- The quality of supervision activities is increasingly improved by applying supervision indicators according to international practices and standards on risk analysis. The supervision reports of the Deposit Insurance of Vietnam have really helped relevant agencies in managing risks to the operations of the banking and financial system;

- A remote monitoring process and a customer information system have been established to serve monitoring activities. In addition to information and reports received from the BHTG, SBV, BHTGVN also collects customer information from the Credit Information Center (CIC). The BHTG is responsible for providing information sources as a basis for analyzing and assessing customer risks in order to have a complete and comprehensive monitoring report.

- The monitoring method has been improved based on the study of monitoring methods according to international practices and standards suitable to the actual conditions of Vietnam. BHTGVN is aiming to mainly monitor risks to provide early warnings to help BHTG organizations take effective preventive measures. For on-site inspection activities, inspections are not carried out widely but focus on inspecting weak units based on the results of remote monitoring activities, which is both cost-saving and does not overlap with the inspection activities of the State Bank.

* Inspection of social insurance organizations

The inspection of deposit insurance organizations is one of the most important tasks of the Vietnam Deposit Insurance Corporation and has been carried out since its establishment. Regarding the content and scope of inspection, the Vietnam Deposit Insurance Corporation is responsible for "monitoring and inspecting the compliance with the provisions of the law on deposit insurance; recommending the State Bank of Vietnam to handle violations of the provisions of the law on deposit insurance". Unscheduled inspections are conducted when detecting signs of violations of the law on deposit insurance by deposit insurance organizations. For newly established deposit insurance organizations, the Vietnam Deposit Insurance Corporation immediately conducts an inspection of the first-period premium payment in combination with guiding the unit to implement the regulations on the issuance and posting of the Deposit Insurance Certificate, on the method of determining insured depositors, calculating and paying deposit insurance premiums, and implementing the information reporting regime for the Vietnam Deposit Insurance Corporation, etc.

On-site inspection activities of BHTGVN contribute to raising awareness of BHTG organizations about BHTG policies, self-consciousness in complying with legal regulations on BHTG and regulations and instructions of BHTGVN. Conclusions of on-site inspections

All of them point out the causes of errors and measures to overcome and handle existing problems, helping the inspected units review their management work, rectify compliance with the law and not repeat the violations in the future. Through each inspection, the inspected units also have the opportunity to present the advantages, difficulties and obstacles in implementing the provisions of the law on social insurance, from which the social insurance agency of Vietnam can review and make appropriate amendments or make recommendations to competent authorities to study and resolve macro-level issues.

2.2.1.5. Financial Support Activities

When a deposit insurance institution is in trouble and at risk of insolvency, financial support is a measure that the deposit insurance organization uses to support these institutions. The deposit insurance organization can support by providing direct loans, buying back assets or taking on debts, or depositing money in troubled banks and guaranteeing loans. The financial support solution of the deposit insurance organization has brought certain effectiveness in handling insolvent credit institutions and at risk of collapse, preventing the spread of instability in the system and creating stability in the community.

Table 2.1.5: Summary of financial support activities

TT

TCBHTG | Area | Time support point | Amount (million VND) | Result | |

1 | QTD Phuong Tu | Hanoi | 2009 | 1000 | QTD has paid off the principal. |

2 | QTD Quy Son | Bac Giang | 2008 | 832 | QTD has paid off principal and interest and is operating normally. |

3 | QTD Duong Willow | Ha Tay | 2007 | 1,500 | QTD has paid off all principal and interest, normal operation |

4 | QTD Tay Ninh Rubber | Tay Ninh | 2006 | 1,000 | QTD has paid off principal and interest and is operating normally. |

5 | QTD Loc Son | Lam Dong | 2005 | 2,600 | QTD has paid off principal and interest and is operating normally. |

Total | 6,932 | ||||

Maybe you are interested!

