- Board of Directors : This is the department with the highest decision-making power of Citibank. The board of directors allocates capital and manages the operations of the entire bank, including credit operations. The board of directors is responsible for setting the bank's risk level; setting strategic goals and general regulations used throughout the bank; reviewing credit granting decisions of credit officers if there is suspicion that they may cause material damage or affect the bank's reputation.

- Credit policy planning department : This department is responsible for maintaining a complete and effective form of credit risk management; participating in planning indirect investments, predicting credit losses; establishing credit policies and standards in accordance with the law and general regulations of the bank; reviewing and amending credit policies if they are deemed to cause unusual risks; considering granting credit authority to qualified officers; preparing reports on indirect investments, focusing on assessing the quality of risk information, risk handling process for all cases exceeding the permitted credit limit.

- Credit Line Management : Credit line managers are responsible for developing and implementing business plans, reviewing and approving loans, and are responsible for the quality of the loans. Credit line managers are also responsible for developing business strategies, reviewing and approving credit programs, managing indirect investments, and checking quality, correcting deficiencies when necessary.

- Business risk assessment department : The staff of this department must have at least 10 years of experience in credit operations and rotate in the department according to the requirements of business development. This department evaluates the business situation of the units and provides risk information in indirect investment; evaluates the independent assessment of credit operations, policies, implementation and procedures in credit management; coordinates activities with independent supervisors and auditors.

Second, Citibank conducts a borrower creditworthiness assessment: the borrower creditworthiness assessment focuses on the following key points according to the traditional "5 Cs of Credit" :

- Character of management: Character of management of the borrower;

- Financial capacity of the venture: Financial capacity of the borrower;

- Collateral security: Collateral to secure the loan;

- Condition of the industry: The field in which the borrower operates;

- Condition of terms: Credit terms and conditions.

Third, Citibank distinguishes between credit granting and approval rights.

Browse:

- The right to grant credit is delegated to credit officers based on their capacity and qualifications, professional skills and experience, education and training, and not based on their position in the bank.

- Approval authority: At Citibank, credit granting is not decided by one person, but by three credit officers who are responsible for lending and must approve individual credit programs or credit transactions.

Fourth, Citibank builds a centralized risk management organization model. Risk management activities are concentrated at the Head Office and divided into 3 functional departments: Operations department, risk management department, and debt management department.

1.3.1.4. Experience of ANZ Bank - Australia

ANZ is one of Australia’s leading banks, with assets of $507 billion in 2009 and more than 30,000 employees across all continents. The characteristics of ANZ’s risk management work are as follows:

- Quantitative risk measurement

Having built an integrated, centralized data system, ANZ can apply the internal credit measurement model and the RAROC model.

+ Internal credit measurement model: ANZ applies this model according to the general process as prescribed by Basel II. However, ANZ evaluates the default probability criterion as a key criterion to consider the creditworthiness of borrowers in the customer rating process. ANZ's credit rating system is designed in reference to the credit rating agency Standard & Poor, and complies with the strict rules of Basel II.

+ Raroc model: ANZ Bank applies the Raroc method and considers it as a method to calculate loan efficiency. According to ANZ, the Raroc method ensures that a loan is approved only if and only if the loan brings value to shareholders. If the RAROC of the loan is lower than the ROE, the loan will be rejected, but if it is higher, it will be approved. Based on this principle, the RAROC standard for ANS's approved loans over the past 5 years is calculated as follows:

Table 1.5: ROE and RAROC for ANZ loans

Year

2002 | 2003 | 2004 | 2005 | 2006 | |

ROE | 21.60% | 20.60% | 17.80% | 15.50% | 18.82% |

RAROC | >21.60% | >20.60% | >17.80% | >15.50% | >18.82% |

Maybe you are interested!

