The bank acts on the customer's behalf to collect commissions.

Estate Administration : This type of trust is formed and applied to the deceased person's assets according to their will.

Asset management under a signed contract: The bank manages assets under a trust contract signed with the principal.

Guardianship: The bank manages all assets for a legally incompetent person, a minor or a mentally ill person.

Maybe you are interested!

-

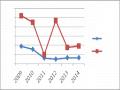

Evaluation of SHB's Business Performance After Merger According to Camel Model

Evaluation of SHB's Business Performance After Merger According to Camel Model -

Indicators Reflecting the Safety of NHTM's Business Operations

Indicators Reflecting the Safety of NHTM's Business Operations -

Company's Business Performance Results for 3 Years (2018-2020)

Company's Business Performance Results for 3 Years (2018-2020) -

Employees, Managers, Executives of Credit Institutions and Foreign Bank Branches Are Not Allowed to Disclose the Organization's Business Secrets

Employees, Managers, Executives of Credit Institutions and Foreign Bank Branches Are Not Allowed to Disclose the Organization's Business Secrets -

Bank Card Business Evaluation Criteria

Bank Card Business Evaluation Criteria

Representative services: Receiving and managing assets such as collecting principal and securities profits, administrative agency, litigation representation, etc.

Treasury management entrustment: The bank will be responsible for collecting and disbursing cash for customers through the branch system and can also send employees to the business to perform this service. The fee collected from this service is not much, but this is one of the services provided by the bank to ensure the level of connection between the business and the bank.

Insurance Services (Bancassurance)

Bancassurance is a channel in the product distribution strategy of insurance companies in association with commercial banks to effectively provide insurance products to their customers. Banks provide insurance services and receive insurance brokerage fees. The insurance services that banks can provide to customers are credit insurance, life insurance, property insurance, etc. These services are increasingly linked with other banking services.

Information consulting service

The bank selects and provides customers with information such as: commodity prices, exchange rates, stock markets, financial status of customers preparing to transact with businesses... In addition, the bank's consulting activities for customers also include services: effective cash flow management, determining an effective capital structure, and consulting on risk management in business.

Safe deposit box rental service

Custody service is a service in which banks keep valuable assets and important documents for customers such as gold, gemstones, savings books, house papers, etc.

Real estate services

For real estate transactions, banks can provide consulting services on safe payment procedures and provide payment services via banks, including consulting on the legal status of real estate, performing procedures for name change, notarization, and transactions to receive service fees.

Trading in gold, silver, precious stones, foreign currency

The above banking operations cannot be separated or independent from each other, but they have a mutual relationship with each other in the banking business process.

1.2.2. Off-balance sheet transactions

Asset and Liability management has long been a top concern for banks, but in recent years, increasingly competitive conditions have forced banks to aggressively seek profits by conducting off-balance sheet activities (transactions that are not recorded on the bank's balance sheet). Off-balance sheet activities include:

Credit guarantee contracts, in which the bank undertakes to guarantee the repayment of a customer's loan to a third party, the lender.

Interest rate swaps, in which a bank commits to exchange interest payments on debt securities with another party.

Interest rate futures and options contracts, in which a bank agrees to deliver or receive securities from another party at a guaranteed price.

A loan commitment contract in which the bank commits to lend up to a certain amount of capital before the contract expires.

Foreign exchange contracts, in which a bank agrees to deliver or receive a specified amount of foreign currency.

1.3. Commercial bank profits

1.3.1. Concept of commercial bank profit

The profit of a commercial bank is the difference determined between the total revenue receivable minus the total reasonable and valid expenses payable. The profit realized during the year is the business result of a commercial bank, including operating profit and other operating profit.

One of the important goals that commercial banks aim for is to maximize profits. Profit is a synthetic indicator reflecting the business results of commercial banks, an important source of accumulation, supplementing equity capital to expand business activities.

1.3.2. How to determine profit

Commercial bank profits include profits before corporate income tax and profits after corporate income tax.

Profit before tax

Is the difference between total income and total expenses .

Profit before tax = Total income – Total expenses

In there:

Commercial bank income includes:

- Interest income from credit activities

- Interest income from deposits at credit institutions

- Interest income from stock investment

- Service fee income

- Income from foreign exchange and gold trading activities

- Income from other profitable assets includes income from capital investment in buying shares, income from other business activities, etc.)

