- Agreed interest rate mechanism: applied either only to lending, or both lending and mobilization.

- LSCB mechanism: includes two forms: (i) mandatory: lending interest rate, mobilization interest rate must not exceed 150% of LSCB; (ii) orientation: for guidance and reference only.

- TLSCV and/or TLS mechanism;

- TLSCV mechanism combined with LSCB.

The Civil Code promulgated in 1995, Clause 1, Article 473, then the Civil Code amended in 2005 with Clause 1, Article 476 stipulates that the lending interest rate between the borrower and the lender must not exceed 150% of the lending interest rate announced by the State Bank. However, it was not until May 2008 that the State Bank issued Decision No. 16/2008/QD-NHNN dated May 16, 2008 regulating the lending interest rate management mechanism, followed by Decision No. 1099/QD-NHNN on lending interest rate, which opened a series of decisions on lending interest rate for the following months, culminating in Decision 1317/2008/QD-NHNN dated June 10, 2008 with the Vietnamese Dong lending interest rate of 14%/year, effective from June 11, 2008 to October 20, 2008. The LSCB played the role of the LSCS until March 2011. On March 3, 2011, the State Bank issued Circular 02/2011/TT-NHNN stipulating the LTM of 14%/year, effective from March 3, 2011. Short-term LTM played the role of the LSCS tool until now. In addition, in 2012, the State Bank also regulated the TLSCV, forcing credit institutions to lower lending interest rates, encouraging businesses and individuals to borrow to expand production and consumption activities, stimulating aggregate demand.

Despite the effective use of the tools of LSCB, TLS, TLSCV, the SBV's sudden increase in LSCB and urgent reduction with large amplitude in a very short period of time, especially in 2008 and 2012 (Appendix 6), made it difficult for credit institutions to manage capital sources and decide on appropriate business interest rates. Some credit institutions looked back and forth to decide on mobilization interest rates and lending interest rates. Small credit institutions often mobilize high interest rates to avoid the movement of deposit flows leading to loss of liquidity. In addition, businesses are passive because they do not have time to prepare capital sources and have not had time to adjust their plans.

production and business. The rapid decrease in interest rates has made credit institutions struggle to find outlets for the capital mobilized at high interest rates in the past. Depositors find it difficult to make investment decisions because when interest rates increase, they expect further increases and when they decrease, they do not know how much and when they will decrease. It would be better to have a forecast of interest rate trends with a high level of reliability so that credit institutions and the public are not surprised in their business and investment activities. In general, the recent change in interest rates in a short period of time has also affected business operations, specifically:

- Requires continuous adjustment of credit contracts between credit institutions and enterprises, mainly in terms and interest rates.

- The movement of savings/payment flows of businesses and individuals from places with low interest rates to places with high interest rates.

- When interest rates are high, some businesses tend to deposit money in credit institutions to earn interest, especially during times of capital difficulties or difficulty in selling products. Furthermore, when lending rates are high, the pressure of borrowing costs weighs heavily on business operating costs, leading to some businesses being unable to pay high borrowing costs.

The increase or decrease of the interest rate depends on the economic situation, the law of supply and demand and the socio-economic development goals. However, the effectiveness of fighting inflation or deflation depends on the public's confidence in the banking and financial system. A correct and effective interest rate policy will strengthen the confidence of the public and investors, production and business, and vice versa, the operational efficiency of the banking system and financial institutions is an important factor in influencing the effectiveness of implementing monetary and financial policies.

3.1.7 Progress of the interest rate management mechanism of the State Bank of Vietnam

Appendix 7 shows through the Gantte diagram the basic milestones in the interest rate management mechanism of the State Bank in the period of 1995 - 2015 for the Vietnamese Dong (VND). Through this Gantte diagram, some observations can be drawn as follows:

+ At some points in time, the interest rate policy was not fully regulated. From January 1998 to August 2000, the State Bank applied the basic interest rate as TLSCV but did not mention the mobilization interest rate. In fact, the mobilization interest rate was flexibly applied by commercial banks. In the period from February 2008 to January 2009, the State Bank applied the compulsory lending interest rate (from February 2008 to May 2008) and the compulsory lending interest rate (from May 2008 to January 2009) but did not mention the lending interest rate. It was not until January 23, 2009 that the State Bank issued Circular 01/2009/TT-NHNN effective from February 1, 2009 regulating lending interest rates according to the agreement mechanism.

