Objective factors , there are four factors affecting the NLCT of a commercial bank:

New commercial banks enter the market with important advantages such as opening up new potentials, having the motivation and desire to gain market share, having consulted with existing commercial banks, having full statistics and forecasts about the market... Thus, regardless of the strength of the new commercial banks, existing commercial banks have seen a threat of the possibility of market share being shared, in addition, new commercial banks have strategies and strengths that existing commercial banks do not have information and strategies to respond to.

Current commercial bank competitors. These are constant concerns of commercial banks in business. Competitors affect the business strategy of commercial banks in the future. In addition, the presence of competitors encourages banks to constantly pay attention to technological innovation and improve the quality of service provided to win in competition.

Pressure from customers. One of the important characteristics of the banking industry is that all individuals, consumer production businesses, and even other banks can be both buyers of banking products and services and sellers of products and services for banks. Those who sell products through deposits, opening transaction accounts or lending all want to receive a high interest rate; meanwhile, those who buy products (borrow capital) want to pay a lower borrowing cost than the actual cost. Thus, banks will have to face the contradiction between effective profit-making activities and retaining customers as well as obtaining the cheapest possible source of capital. This poses many difficulties for banks in their future orientation and methods of operation.

Maybe you are interested!

-

Goffi G's Model for Assessing Tourism Destination Competitiveness and Sustainability

Goffi G's Model for Assessing Tourism Destination Competitiveness and Sustainability -

Indicators for Assessing the Competitiveness of the Commercial Banking System

Indicators for Assessing the Competitiveness of the Commercial Banking System -

Qualitative Indicators for Assessing Business Competitiveness

Qualitative Indicators for Assessing Business Competitiveness -

Some Theories and Contents on Improving Business Competitiveness

Some Theories and Contents on Improving Business Competitiveness -

Survey Results of Experts Assessing Provincial Competitiveness in the Tourism Sector

Survey Results of Experts Assessing Provincial Competitiveness in the Tourism Sector

The emergence of new services. The massive emergence of intermediary financial institutions threatens the advantages of commercial banks when providing new financial services as well as traditional services that are still provided by commercial banks.

responsibility. These intermediaries provide customers with differentiated products and create more diverse choices for buyers, expanding the banking market. This will inevitably have an impact on slowing down the growth rate of commercial banks, and reducing market share. Nowadays, it is believed that when commercial banks become stronger through competition, the commercial banking system will be stronger and more resilient after economic shocks.

Subjective factors : in addition to the objective factors affecting the competitiveness of commercial banks, in reality, the group of factors internal to the commercial banking system also greatly affects the competitiveness of these banks. They include: the management capacity of the bank's board of directors, the capital scale and financial situation of the commercial bank, the technology of providing banking services, the quality of bank staff, the organizational structure, the reputation and prestige of the commercial bank.

1.2. Models and theories for assessing competitiveness

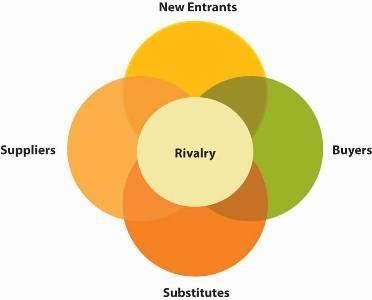

1.2.1. Michael Porter's 5 competitive forces model

The perfect competition model assumes that the rate of profit and the level of risk are balanced between businesses and between industries in the economy. That is, businesses operating in any industry of the economy have the same potential rate of profit and the same level of risk due to the self-regulating mechanism of competition. Businesses in an environment with low profit and high risk will tend to withdraw and seek industries with higher profit potential and less risk. However, many recent research models confirm that different business industries have different profitability, this difference is caused by the structural characteristics of the industry. For example, businesses operating in the telecommunications service sector have different profit rates than construction companies or food processing companies. Michael Porter has provided us with a competitive analysis model according to which a business industry is influenced by five basic forces and is called the five competitive forces model.

Competitive environment. According to Porter, the competitive conditions in an industry depend on many different factors. Among these factors, in addition to the businesses competing with each other within the industry, there are other factors such as customers, supply systems, substitute products or potential competitors. Strategic managers who want to develop an advantage over their competitors can use this tool to analyze the characteristics and scope of the industry in which their business is operating or will be operating.

Figure 1.1: Five competitive forces model

(Source: Michael Porter, “Competitive Strategy, 1980, page 4)

Competitive pressure within the industry : When a business competes and acts in a way that other businesses do not grasp its competitive mechanism, the level of competition becomes increasingly fierce. Competitors either imitate the way to exploit competitive advantages or will seek other advantages, and thus businesses are constantly looking for new ways to compete. The intensity of competition is usually expressed in levels such as: very fierce, high intensity competition, moderate competition, weak competition. These levels of competition depend on the ability

the responsiveness of businesses in building and exploiting competitive advantages. To pursue superior advantages over competitors, a business can choose one or more of the following competitive methods:

Price changes: Businesses can increase or decrease prices to gain a temporary competitive advantage.

Increasing product differentiation: Businesses often compete by improving product features, applying new advances in the production process or to the product itself.

Creative use of distribution channels: Enterprises can implement vertical integration strategies by deeply intervening in the distribution system or using new distribution channels; using distribution channels of related products or distribution channels of other products with similar customer targets.

Exploiting relationships with suppliers: Enterprises use prestige, negotiating power or relationships with the supply system to implement new requirements to create product differentiation, improve product quality or reduce input costs.

