Products at other banks are still traditional and lack innovation, so it is difficult to attract attention and customers.

The software system still has problems and network congestion when there are too many accesses, especially on peak days such as the beginning of the month and the end of the month, causing customers to waste a lot of time waiting for transactions. Moreover, because the program does not support calculations, when customers agree to participate in some products such as: savings interest transferred to ATM cards, personal account transfer to savings books, etc., the transaction officer has to monitor by hand for a long time, so the transaction officer is reluctant to advise the customer. Therefore, these accompanying utilities can be missed and not implemented if the bank staff forgets or the customer goes to another transaction point to make a transaction, easily leading to an unprofessional image of the bank in the eyes of customers.

The capacity and qualifications of the staff are still limited. Although DongA Bank staff are young and dynamic, their professional expertise is not uniform, leading to incorrect accounting, lack of advice on savings products, etc., wasting customers' time.

Currently, compared to some other banks, the facilities at DongA Bank are still quite limited such as: lack of VIP rooms for customers, lack of computers for customers to operate, inconvenient parking lots... this will be the reason why DongA Bank misses a number of potential savings customers. In particular, in the past, the 24-hour system was a competitive advantage of DongA Bank compared to other banks. However, the removal of this transaction system has changed the transaction habits of many savings customers.

Troubleshooting and complaint resolution at DongA Bank still has many shortcomings when the bank's hotline number 1900545464 often has a busy signal or cannot be connected, causing a waste of time and discomfort when savings customers need to contact in case of emergency or have questions.

DongA Bank has not yet taken advantage of the indirect marketing channel from the bank's existing customers through customer care, process improvement, and services so that customers can introduce the bank to their friends, relatives, and partners.

In addition, customer care is still quite passive, lacking a specialized department, causing employees to work responsibly and lack enthusiasm for customers. In addition, the bank has not conducted surveys to find out customer opinions, so a small misunderstanding or mistake can lead to losing customers.

2.2.3.2 Causes of limitations

In recent years, our country's economy has been quite complicated, production and business activities have encountered many difficulties, people's income has decreased... which has significantly affected the business activities of the banking industry in general and DongA Bank in particular.

The State Bank's application of interest rate ceilings has caused many difficulties in mobilizing savings deposits at DongA Bank when it has to compete with large banks.

In the market, there are more and more banks and non-bank credit institutions with the function of mobilizing deposits, making the market share of each bank increasingly narrow. To attract customers, rival banks are increasing marketing and advertising while offering more attractive mobilization products. Meanwhile, DongA Bank is slow to implement these measures.

DongA Bank has not yet developed a specific strategy for mobilizing savings deposits, still leaning towards traditional forms of mobilization and lacking initiative, so marketing and customer care still have many shortcomings.

The reason for the uneven level of staff is that the recruitment and training of staff at DongA Bank has not been focused on and is not systematic in all stages. New employees recruited to DongA Bank are only trained by old employees through the observation process.

Although DongA Bank has invested in developing the Core Banking system, it still cannot meet the practical needs of developing diverse products and services, so DongA Bank still has network congestion and employees have to monitor some new products and services.

Above are the achievements, limitations and causes of limitations in the mobilization of savings deposits at DongA Bank. Therefore, DongA Bank needs to promote the achievements and solve the causes, seriously overcome the limitations to attract more and more customers to deposit savings.

2.3 Testing factors affecting customer satisfaction with savings deposit services at Dong A Bank

2.3.1 Research design

2.3.1.1 Research process

The research process is carried out in two phases: (Refer to Appendix 4 - Research process diagram).

Phase 1: Qualitative research based on factors expected to affect customer satisfaction with savings deposit services at Dong A Bank as stated in chapter 1.

Phase 2: Quantitative research to determine the factors that actually affect customer satisfaction with savings deposit services at Dong A Bank.

2.3.1.2 Research methods

The thesis uses the method of synthesis, comparison, descriptive statistics, analysis and evaluation of factors affecting customer satisfaction with savings deposit services at Dong A Bank. In addition, in the official research phase, the data collection technique is interviews through questionnaires. The collected data is processed using SPSS 20 software. After coding and cleaning, the data will undergo the following official analysis:

- Assessing the reliability of the scales: the reliability of the scale is assessed through the Cronbach's Alpha coefficient, through which inappropriate variables will be eliminated if the total correlation coefficient is small (<0.3). The scale has significant reliability when the Cronbach's Alpha coefficient is greater than 0.7 and the measurement scale has a Cronbach's Alpha coefficient from 0.8 to 1 is the best measurement scale (According to Hoang Trong and Chu Nguyen Mong Ngoc, 2008)

- Next, to test the convergence of observed variables, the author uses the EFA (Exploratory Factor Analysis) method. Variables with a simple correlation coefficient between the variable and the factors (factor loading) less than 0.5 will be eliminated.

