high efficiency, on the other hand, PGD implemented measures to promote PGD image, advertise on radio, approach and attract some new businesses to transact at PGD, so the source of deposits mobilized from economic organizations in 2015 increased sharply with a rate of 30.69%, an increase of 30,323 million VND, accounting for 55.24% compared to 2014.

Thus, in the period 2013 - 2015, this deposit source accounted for the largest proportion of the total mobilized deposit source. This source is often large in scale, low in mobilization costs but unstable, depending heavily on the business performance of the partner. Therefore, PGD needs to introduce specific and flexible customer policies, clearly identify potential customers, offer appropriate incentives, and diversify service types to attract businesses to open accounts and conduct transactions at PGD.

2.2.3.2.Structure of deposit sources by currency

Fearing that the local currency may depreciate, people choose to keep money effectively by buying gold, real estate or strong foreign currencies. In order to meet the maximum needs of customers, PGD has continuously deployed many new forms of mobilization, including forms of mobilization by currency: mobilization by domestic currency deposits and mobilization by foreign currency deposits. The structure of mobilized deposits by currency is shown in the following table:

TABLE 2.11. DEPOSIT STRUCTURE BY CURRENCY TYPE

Unit: million VND

Target

2013 | 2014 | 2015 | |||

Value | Value | Increase Chief | Value | Increase Chief | |

Total funds send mobilization | 175,895 | 184,415 | 4.84% | 233,776 | 26.77% |

2.Classification by currency | |||||

- VND | 153,997 | 165,305 | 7.34% | 212,424 | 28.5% |

Proportion | 87.55% | 89.64% | 90.87% | ||

- Foreign currency (conversion) | 21,899 | 19.11 | - 12.74% | 21,351 | 11.73% |

Proportion | 12.45% | 10.36% | 9.13% | ||

Maybe you are interested!

-

Solutions for tourism development in Tien Lang - 10

zt2i3t4l5ee

zt2a3gstourism, tourism development

zt2a3ge

zc2o3n4t5e6n7ts

- District People's Committees and authorities of communes with tourist attractions should support, promote, and provide necessary information to people, helping them improve their knowledge about tourism. Raise tourism awareness for local people.

*

* *

Due to limited knowledge and research time, the thesis inevitably has shortcomings. Therefore, I look forward to receiving guidance from teachers, experts as well as your comments to make the thesis more complete.

Chapter III Conclusion

Through the issues presented in Chapter II, we can come to some conclusions:

Based on the strengths of available tourism resources, the types of tourism in Tien Lang that need to be promoted in the coming time are sightseeing and resort tourism, discovery tourism, weekend tourism. To improve the quality and diversify tourism products, Tien Lang district needs to combine with local cultural tourism resources, at the same time combine with surrounding areas, build rich tourism products. The strengths of Tien Lang tourism are eco-tourism and cultural tourism, so developing Tien Lang tourism must always go hand in hand with restoring and preserving types of cultural tourism resources. Some necessary measures to support and improve the efficiency of exploiting tourism resources in Tien Lang are: strengthening the construction of technical facilities and labor force serving tourism, actively promoting and advertising tourism, and expanding forms of capital mobilization for tourism development.

CONCLUDE

I Conclusion

1. Based on the results achieved within the framework of the thesis's needs, some basic conclusions can be drawn as follows:

Tien Lang is a locality with great potential for tourism development. The relatively abundant cultural tourism resources and ecological tourism resources have great appeal to tourists. Based on this potential, Tien Lang can build a unique tourism industry that is competitive enough with other localities within Hai Phong city and neighboring areas.

In recent years, the exploitation of the advantages of resources to develop tourism and build tourist routes in Tien Lang has not been commensurate with the available potential. In terms of quantity, many resource objects have not been brought into the purpose of tourism development. In terms of time, the regular service time has not been extended to attract more visitors. Infrastructure and technical facilities are still weak. The labor force is still thin and weak in terms of expertise. Tourism programs and routes have not been organized properly, the exploitation content is still monotonous, so it has not attracted many visitors. Although resources have not been mobilized much for tourism development, they are facing the risk of destruction and degradation.