+ Some periods when the State Bank changed the interest rate tool were too short, such as from February 2008 to May 2008 (3 months), the State Bank applied the compulsory interest rate and then switched to the compulsory interest rate; or in May 2012, the State Bank applied the interest rate equal to the compulsory interest rate plus a margin of 3%, then switched to the interest rate of 13%/year from June 11, 2012. And also starting from June 11, 2012, the State Bank used both the interest rate and the interest rate corridor for credit institutions/commercial banks to conduct capital mobilization and lending activities.

The State Bank has implemented many different interest rate management mechanisms such as the TLSCV management mechanism; TLSCV combined with LSCB; TLS; LSCB, and the negotiated interest rate mechanism. The choice of which interest rate is the fixed LSCS in the State Bank's interest rate management mechanism seems to be left open due to the unsustainable nature of Vietnam's financial system and the products of the money market are still too few and not strong enough to control the economy, as shown by the domestic shocks caused by the financial and monetary crises in the world in 2008 and 2011. This is an issue that needs to be analyzed to clarify the interest rate management mechanism of the State Bank in recent times. Analyzing the current state of the State Bank's interest rate policy using the Taylor rule helps to clarify the role of the State Bank's operating interest rates and to indicate which interest rate is most suitable for the Taylor rule.

3.2 Analysis of the current interest rate policy of the State Bank of Vietnam using the Taylor rule

3.2.1 Conventional calculation method with default coefficients

The author uses formula (1.5) i t = π* + r* + β π (π t – π*) + β y (g t – g*) to calculate the proposed LSCS level by the Taylor rule according to Billi (2011) and compares it with the interest rates of the State Bank to conclude the consistency between the Taylor rule and the actual interest rate policy in Vietnam. The data and implementation steps have been presented in chapter 2 of the thesis.

3.2.1.1 Analysis of interest rate policy by year

TAYLOR TAYLOR

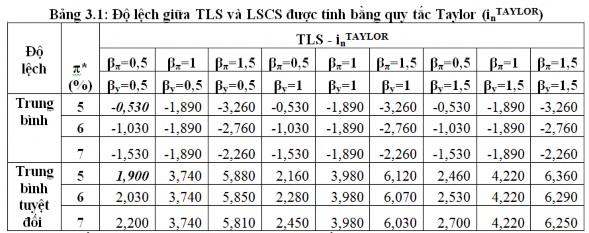

The deviation between the interest rates (years) of the State Bank and the LSCS (years) according to the Taylor rule (5) (i n ) is calculated according to the formula: Deviation = i t – i n at the target inflation rates (CPI) of 5%, 6% and 7%/year with the coefficient pairs (β π , β y ) taking fixed values that are multiples of 0.5 in the range of values [0.5; 1.5], specifically 0.5, 1 and 1.5. The absolute mean value is the average value of the absolute values (>0) of the deviations. The calculation results show that the TLS is relatively close to the LSCS level according to the Taylor rule (i n TAYLOR ) with the coefficient pair (β π =0.5, β y =0.5) (Appendix 9, 10, 11). Table 3.1 summarizes the results of the deviations between TLS and LSCS calculated from the Taylor rule.

Source: Author's calculation from macroeconomic data for the period 2000-2014 Table 3.1 shows the deviation between TLS and LSCS calculated using Taylor rule

per year ( in TAYLOR ) at inflation target levels of 5-7%/year with coefficient pairs (β π ,

β y ) takes on the values of 0.5; 1 and 1.5. The results in Table 3.1 show that the average deviation and the absolute average deviation between TLS and LSCS calculated by the Taylor rule (in TAYLOR ) of the coefficient pair (β π =0.5, β y =0.5) with the target inflation rate of 5%/year have

TAYLOR

lowest difference (smallest absolute value). This is the pair of coefficients of the Taylor rule (1993) with LSCS values close to the TLS of the State Bank in the period 2000-2014.

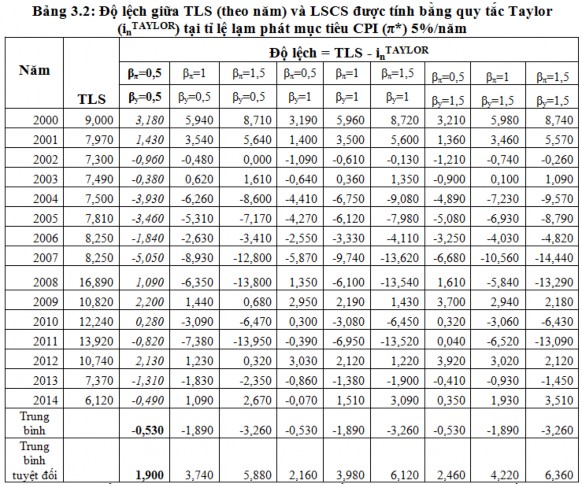

Table 3.2 details the deviation between TLS and i n by year at the target inflation rate (CPI) of 5%/year as a basis for analyzing the SBV's interest rate policy.