-

Current status of deposit insurance policy - 3

Current status of deposit insurance policy - 3 -

Vietnam deposit insurance activities after the deposit insurance law - 2

Vietnam deposit insurance activities after the deposit insurance law - 2 -

Perfecting Vietnam's deposit insurance law in the current period - 1

Perfecting Vietnam's deposit insurance law in the current period - 1 -

Evaluating customer satisfaction with savings deposit services at National Citizen Commercial Joint Stock Bank NCB Tan Huong Transaction Office - 3

Evaluating customer satisfaction with savings deposit services at National Citizen Commercial Joint Stock Bank NCB Tan Huong Transaction Office - 3 -

Assessing the level of satisfaction of individual customers with savings deposit services at Saigon Commercial Joint Stock Bank SCB - Ninh Kieu Branch - 13

Assessing the level of satisfaction of individual customers with savings deposit services at Saigon Commercial Joint Stock Bank SCB - Ninh Kieu Branch - 13

* Source: Annual report of BHTGVN 2014

The Vietnam Deposit Insurance Corporation has provided loans to support 05 QTDNDs with a total amount of nearly 7 billion VND. Of these, 4/5 organizations have paid off their debts and returned to normal operations. Although the amount disbursed for this operation is not much, it contributes to strengthening the confidence of depositors in the credit institution system. The loan helps the Vietnam Deposit Insurance Corporation have a financial source to pay depositors, preventing the situation of mass early withdrawals due to the panic of depositors, which can lead to the risk of bankruptcy of banks and financial intermediaries. When knowing that the state financial organization, the Vietnam Deposit Insurance Corporation, is behind the operations of credit institutions and can provide financial support, depositors will feel secure and will not withdraw their money early. That means the rights and interests of depositors are better protected.

2.2.2. Activities of the Social Insurance Fund after the Law on Social Insurance

The main legal basis for current social insurance activities (attached appendix).

Current social insurance policies (attached appendix).

Current organizational chart of BHTVN (attached appendix).

Current business activities of BHTGVN:

2.2.2.1. Granting and revoking certificates of participation in deposit insurance

The Law on Deposit Insurance creates a legal framework for the issuance and revocation of deposit insurance certificates; enhances the position of the Vietnam Deposit Insurance; and aims to protect the legitimate rights and interests of depositors in an effective, public, and transparent manner. The Law on Deposit Insurance stipulates that at least 15 days before the opening date of operations, credit institutions must submit an application for a deposit insurance certificate. Within 05 working days from the date of receiving a complete application for a deposit insurance certificate, the Vietnam Deposit Insurance is responsible for issuing a deposit insurance certificate. In case the State Bank of Vietnam issues a document temporarily suspending deposit-receiving activities according to regulations, the deposit insurance certificate of the deposit insurance certificate will be temporarily revoked.

As of December 31, 2016, 1,266 credit institutions were granted deposit insurance certificates by the Vietnam Deposit Insurance Corporation, including 95 commercial banks, cooperative banks, 1,168 people's credit funds and 03 microfinance institutions. The Vietnam Deposit Insurance Corporation has done a good job of granting new, renewing and revoking deposit insurance certificates in a timely manner in accordance with regulations, and has well managed deposit insurance institutions through granting and revoking deposit insurance certificates to meet the needs of credit institutions, contributing to enhancing the position of the Vietnam Deposit Insurance Corporation and the public's trust in the banking system. In 2016 alone, the Vietnam Deposit Insurance Corporation has granted new, supplemented and reissued 733 certificates and copies of deposit insurance certificates.

BHTG, revoked 73 certificates and copies of CNTG BHTG, updated and changed 558 CNTG BHTG information.

2.2.2.2. Calculation and collection of deposit insurance premiums

According to the provisions of the Law on Deposit Insurance, the Prime Minister prescribes the deposit insurance fee framework upon the proposal of the State Bank. Based on the deposit insurance fee framework approved by the Prime Minister, the State Bank prescribes the specific deposit insurance fee level for each deposit insurance organization based on the results of the assessment and classification of this organization.

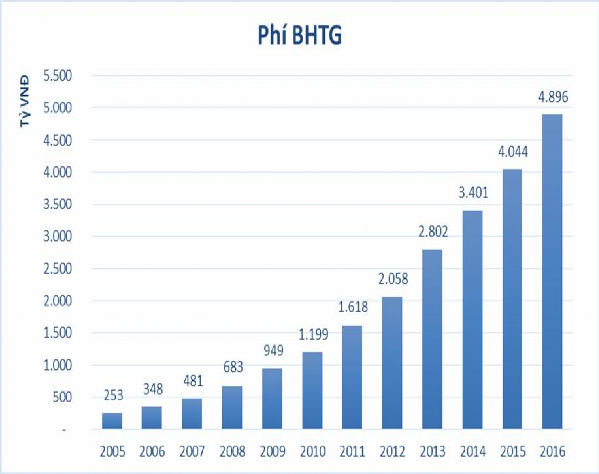

As of December 31, 2016, BHTGVN has collected fees from 1,266 deposit insurance institutions (including 11 credit institutions that do not incur deposit insurance fees) with the actual fee amount collected in the year reaching VND 4,896.7 billion, an increase of VND 852.4 billion (up 21%) compared to the same period in 2015, the total temporarily idle capital has been increased to VND 31,361.55 billion, the total assets of BHTGVN reached more than VND 33 trillion.