2. Based on the results of investigation, analysis, synthesis, evaluation and selective absorption of research results of related topics, the thesis has proposed a number of necessary solutions to improve the efficiency of exploiting tourism resources in Tien Lang such as: promoting the restoration and conservation of tourism resources, focusing on investment and key exploitation of ecotourism resources, strengthening the construction of infrastructure and tourism workforce. Expanding forms of capital mobilization. In addition, the thesis has built a number of tourist routes of Hai Phong in which Tien Lang tourism resources play an important role.

Exploiting Tien Lang tourism resources for tourism development is currently facing many difficulties. The above measures, if applied synchronously, will likely bring new prospects for the local tourism industry, contributing to making Tien Lang tourism an important economic sector in the district's economic structure.

REFERENCES

1. Nhuan Ha, Trinh Minh Hien, Tran Phuong, Hai Phong - Historical and cultural relics, Hai Phong Publishing House, 1993

2. Hai Phong City History Council, Hai Phong Gazetteer, Hai Phong Publishing House, 1990.

3. Hai Phong City History Council, History of Tien Lang District Party Committee, Hai Phong Publishing House, 1990.

4. Hai Phong City History Council, University of Social Sciences and Humanities, VNU, Hai Phong Place Names Encyclopedia, Hai Phong Publishing House. 2001.

5. Law on Cultural Heritage and documents guiding its implementation, National Political Publishing House, Hanoi, 2003.

6. Tran Duc Thanh, Lecture on Tourism Geography, Faculty of Tourism, University of Social Sciences and Humanities, VNU, 2006

7. Hai Phong Center for Social Sciences and Humanities, Some typical cultural heritages of Hai Phong, Hai Phong Publishing House, 2001

8. Nguyen Ngoc Thao (editor-in-chief, Tourism Geography, Hai Phong Publishing House, two volumes (2001-2002)

9. Nguyen Minh Tue and group of authors, Hai Phong Tourism Geography, Ho Chi Minh City Publishing House, 1997.

10. Nguyen Thanh Son, Hai Phong Tourism Territory Organization, Associate Doctoral Thesis in Geological Geography, Hanoi, 1996.

11. Decision No. 2033/QD – UB on detailed planning of Tien Lang town, Hai Phong city until 2020.

12. Department of Culture, Information, Hai Phong Museum, Hai Phong relics

- National ranked scenic spot, Hai Phong Publishing House, 2005. 13. Tien Lang District People's Committee, Economic Development Planning -

Culture - Society of Tien Lang district to 2010.