Source: Author's calculation from macroeconomic data for the period 2000-2014

From the Taylor rule analysis based on the annual data in Table 3.2, the author makes some comments on the interest rate policy of the State Bank:

- Period 2000 - 2001: The State Bank used the interest rate tool of TLSCV combined with LSCB with TLSCV equal to LSCB plus a margin of 0.3%/month (short term) or 0.5%/month (medium, long term). LSCB is considered as TLS. With a higher TLS level than the LSCS suggested by the Taylor rule in the period 2000 - 2001, the rate

The inflation rate has decreased to a low level, specifically in 2000 it was -0.53% and in 2001 it was 0.79% compared to the inflation rate in 1998 of 9.2%/year 27 . The economic growth rate in 2000 was 6.79%/year and 6.89%/year in 2001. This can be considered one of the bases for the State Bank to implement the negotiated interest rate mechanism since 2002.

- During the period 2002-2007, the SBV's TLS was lower than the proposed LSCS according to the Taylor rule. This shows that the SBV implemented a loose monetary policy with an interest rate mechanism agreed between borrowers and lenders. At the end of 2007, the financial crisis in the US occurred and in 2008 affected Vietnam. The inflation rate of our country increased to 19.89%/year (in 2008) compared to 12.75% in 2007, forcing the SBV to tighten monetary policy by applying the basic interest rate.

- The sharp decrease in the difference between TLS and in TAYLOR in recent years

TAYLOR TAYLOR

2008 and 2009 and the positive deviations show the SBV's efforts to control inflation. As a result, the inflation rate decreased significantly to 6.52% in 2009. However, the real GDP growth rate in 2008 was 6.31% and in 2009 was only 5.32%, lower than previous years. In 2010, the SBV's TLS was still higher than i n but the deviation between TLS and i n decreased compared to the deviation in 2009, while the inflation rate was at 11.75%/year, GDP growth was 6.78%/year, both higher than in 2009, showing that the SBV's monetary policy is inclined to stimulate economic growth. However, the inflation rate in the fourth quarter of 2010 increased to 11.75%/year, opening the way for high inflation and economic recession in 2011.

- In 2011, the SBV's TLS was not high enough to control inflation as suggested by the Taylor rule. As a result, the inflation rate increased to 18.13%/year and the real GDP growth rate only reached 5.96%/year.

- In 2012, although the inflation rate decreased to 6.81%/year, the State Bank still maintained a tight monetary policy, reflected in positive deviations and the GDP growth rate only reached 5.03%, lower than the 5.96% of 2011.

- In 2013, 2014, TLS was lower than in TAYLOR and this is only

In addition, the State Bank of Vietnam applied loose monetary policy to stimulate economic growth. The results showed that

27 Data from General Statistics Office of Vietnam (www.gso.gov.vn)

It can be seen that the GDP growth rate is higher than in 2012, specifically 5.92% (2013) and 5.98% (2014).

Thus, for Vietnam - a country with a high inflation rate of an average of 7.73%/year in the period 2000-2014, applying the inflation deviation coefficient of 1.5 (coefficient pair β π = 1.5, β y = 0.5) is not appropriate because the LSCS calculated according to the Taylor formula (1.5) has a higher value than the LSCS of the State Bank in the period 2000-2014 and in fact, the State Bank has effectively controlled inflation in this period, especially in the two years when the Vietnamese economy had high inflation, 2008 (deviation was -13.8) and 2011 (deviation was -13.95). When interest rates become too high, it will strongly affect consumption and investment, because when credit is limited, spending on consumption and investment decreases sharply. Businesses are concerned about unprofitable business, so they do not develop production and goods become scarce. The decrease in supply of goods continues to put pressure on inflation. That explains why some central banks are cautious when applying the principle of "high interest rates to fight high inflation". Lee and Crowley (2010) conducted an assessment of the monetary policy of the European Central Bank (ECB) in 12 member countries of the common currency area (excluding new members Slovenia, Cyprus, Malta and Slovakia) in the period 1999 - 2009, using the original Taylor rule (1993) and found that for key member countries such as France and Germany, the ECB's monetary policy was close to the LSCS level suggested by the original Taylor rule. In contrast, for Greece and Ireland, two countries with relatively high inflation rates in the early years of the assessment period, the ECB's monetary policy was considered too loose compared to the LSCS level suggested by the original Taylor rule.