-

Experience of some countries in applying information technology to develop retail banking activities and lessons for Vietnam Joint Stock Commercial Bank for Industry and Trade - 12

Experience of some countries in applying information technology to develop retail banking activities and lessons for Vietnam Joint Stock Commercial Bank for Industry and Trade - 12 -

Limitations in the Development of Retail Banking Services at Vietnam Joint Stock Commercial Bank for Industry and Trade and the Causes

Limitations in the Development of Retail Banking Services at Vietnam Joint Stock Commercial Bank for Industry and Trade and the Causes -

Orientation and Development Strategy of Vietnam Banking System and Vietnam Joint Stock Commercial Bank for Investment and Development

Orientation and Development Strategy of Vietnam Banking System and Vietnam Joint Stock Commercial Bank for Investment and Development -

Quality of digital banking services for individual customers at Joint Stock Commercial Bank for Foreign Trade of Vietnam - 1

Quality of digital banking services for individual customers at Joint Stock Commercial Bank for Foreign Trade of Vietnam - 1 -

Practices of Improving Business Efficiency of Some Banks in the World and Lessons Learned for Vietnamese Joint Stock Commercial Banks

Practices of Improving Business Efficiency of Some Banks in the World and Lessons Learned for Vietnamese Joint Stock Commercial Banks

Source: [47]

- Centralized risk management organization

ANZ measures risk using a centralised risk management organisation. Firstly, all decisions on ANZ’s risk management strategy are centralised at the Board of Directors. Secondly, to ensure that credit decisions are rigorous and clear, the structure

ANZ's risk management activities are divided into three departments: Business Unit, Relative Credit Group, and Debt Department. Third, for large loans, the final decision is made by the Risk Management Committee and the Risk Management Board.

- Dual RRTD control

ANZ operates in a financial market that has developed over many decades, so all of the bank's credit activities are closely monitored by shareholders and the market. This contributes to increasing the transparency and openness of ANZ's information.

In addition, ANZ also focuses on building a comprehensive internal credit control system, including: (i) A system to warn of unusual signs of credit that is studied and put into operation so that losses can be promptly remedied; (ii) "Crisis testing" activities are carried out periodically or at times when the economy shows signs of instability to accurately quantify risks in each period and have measures to prevent, reserve for risks, and appropriate pricing policies; (iii) Internal audit activities with surprise inspection methods are being maintained very effectively to ensure absolute compliance in the system.

1.3.2. Lessons learned for Vietnam Joint Stock Commercial Bank for Industry and Trade in credit risk management

Through research on risk management in some banks around the world, the lessons learned for VietinBank are:

1.3.2.1. Implement credit risk management according to international practices, increase the use of quantitative methods in analyzing and assessing credit risks.

There is no common “scenario” for the Basel 2 implementation roadmap of commercial banks. Basel 2 includes 3 pillars and provides many approaches to measuring capital for credit risk. Each bank, based on the characteristics of credit risk and credit risk management capacity, has the most suitable choice for its approach as well as the time to comply with each pillar of Basel 2: It is possible to apply one or more approaches to credit risk, it is possible to gradually comply with each pillar or all 3 pillars at the same time. The Basel 2 implementation process must be associated with the process of innovation and improving credit risk management capacity.

To facilitate the implementation of Basel 2, the system of regulations and guidelines for Basel 2 implementation must be completed before the deadline.

In fact, in countries that have implemented Basel 2, the banking supervision agencies of each country have prepared and completed the legal corridor for Basel 2: Issued drafts, widely solicited opinions from commercial banks and related parties for completion.

Because the RRTD management system is not really effective, the Basel 2 compliance process must be a complete process and gradually comply with each step on the basis of taking advantage of available capacity to minimize costs during the implementation process. According to the experience of commercial banks surveyed by NCS, Basel 2 compliance does not necessarily have to follow the most complicated approach, banks need to choose an approach that is suitable to the current credit operations and current capabilities of each bank.

Although the Basel Committee recommends that commercial banks should aim to approach IRB for RRTD, especially advanced IRB. However, in reality, meeting the minimum requirements to access IRB is quite strict. Therefore, even large commercial banks with modern RRTD management systems still have to approach IRB for each market segment (some market segments are still approached by the SA method) according to the principle that the market segment with the advantage will comply first, the segments that have not met will be gradually improved until they meet the minimum conditions to comply.

For the IRB method, Basel emphasizes the issue of verifying the effectiveness and accuracy of internal estimates. Therefore, the surveyed commercial banks are required by the Banking Supervision Agency to have a transition period before applying - parallel approach to the traditional method (or SA) and IRB - this period can be considered as a trial operation period. At the surveyed commercial banks, there are regulations on the minimum time for parallel operation and this period will end when the verification shows that the estimation results meet the requirements of Basel 2 standards.