14.Website www.HaiPhong.gov.vn

APPENDIX 1

List of national ranked monuments

STT

Name of the monument

Number, year of decisiondetermine

Location

1

Gam Temple

938 VH/QĐ04/08/1992

Cam Khe Village- Toan Thang commune

2

Doc Hau Temple

9381 VH/QĐ04/08/1992

Doc Hau Village –Toan Thang commune

3

Cuu Doi Communal House

3207 VH/QĐDecember 30, 1991

Zone II of townTien Lang

4

Ha Dai Temple

938 VH/QĐ04/08/1992

Ha Dai Village –Tien Thanh commune

APPENDIX II

STT

Name of the monument

Number, year of decision

Location

1

Phu Ke Pagoda Temple

178/QD-UBJanuary 28, 2005

Zone 1 - townTien Lang

2

Trung Lang Temple

178/QD-UBJanuary 28, 2005

Zone 4 – townTien Lang

3

Bao Khanh Pagoda

1900/QD-UBAugust 24, 2006

Nam Tu Village -Kien Thiet commune

4

Bach Da Pagoda

1792/QD-UB11/11/2002

Hung Thang Commune

5

Ngoc Dong Temple

177/QD-UBNovember 27, 2005

Tien Thanh Commune

6

Tomb of Minister TSNhu Van Lan

2848/QD-UBSeptember 19, 2003

Nam Tu Village -Kien Thiet commune

7

Canh Son Stone Temple

2160/QD-UBSeptember 19, 2003

Van Doi Commune –Doan Lap

8

Meiji Temple

2259/QD-UBSeptember 19, 2002

Toan Thang Commune

9

Tien Doi Noi Temple

477/QD-UBSeptember 19, 2005

Doan Lap Commune

10

Tu Doi Temple

177/QD-UBJanuary 28, 2005

Doan Lap Commune

11

Duyen Lao Temple

177/QD-UBJanuary 28, 2005

Tien Minh Commune

12

Dinh Xuan Uc Pagoda

177/QD-UBJanuary 28, 2005

Bac Hung Commune

13

Chu Khe Pagoda

177/QD-UBJanuary 28, 2005

Hung Thang Commune

14

Dong Dinh

2848/QD-UBNovember 21, 2002

Vinh Quang Commune

15

President's Memorial HouseTon Duc Thang

177/QD-UBJanuary 28, 2005

NT Quy Cao

Ha Dai Temple

Ben Vua Temple

Tien Lang hot spring

div.maincontent .p { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; } div.maincontent p { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; } div.maincontent .s1 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; font-size: 16pt; } div.maincontent .s2 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s3 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s4 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; font-size: 14pt; } div.maincontent .s5 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; font-size: 14pt; } div.maincontent .s6 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s7 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s8 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; vertical-align: 6pt; } div.maincontent .s9 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 12pt; } div.maincontent .s11 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; tex

Solutions for tourism development in Tien Lang - 10

zt2i3t4l5ee

zt2a3gstourism, tourism development

zt2a3ge

zc2o3n4t5e6n7ts

- District People's Committees and authorities of communes with tourist attractions should support, promote, and provide necessary information to people, helping them improve their knowledge about tourism. Raise tourism awareness for local people.

*

* *

Due to limited knowledge and research time, the thesis inevitably has shortcomings. Therefore, I look forward to receiving guidance from teachers, experts as well as your comments to make the thesis more complete.

Chapter III Conclusion

Through the issues presented in Chapter II, we can come to some conclusions:

Based on the strengths of available tourism resources, the types of tourism in Tien Lang that need to be promoted in the coming time are sightseeing and resort tourism, discovery tourism, weekend tourism. To improve the quality and diversify tourism products, Tien Lang district needs to combine with local cultural tourism resources, at the same time combine with surrounding areas, build rich tourism products. The strengths of Tien Lang tourism are eco-tourism and cultural tourism, so developing Tien Lang tourism must always go hand in hand with restoring and preserving types of cultural tourism resources. Some necessary measures to support and improve the efficiency of exploiting tourism resources in Tien Lang are: strengthening the construction of technical facilities and labor force serving tourism, actively promoting and advertising tourism, and expanding forms of capital mobilization for tourism development.

CONCLUDE

I Conclusion

1. Based on the results achieved within the framework of the thesis's needs, some basic conclusions can be drawn as follows:

Tien Lang is a locality with great potential for tourism development. The relatively abundant cultural tourism resources and ecological tourism resources have great appeal to tourists. Based on this potential, Tien Lang can build a unique tourism industry that is competitive enough with other localities within Hai Phong city and neighboring areas.

In recent years, the exploitation of the advantages of resources to develop tourism and build tourist routes in Tien Lang has not been commensurate with the available potential. In terms of quantity, many resource objects have not been brought into the purpose of tourism development. In terms of time, the regular service time has not been extended to attract more visitors. Infrastructure and technical facilities are still weak. The labor force is still thin and weak in terms of expertise. Tourism programs and routes have not been organized properly, the exploitation content is still monotonous, so it has not attracted many visitors. Although resources have not been mobilized much for tourism development, they are facing the risk of destruction and degradation.

