The theory of securities and the securities market in Vietnam has not really met the requirements of practice, has not really created conditions and premises for the formation and development of the derivative securities market in Vietnam, including the application of securities options - the research object of this topic.

Before the Securities Law 2006 was enacted

The Vietnamese stock market is one of the youngest and smallest stock markets in the world. It has been just over 10 years since the Vietnam Securities Commission was established under Decree 75/CP on January 1, 1996. If we count from the date of Decision 127/1998/QD-TTg on July 11, 1998 on the establishment of two stock exchanges in Ho Chi Minh City and Hanoi, the age of the Vietnamese stock market is only 9 years. In fact, the Ho Chi Minh City Stock Exchange only started operating on July 20, 2000 and the first trading session took place on June 28, 2000; while the Hanoi Stock Exchange did not officially start operating until March 2005. Up to now, the Government and relevant agencies have had less than 10 years to promulgate, amend and perfect legal regulations on the stock market, so limitations and shortcomings are inevitable.

Maybe you are interested!

-

Using Cross Currency Contracts to Speculate on the Foreign Exchange Market:

Using Cross Currency Contracts to Speculate on the Foreign Exchange Market: -

Strengthening Control, Restriction and Gradually Eliminating Activities of the Unofficial Foreign Exchange Market

Strengthening Control, Restriction and Gradually Eliminating Activities of the Unofficial Foreign Exchange Market -

Balancing Supply and Demand of a Country's Currency in the Foreign Exchange Market

Balancing Supply and Demand of a Country's Currency in the Foreign Exchange Market -

Foreign Currency Demand in the Informal Foreign Exchange Market

Foreign Currency Demand in the Informal Foreign Exchange Market -

Deploying derivatives in the foreign exchange market - experience from China and development solutions for Vietnam - 13

Deploying derivatives in the foreign exchange market - experience from China and development solutions for Vietnam - 13

The first document to regulate can be said to be Decree 48/1998/ND-CP dated July 11, 1998 on securities and the securities market regulating the issuance of securities to the public, securities transactions and related services. This is the first time the concept of securities and securities transactions has been legalized in Vietnam. As the first document, what the above decree mentioned is only at a basic level, providing the recipients with very limited knowledge about securities. The decree also has guidelines for the issuance and trading of securities, however at the time

At the time of the decree's issuance, the two stock exchange centers had to operate for another two years to verify whether the provisions in the above document were consistent with reality or not. The provisions of the Decree, which are principles for market operations, were built mainly on theory, based on the Vietnamese legal framework in 1998 and referring to the laws on stock markets of countries around the world, with no basis in practice. Regarding stock options, the above decree did not mention them at all. Securities as defined by the decree only include stocks, bonds, fund certificates and other types of securities. Thus, at this time, the concept of derivative securities was unknown in Vietnam.

The above regulations were gradually improved, leading to the promulgation of Decree 144/2003/ND-CP dated November 28, 2003 on securities and the securities market, containing quite important amendments and supplements, especially the loosening of the participation rate of foreign parties in the Vietnamese securities market, and the beginning of specific regulations on the information disclosure regime of market entities.

However, Decree 144 only regulates the issuance of securities to the public by joint stock companies, not the issuance of shares by equitized state-owned enterprises, the issuance of securities by credit institutions, and foreign-invested enterprises converted into joint stock companies. This limits the development of the primary market and creates inequality among types of enterprises in issuing securities to the public.

Decree 144 only regulates the activities of the centralized securities trading market (the stock exchange), not the decentralized securities trading activities. This limits the development of the secondary market.

On the other hand, stock trading activities are taking place quite actively in the free market without State management.

Furthermore, this decree still retains the weakness of Decree 48, which is that it does not recognize derivative instruments as commodities that can be traded on the market; securities are still only stocks, bonds and fund certificates.

The above decrees have been issued to create the initial legal framework for securities trading. However, there is no specific circular guiding how to implement them (except for the circular guiding the bidding of government bonds on the stock market). This makes it difficult for entities to understand and conduct securities transactions in general, let alone securities options transactions.