1.3.2.2. Selecting a credit risk management model based on the specific conditions of Vietnam Joint Stock Commercial Bank for Industry and Trade

Commercial banks around the world are very flexible in choosing a risk management model that is suitable to their conditions and internal resources, moving towards a model that meets international standards. The combination of risk management methods is very diverse and changes when market conditions change.

For example, Citibank, although operating in a developed financial market, was plagued by high levels of overdue debt from the 1990s onwards and the market

As derivatives grew, Citibank added qualitative metrics through its credit scoring system to analyze additional subprime loans.

Furthermore, determining the RRTD management model must be appropriate and compatible with the specific conditions of each bank. A bank developing in a weak financial market cannot immediately switch to applying a quantitative model because the information data in that market cannot improve immediately, or cannot apply a dual control model because in a developing financial market, the control role of the market is very vague. If the model is determined to be inappropriate for its conditions, it will waste resources and not bring practical results.

1.3.2.3. The effectiveness of credit risk management depends on the results of the stages in credit risk management.

Commercial banks around the world closely combine the stages of the credit risk management process from recognition to measurement, management, and control to form a whole in risk management activities. Quantitative measurement activities will create accurate information and can accumulate information about a focal point, on the basis of which the bank can organize centralized management. On the basis of information and collective risk management activities, the internal control department can well control the bank's credit activities. If a bank only conducts credit risk management based on risk measurement or only cares about risk organization, it will not bring about synchronous efficiency.

The Bank continuously reviews, reports and controls risks. The Bank needs to pay attention to improving system governance and avoiding potential risks in business operations by regularly reviewing key risks such as credit, interest rate, liquidity and market to ensure that these risks do not exceed acceptable levels. Particularly for RRTD, the Bank needs to complete the internal rating system and analyze monthly fluctuations in risk levels for each industry as well as enterprises, ensuring that established limits are not exceeded, thereby maintaining the Bank's consistent risk appetite.

1.3.2.4. Perfecting and complying with the legal system

To ensure the safety of the banking system, in 1988, the Basel Committee on Banking Supervision approved the first document called the Basel Capital Accord (the Basel Capital Accord or Basel I), requiring banks operating internationally to hold a minimum capital level. According to Basel I, a bank's total capital must be at least 8% of its RRTD. On June 26, 2004, the new Basel Capital Accord (Basel II) was officially issued. The Basel II Accord provides 03 methods of calculating RRTD including: Method

Standardised method, Foundation Internal Ratings Based (FIRB) method and Advanced Internal Ratings Based (AIRB) method.

ANZ Bank operates a good model because it develops in a stable and public legal environment, accounting standards on credit activities, risk provisions, debt management mechanisms are improved, borrowing enterprises must publicly disclose full financial reports, and the financial situation is clear.

For Vietnamese commercial banks, it is necessary to comply with regulations on debt classification and provisioning for credit risks in accordance with Circular No. 02/2013/TT-NHNN dated January 21, 2013 and Circular 09/2014/TT-NHNN amending Circular 02/2013/TT-NHNN of the Governor of the State Bank, gradually diversifying credit activities towards standardization and conformity with international practices.

1.3.2.5. Modernize technology to operate an effective credit risk management model

Most banks such as ANZ and Citibank have a solid technology foundation, which is the basis for banks to apply the QTRRTD model. The information systems of these banks are all processed automatically and centrally, with software that can classify loans that are due, overdue and problematic, and from there, provide reports to different management levels. The centralized information system will help banks analyze customers better and provide corresponding risk management measures. Therefore, information technology is the key to operating the QTRRTD model.

Banks need to build a modern information technology system to help bank staff easily look up and search for information related to customers. In addition, a modern information technology system also helps improve the quality of customer analysis and assessment, minimizing risks due to lack of information. Build a centralized data management system for the entire bank as a basis for continuous and timely evaluation and monitoring of investment credit portfolios.

