VND/month, currently raising 2 small children and 1 elderly mother, the deduction is 4.8 million VND, thus, taxable income is 15.2 million VND, the tax payable is 2.28 million VND/month, lower than the lump-sum tax rate currently applied according to the Law on Corporate Income Tax.

Thus, for low-income business households and the number of dependents for the business registrant, the tax payable will be lower. This is a very beneficial point for business individuals in comparison with the tax they are currently subject to.

The budget revenue from individual businesses may decrease, but this is a measure to encourage and motivate small businesses to become large enterprises, thereby contributing more, more stably and firmly to the state budget. This is one of the policies that reflects the Party and State's viewpoint of easing the burden on the people, which is specified in the personal income tax incentive policy. Moreover, the transfer of individual businesses to pay personal income tax is also completely consistent with international practice when Vietnam becomes a member of the World Trade Organization (WTO).

Advantages of implementing the Personal Income Tax Law for individual business entities.

Firstly , for many years now, business individuals have been paying taxes according to the law, so their awareness of tax obligations has become a habit and routine, so switching to paying personal income tax for them is simply a matter of changing the name of the tax, not much disruption. This is the most fundamental and basic advantage.

Maybe you are interested!

-

Personal income tax law from practice in Thai Binh province - 11

Personal income tax law from practice in Thai Binh province - 11 -

Implementing the application of personal income tax law in Vietnam - 15

Implementing the application of personal income tax law in Vietnam - 15 -

Tax Administration Law on Tax Audit, Tax Inspection and Handling of Violations of Personal Income Tax Law

Tax Administration Law on Tax Audit, Tax Inspection and Handling of Violations of Personal Income Tax Law -

Basic Orientations in Perfecting Personal Income Tax Law in Vietnam

Basic Orientations in Perfecting Personal Income Tax Law in Vietnam -

Practical implementation of personal income tax law in Quang Ngai province - 10

Practical implementation of personal income tax law in Quang Ngai province - 10

Second, the process of tax management, especially tax management for business households, the tax sector often receives close coordination from state management agencies, local authorities, organizations and unions; especially the enthusiastic and responsible support of the commune and ward tax advisory council, has created many favorable conditions for tax authorities in determining

Sales, expenses, income, tax collection management, urging and enforcing tax debt collection.

Third , the actual tax management process has given the staff of civil servants directly managing business households the advantage of understanding each unique characteristic of this subject. From here, many localities have had initiatives and effective management measures, which have been replicated and summarized into common experiences of the entire tax sector.

Fourth , the tax sector has been promoting the application of information technology (IT) in tax management in general and tax management for individual businesses in particular. These applications have helped tax authorities better control taxpayers, tax bases and monitor tax collection progress. In particular, to implement the Law on Personal Income Tax, the tax sector has developed many projects to apply IT in management, so efficiency will certainly be guaranteed.

Difficulties in implementing the Personal Income Tax Law for individual business entities.

As an inherent characteristic, the majority of business individuals do not implement the invoice and voucher accounting regime , and if they do, they do not comply with regulations, so accurately determining the business turnover of this group is a big challenge.

According to the regulations in the tax collection management process for individual business households (currently business individuals - new taxpayers of the Personal Income Tax Law) issued under Decision 1201 QD/TCT-TCCB dated July 26, 2004 of the General Department of Taxation in Section b, Point 1, Section I, Part B for tax stabilization households on actual revenue investigation: "The tax team selects a number of business households representing industries and business scales for typical investigation as a basis for assessing the accuracy of declarations self-declared by business households and as a basis for negotiating with business households that declare incorrect revenue or determining tax for business households that do not declare or submit declarations".

Most of the stable taxable revenue for business households is not adjusted to keep up with the increase in market prices. Tax authorities understand this, but to make timely adjustments, they must go through the step of investigating and surveying the actual revenue of the business households. In fact, when making a revenue declaration, business households often respond by declaring lower than the actual revenue, even declaring lower than the revenue that was stabilized for tax in the previous period. Therefore, investigating and surveying taxable revenue in the process of tax management for individual production and business households is not a simple task.

