOT model

Strengths (S)

- Institutions, regulations, risk management, recruitment

increasingly reasonable and effective use

- Increasingly prestigious brand

- Products, credit services, foreign exchange, money

competitive international currency and payments

- Advanced technology supports product development and delivery and risk management

- Network, market share, and relative reputation

good in the north and central south

- Healthy, stable and effective finance

high business

- Young, dynamic, well-trained staff, fluent in foreign languages

Weakness (W) - Not yet strong in Ho Chi Minh City - the largest market in the country - Thin staff, lack of staff to meet requirements network growth rate - Management and administration work has not been achieved. modern international banking standards - Low charter capital, weak reputation compared to leading competitors - Credit risk assessment system not yet really effective | |

Opportunity (O) - Redistribute the market share bank - Develop the right market and business sector business advantage | Challenge (T) - Possibility of further reduction in interest rate ceiling - Permitted credit growth scale narrow - Credit demand decreased - The problem of bad debt has no solution - Pressure to improve financial capacity - Restructuring pressure - Competition from foreign investors |

Maybe you are interested!

-

Usd/vnd Exchange Rate Developments During 11/26/2008 – 01/23/2009

Usd/vnd Exchange Rate Developments During 11/26/2008 – 01/23/2009 -

The impact of interest rate and exchange rate fluctuations on profitability and stock return fluctuations at Vietnamese commercial banks - 9

The impact of interest rate and exchange rate fluctuations on profitability and stock return fluctuations at Vietnamese commercial banks - 9 -

Research Results on the Relationship Between Exchange Rate Level and FDI Capital in Vietnam and Discussion

Research Results on the Relationship Between Exchange Rate Level and FDI Capital in Vietnam and Discussion -

Forecast of Population Growth Rate, GDP and CPI According to Scenarios to 2020 Average According to Stages, %.

Forecast of Population Growth Rate, GDP and CPI According to Scenarios to 2020 Average According to Stages, %. -

Hedging exchange rate risks at Mekong Delta Housing Development Bank, Hanoi branch - 16

Hedging exchange rate risks at Mekong Delta Housing Development Bank, Hanoi branch - 16

2.4.1. Opportunities and challenges

2.4.1.1. Challenges

Possibility of further reduction of interest rate ceiling: According to the Resolution of the National Assembly as well as the general policy of the Government and the State Bank, monetary policy in 2012 will continue to be closely oriented but will gradually reduce interest rates to remove difficulties for businesses. Therefore, when inflation in recent months has been on a downward trend, the possibility of reducing the interest rate ceiling early next year is entirely possible. Using administrative orders to force banks to only mobilize capital at interest rates not exceeding the ceiling is probably only a temporary solution, difficult to maintain in the long term, in other words, this is a solution that is not market-oriented. However, in

In the current context, the State Bank still needs to use this strong solution to achieve larger economic goals. Accordingly, this will be one of the important reasons why banks continue to face difficulties in attracting VND deposits. In addition, the cautious monetary policy also limits the money supply to the market, significantly affecting the liquidity of the entire system in general and Techcombank in particular .

Limited credit growth scale: Also according to the orientation of the State Bank, the credit growth target in 2012 is likely to be only 15-17%, if not counting 2011, this is the lowest level since 2003, in the face of the domestic economic situation facing difficulties, the slow credit growth situation may continue into the following years. In reality, the credit growth of the whole system is currently at a very low level when the whole year is estimated to only reach about 12-13% compared to the end of the previous year, so the total credit growth scale allowed to increase in 2012 for banks calculated on this figure will be quite limited.

In addition, the State Bank also issued a policy requiring all credit institutions to reserve 20% of total outstanding loans for the agricultural and rural areas. Techcombank, one of the banks that does not have an advantage in this area, will have to transfer an equivalent amount of capital to Agribank for disbursement. Thus, although this regulation has a very positive effect on the economy in general and the agricultural production area in particular, it may be a disadvantage for Techcombank, which has the ability to earn higher profits from disbursing the above capital to other areas.

Decreased credit demand: The world and Vietnamese economies in 2012 are forecasted to face many difficulties, causing people to tighten their spending, and decreased consumer demand, indirectly affecting the demand for banking services. In addition, decreased consumer demand also causes businesses to continue to reduce production or operate at a low level. Thus, production credit demand and consumer credit demand in 2012 are expected to be narrowed, new credit is quite limited while banks are thoroughly recovering bad debts, and Techcombank's credit segment profits are not expected to grow strongly.

The problem of bad debt has not been solved: Bad debt and bad debt handling will continue to be a hot issue in 2012 and the following years when the actual bad debt ratio is said to be much larger than the level of over 3% of total outstanding debt announced by the State Bank of Vietnam at the end of August 2011. In August 2012, according to the report of the Governor of the State Bank of Vietnam to the National Assembly, the ratio

The actual bad debt ratio is over 8%, while Fitch announced that Vietnam's bad debt in VND at the end of June 2012 was about 13% of total outstanding debt. In addition, from April 1, 2012, the State Bank will officially and regularly announce 5/12 operational safety indicators of the banking system including CAR, ROA, ROE, bad debt ratio and outstanding debt ratio in each sector. Accordingly, the official disclosure of the bad debt ratio of the entire system may have certain impacts on people's confidence in the safety of the banking system. Currently, in addition to the available provisions at banks in general and Techcombank in particular, the issue of bad debt handling still has no specific solution and will be an important factor affecting the restructuring process of the banking system now and in the future in the coming years.

