faster than lending to large corporate customers, this proves that the efficiency in lending to SME customers is not high.

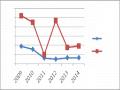

Total income from lending activities tends to increase gradually over the years, in 2017 it reached 139,055 million VND, in 2018 it increased to 184,585 million VND (an increase of 32.74% corresponding to 45,529 million VND). By 2019, it reached a value of

220,597 million VND (up 19.51% equivalent to 36,013 million VND).

The total income of the Bank tends to increase gradually over the years, in 2017 it reached 208,583 million VND, in 2018 it increased to 276,877 million VND (an increase of 32.74% corresponding to 68,294 million VND). By 2019, it reached a value of 330,896 million VND (an increase of 19.51% corresponding to 54,019 million VND).

Maybe you are interested!

-

Evaluation of SHB's Business Performance After Merger According to Camel Model

Evaluation of SHB's Business Performance After Merger According to Camel Model -

Improving the effectiveness of Can Tho Insurance Company's business strategy - 1

Improving the effectiveness of Can Tho Insurance Company's business strategy - 1 -

NHTM's Business Performance Evaluation Indicators

NHTM's Business Performance Evaluation Indicators -

Quality of life of Alzheimer's patients, caregivers and evaluation of the effectiveness of some non-pharmacological interventions - 6

Quality of life of Alzheimer's patients, caregivers and evaluation of the effectiveness of some non-pharmacological interventions - 6 -

Evaluation of the effectiveness of the Forest Environmental Services Payment Policy on forest management and protection, improving people's lives in the Cua Dat Hydropower Plant Basin in Thanh Hoa province, period from 2012-2016 - 13

Evaluation of the effectiveness of the Forest Environmental Services Payment Policy on forest management and protection, improving people's lives in the Cua Dat Hydropower Plant Basin in Thanh Hoa province, period from 2012-2016 - 13

When considering the ratio of income from lending to SMEs to total income from lending activities and to the total income of the Bank, it can be seen that: the ratio of income from lending to SMEs is quite good. Currently, Maritimebank Bac Ninh is gradually shifting its structure to lending to SMEs, short-term is completely reasonable. However, the level of income increase is not good compared to the growth of loan turnover and outstanding loans. Therefore, the branch needs to find solutions to further improve lending efficiency, especially lending to SMEs.

2.3. Evaluation of the effectiveness of lending to small and medium enterprises of Maritimebank - Bac Ninh Branch

2.3.1. Results achieved

In the past 3 years, Maritimebank Bac Ninh's lending activities to SMEs have achieved quite impressive results, showing the efforts and great successes in applying the bank's investment strategy in which SME customers are the important target that the bank targets. From the above figures and analysis, we can see some of the main successes of Maritimebank Bac Ninh in lending to SMEs as follows:

Income from lending to SME customers has increased gradually over the years: In 2017, income from lending to SME reached 38,190 million VND, and by 2018 it had increased to

48,266 million VND (up 26.39% compared to 2017, equivalent to a value of 10,076

million VND). By 2019, it had increased to VND 53,759 million (an increase of 11.38%, equivalent to VND 5,493 million), accounting for a relatively high proportion in the structure of loans to corporate customers of Maritimebank Bac Ninh, respectively 45%; 44.58%; 45.03% in the past 3 years, and accounting for an important part of the Bank's total income. This shows the orientation and strategy of focusing and effectively exploiting lending activities to SME customers.

The loan turnover and outstanding loans for SMEs over the total outstanding loans have increased continuously over the years, significantly increasing the income of Maritimebank Bac Ninh, stimulating the business capacity and the agility and flexibility of credit officers in the current competitive market mechanism. The reasonable shift in loan structure between short-term and medium- and long-term, between the state-owned economy and the non-state-owned economy. In particular, Maritimebank Bac Ninh has implemented many modernization programs (SIBS, BDS, Golive, R17...) as a premise for the bank to develop more sustainably.

The credit quality of all outstanding debts has been controlled at an acceptable level, reviewed and analyzed for difficulties and advantages to find the most suitable solution.

Credit activities towards SMEs help Maritimebank Bac Ninh expand its market share, develop modern banking services and enhance the reputation and competitiveness of Maritimebank Bac Ninh in the area of operation. At the same time, it disperses risks in the bank's credit activities. Ensures the highest efficiency.

2.3.2. Some limitations and causes

2.3.2.1. Some limitations

Besides the achieved results, SME lending activities still have some limitations as follows.