- Testing structural model hypotheses and overall model fit. Multivariate regression model and testing at 5% significance level:

Satisfaction = β0 + β1 * Bank image + β2 * Financial benefits + β3 * Security + β4 * Convenience + β5 * Products and services + β6 * Staff + β7 * Recommendation.

2.3.1.3 Scale design

In the study, the author uses an interval scale because it is a highly accurate scale and is widely used in statistical analysis. All observed variables in the factors use a 5-point Likert scale. With option 1 meaning “completely disagree” with the statement to option 5 meaning “completely agree” with the statement. Because the 5-point Likert scale is widely used and suitable for the characteristics of the research problem (Refer to Appendix 7 - Scale coding).

2.3.1.4 Sample design

* Sample size

In exploratory factor analysis (EFA), sample size is often determined based on the minimum size and number of measurement variables included in the analysis. According to Hair et al. (1998), to be able to analyze EFA, the minimum sample size must be

50, preferably 100. The ratio of observations/items is 5:1, meaning that a data set with at least 5 samples per item is needed. In this study, with 25 items, the minimum number of observations is 5 x 25 = 125.

In addition, to conduct regression analysis, Tabachnick and Fidell (1996) suggested that the sample size must be ensured according to the formula: n > = 8m + 50. In which: n is the sample size and m is the number of independent variables of the model.

In the study, with the number of independent variables being m= 7, the minimum number of observed samples is: n>= 8 x 7 + 50 = 106. Based on that and the principle that the larger the sample, the better, the author collected data with a sample size such that n> 150.

* How to take sample

In the research, the author uses the convenience sampling method. This is a non-probability sampling method, the author approaches the sample elements by the convenience method (According to Nguyen Dinh Tho, 2012). That is, in this convenience sampling method, any customer who agrees to participate in the interview when transacting at the transaction offices, branches, and transaction offices of DongA Bank can be selected for the sample.

2.3.2 Qualitative research

The preliminary study mainly focused on interviews and one-on-one discussions with 14 people, including 9 bank employees (including 1 deputy manager of operations, 4 tellers and 4 staff from the business development department) and 5 customers who have used savings deposit services at joint stock commercial banks in Ho Chi Minh City based on a pre-prepared preliminary interview sheet (Refer to Appendix 2 - Discussion on savings deposit services).

Among the 14 participants in the one-on-one discussion, there were 6 men and 8 women between the ages of 24 and 56. The preliminary results of the study were as follows:

- Regarding the time of using the savings service: all participants in the preliminary survey have used the savings service for over a year, so they have some experience in choosing and evaluating banks when making savings deposits.

- Regarding the statements of the scales: all 14 participants in the preliminary survey understood the meaning of the statements.

There are 3 people who think that the criterion “Having many social activities, for the community” should be made a part of the Bank Brand factor. Considering that when banks regularly have sponsorship programs, community activities will help many people know about the program, leading to knowledge and good impressions of the bank brand, the author will add an observation variable to make the criterion “Having many social activities, for the community” a component of the Bank Brand factor.

Regarding the factor of the staff, 4 interviewees who are customers who deposit savings believe that nowadays, the appearance of the staff includes: appropriate clothing, age, dynamism, appearance... will make them feel the professionalism and dynamism of the bank and attract them to make more transactions. Considering that the transaction staff are the representatives of the Bank who directly contact customers, their image will partly affect the image of the bank in the perception of customers, so the author will include 2 criteria "DongA Bank staff's clothing is neat and suitable" and "DongA Bank staff are young, dynamic, and good-looking" in the factor of the staff.

In addition, 3 of the interviewees said that: in a family, if there is a family member working at a bank, it will greatly affect customer satisfaction. Because, family members will feel more secure when their relatives work at the bank where they deposit money. In addition, some customers will have the mentality of "supporting" their relatives in implementing the bank's capital mobilization target. Considering the above opinion is reasonable, the author will include the criterion: "Having relatives working at DongA Bank" in the Referral factor.

The purpose of the preliminary study is to check the clarity of the words, assess the accuracy of the meaning of each statement, and search for new statements. The interview content will be recorded to serve as a basis for editing and supplementing.

supplement the observed variables in the scale. The result of this preliminary study is a questionnaire ready for the formal quantitative research step.