In practice, managers must perform their duties within a certain period of time and according to regulations in each investigation and survey to adjust the tax rate to suit the business reality. Therefore, the investigation and survey of actual revenue becomes a difficult task, especially for businesses operating on the streets. Normally, the tax authority receives a number of revenue declarations from business households and among them, there are many declarations of revenue that are too low compared to actual production. Some business households that do not prepare and submit declarations said that when they received the declarations from the tax authority, they knew that there would be an adjustment of the tax rate to be paid, so they waited and did not declare in a hurry. Moreover, business households usually only focus on the tax rate to be paid, paying little attention to taxable revenue, so when they have to declare their revenue, they are worried and find ways to declare incorrectly the revenue achieved in business.

The process of implementing this work has shown some experiences: For some industries that can be specifically calculated such as food and beverage, services..., managers can quickly conduct sales investigation operations. For some service industries that use grid power, managers need to grasp the corresponding revenue on the number of kw/hour of electricity such as milling, mechanical processing, manufacturing of consumer goods... For the type of

Entertainment service businesses such as karaoke, billiards, internet, video games... need to base on average operating hours to survey revenue. As for commercial business households, managers must have a firm grasp of the business forms such as wholesale and retail; supply sources of goods; regular customers, business conditions and actual purchasing power of each group of goods through surveys of households in the same industry, through consumer opinions... to have appropriate revenue adjustments.

On the other hand, tax teams must strengthen coordination with the economic information synthesis department that provides import and export documents of enterprises and business households using invoices and documents, thereby being able to predict the actual revenue of business households. A necessary and equally important task that effectively supports the investigation of actual revenue is to publicly post the expected revenue of business households at appropriate locations, then publicly announce the posting location so that business households know and participate in giving opinions, helping tax authorities have more basis to determine the revenue of households that is unreasonable, not in accordance with actual production and business in order to make adjustments.

The investigation and survey of actual revenue to calculate taxes is not a simple task for managers of individual business households. If this task is not properly invested in and implemented in accordance with the correct legal processes and procedures, it will encounter many difficulties, especially when having to recalculate tax rates to prepare for a new tax stabilization period for business households. Therefore, to do this task well, managers must constantly train their ideology, ethics, lifestyle, be dedicated to their profession and have the spirit of learning and improving their professional skills, ensuring close contact with the grassroots, in order to stabilize revenue sources and establish social justice.

In the condition that cash payment is still the main method of economic transaction in our country, and is even more popular for business households, controlling the arising revenues is not easy.

In addition, the management of family circumstances for business individuals is also more complicated than that of salaried employees . Because while the political and economic interests of salaried employees are relatively closely tied to the employer, for business individuals, all potential interests are not tied to any organization, and if there is a connection, it is very loose, so there may be many cases of dishonest declaration of family circumstances and dependents. In addition, in reality, there is a large number of business households that do not have a business registration, so the legal basis for determining the subject and tax management is also very difficult to find.

Many individual business households employ relatives such as parents, children, etc. to help with the business in a labor-for-profit manner, but they are not entitled to family deductions, except in the case of minor children. The remaining cases, although not considered dependents, are still included in the business expenses to be deducted when determining taxable income. If the business household implements the invoice and voucher accounting regime and has a labor contract, the determination of expenses is based on the accounting books and labor contracts. If accounting and labor contracts are not implemented, the rate of fixed income as prescribed by the tax authority will be implemented.

6. TAX PAYMENT DEADLINE

On February 6, 2009, the Ministry of Finance issued Circular No. 27/2009/TT-BTC, guiding the implementation of the extension of the deadline for paying personal income tax until the end of May 2009 after many difficulties, not being prepared in time to implement the tax law as well as the impact of objective factors such as the world economic crisis. This Circular takes effect after 45 days from the date of signing, February 6, 2009.

and applies to income arising from January 1, 2009, i.e. income from 2008 is still subject to personal income tax as usual.

Accordingly, the subjects eligible for deferment of personal income tax payment are resident individuals with taxable income from business; income from salaries and wages; income from capital investment; income from capital transfer (including securities transfer); income from royalties; income from franchising.

-- These incomes are directly related to production and business; in addition, there is income from inheritance; income from receiving gifts. Non-resident individuals with taxable income from capital investment, capital transfer (including securities transfer); income from royalties; income from franchising are also subject to deferment of personal income tax payment.