Income from lending to SMEs at Maritimebank Bac Ninh branch has increased over the years, but the growth rate has decreased. Because the increase in income compared to the increase in outstanding loans and SME lending turnover is on a downward trend, this proves that outstanding loans and arising lending turnover have not brought about efficiency, the more

The expected return on loan has not increased proportionally, and the efficiency of SME lending is not high.

Income from lending to SMEs compared to income from lending to corporate customers or compared to total lending income is on a downward trend. This is a warning sign that lending is having problems, lending efficiency is not optimized to bring the highest efficiency in lending to SMEs.

Maritimebank Bac Ninh's lending activities are mainly short-term loans, medium and long-term loans are still very modest. The characteristic of short-term funding sources is that the maturity date is very short, usually less than a year, many payments must be made within a short period of time. If businesses abuse and Maritimebank Bac Ninh does not manage this capital source well, it will lead to insolvency, especially in the case of using short-term capital for long-term investment. Thus, not being able to access medium and long-term capital will be a significant difficulty for SMEs in forming fixed assets and expanding production and business.

Many SMEs have not been able to access loans at Maritimebank Bac Ninh. As we know, SMEs have low capital and financial capacity, so the requirement for customers to meet the ratio of collateral and high equity requirements makes many SMEs with good business plans unable to borrow capital from the Bank because they do not meet the regulations on collateral and equity, or when they have finished arranging the collateral, they have lost the business opportunity.

Transaction processing time is still long compared to other commercial banks in the same area, making customers dissatisfied with the waiting time: In general, transaction processing time is still long, affecting the opportunity cost of Maritimebank Bac Ninh itself and of customers, reducing lending efficiency.

2.3.2.2. Causes of limitations

Subjective causes

On the bank side

Maritimebank Bac Ninh's orientation to expand lending to SME customers is completely appropriate based on the branch location and business activities of the banks.

SME customers in the area. In each period, Maritimebank in general and Maritimebank Bac Ninh in particular always come up with new strategies to attract more and more SME customers to transact. Specifically in increasing sales and outstanding loans every year. However, the efficiency from SME customers is not high because: The bank always offers loans with minimum interest rates, has not diversified services to customers, leading to low lending efficiency and partly to attract customers, Maritimebank Bac Ninh also faces many other banks offering at the same time. Attracting customers is important, but improving efficiency is even more important, only then will the income from SME customers be increased.

Maritimebank Bac Ninh's lending activities are mainly short-term loans. The advantage of short-term lending is that the capital turnover is very fast, the bank will collect the principal and interest soon. However, the disadvantage is that if the capital source is not well managed, the turnover according to each industry will lead to the inability to pay. In addition, with each short-term funding source, the bank will not earn high profits. Currently, Maritimebank Bac Ninh does not have a specific direction in lending to businesses borrowing medium and long-term capital to form fixed assets for production and business. In the coming time, Maritimebank Bac Ninh will have an implementation plan, aiming to bring higher income when using medium and long-term capital to lend to SME customers.

The Bank's loan procedures and processes are currently applied to all corporate customers, so there are some points that are not suitable for the specific operations of the SME sector. The Bank needs to offer products and services that are suitable for the characteristics and features of each SME. The Bank needs to divide each industry and SME customer into priority groups to focus on marketing and care. The branch still does not have specialized staff in charge of this general area. The time to review and approve SME loan decisions at the branch is also relatively long, averaging more than a week, so it often misses business opportunities for customers, while customers can now have many banks offering offers.

The ability to manage, collect, process and classify information about SME customers is still limited. The Bank's information technology system is not yet able to meet customer management requirements. With existing customers, the Bank needs to assess the business performance, financial situation, profitability and debt repayment ability of the enterprise, thereby proposing solutions to increase income for each SME customer (specifically: increase interest rates, apply interest rate frameworks with the condition that the enterprise meets the average outstanding balance, uses a certain number of banking services, etc.).

The branch management has not focused on marketing, and has no specific policies or measures to find new customers and take good care of potential customers to increase outstanding loans and increase lending market share in the area of operation.

For SMEs

The first reason comes from the small and medium scale of the enterprise. Due to the potential risks due to the characteristics of the SME sector, banks often require enterprises to have collateral. However, due to low equity, low financial capacity... SMEs often fall into a state of lacking collateral, or collateral is much lower than the loan demand or collateral documents lack legality... Therefore, these enterprises face many difficulties in accessing bank loans.

The feasibility and profitability of projects and business plans are considered a key factor in making decisions related to loan applications of enterprises. However, because SMEs are often weak in management and financial skills, and have limited professional qualifications, the construction of projects and business plans is difficult. This is especially true for enterprises in the agricultural, forestry and fishery sector.