2. Based on the results of investigation, analysis, synthesis, evaluation and selective absorption of research results of related topics, the thesis has proposed a number of necessary solutions to improve the efficiency of exploiting tourism resources in Tien Lang such as: promoting the restoration and conservation of tourism resources, focusing on investment and key exploitation of ecotourism resources, strengthening the construction of infrastructure and tourism workforce. Expanding forms of capital mobilization. In addition, the thesis has built a number of tourist routes of Hai Phong in which Tien Lang tourism resources play an important role.

Exploiting Tien Lang tourism resources for tourism development is currently facing many difficulties. The above measures, if applied synchronously, will likely bring new prospects for the local tourism industry, contributing to making Tien Lang tourism an important economic sector in the district's economic structure.

REFERENCES

1. Nhuan Ha, Trinh Minh Hien, Tran Phuong, Hai Phong - Historical and cultural relics, Hai Phong Publishing House, 1993

2. Hai Phong City History Council, Hai Phong Gazetteer, Hai Phong Publishing House, 1990.

3. Hai Phong City History Council, History of Tien Lang District Party Committee, Hai Phong Publishing House, 1990.

4. Hai Phong City History Council, University of Social Sciences and Humanities, VNU, Hai Phong Place Names Encyclopedia, Hai Phong Publishing House. 2001.

5. Law on Cultural Heritage and documents guiding its implementation, National Political Publishing House, Hanoi, 2003.

6. Tran Duc Thanh, Lecture on Tourism Geography, Faculty of Tourism, University of Social Sciences and Humanities, VNU, 2006

7. Hai Phong Center for Social Sciences and Humanities, Some typical cultural heritages of Hai Phong, Hai Phong Publishing House, 2001

8. Nguyen Ngoc Thao (editor-in-chief, Tourism Geography, Hai Phong Publishing House, two volumes (2001-2002)

9. Nguyen Minh Tue and group of authors, Hai Phong Tourism Geography, Ho Chi Minh City Publishing House, 1997.

10. Nguyen Thanh Son, Hai Phong Tourism Territory Organization, Associate Doctoral Thesis in Geological Geography, Hanoi, 1996.

11. Decision No. 2033/QD – UB on detailed planning of Tien Lang town, Hai Phong city until 2020.

12. Department of Culture, Information, Hai Phong Museum, Hai Phong relics

- National ranked scenic spot, Hai Phong Publishing House, 2005. 13. Tien Lang District People's Committee, Economic Development Planning -

Culture - Society of Tien Lang district to 2010.