Pressure to improve financial capacity : The policy of improving financial capacity and operational efficiency of the Vietnamese banking system was initiated from Decree 141/2006/ND-CP when the Government set out a roadmap to increase the legal capital of banks to 3,000 billion VND by 2010. In addition, the roadmap to increase legal capital to 5,000 billion VND by 2012 and 10,000 billion VND by 2015 is also under consideration for application. Along with this process, the State Bank of Vietnam has also continuously issued regulations requiring banks to improve operational safety standards and liquidity such as Decision 493/2005/QD-NHNN on general and specific provisions, Circular 13 and Circular 19 in 2010 setting out standards on CAR, credit granting ratio, etc. The implementation of the above regulations has exposed many weaknesses of the Vietnamese banking system when not all banks meet the requirements of the State Bank of Vietnam on time, some documents have had to be amended or postponed to create conditions for banks to comply with the regulations. Although many targets in the regulations set by the State Bank have always been achieved, in the context of deep economic integration, in the coming years, there will certainly be more foreign banks entering the domestic market, so improving financial capacity is a significant pressure for Techcombank.

Restructuring pressure : Many shortcomings of the banking system have been revealed in recent times, weak liquidity along with high bad debt risking the safety of the system, making restructuring and reforming the entire financial system, of which the most important is the banking system, an urgent issue and difficult to delay any longer. The State Bank also expressed its desire to restructure the system.

Banks passed many important policies in 2011 to accelerate the restructuring process. The pressure to merge banks reached its peak in 2011 and early 2012 when many banks faced serious liquidity difficulties and were in dire need of money to repay debts. The State Bank of Vietnam also had a legal framework for bankruptcy and bank mergers through the issuance of Circular 34/2011/TT-NHNN on the procedures for revoking licenses and liquidating assets of credit institutions. Thus, the internal weakness of banks leading to the pressure to restructure is posing a challenge for these organizations with two options: either finding a merger partner to improve financial capacity or accepting dissolution.

After LienVietBank and VPSC, the recent merger of three banks Ficombank, SCB and Tinnghiabank is the second merger in the banking industry but the first in the restructuring roadmap of the Vietnamese banking system set by the State Bank. After the merger, the newly established bank will have total assets estimated at over VND150,000 billion with a charter capital of about VND10,600 billion and over 200 branches and transaction offices. Accordingly, the charter capital of the newly merged bank will be equivalent to Eximbank and larger than some large domestic joint stock commercial banks such as ACB, MB, Sacombank and Techcombank. Thus, restructuring the banking system, in addition to creating pressure to merge or dissolve weak banks, this process also creates new banks after the merger and may become a new competitive challenge for Techcombank in the future.

Competition from foreign investors: Although the restrictions on foreign banks (charter capital, total assets, operating term, form, and field of operation) were removed in 2011 according to the roadmap after Vietnam joined the WTO, due to the difficulties of the world economy, the development level of foreign banks in 2012 was still limited. It is expected that the explosive growth and fierce competition in areas such as retail banking, trade finance, capital trading, and foreign currency of foreign banks will continue from 2013 onwards .

2.4.1.2. Opportunity

Redistribute the market share to banks:

The economic restructuring process, including restructuring of state-owned enterprises, restructuring of the banking system and restructuring of public investment, is expected to take place strongly.

in the coming years. This process is both a challenge and also creates many opportunities for acquiring cheap assets and diversifying investments of banks with healthy financial status.

The challenge of weak banks being acquired by mergers and acquisitions is also an opportunity for Techcombank to participate in acquiring other banks to improve financial potential and quickly expand its network of operations and customer base .

Opportunities for Techcombank to develop to its strengths:

On the other hand, the restructuring process can also be a positive factor for Techcombank to develop in the right market and business areas where it has advantages. The current market has little clear distinction between banks (weak banks and small banks). Therefore, when Techcombank can truly promote its strengths in its right business areas instead of investing widely in the race to develop similar products like in the market, this is an opportunity to affirm its name and stand firm in the restructuring battle + the entire system of these banks .

2.4.2. Strengths and weaknesses

2.4.2.1 Strengths

Institutions, processes, risk management, and recruitment are increasingly reasonable and effective.

The institution is specifically decentralized, from the Council to the affiliated departments/offices and the delegation of authority is transparent. Each individual and collective is assigned certain authority, appropriate to the field of participation and accompanied by the responsibilities of the work undertaken.

Risks in banking operations are inevitable and therefore, to ensure optimal business performance, the bank's risk management capacity must be good. With such a consistent and thorough view of Teccombank on the importance of risk management, in 2011 Techcombank developed the Credit and Risk Management division, continuing to mark a new development in this work, especially the development in credit risk management, which has always been identified as the main risk that needs to be strictly controlled by Techcombank.

The establishment of the Credit and Risk Management Division with the advice of HSBC is considered a complete step in the development of the organizational structure for Techcombank's risk management. With the establishment of the division, risk management and risk