2.3.3 Quantitative research

2.3.3.1 Descriptive statistics of the research sample

The questionnaire (Refer to Appendix 1 - Customer opinion survey form) was sent to the sample subjects in 2 forms: directly distributing the survey form to customers and sending the survey form online via email and social networks during the period from April 2014 to September 2014. The results obtained are as follows:

- Out of 190 questionnaires distributed directly at the Transaction Office, branches, transaction offices of Dong A Bank and other survey subjects. The results obtained 150 valid survey forms and 40 invalid survey forms because the survey forms had many blank spaces and the interview subjects had never deposited savings at Dong A Bank.

- Of the 100 online survey questionnaires sent, 65 were valid and 35 were invalid because the interviewees had never made a savings deposit or had never made a savings deposit at Dong A Bank.

Thus, the total number of valid samples collected is 215 observation units, meeting the condition that the sample size must be from 150 or more. The following are the characteristics of customers depositing savings at Dong A Bank, through the 215 collected survey samples (Refer to Appendix 8 - Descriptive statistics of qualitative variables).

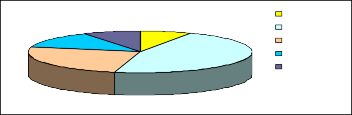

* Description of study sample by age

8.4%

7.4%

13.0%

Under 20

From 20-34

From 35-44

From 45-59

Over 60

25.1%

46.0%

Figure 2.3 Customer survey results by age

(Source: From author's survey results)

From chart 2.3 on customer survey results by age, it shows that the surveyed customers are mainly in the age group of 20-44 years old (in which the age group of 20-34 years old)

accounting for the highest proportion, followed by the group over 35-44 years old). Because in this period, most customers are working and have stable jobs, they often set aside a portion of their income to save for the future. Next is the group of customers aged 45-59 and the group over 60 years old, accounting for an average proportion because at this age, customers are about to retire or have retired, so they tend to save to earn interest to cover living expenses. Finally, the group under 20 years old has the lowest proportion because these customers are mainly students, so they do not have much money to save.

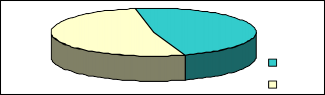

* Description of the study sample by gender

47.9%

Male

Female

52.1%

Figure 2.4 Customer survey results by gender

(Source: From author's survey results)

From the chart 2.4 on the results of the customer survey by gender, it can be seen that the distribution of male and female customers is relatively even. However, the number of female customers is about 52.1%, higher than the number of male customers is 47.9%. This is consistent with the reality of the importance of women in the family, usually women are the ones who keep the money, have decisions about money management in the family.

* Description of the study sample by educational level

Table 2.5 Customer survey results by education level

EDUCATION

Frequency | Part hundred | Percent valid | Percent accumulate | ||

Value | High school or below | 34 | 15.8 | 15.8 | 15.8 |

College / Secondary | 62 | 28.8 | 28.8 | 44.7 | |

University | 104 | 48.4 | 48.4 | 93.0 | |

After Postgraduate | 15 | 7.0 | 7.0 | 100.0 | |

Total | 215 | 100.0 | 100.0 | ||

Maybe you are interested!

-

Factors affecting customer satisfaction with the quality of international money transfer services at Dong A Commercial Joint Stock Bank - 1

Factors affecting customer satisfaction with the quality of international money transfer services at Dong A Commercial Joint Stock Bank - 1 -

Factors affecting customer loyalty to international payment services at Asia Commercial Joint Stock Bank - 12

Factors affecting customer loyalty to international payment services at Asia Commercial Joint Stock Bank - 12 -

Factors affecting job satisfaction of employees of Joint Stock Commercial Bank for Foreign Trade of Vietnam in Ho Chi Minh City - 17

Factors affecting job satisfaction of employees of Joint Stock Commercial Bank for Foreign Trade of Vietnam in Ho Chi Minh City - 17 -

Relationship marketing factors affecting customer loyalty to Vietnam Joint Stock Commercial Bank for Investment and Development in Ho Chi Minh City - 2

Relationship marketing factors affecting customer loyalty to Vietnam Joint Stock Commercial Bank for Investment and Development in Ho Chi Minh City - 2 -

Factors affecting customer loyalty to retail banking services at Dong A Commercial Joint Stock Bank, District 5 branch - 2

Factors affecting customer loyalty to retail banking services at Dong A Commercial Joint Stock Bank, District 5 branch - 2

(Source: From author's survey results)

From the data in Table 2.5 describing the educational level of surveyed customers, it shows that the majority of customers have a relatively high level of education (the highest being the level of education).