CHAPTER 2: OVERVIEW OF MONETARY POLICY

THROUGH INTEREST RATES AND BOND SLIDES AND BANK PROFITABILITY.

2.1. Theory on profitability of commercial banks

Maybe you are interested!

-

Loan Interest Rates in USD Without Collateral

Loan Interest Rates in USD Without Collateral -

Theoretical Basis and Empirical Studies on Brand Valuation of Vietnam's NHTM

Theoretical Basis and Empirical Studies on Brand Valuation of Vietnam's NHTM -

Profitability Ratios

Profitability Ratios -

NHTM's Business Performance Evaluation Indicators

NHTM's Business Performance Evaluation Indicators -

Increasing the Difference Between Lending and Deposit Interest Rates

Increasing the Difference Between Lending and Deposit Interest Rates

The business performance of a commercial bank reflects the ability to use resources to maximize profits with the lowest cost and highest revenue. The business performance of a commercial bank directly determines the existence and development of each bank. An effective commercial bank will increase its reputation and create peace of mind for customers, thereby contributing to increasing capital mobilization and creating increasingly higher profits. Therefore, commercial banks consider business activities as their most important goal.

2.1.1. Operational efficiency of commercial banks

The business performance of commercial banks directly determines the existence and development of the Bank. Depositors will feel more secure if they deposit money in a commercial bank with good business performance and reputation in the market. That will make the capital mobilization target of the Bank easier and more favorable. On that basis, commercial banks will expand their scale of operations to improve quality, contribute to increasing profits and attracting more customers. Therefore, the top goal of the Bank's business activities is operational efficiency.

The business performance of commercial banks is assessed through the financial capacity of the bank through indicators to ensure safety in the business activities of commercial banks such as credit limits for customers, minimum capital safety, etc. and business capacity , in which indicators on profitability ratios are often mentioned the most.

The business performance of commercial banks is shown through profitability indicators such as return on assets (ROA), return on equity (ROE), net interest income (NIM)... These indicators provide an overview of the business performance of commercial banks, helping to show the profits earned through lending, investment, and service activities based on existing scale, capital, and assets.

The indicators measuring the business activities of commercial banks must be taken through many stages and periods to grasp the trends, development capabilities as well as the operation cycle of the Bank more comprehensively. At the same time, the thesis relies on the reality in Vietnam with the business scale of the Bank to determine the results after running the data to provide appropriate solutions.

2.1.2. Profitability ratio of commercial banks

2.1.2.1. Definition

The profitability of a bank is always a matter of primary concern for bank managers because a bank with high and sustainable profits will have the ability to develop highly and be competitive in an international integration environment. It can be seen that the business results of a bank are reflected through profits. If a bank has high profits, it shows that the bank is operating effectively, creating trust with customers, and has high technical and technological conditions, which will motivate customers to increasingly deposit money and participate more in the bank's products, contributing to creating conditions for the bank to grow.

In commercial banks, profits are generated by borrowing (selling debts) according to different criteria such as liquidity, risk, face value, maturity, interest rate, etc., and then the bank lends them back (buys assets). This process of borrowing and lending is called asset conversion, which means that the bank uses savings to invest in assets.

savings of one person to lend to another and profit is the income from providing services related to the above asset transformation process (if the bank can provide the desired services at cost n and get high income from the assets, the bank will get profit) according to Nguyen Van Tien and Pham Huu Hong Thai (2014).

One of the factors reflecting the efficiency of a bank's business operations is the profitability ratio. The profitability of commercial banks is often measured through quantitative indicators such as: the absolute value of after-tax profit, growth rate, profit structure and indicators showing the profitability ratio such as return on equity (ROE), return on assets (ROA), net interest margin (NIM)... the more efficient a bank is, the higher this group of indicators is. According to Horward and Upton, the ability of a certain investment to generate profit is called the profitability ratio.

Some people often confuse the concepts of profit and profitability. Sometimes, the terms “profit” and “profitability” are used interchangeably. But in reality, the two terms are different in meaning. Profit is an absolute term, referring to the total income of a bank over a certain period of time; whereas profitability is a relative concept, referring to the efficiency of a bank’s operations.

2.1.2.2. Indicators measuring the profitability of commercial banks

Banks need to consider the profit level, balance the costs for losses that occur to measure the bank's profitability and is shown through the following indicators:

Return on Assets (ROA)

The assets of a bank are formed from loans and equity, and both of these sources of capital are used to finance the activities of commercial banks. The ratio of income on total assets (ROA) is the indicator used in most studies measuring the profitability of banks such as Sufian (2011), Naceur et al. (2008)…

The ROA indicator shows the effectiveness of the organization and management of the unit's operations. The results of the indicator show how much profit is generated for each dong of assets used in the production and business process. Through ROA, it shows the ability to use assets effectively to generate profits. The higher the ROA, the more effective the bank's ability to use assets to generate profits and create good business performance for the bank. Therefore, the higher the ROA ratio, the higher the bank's profitability according to Davydenko (2011). ROA depends not only on the bank's policy decisions but also on macroeconomic factors that the bank cannot control.