In the business activities of commercial banks, interest income from credit activities often accounts for a large proportion of total income, and is also a part of income affected by many types of risks.

Commercial bank costs include:

- Deposit interest payment costs

- Loan interest payment costs

- Interest payment costs for issuing valuable papers

- Banking service operating costs

- Securities trading costs

- Cost of foreign exchange and gold trading

- Salaries and benefits paid to bank employees

- Depreciation costs of physical assets of the bank

- Management costs

- Provision for credit losses

- Other expenses (including capital contribution costs to purchase shares, expenses for other business activities, etc.)

Profit after tax

Is the difference between pre-tax profit and corporate income tax.

Corporate income tax = Profit before tax x Corporate income tax rate Profit after tax = Profit before tax - Corporate income tax

1.3.3. Indicators for evaluating commercial banks' business performance

1.3.3.1. Profit after tax on income

After-tax profit margin on income =

Profit after tax

Income

x 100

Profit after tax on income = Profit after tax / Income This indicator shows the efficiency of profit after tax on one dong of income.

1.3.3.2. Return on total assets (ROA)

Return on total assets =

Profit after tax Total assets

x 100

Return on assets measures the efficiency of a bank in using its assets to generate profits after removing the impact of taxes; since assets are independent of the capital structure, the return on assets is also independent of the capital structure that forms the assets.

Since ROA is the rate of return for both creditors and owners after deducting corporate income tax, the numerator to determine ROA includes both the profit for owners, which is profit after tax (EAT), and the profit for creditors, which is interest expense.

This total profit is called earnings before interest and after tax.

ROA is an indicator to evaluate the effectiveness of bank management, showing the ability in the process of converting assets into net income.

1.3.3.3. Return on equity (ROE)

Profit after tax

Return on equity

Equity

x 100

ROE measures the rate of return to the bank's shareholders. It represents the income that shareholders receive from their capital investment in the bank.

Increasing the rate of return on equity is the most important goal in the business activities of commercial banks.

1.3.3.4. Net Interest Margin (NIM)

Net interest margin (NIM) is the difference between interest income and interest expense, all divided by earning assets. NIM measures efficiency and profitability. It is monitored by banks because it helps them forecast their profitability through tight control of earning assets and the search for the lowest cost sources of funds.

Marginal income ratio =

Interest Income – Interest Expense Earning Assets

x 100

1.3.3.5. Non-interest margin (NM)

Non-interest margin (NM) measures the difference between non-interest income and non-interest expenses (salary costs; equipment repairs and maintenance; credit loss costs, etc.).

Non-interest margin =

Non-interest income – Non-interest expenses Earning assets

x 100

1.3.4. The role of profit

For commercial banks

The business activities of commercial banks in a market economy aim to achieve profit goals within the framework of the law. Profit is both the goal and the condition for the existence and development of banks.

Profit affects all activities and financial capacity of commercial banks. A commercial bank with high profit, large revenue and reasonable costs will ensure solvency and create prestige in mobilizing domestic and foreign capital.

Profit is an important source of accumulation to increase the scale of the capital of commercial banks, and at the same time is a source to encourage material benefits for workers, linking the efforts of workers with their final results, improving workers' lives, motivating them to be creative, improving skills to increase labor productivity, and perfecting products.

For the economy and society

Profit is not only a part of the pure income of commercial banks but also an important source of revenue for the State budget, the most important source of accumulation to carry out expanded social reproduction and meet the development needs of society.

In addition, the profit of a commercial bank is a part of the cash flow, based on which investors, shareholders, state management agencies... determine the value of a commercial bank, and at the same time is the basis for evaluating the management and operational capacity of the Board of Directors of a commercial bank and evaluating the financial capacity and operational capacity of a commercial bank.

For joint stock commercial banks, after-tax profits, after covering special expenses, are usually divided into two parts: (i) Payment to shareholders in the form of dividends based on the value of shares; (ii) Supplementing equity capital.