Objective reasons:

Firstly: The branch's lending interest rates in recent times, especially in the period 2017-2019, have increased at times due to strong demand from SMEs and fluctuations in the market.

Due to the fluctuations of the gold and real estate markets, many businesses cannot or do not dare to borrow capital from banks even though their business plans are very effective. This situation causes small businesses with limited capital to reduce the scale of production and business activities or have to stop production, while businesses with favorable conditions in terms of capital and revenue limit borrowing from banks to minimize financial costs.

Second: Some SMEs lack an honest and transparent financial information system, so they have not yet created trust with banks. In addition to the reason that enterprises are weak in corporate governance, it is also because the State has not yet had specific regulations on financial accounting and auditing of financial statements for SMEs, and there are no specific guidelines on forms and types of annual financial statements of enterprises. This makes it difficult for banks to collect accurate information on the financial situation of enterprises.

In addition, the lack of uniformity in the legal framework of the state is also one of the reasons causing difficulties for bank lending activities to SMEs. Specifically, these are:

In lending regulations, documents proving property ownership must be notarized, but the notarization procedure is still cumbersome and time-consuming, causing difficulties for both customers and banks. Sometimes, there are cases of state officials causing procedural harassment.

Regarding the handling of secured assets: according to regulations, when the borrower cannot repay the debt, the bank has the right to foreclose or auction the assets. However, in the event of a lawsuit, the trial procedure is very cumbersome, causing difficulties for the bank in terms of time and costs. If the bank wins the lawsuit, the enforcement of the judgment will encounter many difficulties, sometimes lasting several years, causing many losses for the bank.

Regulations on the establishment, merger, dissolution and bankruptcy of enterprises are not clear. Many times, loss-making enterprises merge with other enterprises, making it very difficult for banks to collect debts. In case of bankruptcy, the bank's debt is very difficult to collect because there are no specific regulations.

CHAPTER 3. SOLUTIONS TO IMPROVE THE EFFICIENCY OF LENDING TO SMALL AND MEDIUM ENTERPRISES AT VIETNAM MARITIME COMMERCIAL JOINT STOCK BANK - BAC NINH BRANCH

3.1. Orientation to improve the efficiency of lending to small and medium enterprises of Maritimebank - Bac Ninh Branch

3.1.1. General orientation of Maritimebank

- Building a strong banking model with many resources and potentials, operating internationally, leading in the country, commensurate with the region.

- Create and demonstrate the brand, position, image, and cultural identity of the business according to the modern banking model.

- Be proactive in creating, promoting internal strength, closely following the domestic and international economic and political situation to promptly respond to unexpected events that may occur.

- Reasonable credit enhancement coupled with equity growth.

- Develop customers in both scale and quality.

- Focus on improving credit quality, ensuring compliance with the State Bank's credit regulations, reducing overdue debt, and not generating new bad debts.

- Diversify banking products, improve technology.

- Human resources are the key to success, creating human resources with qualifications, knowledge, skills, experience and encouraged by a system of material and spiritual motivation and suitable working conditions.

About capital

- Ensure adequate capital for credit and investment needs, while contributing to capital balance for the entire system;

- Diversify mobilized capital sources, expand the capital mobilization network associated with stable outstanding loan growth, focus on attracting deposits from residents, businesses and other economic sectors to maximize the exploitation of idle money in the market, avoiding dependence on a few economic organizations. Focus on the distribution of

Analyze and classify customers who have credit relationships with the bank to have a reasonable and effective credit investment orientation;

- Promote profitable capital business, focus on growing low-cost capital sources.

- Ensure capital safety.

About credit activities

- Continue to prioritize targeting new markets such as individual customers, SMEs, developing consumer credit, and building a solid customer base;

- Prioritize the development of customers using full banking product packages;

- Diversify and improve the quality of credit services;

- Consider the quality and safety of credit activities as the top goal, link credit growth with strict control of credit growth quality and efficiency, and limit the increase of new bad debts;

- Be determined in directing and promoting debt collection, handling off-balance sheet debt, and overdue interest based on applying appropriate measures for each debt such as debt collection, lawsuits, debt sales, etc.

- Continue to innovate credit granting procedures towards simplicity and convenience.

About investment activities

- Continue to research joint stock enterprises, develop and implement plans to restructure investment portfolios reasonably, effectively and profitably;

- Diversify investment portfolio to minimize investment risks.

About service activities

- Strongly develop payment services via banks and non-cash payments based on a modern, safe, reliable and efficient technology system and banking payment system in accordance with international practices and standards;

- Improve banking payment utilities to encourage economic sectors, especially individuals, to use banking payment services;