Threat of substitutes : In Porter's model, substitutes refer to products from other industries. For economists, the threat of substitutes exists when the demand for a product is affected by changes in the prices of substitutes. The price elasticity of a product is affected by substitutes; the simpler the substitutes, the more elastic the demand because customers have more choices. Substitutes depend on the ability of firms in an industry to raise prices. The rivalry caused by the threat of substitutes is due to products from other industries. While the threat of substitutes usually affects an industry through price competition, there can be threats of substitutes from other sources.

Competitive pressure from customers : Is the ability of customers to influence

an industry. Usually when the customer has the advantage in negotiating or is called a powerful customer, the relationship between suppliers and customers in an industry is close to the market situation that economists call oligopoly - that is, the case in the market where there are many sellers and only one or a very few buyers. In such market conditions, the buyer often has the decisive role in determining the price. In practice, such oligopoly market situations rarely occur, but there is often an asymmetry between an industry and the buyer market.

Competitive pressure from suppliers : Manufacturing industries require raw materials, labor, and other inputs. These requirements lead to buyer-supplier relationships between the manufacturing industry (as a group of producers in an industry) and the suppliers (who provide the inputs). Suppliers, if they have bargaining power, can exert significant influence on the manufacturing industry, such as forcing down the price of raw materials.

Competitive pressure from potential competitors : potential competitors are businesses that are not currently present in the industry but may influence the industry in the future.

1.2.2. Victor Smith's Theory of Competition

According to Victor Smith (2002), Core competencies in the retail sector of the financial service industry, to compete, it is necessary to develop the following 5 factors:

Brands: by developing brand awareness through advertising and managing customer expectations, continuously strengthening customer trust and satisfaction; businesses will increase their value in the market. That is the key to showing the difference of businesses compared to competitors.

Product: a product has value to customers when it satisfies a certain customer need. Pricing is based on customer value, not just marginal cost.

Service: Service includes two parts: customer interface and transaction execution. Customer interface is the responsibility of all departments that have direct interaction with customers such as: sales department, customer support department via phone, corporate website, voice response system and mail. To develop customer service, it is necessary to develop data, internet technology, and manage customer interactions. This requires training, instilling confidence in employees and creating a comprehensive knowledge system to manage customer needs, maintain competitive advantage. Transaction execution: is receiving data from customers and processing data.

Intellectual Capital: Intellectual capital includes human capital and applied skill set. It is the responsibility of management to identify and convert know-how into knowledge and skills that can be applied to the business. These skills are: knowledge management, human resource management, technology and product knowledge.

Cost and Infrastructure: includes flexible organization and systematic integration, value chain management, risk/cost management, compliance with regulations and safety, etc. with the aim of bringing high financial efficiency and increasing shareholder value.

1.3. Criteria for assessing bank competitiveness

1.3.1. Financial capacity

The financial capacity of a bank represents the strength of a bank at a given point in time. The financial capacity of a bank is analyzed based on the following criteria:

Equity capital scale : equity capital provides financial capacity for the growth process, expansion of scale and scope of operations as well as for the development of new products and services of the bank. Equity capital is formed from the following sources: charter capital, reserve fund to supplement charter capital, undistributed profits, and other funds of the bank. Capital is an important factor because it

It shows the strength and competitiveness of the bank in the market, and it is also the basis for the bank to expand its operations to regional and world financial markets.

Asset quality: the scale, structure and quality of assets will determine the existence and development of the bank, while assets include profitable assets (accounting for 80-90% of total assets) and non-profitable assets (accounting for 10-20% of total assets). Profitable assets include loans, financial leases and investments in securities, joint ventures, etc. The quality of a bank's assets is a composite indicator that reflects the financial sustainability and management capacity of a bank. Most risks in currency trading are concentrated in assets.

Bank profitability: associated with the quality of assets and the efficiency of asset use of the bank. Improving the quality of assets and capital sources is also improving the efficiency of the bank's business operations. Profitability is a synthetic indicator to evaluate the business efficiency and development level of a bank. To evaluate the profitability of a bank - people often use the indicators of net profit on assets (ROA), net profit on equity (ROE) or net profit on revenue.

Ensuring capital safety in banking operations: ensuring solvency is the bank's ability to be ready to pay, to pay customers and the ability to compensate for losses when risks occur in business operations.

1.3.2. Products and services

Competing through products and services is always the top goal of banks. The strategy applied by banks is to invest in technology to create the necessary infrastructure for product and service development, market segmentation and design of unique products, increasing the content.

technology and utilities for existing products and services, or find affiliate partners with advantages in customers, technology networks, ...

1.3.3. Management capacity

Management and executive capacity is reflected in the management and executive ability of the bank's board of directors to ensure the bank's operations are effective, safe and stable. The management capacity of the board of directors reflects the vision, strategic goals and risk appetite of a bank.

Banks, with the characteristics of being “money” business organizations, have high risks and great influence, so the issue of governance is very important, especially for a developing country like Vietnam, when banks are an extremely important external financial source for businesses. A bank with poor governance will not only cause losses for that bank, but also create certain chain risks for other units and vice versa.

1.3.4. Technological capacity

Technology has a profound impact on the competitiveness of commercial banks, is a factor that directly affects product quality, and is the most important component of the necessary infrastructure factors in the banking sector. Technology not only helps commercial banks improve their management and operation capabilities, information processing, and labor productivity, but also improves the quality and diversity of products and expands the operating space of banks. In the book Commercial Banking Management, Peter Rose wrote, "The modern banking system increasingly resembles a fixed-cost industry. Banks that want to maintain profits and competitiveness must expand their operations, often by gaining an advantage over smaller banks that are unable to keep up with technological changes." He saw machines taking over more and more of the daily work of banks. These automated devices are shortening the operating time of banking activities by record levels, while increasing the accuracy and convenience of banking services. In the context of increasingly fierce competition, technology is used by commercial banks as a powerful weapon to create competitive advantages.