Subjects not eligible for tax deferral include resident individuals with income from real estate transfers; winnings (lottery, gambling); receiving inheritances; gifts; and non-resident individuals (including those not present in Vietnam or leaving Vietnam before June 30, 2009) with taxable income from business, salary, wages, real estate transfers, winnings, receiving inheritances, receiving gifts. If tax is payable, the contribution of these revenues only accounts for 20% of the total revenue from personal income tax to the budget.

The tax payment deferral period is from January 1, 2009 to May 31, 2009. After that, the continued deferral or payment of personal income tax after that time will be considered by the National Assembly at the 5th session taking place in May 2009. However, for now, taxpayers still have to declare, calculate and pay taxes, but that tax will be refunded to income earners.

In mid-April 2009, the Ministry of Finance submitted to the Government a plan to exempt and reduce personal income tax in 2009. The specific plan has not been disclosed, but the exemption and reduction levels are designed to benefit the majority of the population (meaning that taxable income can be exempted for up to 6 months or 7 months).

The first month of the year, the rest is considered for reduction. In addition, the exemption and reduction levels are also based on the actual income of the people, in which people with low income are exempted or reduced a lot; people with high income may only be reduced but not exempted.

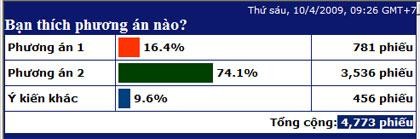

Previously, the Tax Authority proposed two options for exemption and reduction of personal income tax:

Option 1: Exempt tax for the first 5 months of the year for all types of income eligible for extension. For the last 7 months of the year, reduce tax by 100,000 VND per month for those with income from salaries, wages, and income from business activities.

Option 2: Exemption of tax for the first 6 months of the year for all types of income that are eligible for extension. The remaining 6 months of the year continue to exempt tax for income from royalties, franchises, income from inheritance, and securities gifts. For taxable individuals with income from salaries, wages, and business income, the tax will be reduced by 200,000 VND per month.

According to the Ministry of Finance's calculations, if option 1 is implemented, in 2009 the state budget will reduce personal income tax revenue by about 5,200 billion VND. If option 2 is implemented, the state budget will reduce revenue by about 6,700 billion VND. Thus, if option 2 is implemented, personal income tax revenue in 2009 will decrease by about 46% compared to the revenue approved by the National Assembly and the budget revenue will decrease by an additional 1,500 billion VND compared to option 1. The Ministry of Finance is leaning towards option 2 because it seems more reasonable in the context of economic crisis and people's difficult lives. According to a statistic, out of 4,773 comments sent to VnExpress.net, 74.1% agreed with option 2. 7

However, the final plan still has to wait for the opinions of National Assembly deputies in the meeting in early October and the 5th session of the National Assembly opening on May 20.

7 VnExpress.net April 09

6.1 Purpose of deferring personal income tax payment.

Tax deferral is to stimulate consumption

The tax deferral for all subjects will cause the budget to lose about 1,000 billion VND each month, significantly affecting the budget revenue, but this will stimulate consumption, supporting people to have more spending to overcome the current difficult situation. Even the income of singers is temporarily not subject to personal income tax because when the economy declines, shows also decrease. In short, the purpose of tax deferral is to supplement revenue.

According to economic experts, the decision to defer personal income tax payment is in line with the measures we are currently implementing to stimulate demand, especially consumer demand. The point is whether the deferral of tax payment really stimulates consumption as desired? As in the case of the US, of course, it is not entirely true for the situation in Vietnam, but it is also an experience to consider. President-elect Obama decided to spend 300 billion USD on reducing personal income tax in the next two years (while in Vietnam, the deadline for paying personal income tax has only been temporarily extended). Some economists believe that reducing personal income tax will not be effective because consumers tend to save part of the reduced tax amount, especially when the tax reduction is only temporary. Therefore, the spillover effect of this measure is not high. Some studies on the mid-2008 tax refund in the US show that a very large part (80%) of the tax refund was saved by people instead of spent, significantly reducing the effectiveness.