Number of TCTG BHTG

1,300

1,250

1,200

1,150

1,100

1,050

1,000

950

1,229 1,232

1,235

1,240

1,266

1,185

1.111

1.129

1,146

1,077

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Year

Number of TCTG BHTG

TCTG BHTG

Figure 2.2.1. Number of TCTG BHTG generating BHTG fees over the years (period from 2007 - 2016)

*Source: Annual report of BHTGVN

a. Deposit insurance fee and fee framework

Deposit insurance fee is the amount of money that the deposit receiving organization contributes to insure the deposits of insured depositors according to regulations. Regulations on calculating and collecting deposit insurance fees are implemented based on the average balance of individual deposits in Vietnamese Dong deposited at deposit insurance organizations. Currently, the deposit insurance fee is 0.15%/year on the total average insured balance, applied equally to all

all deposit insurance organizations. BHTGVN is urgently developing a deposit insurance fee project to submit to the State Bank for approval.

Deposit insurance premiums are an important tool in developing deposit insurance policies in each country. Developing appropriate deposit insurance premium policies not only helps ensure the financial capacity and ability to respond to risks of deposit insurance organizations but also creates fairness and healthy competition among deposit insurance organizations.

b. How to calculate and collect deposit insurance premiums, deadline for payment

* Calculate deposit insurance premium

1.The basis for calculating the deposit insurance premium of the premium collection quarter is the total average deposit balance of all types of insured deposits at the deposit insurance fund of the quarter immediately preceding the premium collection quarter.

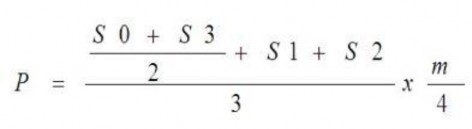

2.The amount of deposit insurance premium payable for the collection quarter is calculated by the following formula:

In there:

- P: is the deposit insurance premium payable for the fee collection quarter.

- S0: is the insured deposit balance at the beginning of the first month of the previous quarter adjacent to the fee collection quarter. S1, S2, S3: is the insured deposit balance at the end of the first, second and third months of the previous quarter adjacent to the fee collection quarter.

- m: is the deposit insurance premium payable.

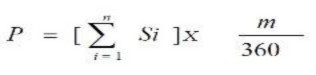

3.In case TCTG BHTG calculates and pays the fee for the first quarter of participating in BHTG, the following formula applies:

In which: - P: is the deposit insurance premium payable for the first quarter.

- Si: is the insured deposit balance on day i (i=1 →n); S1 is the insured deposit balance at the end of the first day of receiving the deposit; Sn is the insured deposit balance

last day of first quarter).

- m: is the deposit insurance premium payable.

4. The BHTG after merger or consolidation shall apply the formula for calculating the BHTG premium specified in Section 2 , in which S0 is the total insured deposit balance of the BHTG participating in the merger or consolidation at the beginning of the first month of the previous quarter adjacent to the premium collection quarter; S1, S2, S3 are the total insured deposit balances of the BHTG participating in the merger or consolidation at the end of the first, second, and third months of the previous quarter adjacent to the premium collection quarter.

5.Insured deposit balance, deposit insurance fee and late payment fee are rounded to the nearest thousand dong according to the following principle: greater than or equal to (≥) 500 dong is rounded up to 1,000 dong, less than (<) 500 dong is rounded down to 0 dong.

* Deadline for payment of deposit insurance premium

The BHTG fee is calculated and paid periodically every quarter of the fiscal year. No later than the 20th of the first month of the fee collection quarter, the BHTG TCTG must pay the BHTG fee to BHTGVN. In case the last day of the fee payment deadline falls on a holiday, Tet holiday, or weekend, the BHTG TCTG will pay on the next working day immediately following the holiday, Tet holiday, or weekend.