14.Website www.HaiPhong.gov.vn

APPENDIX 1

List of national ranked monuments

STT

Name of the monument

Number, year of decisiondetermine

Location

1

Gam Temple

938 VH/QĐ04/08/1992

Cam Khe Village- Toan Thang commune

2

Doc Hau Temple

9381 VH/QĐ04/08/1992

Doc Hau Village –Toan Thang commune

3

Cuu Doi Communal House

3207 VH/QĐDecember 30, 1991

Zone II of townTien Lang

4

Ha Dai Temple

938 VH/QĐ04/08/1992

Ha Dai Village –Tien Thanh commune

APPENDIX II

STT

Name of the monument

Number, year of decision

Location

1

Phu Ke Pagoda Temple

178/QD-UBJanuary 28, 2005

Zone 1 - townTien Lang

2

Trung Lang Temple

178/QD-UBJanuary 28, 2005

Zone 4 – townTien Lang

3

Bao Khanh Pagoda

1900/QD-UBAugust 24, 2006

Nam Tu Village -Kien Thiet commune

4

Bach Da Pagoda

1792/QD-UB11/11/2002

Hung Thang Commune

5

Ngoc Dong Temple

177/QD-UBNovember 27, 2005

Tien Thanh Commune

6

Tomb of Minister TSNhu Van Lan

2848/QD-UBSeptember 19, 2003

Nam Tu Village -Kien Thiet commune

7

Canh Son Stone Temple

2160/QD-UBSeptember 19, 2003

Van Doi Commune –Doan Lap

8

Meiji Temple

2259/QD-UBSeptember 19, 2002

Toan Thang Commune

9

Tien Doi Noi Temple

477/QD-UBSeptember 19, 2005

Doan Lap Commune

10

Tu Doi Temple

177/QD-UBJanuary 28, 2005

Doan Lap Commune

11

Duyen Lao Temple

177/QD-UBJanuary 28, 2005

Tien Minh Commune

12

Dinh Xuan Uc Pagoda

177/QD-UBJanuary 28, 2005

Bac Hung Commune

13

Chu Khe Pagoda

177/QD-UBJanuary 28, 2005

Hung Thang Commune

14

Dong Dinh

2848/QD-UBNovember 21, 2002

Vinh Quang Commune

15

President's Memorial HouseTon Duc Thang

177/QD-UBJanuary 28, 2005

NT Quy Cao

Ha Dai Temple

Ben Vua Temple

Tien Lang hot spring

div.maincontent .p { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; } div.maincontent p { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; } div.maincontent .s1 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; font-size: 16pt; } div.maincontent .s2 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s3 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s4 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; font-size: 14pt; } div.maincontent .s5 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; font-size: 14pt; } div.maincontent .s6 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s7 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s8 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; vertical-align: 6pt; } div.maincontent .s9 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 12pt; } div.maincontent .s11 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; tex -

Evaluating customer satisfaction with savings deposit services at National Citizen Commercial Joint Stock Bank NCB Tan Huong Transaction Office - 3

Evaluating customer satisfaction with savings deposit services at National Citizen Commercial Joint Stock Bank NCB Tan Huong Transaction Office - 3 -

Impact of Financial Market Development on Enterprise Capital Structure by National Institutional Quality

Impact of Financial Market Development on Enterprise Capital Structure by National Institutional Quality -

The impact of financial market development on the capital structure of listed enterprises in the ASEAN Economic Community - 28

The impact of financial market development on the capital structure of listed enterprises in the ASEAN Economic Community - 28 -

Analysis of Capital Structure and Cost of Capital at Some Typical Enterprises

Analysis of Capital Structure and Cost of Capital at Some Typical Enterprises

(Source: Business results report of ACB Commercial Joint Stock Bank – Hanoi Branch –

Thanh Nhan Transaction Office 2013-2015)

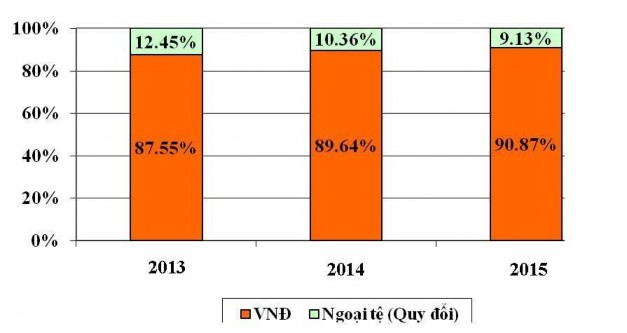

Chart 2.3: Structure of mobilized deposits classified by currency type

(Source: Business results report of ACB Commercial Joint Stock Bank – Hanoi Branch –

Thanh Nhan Transaction Office 2013-2015)

Mobilization by local currency deposits

Based on the data table and analysis chart, we can see that the main source of mobilized deposits of PGD is the source of mobilized deposits in domestic currency. On average, this source accounts for over 80% of the total mobilized deposits and has a fairly good growth rate. In 2014, the mobilized domestic currency deposits increased by 7.34%, equivalent to 11,308 million VND compared to 2013, accounting for 89.64% of the total mobilized capital. In 2015, this source increased sharply with an increase rate of 28.5%, equivalent to 47,119 million VND compared to 2014, accounting for 90.87% of the total mobilized deposits.