The goal of commercial banks is to maximize the owners' benefits, that is, to maximize the ratio of net profit/equity. However, commercial banks cannot pursue the profit target at all costs, regardless of compliance with safety assurance principles, because the operations of the commercial banking system are very sensitive, the risks arising in the operations of the banking system are contagious and cause serious consequences for the economic system, not only in a country but also in the regional economy, even the global economy.

1.4. Factors affecting commercial bank profits

There have been many studies in the world on bank profits as well as factors affecting bank profits. Here are the results of some studies.

In the study on the determinants of bank profitability in Macao by Anna PI Vong and Hoi Si Chan, the authors pointed out the factors affecting the profitability of Macao banks, in which: Capital strength is the most important factor determining profitability, well-capitalised banks are found to have lower risks and therefore this advantage

are fully translated into higher profits. Asset quality, as measured by loan-loss, adversely impacts bank performance. In addition, a large deposit/retail network does not help banks in increasing their operational efficiency. And finally, of all the macro variables, only inflation rate is significantly correlated with bank performance.

Some studies on the determinants of bank profitability divide the influencing factors into internal and external factors, these studies identify ROA, ROE as dependent factors, while the influencing factors are independent factors. Internal factors focus on specific characteristics: capital size/magnitude; outstanding loans and total deposits; while external factors are considered as macroeconomic indicators, gross national income (GDP), inflation rate (INF), and market capitalization index (MC), etc.

Specifically: Molyneux and Thornton (1992) studied banking industry profits in 18 different countries in the European region, data were collected during the period from 1986-1989, the study found a significant positive relationship between interest rates, bank concentration and government ownership.

Demirguc-Kunt and Maksimovic (1998) identified a positive relationship between size and profitability, increasing capital makes it easier for banks to meet stringent capital requirements, thus they have more resources to lend and as a result increase profits. Naceur and Goaied (2001) identified the factors affecting Tunisian bank efficiency during the period 1980-1995, the best developed banks always strive to have a good workforce, capital productivity and achieve a high balance between total deposits and assets.

Chen and Yeh (1998) studied the performance of 33 Taiwanese banks, using variables such as loan services, investment portfolio, interest income, and non-interest income as output variables, and simultaneously considering the number of employees, total bank assets, number of bank branches, operating expenses, and total deposits as input variables.

In summary, factors that can affect bank profits can be divided into two groups: internal factors and external factors.

1.4.1 External factors

Monetary policy

Banks are special businesses that are affected by many policies and regulations of the Government and the State Bank. Any adjustment by the State Bank on finance and currency affects the ability to mobilize and use capital, for example: The regulation of the required reserve ratio for commercial banks forces banks to consider how to use capital and mobilize capital effectively; Or the State Bank's increase or decrease in refinancing interest rates greatly affects the situation of capital mobilization and credit granting. In particular, in the period of high inflation, the State Bank increases the required reserve ratio, causing the mobilized capital used for profitable lending to decrease, leading to a decrease in the income and profit of commercial banks.

Although monetary policy has a great influence on commercial banks, the limitation of the thesis is that it has not quantified the impact of monetary policy on profits.

Inflationary

High inflation makes it difficult for banks to mobilize capital. To mobilize capital, or to prevent capital from flowing from their bank to other banks, they must raise the mobilization interest rate close to the developments of the capital market. But how much is reasonable to raise is always a difficult problem for each bank. An unexpected race for mobilization interest rates at most banks always creates a new mobilization interest rate level, then continues to compete to push up the mobilization interest rate, some banks bring the mobilization interest rate close to the credit interest rate, banking business suffers huge losses but still does it, causing instability for the entire banking system. High inflation, the State Bank must tighten monetary policy to reduce the amount of money in circulation, but the demand for loans from businesses and individual businesses is still very large, banks can only meet the needs of a few customers with signed contracts or projects that are truly effective, with an acceptable level of risk. On the other hand, due to the high mobilization interest rate, the lending interest rate is also high, which has worsened the investment environment of banks, moral hazard will appear. Due to the decrease in purchasing power of Vietnamese Dong, the increase in gold and foreign currency prices, mobilizing capital with a term of 6 months or more is really difficult for each bank, while the demand for medium and long-term loans for customers is very large, so the use of short-term capital for medium and long-term loans in the past time at each bank is not small. This has affected the liquidity of banks, so term risk and exchange rate risk are inevitable.