CONCLUSION OF CHAPTER 1

Chapter 1 outlines the basic contents of bank risk management, including the nature of risk management, classification, causes and impacts of risk management on bank operations. An important content in this chapter is risk management, clarifying the concept of risk management, the need for risk management, the contents of risk management include: risk identification, risk analysis and assessment, risk response and risk control. In addition, this chapter delves into the study of measurement models, risk management models currently used by banks around the world along with compliance with the Basel Convention in risk management. To have a comprehensive view of QTRRTD, the author studies the experience of QTRRTD of some countries in the world with the same level of development or in the same region with similar economic conditions as Vietnam, thereby providing lessons in QTRRTD for the system of Vietnam Joint Stock Commercial Bank for Industry and Trade.

CHAPTER 2

CURRENT STATUS OF CREDIT RISK MANAGEMENT AT VIETNAM JOINT STOCK COMMERCIAL BANK FOR INDUSTRY AND TRADE

2.1 OVERVIEW OF VIETNAM JOINT STOCK COMMERCIAL BANK FOR INDUSTRY AND TRADE

2.1.1 The formation and development process of Vietnam Joint Stock Commercial Bank for Industry and Trade

In 1988, after separating from the State Bank of Vietnam, VietinBank was established, a commercial bank playing an important role, a pillar of the Vietnamese banking industry. VietinBank has a nationwide network with 01 Transaction Center, 150 branches and over 1,000 Transaction Offices/Savings Funds, with 9 independent accounting companies: Financial Leasing Company, Industrial and Commercial Securities Company, Debt Management and Asset Exploitation Company, VietinBank Insurance Company, Fund Management Company, Gold and Gemstone Company, Trade Union Company, Global Money Transfer Company, VietinAviva Company and 05 public service units: Information Technology Center, Card Center, Human Resources Training and Development School, Bank Star I motel and Bank Star II motel - Cua Lo. VietinBank is the first bank in Vietnam to open a branch in Europe, marking a remarkable development of Vietnam's finance in the regional and world markets. In addition, VietinBank has correspondent relationships with over 900 financial institutions in more than 90 countries and territories worldwide.

Table 2.1 Financial indicators of VietinBank in the period 2011 - 2017

Unit: Billion VND, %

Target

2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | |

Total assets | 460,420 | 503,530 | 576,368 | 661.241 | 779,483 | 948,699 | 1,095,060 |

Owner's equity | 28,491 | 33,625 | 54,075 | 55,259 | 56,110 | 60,399 | 63,765 |

Charter capital | 20,230 | 26,218 | 37,234 | 37,234 | 37,234 | 37,234 | 37,234 |

Total capital Action | 420,212 | 460,082 | 511,670 | 595,096 | 711,785 | 870.163 | 896,958 |

Total outstanding credit | 293,434 | 405,744 | 460,079 | 542,685 | 676,688 | 721,798 | 889,895 |

Net profit from Business before RRTD provision expense | 13,296 | 12,526 | 11,874 | 11,226 | 12,024 | 13,591 | 17,550 |

DPRRTD cost | (4,904) | (4,357) | (4,123) | (3,923) | (4,679) | (5,022) | (8,343) |

Profit before tax | 8,392 | 8,168 | 7,751 | 7.303 | 7,345 | 8,569 | 9,206 |

Corporate income tax | (2,132) | (1,998) | (1,943) | (1,576) | (1,628) | (1,712) | (1,747) |

Profit after tax | 6,259 | 6.169 | 5.808 | 5,727 | 5,717 | 6,858 | 7,458 |

ROA | 2.03% | 1.7% | 1.4% | 1.2% | 1.0% | 1.0% | 1.0% |

ROE | 26.74% | 19.9% | 13.7% | 10.5% | 10.3% | 11.8% | 12.0% |

Bad debt/credit balance ratio | 0.75% | 1.35% | 0.82% | 0.90% | 0.73% | 0.93% | 1.14% |

Capital Adequacy Ratio (CAR) | 10.57% | 10.33% | 13.2% | 10.4% | 10.6% | 10.4% | 10.5% |

Source: [26], [27], [28], [29], [30], [31], [32]