In a competitive environment, commercial banks are always ready to offer higher interest rates, PGD has strived to diversify its deposit forms such as Dai Loc savings, Loc Bao Toan savings, promotional savings, prize savings, etc. to attract more customers. In parallel with finding new customers, PGD also offers preferential policies for long-term customers, strengthening their loyalty. Therefore, in the context of fierce competition among banks in the market, the source of mobilized domestic currency deposits is still increasing, accounting for a stable proportion.

Mobilization in foreign currency

Through the table, the source of foreign currency deposits mobilized by PGD has tended to decrease in recent years. In 2014, this source of capital decreased by 12.74% compared to 2013, accounting for 10.36% of the total mobilized deposits. In 2015, the world economy improved, along with the constant efforts of PGD staff, the amount of foreign currency mobilized increased sharply compared to 2014 with an increase rate of 11.73%, equivalent to 2,241 million VND, accounting for 9.13% of the total mobilized deposits.

2.2.3.3 Structure of deposit sources classified by term

According to the deposit term, the structure of mobilized deposits divided by term includes: demand deposits and term deposits. Currently, according to ACB's regulations, term deposits are divided into 3 types: term deposits under 12 months, term deposits from 12 - 24 months and term deposits over 24 months. The structure of mobilized deposits divided by term in the period 2013 - 2015 of Thanh Nhan Transaction Office is shown in the following table:

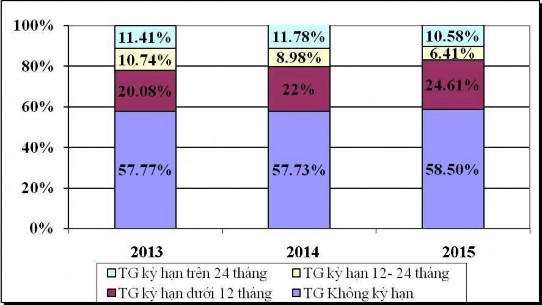

TABLE 2.12. DEPOSIT STRUCTURE BY TERM

Unit: million VND

Target

2013 | 2014 | 2015 | ||||

Value | Value | Increase Chief | Value | Increase Chief | ||

Total deposits mobilize | 175,895 | 184,415 | 4.84% | 233,776 | 26.77% | |

3. Classify by term | ||||||

- No term | 101,590 | 105,546 | 3.89% | 136,754 | 29.57% | |

Proportion | 57.77% | 57.23% | 58.5% | |||

-Term under 12 months | 35,321 | 38,578 | 14.88% | 57,298 | 41.2% | |

Proportion | 20.08% | 22% | 24.61% | |||

-Term from 12-24 months | 18,897 | 16,564 | -12.35% | 14,986 | -9.53% | |

Proportion | 10.74% | 8.98% | 6.41% | |||

- Term over 24 months | 20,087 | 21,727 | 8.16% | 24,738 | 13.86% | |

Proportion | 11.41% | 11.78% | 10.58% | |||

(Source: Business results report of ACB Commercial Joint Stock Bank – Hanoi Branch –

Thanh Nhan Transaction Office 2013-2015)

Chart 2.4: Deposit structure by term

(Source: Business results report of ACB Commercial Joint Stock Bank – Hanoi Branch –

Thanh Nhan Transaction Office in 2013-2015) Based on the data table and analysis chart, we see that the source of mobilized non-term deposits accounts for the largest proportion in the total mobilized deposits of the transaction office, followed by the source of deposits with terms of less than 12 months. The sources of funds are classified as

This type of product has been growing over the years.

Non-term deposit source

This source of money is mainly payment deposits of individuals and businesses in the area. In the period 2013 - 2015, this source of money grew strongly. In 2014, the growth rate was only 3.89%, equivalent to 3,956 million VND compared to 2013, accounting for 57.23% of the deposit source, but by 2015 this rate had reached29.57%, equivalent to 31,208 million VND, accounting for 58.5% of total deposits. This achievement is due to the PGD proactively seeking potential customers, offering utilities for the services provided: fast payment, high accuracy, safety and security.