* Deposit insurance premium collection

All deposit insurance organizations calculate and pay premiums according to regulations. Units in the entire deposit insurance system of Vietnam have actively coordinated to monitor, urge, guide, resolve problems and handle violations in calculating and paying deposit insurance premiums for deposit insurance organizations. Deposit insurance organizations strictly comply with regulations on calculating and paying premiums to meet the requirements of improving the financial capacity of Vietnam deposit insurance, ensuring resources to better protect the interests of depositors.

In 2012, BHTGVN collected fees from 1,229 insured depository institutions with a total actual fee paid of over VND2,057 billion, an increase of over 27% compared to 2011. The total deposit balance subject to insurance was approximately VND1.5 million billion (in 2011, approximately VND1.1 million billion). In 2013, BHTGVN collected fees from 1,232 insured depository institutions with a total expected fee of over VND2,057 billion.

2,500 billion VND, an increase of more than 16% compared to 2012. BHTGVN is insuring more than 2 million billion VND deposited at BHTG banks. In 2014, BHTGVN collected fees from 1,235

TCTG BHTG, the accumulated BHTG premium collected since the beginning of the year is 3,400 billion VND. After the on-site inspection results, BHTGVN collected additional premiums from units that paid less than 14.4 billion VND. In 2015, BHTGVN collected premiums from 1,240 TCTG BHTG with the amount of 4,044 billion VND, an increase of 644 billion VND (an increase of 18.9%) compared to 2014. In 2015, Construction Joint Stock Commercial Bank paid nearly 31.3 billion VND for 03 premium collection periods: Quarter IV/2014; Quarter I, IV/2015. Thus, the BHTG premium of Construction Joint Stock Commercial Bank still has 02 premium collection periods that have not been paid (Quarter II, III/2015) with a total amount of more than 18.7 billion VND. BHTGVN has actively worked with this unit and advised the State Bank to handle and recover the outstanding fees in the context of implementing this bank restructuring project. In 2016, the entire system had 1,266 BHTG depository institutions paying BHTG fees (11 units did not incur BHTG fees), an increase of 15 BHTG depository institutions compared to the end of 2015, the collected BHTG fees were: 4,896 billion VND, an increase of 863 billion VND (up 21.4%) compared to 2015.

Figure 2.2.2: Social Insurance Fees Collected by Year

* Source: Annual report of BHTGVN

c. Advantages and disadvantages of deposit insurance policy

Deposit insurance premiums in Vietnam are applied at a fixed rate of 0.15% of the insured deposit balance for all deposit insurance institutions in Vietnam. The above premium rate has been applied since the beginning of deposit insurance activities until now. The flat premium has met the basic objectives of deposit insurance policy in Vietnam and is especially suitable for the initial stage of operation of the Vietnam Deposit Insurance.

The deposit insurance premium is applied uniformly to all deposit insurance organizations and the use of insured deposit balances as the basis for calculating the premium facilitates the calculation of the premium to be convenient, simple, and easy to check; at the same time, it minimizes the occurrence of complicated reports on data related to the calculation and payment of premiums. This facilitates the initial implementation of the deposit insurance policy. On the other hand, the deposit insurance premium revenue has contributed significantly to improving the financial capacity of the Vietnam Deposit Insurance. The size of the fund capital of the Vietnam Deposit Insurance has increased from VND 1,000 billion initially allocated by the Government to more than VND 9,896 billion by the end of 2016.

In addition to the above advantages, the uniform deposit insurance fee also reveals fundamental limitations. Insured deposits have increased rapidly while the deposit insurance fee has been maintained at a fixed level of 0.15% in recent times. This has caused the deposit insurance fund/insured deposit balance ratio to gradually decrease in recent years. From 1.07% in 2005 to about 0.8% in 2011 and by 2016, this ratio had decreased to 0.76%. On the other hand, the application of a uniform deposit insurance fee does not encourage credit institutions to improve safety and limit risks in operations, minimizing risks to enjoy low fees. This does not create motivation for fair competition among deposit insurance institutions.

Vietnam has successfully applied a uniform deposit insurance premium for all deposit insurance institutions in the early years of deposit insurance implementation. In response to the requirements of international integration, encouraging fair competition among credit institutions and improving the financial capacity of the Vietnam Deposit Insurance, the uniform deposit insurance premium is no longer suitable. The 2012 Law on Deposit Insurance assigned the Prime Minister to prescribe the deposit insurance premium framework upon the proposal of the State Bank of Vietnam. Based on this framework, the State Bank of Vietnam prescribes specific deposit insurance premium levels for deposit insurance institutions based on the results of the assessment and classification of these organizations.