Through the data table 2.1 above, we can see that VietinBank is one of the 4 largest commercial banks in Vietnam. The total assets of the bank have been increasing continuously in the past 7 years, in 2011 the total assets were 460,420 billion VND, in 2012 it was 503,530 billion VND, in 2013 it was 576,368 billion VND, in 2014 it was 661,241 billion VND, in 2015 it was 779,483 billion VND. Regarding the equity and charter capital of VietinBank in the period of 2011 - 2015, it also increased continuously. We can see that the equity of VietinBank in 2011 was 28,491 billion VND, in 2012 it was 33,625 billion VND, in 2013 it was 54,075 billion VND, in 2014 it was 55,259 billion VND, in 2015 it was 56,110 billion VND, the charter capital in 2011 was

20,230 billion VND, 2012 was 26,218 billion VND, 2013, 2014 and 2015 VietinBank's charter capital was 37,234 billion VND

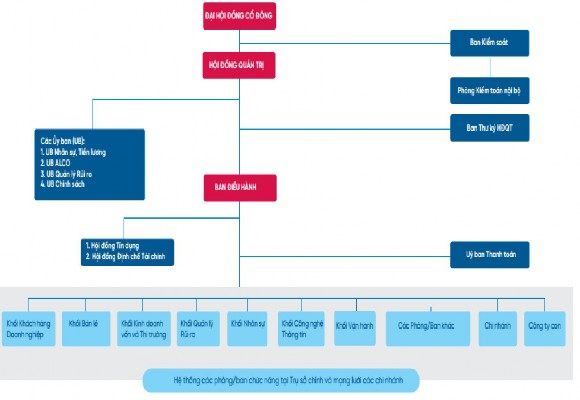

2.1.2 Model of organizational structure of Vietnam Joint Stock Commercial Bank for Industry and Trade

VietinBank's organizational management model is similar to the model implemented by modern banks in the world. Accordingly, the Board of Directors' supervision of the Executive Board (General Director and Deputy General Directors) is carried out according to the bank's internal governance regulations. In addition, the General Director is also a member of the Board of Directors, so it always ensures the Board of Directors' supervision in operational activities. There are regular meetings and standing meetings. Regular meetings take place monthly. Standing meetings take place weekly. At VietinBank, it is clearly stated that among the members of the Board of Directors, which members only attend regular meetings, which members are required to attend both regular meetings and standing meetings. At regular meetings, the General Director must report on all aspects of the bank's operations. In addition, the General Director must also report to the Board of Directors on topics, the implementation of resolutions of the General Meeting of Shareholders, resolutions and decisions of the Board of Directors. Assisting the Board of Directors in supervising the activities of the Executive Board is the Board of Supervisors. The Board of Directors assigns the Board of Supervisors to periodically inspect and report on the implementation of resolutions and decisions of the Board of Directors. The organizational structure of VietinBank has been and is being fundamentally improved in a more complete direction. Specifically, the organizational model has been restructured, basically dividing departments according to customer segments, combining according to products and services; decentralizing management according to the model to improve management efficiency and enhance risk management skills, improve the quality and efficiency of business operations, expand the network and develop new products on the basis of modern technology platforms. VietinBank's leadership is capable, dedicated, proactive and sensitive in directing

Business Operations. Most of the positions in the Board of Directors have undergone advanced training in business administration knowledge according to international practices. Over the past years, the Bank's Board of Directors has successfully directed the restructuring process of VietinBank under the direction of the Government and the State Bank of Vietnam. In particular, in the past 4 years, VietinBank has continuously implemented solutions to improve risk management capacity, ensuring the goal of sustainable growth.

Diagram 2.1. Organizational structure model of VietinBank

The Asset-Liability Management Model as recommended by the International Consultant is also being implemented. Accordingly, the bank's asset portfolio is centrally managed, adjusted by management tools such as internal capital transfer pricing policy, operating limits of each department, profit targets for each product and sales channel. Management of interest rate and liquidity risks are all centrally implemented at the Head Office, thus limiting risks to a low level, and non-financial income is increasing. There are also committees under the Board of Directors. The committees operate according to

The regulations on organization and operation of each Committee are issued by the Board of Directors. At VietinBank, there are 05 Committees: Risk Management Committee; Human Resources, Salary and

Reward Committee; Policy Committee; Asset-Liability Management Committee; Technology Development Strategy Research Committee.