Term deposits under 12 months

This source of money mainly includes term deposits and savings deposits with a term of less than 12 months. Like non-term deposits, this source of money also accounts for a large proportion of total deposits and has a fairly high growth rate. In 2014, this source of money grew by 14.88% compared to 2013, accounting for 22% of total mobilized deposits. Because ACB is one of the

leading commercial banks with high reputation in the market; in addition, the branch carried out many marketing activities, expanding customer relations, so this source of money in 2015 increased at a rate nearly three times higher than the growth rate of the previous year, up 41.2% compared to 2014, equivalent to 18,720 million VND, accounting for 24.61% of the total deposit source.

Currently, short-term deposits are popular with people. This is because the Vietnamese Dong is depreciating, the consumer price index is increasing dramatically, people mainly keep money for consumption or deposit money in banks with short terms. On the other hand, due to the emergence of many new attractive investment channels such as stocks, real estate, short-term deposits can help people be flexible in investing. Short-term deposits account for a large proportion of the total mobilized deposits, posing a challenge for PGDs on how to be proactive in medium and long-term lending.

Term deposits from 12-24 months

This is a source of money including medium-term deposits and is mainly used to finance medium-term investment projects. This source of money accounts for the smallest proportion of the total mobilized deposits of PGD and has also decreased significantly in the past period. In 2014, this source of money decreased sharply by 12.35% compared to 2013, accounting for 8.98% of the total mobilized deposits. By 2015, it decreased by 9.53%, equivalent to 1,578 million VND compared to 2014, accounting for only 6.41% of the total customer deposits. The reason for the sharp decrease in this source of money in recent years is due to the nature of medium-term deposits - deposits with lower interest rates than long-term deposits. When wanting to receive high interest rates and long-term deposits, customers will choose long-term deposits. When the economic situation is still volatile like today, customers will choose short-term deposit solutions.

Term deposits over 24 months

This is a source of money including long-term deposits and used to finance long-term investment projects of PGD. In the period of 2013 - 2015, this form of mobilization of PGD has increased sharply. In 2014, the growth rate was 8.16%, equivalent to 1,640 VND compared to 2014, accounting for 11.78% of total customer deposits. By 2015, the growth rate was up to 13.86%, accounting for 10.58% of total deposits. The source of long-term deposits has grown steadily over the years, showing that the stable source of capital to finance long-term projects is on the rise. In the current difficult economic conditions, PGD's proactive mobilization of

Long-term deposits, maintaining good growth momentum, show that the Board of Directors' direction in deposit mobilization is on the right track.

Looking at the overall structure of deposit sources by term, in 2013 the proportion of non-term deposits was 57.77%, short-term deposits was 20.08%, medium and long-term deposits were 10.74% and 11.41% respectively, in 2014 and 2015 the proportion of non-term deposits, short-term deposits and medium and long-term deposits were 57.73%, 22%, 8.98%, 11.78% and 58.50%, 24.61%, 6.41%, 10.58% respectively. Thus, in general, medium and long-term deposits are much lower than short-term and non-term deposits, which affects the bank's lending capacity. PDG should focus on measures to increase medium and long-term deposits such as increasing deposit interest rates... to increase this deposit source for PGD.

Factors affecting capital mobilization activities at Thanh Nhan Branch

2.2.4.1 Subjective factors

Technology level

Staff and workers at Thanh Nhan Branch are exposed to the most modern and advanced technology, but there are still some limitations such as PDG does not have its own information technology department, and online money transfer and payment packages are still not widely used by customers, causing the loss of a number of customers to the Branch.

Reception level

PGD has paid great attention to the conduct of its staff. All staff of PGD need to have good professional qualifications and good professional ethics, which is one of the necessary requirements to attract customers to PGD Thanh Nhan in the modern economic era. At the end of the working day, some staff are not dedicated to customers coming to PGD, making customers dissatisfied.