In addition to the two important documents above, a number of related documents were also issued to regulate the market such as the decree on administrative sanctions in the field of securities and the stock market, the decree on the organization and operation of securities inspection ...

At this time, regulations on the stock market and implementation guidelines are still lacking, requiring the issuance of a document with higher legal value and market regulation, the Securities Law replacing Decree 144 to complete the legal environment according to market requirements as well as integration requirements of the financial sector. To develop operations related to stock options, the new law needs to recognize derivative financial instruments as commodities on the stock market.

After the Securities Law 2006 was enacted:

The Securities Law 2006 - Law No. 70/2006/QH11 was passed by the 11th National Assembly on June 29, 2006, effective from January 1, 2007 after 3 years of development, with 10 drafts with many steps of addition, amendment, soliciting comments from all participants and interested in the securities market as well as submitting for comments from competent authorities. The birth of the law is considered a breakthrough in creating a complete legal framework to promote the development of the Vietnamese securities market. The Securities Law will create a basis for the securities market to develop rapidly and stably, creating peace of mind for organizations and individuals when participating in business and investment, while helping the public easily understand securities, the securities market and creating a legal basis for the public to participate in the market when conditions permit. Accordingly, the State encourages and creates favorable conditions for organizations and individuals of all economic sectors and all classes of people to participate in investment and activities in the stock market in order to mobilize medium-term and long-term capital sources for development investment. The promulgation of the Securities Law helps to clearly define the role of each long-term and short-term capital market in the structure of the stock market in general, as well as promote the autonomy of enterprises when mobilizing capital in the stock market. In addition, it will reduce the burden of using short-term capital for long-term loans of the current banking system. At the same time, the State has a management and supervision policy to ensure that the stock market operates fairly, publicly, transparently, safely and effectively.

The Securities Law was issued in the context of a centralized securities market that had been in existence for more than 5 years, so the provisions in the law were built on the basis of market research, with high practicality; at the same time, at the end of 2006, the securities market was extremely vibrant, it could be called hot, the VnIndex increased rapidly and continuously, investors made demands on market transparency, safety and efficiency for their investments. Therefore, the issuance of the Securities Law met their expectations.

Research on the 2006 Securities Law shows that the State has made a fairly clear statement on securities development policy, emphasizing issues of information disclosure and transparency, procedures and processes that market entities must follow, focusing on market inspection and supervision; handling and resolving disputes in the securities sector.

The breakthrough point in this law is the mention of derivative financial instruments such as stock purchase rights, warrants, call options, put options, futures contracts, securities groups or securities indices. This shows the recognition of the above types of securities, creating the initial basis for forming the market and conducting transactions.

Following the 2006 Securities Law, Decree 14/2007/ND-CP was also issued detailing the implementation of a number of articles of the Securities Law. Along with that, the Ministry of Finance has a number of circulars providing specific guidance on activities on the stock market such as circulars guiding information disclosure on the stock market, circulars guiding documents for registration of public offering of securities ... This demonstrates the government's efforts in synchronizing and perfecting its legal system.

2. Developments in the foreign exchange market and the stock market in recent times 2.1. Foreign exchange market

Over the years, the State Bank of Vietnam (SBV) has been very successful in managing the exchange rate policy. While the value of currencies against the US Dollar fluctuates erratically, the USD/VND exchange rate has always been stable. This not only contributes to the stability of the domestic financial system but also creates a stable economic environment, especially for exports.

The SBV is applying a floating exchange rate policy but with State regulation. Since 1999, the SBV has maintained a daily fluctuation band of +/-0.25% against the USD. The SBV intervenes in the market mainly through open market operations.

In 2000 and 2001, with the export promotion policy, the Dong (VND) was devalued quite strongly against the dollar, by 3.46% and 3.9% respectively. However, since then, the annual depreciation rate has gradually decreased.

As of September 30, 2006, one dollar was worth

16,051 VND, up 137 points, equivalent to 0.86% compared to the beginning of the year (15,914). In previous years, the depreciation rate of VND against USD was as follows: 2005, 0.86%; 2004, 0.84%; 2003, 1.56%; 2002, 1.98%.