3.2.1.2 Quarterly interest rate policy analysis

Appendix 3 on the interest rate policy shows that the SBV has changed the interest rate policy continuously in 2008 and the interest rate policy monthly and/or quarterly in the period 2010-2014 to control inflation and maintain economic growth. Analysis of annual data allows to sketch an overview of the interest rate policy. However, to better understand the SBV's interest rate policy through the lens of the Taylor rule, it is necessary to use quarterly data.

TAYLOR

In general, the results of determining LSCS by Taylor rule with quarterly data (i q TAYLOR ) are similar to the results with annual data, accordingly the average deviation and the absolute average deviation between TLS and LSCS calculated by Taylor rule (i n ) of the coefficient pair (β π =0.5, β y =0.5) with the CPI target inflation rate of 5%/year have the lowest difference (smallest absolute value) compared to other types of interest rates (Appendix 12A, 12B). The summary results are presented in Table 3.3.

Table 3.3: Deviation between interest rates (quarterly) and the Taylor rule LSCS ( i q TAYLOR ) at different inflation targets (π*), 2000Q1-2014Q4

Interest rate

Average value | Absolute mean value | |||||

π*=5% | π*=6% | π*=7% | π*=5% | π*=6% | π*=7% | |

LSTCK | -4.09 | -4.59 | -5.09 | 4.23 | 4.68 | 5.14 |

LSTCV | -2.49 | -2.99 | -3.49 | 2.94 | 3.29 | 3.71 |

LSCB | -2.19 | -2.69 | -3.19 | 2.96 | 3.30 | 3.67 |

TLS | -0.46 | -0.96 | -1.46 | 2.04 | 2.17 | 2.34 |

Maybe you are interested!

-

Perfecting the interest rate management mechanism of the State Bank of Vietnam in the conditions of a market economy - 30

Perfecting the interest rate management mechanism of the State Bank of Vietnam in the conditions of a market economy - 30 -

Applying Taylor rule in the interest rate management mechanism of the State Bank of Vietnam - 28

Applying Taylor rule in the interest rate management mechanism of the State Bank of Vietnam - 28 -

Applying Taylor rule in the interest rate management mechanism of the State Bank of Vietnam - 31

Applying Taylor rule in the interest rate management mechanism of the State Bank of Vietnam - 31 -

Interest rate risk management at Vietnam Joint Stock Commercial Bank for Industry and Trade - 32

Interest rate risk management at Vietnam Joint Stock Commercial Bank for Industry and Trade - 32 -

Basic Theory of Interest Rate Risk Management of Commercial Banks

Basic Theory of Interest Rate Risk Management of Commercial Banks

Source: Author's calculation from macroeconomic data for the period 2000-2014 Through analyzing Taylor's rule (1993) based on quarterly data, the author draws some conclusions.

Comments on the State Bank's interest rate policy:

- Period 2000Q1 – 2001Q4: TLS was always higher than the LSCS calculated according to the Taylor rule (i q TAYLOR ), however the deviation between TLS and i q TAYLOR gradually decreased, indicating that the SBV gradually loosened monetary policy. In 2001, TLS gradually decreased by quarter (Appendix 12A). GDP growth rate in this period was stable at over 6.5%/year (except for the period 2000Q2 when it only reached 4.8%/year) (Appendix 2).

- From 2002Q1 to 2008Q2, the SBV's TLS was always lower than the base rate calculated by the Taylor rule. This shows that the SBV implemented a loose monetary policy. During the period of 2002-2007, the SBV implemented a negotiated interest rate mechanism. On February 26, 2008, the SBV issued Official Dispatch No. 02/CD-NHNN stipulating the base rate of 12%/year, followed by Decision No. 16/2008/QD-NHNN dated May 16, 2008 stipulating the basic interest rate management mechanism to replace the negotiated interest rate mechanism. As a result, from 2008Q3, the deviation between the SBV's TLS and i q TAYLOR was greater than zero, which shows that the SBV implemented a tight monetary policy to control inflation. The inflation rate in 2009 decreased to 6.52% compared to 19.89% in 2008.