Network

In the current economic development, to grasp the customer's taste in the best way, all departments in the transaction office must have close links to support each other thoroughly. Thanh Nhan transaction office is still not closely linked with the transaction offices of the Bank in the area.

Interest rate

The first thing that any individual or economic organization wants to refer to when depositing money in a bank is the interest rate. PGD has set goals to find appropriate interest rates for each type of product and each target.

customers so as not to miss any potential customers when they come to PGD such as savings for settling down, savings for little angels... but PGD must always look for product packages with more attractive interest rates to attract customers.

Form of capital mobilization deposits

PGD has many forms of capital mobilization, deposits and terms, rich, diverse, flexible to serve all customers. However, PGD is still limited in promoting the Bank's product packages, not focusing on specific and clear advice on capital mobilization forms, making customers coming to PGD still confused.

Deposit mobilization structure

PGD should study the market and customer needs to come up with a reasonable capital mobilization structure without affecting costs. Hanoi is the capital city where many large and small businesses are concentrated, so PGD should have policies to attract this customer base.

PGD's reputation and brand

Thanh Nhan Branch has been operating for many years with the quality and reputation it has today thanks to the collective of staff and workers. However, the Branch still has to try harder so that ACB's brand will gain more and more trust from the people. This is a form of promotion for the Branch in particular and ACB Commercial Joint Stock Bank in general.

2.2.4.2 Objective factors

Economic environment

The economic environment will determine people's income. It will then affect the capital demand and the amount of deposits of customers. Therefore, it has a strong impact on the capital mobilization activities of PGD, so PGD Thanh Nhan should have policies to attract traditional customers and new customers with attractive product packages such as savings with high interest rates and capital safety. Moreover, a country's monetary policy will directly affect the capital mobilization activities of banks...

Political and legal environment

To ensure the equitable development of all economic sectors, each country must have a certain institution to regulate and supervise the compliance with the law of all subjects in the economy. Any business activity must be subject to strict regulation and supervision by the law and competent authorities. Adjustment of the State Bank of Vietnam on financial policy

Currency also strongly affects the operation of the bank. Therefore, Thanh Nhan Branch is also affected more or less by these things.

Competitive environment

Located in a favorable and developed economic region, there are many branches and transaction offices of major banks such as Vietcombank, Viettinbank, Lienvietbank,... competing in all aspects. Thanh Nhan Transaction Office must have clear goals and directions to attract customers to the transaction office.

Customer

PGD must understand the psychology of its customers to find the most suitable policies so as not to miss any customers when they come to PGD. High interest rates, capital safety, convenient services, fast and accurate are the top psychological factors that customers come to the Bank. The more customers trust the bank, the more stable the bank's cash flow and inflow will be, creating better conditions for the bank to mobilize capital for itself.

2.2.5 Efficiency of capital mobilization of Thanh Nhan Branch

In today's fiercely competitive economy, capital mobilization is a matter of survival for commercial banks to maintain and improve business efficiency, meet the capital needs of the economy, and bring high profits to banks. In order to expand market share and mobilize more and more deposits from economic organizations and residents, banks compete with each other in all aspects: technology, product and service quality, location, infrastructure facilities... In which, the important factor that needs to be mentioned is the mobilization interest rate.

In the total cost of mobilized capital, the interest expense payable on mobilized capital is an important factor and greatly affects the quality and business efficiency of the transaction office. It accounts for the largest proportion and fluctuates the most. Increasing mobilized capital in the condition that the interest expense payable on mobilized capital is too high will cause difficulties in resolving the output of capital or reduce the bank's profits. Therefore, considering the interest expense payable on mobilized capital and the fluctuation of this expense is considered a regular task in the management of mobilized capital, an important content in assessing the capital mobilization situation of the bank.

The regulation of ceiling interest rates for commercial banks by the State Bank of Vietnam helps the interest rate situation to be quite stable and the temporary interest rate is not a competitive tool for banks. However, ACB Commercial Joint Stock Bank also needs to diversify.