From the beginning of 2006 to October 12, 2006, the lowest level reached was 15,901 on March 14, the highest level reached was 16,056 on September 29. The level of 16,056 reached was also 60 points higher than the day when the exchange rate on the free market reached the exchange level of 17,200 (May 9, 2006).

In 2007, on February 9, the USD price fell below 16,000 VND after many days of decline, and remained so until the end of the month, due to the sudden increase in foreign currency supply while the amount of VND from the banking system was not enough to meet the demand. However, since March 2, the USD/VND exchange rate of banks reached 16,001 and has been increasing continuously since then.

However, in the last few months of the year, there was a surplus of foreign currency at commercial banks. The exchange rates of commercial banks were continuously set at the floor price, the lowest level within the allowed range (+/- 0.5% compared to the average interbank exchange rate), which was explained by the surplus of foreign currency.

A large amount of foreign currency flows into our country through many channels such as: stock market, FDI capital, remittances and is converted into VND at commercial banks. Currently, the foreign currency trading turnover of banks is about 100 million USD/day, in which the main selling customers are export enterprises and foreign investment funds, the buying customers are import enterprises and domestic banks. The amount of foreign currency bought is larger than the amount of foreign currency sold by several million USD/day. This has caused banks to have a surplus of foreign currency in the market. Besides, people's psychology of preferring to keep USD has decreased when they realize that long-term savings deposits in USD are not as profitable as in VND.

The attractiveness of USD is getting weaker, while enterprises still prefer to borrow foreign currency. Even though the foreign currency lending interest rate is at 6-7%/year, enterprises borrowing foreign currency still benefit 1-2% compared to borrowing VND. These two opposite trends show that banks are in a situation of excess foreign currency in the buying and selling channels but lacking foreign currency in the mobilization and lending channels. This explains why in the current context, many banks complain about excess foreign currency but some banks still announce an increase in foreign currency mobilization interest rates.

To balance these two markets, some banks take foreign currency in the buying and selling market to solve the foreign currency demand in the lending market. However, the solution of using VND to buy USD and then lending poses a potential risk for banks when the USD/VND exchange rate fluctuates. For example, when buying USD to lend, the USD price is at 16,078 VND/USD, but after 3 months of selling USD for VND, the USD price drops to 15,900-16,000 VND/USD, at which time the bank will incur a loss. In fact, when implementing this solution, if the bank is not exposed to the risk of exchange rate fluctuations, the profit earned is not high. Therefore, although the foreign currency status is regulated at 30%, in reality, no bank dares to keep an amount of foreign currency accounting for 30% of its capital.

In the past two weeks from October 7 to October 21, the VND/USD exchange rate began to fall sharply, holding a large amount of foreign currency means losses. Therefore, most banks currently do not use VND to buy foreign currency and lend it out, but mainly choose to increase USD mobilization interest rates. The solution of using VND to buy foreign currency and then lend it out is only implemented when having to meet urgent foreign currency needs of customers. Thus, solving the problem of excess and shortage of foreign currency is still a difficult problem for banks.

Because Vietnamese businesses mainly use USD in payments, any exchange rate fluctuations will affect production and business activities. Therefore, having financial tools to help businesses hedge against exchange rate risks is essential.

2.2.Stock market

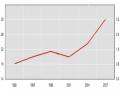

Planners, economic experts, amateur stock market players, or simply ordinary people all see that "The Vietnamese stock market in recent times (late 2006 and early 2007) has developed too quickly and with great volatility, marking an important year in the volatile turnaround of the country's economy.

Since its launch and operation in the Vietnamese market, the stock market has been operating for 7 years, but it has only been really bustling and significant, the most exciting was last year, especially the last months of 2006. The index of the Vietnamese stock market increased by 85% in 2004-2005 and skyrocketed by 145% in 2006. But in the first 6 months of 2007, this index only increased by 35%. A closer analysis shows that in late January and early February 2007, the index of the Vietnamese stock market increased by nearly 100 points in one week from 974.76 on January 26, 2007 to 1,074.55 on February 2, 2007. In 2