ROA = Profit after tax * 100

Total assets

According to Rivard et al. (1997), ROA is the best indicator to measure the profitability of a bank because ROA is not affected by the increase in capital and ROA shows the ability to generate profitability of the bank from its own asset portfolio. The only problem with ROA is that the above ratio does not take into account off-balance sheet factors that may affect the bank's operations according to Davydenko (2011).

Compared with ROE, the return on assets ratio further measures the efficiency of the bank's financial leverage resources. Return on total assets

Assets are more comprehensive than return on equity, but can also be a more confounding factor than return on equity.

Return on Equity (ROE)

Return on equity (ROE) is the ratio of net income to total equity. It shows how much profit is generated for each dollar of capital from the bank's owners over a given period of time (usually assumed to be 1 year). In other words, ROE measures the benefits that shareholders (bank owners) receive from their invested capital. Studying ROE will show how the bank has used its invested capital to generate profits (Gul, Irshad and Zaman (2011)).

ROE = Profit after tax

Total equity

* 100

ROE is a measure of the rate of return to the bank's shareholders. It represents the income that shareholders receive from investing in the bank (i.e. investing at risk in the hope of earning a reasonable level of income).

According to resource theory, capital is an important factor in the resources of every business. The good exploitation of resources to create profits shows the efficiency of the business owner's profitability.

The higher the ROE ratio, the more effective the bank is in using its shareholders' capital, balancing shareholders' capital and borrowed capital to exploit its advantages in the process of capital mobilization and expansion. Therefore, the higher the ROE ratio, the more attractive the bank's shares are to investors.

According to Davydenko (2011), to best evaluate profitability, it is necessary to consider both ROA and ROE indicators, although these two indicators have different meanings, both indicate the same thing.

management's effectiveness in generating returns from shareholders' investments and investments in banks' asset portfolios.

Other indicators

In addition to the two indicators ROA and ROE, the profitability of commercial banks is also shown and measured by other indicators in research articles by other authors such as:

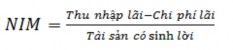

- Net Interest Margin (NIM)

In the studies of Rose (1999), Liu et al. (2010), Dietrich et al. (2011), the interest margin ratio is used as a dependent variable to analyze the factors affecting the profitability of banks. The higher this ratio, the higher the profitability of the bank. NIM is determined by total interest revenue minus total interest expenses over average total earning assets. Accordingly, average total earning assets are measured according to items including deposits at the State Bank, credit institutions, customer loans and investment securities.

The interest margin measures the spread between interest income and interest expenses that a bank can achieve by closely controlling its income-earning assets and pursuing the lowest-cost sources of funds.

NIM shows the management capacity of bank leaders and employees to maintain the growth potential from revenue sources compared to the increase in costs (Rose, 1989). Through that, it helps the Bank improve its ability to control the use of assets to generate profits and helps assess which capital sources have costs.

lowest. However, NIM does not take into account service fees as well as other non-interest income and operating expenses, such as personnel and asset costs, or credit risk provisioning costs, so NIM does not fully reflect the profitability of the entire banking industry according to Naceur et al. (2008).

- Return on Capital Employed (ROCE)

Return on capital employed is an indicator of a bank's ability to generate profits based on the amount of capital employed, and the higher the ROCE, the higher the bank's ability to generate profits (Zaman et al. (2011)) ROCE is calculated according to the formula:

In which: Capital used = Total assets - short-term debt

ROCE is a good indicator to compare the profitability of banks. Besides, ROCE is also used to evaluate the operational efficiency of banks.

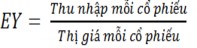

- Stock Slope (EY – Earning Yields)

All of the above metrics use book value, except for EY which uses market value calculated using the formula

According to Sangoi (2011), stock slope is an important indicator indicating the future profitability of commercial banks based on market assessments. If EY is high, it means that the market predicts a low profit growth in the future and low EY shows the market's hope for high profit growth in the future.

2.2. Interest rate policy and bond slope.

The paper uses the proposal of Claudio Borio et al. (2017) to measure monetary policy through interest rates and bond slopes. There are many monetary policy tools, but the common goal of these tools is to adjust the supply and demand effects and risks of the domestic currency. The market receives the adjustment impact from the total monetary policy tools and shows the fluctuations through interest rates and bond slopes. In other words, the fluctuations in interest rates and bond slopes are the output of monetary policy tools, recording the effective adjustment results of monetary policy adjustment tools.

Stabilizing the domestic currency and controlling inflation are considered the most important goals of the central banks in all countries in the world and Vietnam is no exception. And interest rates are the most important goals, reflecting the influence of monetary policy tools in the management of the central bank.

2.2.1. General introduction to Monetary Policy

Monetary policy is a system of viewpoints, policies and measures of the state, policy tools implemented by the central bank to regulate money supply, to influence and adjust to achieve monetary-credit, banking and foreign exchange activities to promote the development of the national economy.