2.1.3. Current status of business performance of Vietnam Joint Stock Commercial Bank for Industry and Trade in the period 2011 - 2017

2.1.3.1 Capital mobilization

We can analyze in depth the total mobilized capital and the mobilized capital structure of VietinBank through the following table and chart:

Table 2.2 Structure of mobilized capital of VietinBank in the period 2011 -

2017

Unit: %

Year

2011 | 2012 | 2013 | 2014 | 2015 | 2016 | ||

Total mobilized capital | 100 | 100 | 100 | 100 | 100 | 100 | 100 |

Customer deposits | 61.70 | 62.84 | 71.24 | 71.27 | 69.26 | 75.98 | 76.02 |

GTCG Release | 2.64 | 6.23 | 3.24 | 0.89 | 2.93 | 2.77 | 2.76 |

Borrow from State Bank and other credit institutions | 24.20 | 21.65 | 15.75 | 18.23 | 15.80 | 10.45 | 10.44 |

Other mobilization | 11.46 | 9.28 | 9.77 | 9.60 | 12.01 | 10.80 | 10.78 |

Source: [26], [27], [28], [29], [30], [31], [32]

870,163 896,958

711,785

595.0

420,212 460,082

511.67

96

1000

800

Total mobilized capital (billion VND)

600

400

200

0

2011 2012 2013 2014 2015 2016 2017

Chart 2.1 Total mobilized capital of VietinBank in the period 2011 - 2017

Source: [26], [27], [28], [29], [30], [31], [32]

Through the chart and table above, we can see that as of December 31, 2017, the total mobilized capital reached 896,958 billion VND. In 2016, the total mobilized capital of VietinBank was

870,163 billion VND, up 22% compared to 2015, December 31, 2015, VietinBank's total mobilized capital was 711,785 billion VND, up 19.61% compared to 2014. In 2014, it was 595,096 billion VND, up 16.3% compared to 2013 and reached 104% of the plan of the shareholders' meeting. VietinBank continues to maintain a capital growth rate in line with capital usage needs, and its capital structure is diversified. Capital mobilized from economic organizations increased by 13% and capital mobilized from the population increased by 19% compared to 2014. International capital sources such as ODA, ADB, WB... grew positively by 22.7% compared to the end of 2014. This has affirmed the prestige and strong brand of VietinBank in the market in the context of increasing competitive pressure.

2.1.3.2 Credit activities

Table 2.3 Total outstanding credit of VietinBank in the period 2011 - 2017

Unit: Billion VND, %

Target

2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | |

Total outstanding credit | 293,434 | 405,744 | 460,079 | 542,685 | 676,688 | 721,798 | 889,895 |

Growth rate compared with last year | - | 38.27 | 13.39 | 17.79 | 24.69 | 6.67 | 23.29 |

Source: [26], [27], [28], [29], [30], [31], [32]

As of December 31, 2017, VietinBank's total balance reached VND 889,895 billion, an increase of 23.29% compared to 2016. In 2016, it reached VND 721,798 billion, an increase of 6.67% compared to 2015. Credit balance as of December 31, 2015 reached VND 676,688 billion, an increase of 24.69% compared to 2014. Credit balance as of December 31, 2014 reached VND 542,685 billion, an increase of 117.79% compared to 2013 (higher than the average growth rate of the whole industry), reaching 104.5% of the plan. Outstanding credit as of December 31, 2013 reached VND 406,079 billion, up 13.39% compared to 2012, outstanding credit as of December 31, 2012 reached VND 405,744 billion, up 38.27% compared to 2011, outstanding credit as of December 31, 2011 was VND 293,434 billion.

900

800

700

600

500

400

889,895

721,798

676,688

542,685

Total outstanding credit (billion VND)

460,079

405,744

300 293,434

200

100

0

2011 2012 2013 2014 2015 2016 2017

Chart 2.2 Total outstanding credit balance of VietinBank in the period 2011 - 2017 Source: [26], [27], [28], [29], [30], [31], [32]

Through the above table, we can see that VietinBank's credit balance has a reasonable growth rate every year, in line with the general trend and market developments. However, we should not only consider sales, more importantly, we should pay attention to the overall and comprehensive consideration of profit indicators and ensure capital safety.

2.1.3.3 Business performance

Regarding the business performance of VietinBank in the period 2011 - 2017, we can see the data in the following table 2.3: