44

Payment and account services to support capital mobilization. Payment services include: money transfer, salary payment, import/export payment, payment of electricity and water bills, telephone bills, purchase of train and air tickets. Account services include: automatic investment services, account overdraft, etc. In addition, customers can easily access modern banking services through electronic banking channels based on advanced technology platforms, with high safety and security.

Table 2.2: Deposit mobilization products and services of Vietinbank Phu Yen, BIDV Phu Yen, Agribank Phu Yen and Vietcombank Phu Yen as of December 31, 2017

STT

Product Name | Vietinbank Phu Yen | BIDV Phu Yen | Agribank Phu Yen | Vietcombank Phu Yen | |

1 | Payment deposit | X | X | X | X |

2 | Savings deposit unlimited | X | X | X | X |

3 | Savings deposit Term | X | X | X | X |

4 | Accumulated savings | X | X | X | |

5 | Savings deposit multi-term | X | |||

6 | Margin deposit | X | X | ||

7 | Overdraft deposit | X | |||

8 | Term investment deposit automatic limit | X | X | ||

9 | Multi-investment deposits power | X | |||

10 | Flexible investment deposits active / Deposit as desired | X | X | X | |

11 | Save on study | X | X | X |

Maybe you are interested!

-

Solutions to enhance capital mobilization at Lien Viet Post Joint Stock Commercial Bank - Hai Phong Branch - 9

Solutions to enhance capital mobilization at Lien Viet Post Joint Stock Commercial Bank - Hai Phong Branch - 9 -

Solutions to enhance capital mobilization at Lien Viet Post Joint Stock Commercial Bank - Hai Phong Branch - 8

Solutions to enhance capital mobilization at Lien Viet Post Joint Stock Commercial Bank - Hai Phong Branch - 8 -

Evaluation of Capital Mobilization Activities of Lien Viet Post Joint Stock Commercial Bank - Hai Phong Branch

Evaluation of Capital Mobilization Activities of Lien Viet Post Joint Stock Commercial Bank - Hai Phong Branch -

Capital Mobilization Situation At Mb Viet Tri Branch

Capital Mobilization Situation At Mb Viet Tri Branch -

Solutions for tourism development in Tien Lang - 10

zt2i3t4l5ee

zt2a3gstourism, tourism development

zt2a3ge

zc2o3n4t5e6n7ts

- District People's Committees and authorities of communes with tourist attractions should support, promote, and provide necessary information to people, helping them improve their knowledge about tourism. Raise tourism awareness for local people.

*

* *

Due to limited knowledge and research time, the thesis inevitably has shortcomings. Therefore, I look forward to receiving guidance from teachers, experts as well as your comments to make the thesis more complete.

Chapter III Conclusion

Through the issues presented in Chapter II, we can come to some conclusions:

Based on the strengths of available tourism resources, the types of tourism in Tien Lang that need to be promoted in the coming time are sightseeing and resort tourism, discovery tourism, weekend tourism. To improve the quality and diversify tourism products, Tien Lang district needs to combine with local cultural tourism resources, at the same time combine with surrounding areas, build rich tourism products. The strengths of Tien Lang tourism are eco-tourism and cultural tourism, so developing Tien Lang tourism must always go hand in hand with restoring and preserving types of cultural tourism resources. Some necessary measures to support and improve the efficiency of exploiting tourism resources in Tien Lang are: strengthening the construction of technical facilities and labor force serving tourism, actively promoting and advertising tourism, and expanding forms of capital mobilization for tourism development.

CONCLUDE

I Conclusion

1. Based on the results achieved within the framework of the thesis's needs, some basic conclusions can be drawn as follows:

Tien Lang is a locality with great potential for tourism development. The relatively abundant cultural tourism resources and ecological tourism resources have great appeal to tourists. Based on this potential, Tien Lang can build a unique tourism industry that is competitive enough with other localities within Hai Phong city and neighboring areas.

In recent years, the exploitation of the advantages of resources to develop tourism and build tourist routes in Tien Lang has not been commensurate with the available potential. In terms of quantity, many resource objects have not been brought into the purpose of tourism development. In terms of time, the regular service time has not been extended to attract more visitors. Infrastructure and technical facilities are still weak. The labor force is still thin and weak in terms of expertise. Tourism programs and routes have not been organized properly, the exploitation content is still monotonous, so it has not attracted many visitors. Although resources have not been mobilized much for tourism development, they are facing the risk of destruction and degradation.

2. Based on the results of investigation, analysis, synthesis, evaluation and selective absorption of research results of related topics, the thesis has proposed a number of necessary solutions to improve the efficiency of exploiting tourism resources in Tien Lang such as: promoting the restoration and conservation of tourism resources, focusing on investment and key exploitation of ecotourism resources, strengthening the construction of infrastructure and tourism workforce. Expanding forms of capital mobilization. In addition, the thesis has built a number of tourist routes of Hai Phong in which Tien Lang tourism resources play an important role.

Exploiting Tien Lang tourism resources for tourism development is currently facing many difficulties. The above measures, if applied synchronously, will likely bring new prospects for the local tourism industry, contributing to making Tien Lang tourism an important economic sector in the district's economic structure.

REFERENCES

1. Nhuan Ha, Trinh Minh Hien, Tran Phuong, Hai Phong - Historical and cultural relics, Hai Phong Publishing House, 1993

2. Hai Phong City History Council, Hai Phong Gazetteer, Hai Phong Publishing House, 1990.

3. Hai Phong City History Council, History of Tien Lang District Party Committee, Hai Phong Publishing House, 1990.

4. Hai Phong City History Council, University of Social Sciences and Humanities, VNU, Hai Phong Place Names Encyclopedia, Hai Phong Publishing House. 2001.

5. Law on Cultural Heritage and documents guiding its implementation, National Political Publishing House, Hanoi, 2003.

6. Tran Duc Thanh, Lecture on Tourism Geography, Faculty of Tourism, University of Social Sciences and Humanities, VNU, 2006

7. Hai Phong Center for Social Sciences and Humanities, Some typical cultural heritages of Hai Phong, Hai Phong Publishing House, 2001

8. Nguyen Ngoc Thao (editor-in-chief, Tourism Geography, Hai Phong Publishing House, two volumes (2001-2002)

9. Nguyen Minh Tue and group of authors, Hai Phong Tourism Geography, Ho Chi Minh City Publishing House, 1997.

10. Nguyen Thanh Son, Hai Phong Tourism Territory Organization, Associate Doctoral Thesis in Geological Geography, Hanoi, 1996.

11. Decision No. 2033/QD – UB on detailed planning of Tien Lang town, Hai Phong city until 2020.

12. Department of Culture, Information, Hai Phong Museum, Hai Phong relics

- National ranked scenic spot, Hai Phong Publishing House, 2005. 13. Tien Lang District People's Committee, Economic Development Planning -

Culture - Society of Tien Lang district to 2010.

14.Website www.HaiPhong.gov.vn

APPENDIX 1

List of national ranked monuments

STT

Name of the monument

Number, year of decisiondetermine

Location

1

Gam Temple

938 VH/QĐ04/08/1992

Cam Khe Village- Toan Thang commune

2

Doc Hau Temple

9381 VH/QĐ04/08/1992

Doc Hau Village –Toan Thang commune

3

Cuu Doi Communal House

3207 VH/QĐDecember 30, 1991

Zone II of townTien Lang

4

Ha Dai Temple

938 VH/QĐ04/08/1992

Ha Dai Village –Tien Thanh commune

APPENDIX II

STT

Name of the monument

Number, year of decision

Location

1

Phu Ke Pagoda Temple

178/QD-UBJanuary 28, 2005

Zone 1 - townTien Lang

2

Trung Lang Temple

178/QD-UBJanuary 28, 2005

Zone 4 – townTien Lang

3

Bao Khanh Pagoda

1900/QD-UBAugust 24, 2006

Nam Tu Village -Kien Thiet commune

4

Bach Da Pagoda

1792/QD-UB11/11/2002

Hung Thang Commune

5

Ngoc Dong Temple

177/QD-UBNovember 27, 2005

Tien Thanh Commune

6

Tomb of Minister TSNhu Van Lan

2848/QD-UBSeptember 19, 2003

Nam Tu Village -Kien Thiet commune

7

Canh Son Stone Temple

2160/QD-UBSeptember 19, 2003

Van Doi Commune –Doan Lap

8

Meiji Temple

2259/QD-UBSeptember 19, 2002

Toan Thang Commune

9

Tien Doi Noi Temple

477/QD-UBSeptember 19, 2005

Doan Lap Commune

10

Tu Doi Temple

177/QD-UBJanuary 28, 2005

Doan Lap Commune

11

Duyen Lao Temple

177/QD-UBJanuary 28, 2005

Tien Minh Commune

12

Dinh Xuan Uc Pagoda

177/QD-UBJanuary 28, 2005

Bac Hung Commune

13

Chu Khe Pagoda

177/QD-UBJanuary 28, 2005

Hung Thang Commune

14

Dong Dinh

2848/QD-UBNovember 21, 2002

Vinh Quang Commune

15

President's Memorial HouseTon Duc Thang

177/QD-UBJanuary 28, 2005

NT Quy Cao

Ha Dai Temple

Ben Vua Temple

Tien Lang hot spring

div.maincontent .p { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; } div.maincontent p { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; } div.maincontent .s1 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; font-size: 16pt; } div.maincontent .s2 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s3 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s4 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; font-size: 14pt; } div.maincontent .s5 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; font-size: 14pt; } div.maincontent .s6 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s7 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s8 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; vertical-align: 6pt; } div.maincontent .s9 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 12pt; } div.maincontent .s11 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; tex

Solutions for tourism development in Tien Lang - 10

zt2i3t4l5ee

zt2a3gstourism, tourism development

zt2a3ge

zc2o3n4t5e6n7ts

- District People's Committees and authorities of communes with tourist attractions should support, promote, and provide necessary information to people, helping them improve their knowledge about tourism. Raise tourism awareness for local people.

*

* *

Due to limited knowledge and research time, the thesis inevitably has shortcomings. Therefore, I look forward to receiving guidance from teachers, experts as well as your comments to make the thesis more complete.

Chapter III Conclusion

Through the issues presented in Chapter II, we can come to some conclusions:

Based on the strengths of available tourism resources, the types of tourism in Tien Lang that need to be promoted in the coming time are sightseeing and resort tourism, discovery tourism, weekend tourism. To improve the quality and diversify tourism products, Tien Lang district needs to combine with local cultural tourism resources, at the same time combine with surrounding areas, build rich tourism products. The strengths of Tien Lang tourism are eco-tourism and cultural tourism, so developing Tien Lang tourism must always go hand in hand with restoring and preserving types of cultural tourism resources. Some necessary measures to support and improve the efficiency of exploiting tourism resources in Tien Lang are: strengthening the construction of technical facilities and labor force serving tourism, actively promoting and advertising tourism, and expanding forms of capital mobilization for tourism development.

CONCLUDE

I Conclusion

1. Based on the results achieved within the framework of the thesis's needs, some basic conclusions can be drawn as follows:

Tien Lang is a locality with great potential for tourism development. The relatively abundant cultural tourism resources and ecological tourism resources have great appeal to tourists. Based on this potential, Tien Lang can build a unique tourism industry that is competitive enough with other localities within Hai Phong city and neighboring areas.

In recent years, the exploitation of the advantages of resources to develop tourism and build tourist routes in Tien Lang has not been commensurate with the available potential. In terms of quantity, many resource objects have not been brought into the purpose of tourism development. In terms of time, the regular service time has not been extended to attract more visitors. Infrastructure and technical facilities are still weak. The labor force is still thin and weak in terms of expertise. Tourism programs and routes have not been organized properly, the exploitation content is still monotonous, so it has not attracted many visitors. Although resources have not been mobilized much for tourism development, they are facing the risk of destruction and degradation.

2. Based on the results of investigation, analysis, synthesis, evaluation and selective absorption of research results of related topics, the thesis has proposed a number of necessary solutions to improve the efficiency of exploiting tourism resources in Tien Lang such as: promoting the restoration and conservation of tourism resources, focusing on investment and key exploitation of ecotourism resources, strengthening the construction of infrastructure and tourism workforce. Expanding forms of capital mobilization. In addition, the thesis has built a number of tourist routes of Hai Phong in which Tien Lang tourism resources play an important role.

Exploiting Tien Lang tourism resources for tourism development is currently facing many difficulties. The above measures, if applied synchronously, will likely bring new prospects for the local tourism industry, contributing to making Tien Lang tourism an important economic sector in the district's economic structure.

REFERENCES

1. Nhuan Ha, Trinh Minh Hien, Tran Phuong, Hai Phong - Historical and cultural relics, Hai Phong Publishing House, 1993

2. Hai Phong City History Council, Hai Phong Gazetteer, Hai Phong Publishing House, 1990.

3. Hai Phong City History Council, History of Tien Lang District Party Committee, Hai Phong Publishing House, 1990.

4. Hai Phong City History Council, University of Social Sciences and Humanities, VNU, Hai Phong Place Names Encyclopedia, Hai Phong Publishing House. 2001.

5. Law on Cultural Heritage and documents guiding its implementation, National Political Publishing House, Hanoi, 2003.

6. Tran Duc Thanh, Lecture on Tourism Geography, Faculty of Tourism, University of Social Sciences and Humanities, VNU, 2006

7. Hai Phong Center for Social Sciences and Humanities, Some typical cultural heritages of Hai Phong, Hai Phong Publishing House, 2001

8. Nguyen Ngoc Thao (editor-in-chief, Tourism Geography, Hai Phong Publishing House, two volumes (2001-2002)

9. Nguyen Minh Tue and group of authors, Hai Phong Tourism Geography, Ho Chi Minh City Publishing House, 1997.

10. Nguyen Thanh Son, Hai Phong Tourism Territory Organization, Associate Doctoral Thesis in Geological Geography, Hanoi, 1996.

11. Decision No. 2033/QD – UB on detailed planning of Tien Lang town, Hai Phong city until 2020.

12. Department of Culture, Information, Hai Phong Museum, Hai Phong relics

- National ranked scenic spot, Hai Phong Publishing House, 2005. 13. Tien Lang District People's Committee, Economic Development Planning -

Culture - Society of Tien Lang district to 2010.

14.Website www.HaiPhong.gov.vn

APPENDIX 1

List of national ranked monuments

STT

Name of the monument

Number, year of decisiondetermine

Location

1

Gam Temple

938 VH/QĐ04/08/1992

Cam Khe Village- Toan Thang commune

2

Doc Hau Temple

9381 VH/QĐ04/08/1992

Doc Hau Village –Toan Thang commune

3

Cuu Doi Communal House

3207 VH/QĐDecember 30, 1991

Zone II of townTien Lang

4

Ha Dai Temple

938 VH/QĐ04/08/1992

Ha Dai Village –Tien Thanh commune

APPENDIX II

STT

Name of the monument

Number, year of decision

Location

1

Phu Ke Pagoda Temple

178/QD-UBJanuary 28, 2005

Zone 1 - townTien Lang

2

Trung Lang Temple

178/QD-UBJanuary 28, 2005

Zone 4 – townTien Lang

3

Bao Khanh Pagoda

1900/QD-UBAugust 24, 2006

Nam Tu Village -Kien Thiet commune

4

Bach Da Pagoda

1792/QD-UB11/11/2002

Hung Thang Commune

5

Ngoc Dong Temple

177/QD-UBNovember 27, 2005

Tien Thanh Commune

6

Tomb of Minister TSNhu Van Lan

2848/QD-UBSeptember 19, 2003

Nam Tu Village -Kien Thiet commune

7

Canh Son Stone Temple

2160/QD-UBSeptember 19, 2003

Van Doi Commune –Doan Lap

8

Meiji Temple

2259/QD-UBSeptember 19, 2002

Toan Thang Commune

9

Tien Doi Noi Temple

477/QD-UBSeptember 19, 2005

Doan Lap Commune

10

Tu Doi Temple

177/QD-UBJanuary 28, 2005

Doan Lap Commune

11

Duyen Lao Temple

177/QD-UBJanuary 28, 2005

Tien Minh Commune

12

Dinh Xuan Uc Pagoda

177/QD-UBJanuary 28, 2005

Bac Hung Commune

13

Chu Khe Pagoda

177/QD-UBJanuary 28, 2005

Hung Thang Commune

14

Dong Dinh

2848/QD-UBNovember 21, 2002

Vinh Quang Commune

15

President's Memorial HouseTon Duc Thang

177/QD-UBJanuary 28, 2005

NT Quy Cao

Ha Dai Temple

Ben Vua Temple

Tien Lang hot spring

div.maincontent .p { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; } div.maincontent p { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; } div.maincontent .s1 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; font-size: 16pt; } div.maincontent .s2 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s3 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s4 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; font-size: 14pt; } div.maincontent .s5 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; font-size: 14pt; } div.maincontent .s6 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s7 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s8 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; vertical-align: 6pt; } div.maincontent .s9 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 12pt; } div.maincontent .s11 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; tex

45

road/ savings save for children | |||||

12 | Social Security Savings | X | |||

13 | Retirement Savings | X | |||

14 | Accumulated deposit remittance | X | X | ||

15 | Business deposits stock | X | |||

16 | Investment capital deposit Directly abroad | X | |||

17 | Investment capital deposit directly/indirectly into Vietnam | X | |||

18 | Special deposit use | X | |||

19 | Deposit no. periodically | X | |||

20 | Accumulated savings and investment | X | |||

21 | Staff deposit worker | X |

(Source: Compiled from the websites of Vietinbank, BIDV, Agribank, Vietcombank in 2017)

Vietinbank Phu Yen currently has 10 types of deposit products for individual customers and 6 deposit products for corporate customers. In addition to common products such as payment deposits, non-term savings deposits, term savings deposits, Vietinbank Phu Yen also has competitive products such as multi-term savings, multi-purpose investment deposits, overdraft deposits with differences compared to other products.

46

with other banks. Other banks in the area also have attractive, highly competitive products. Agribank Phu Yen has floating interest rate term savings products, social security savings, school savings, flexible non-periodic deposits for many customer groups. BIDV Phu Yen has products such as remittance deposits, securities trading deposits, direct/indirect investment capital deposits in Vietnam, Vietcombank Phu Yen has deposit products such as: savings for children, savings and investment deposits, employee deposits with more utilities than Vietinbank. In general, what are the differences and non-competitiveness of deposit products compared to other banks? Vietinbank needs to design deposit products focusing on different customer groups, with many flexible features when depositing or withdrawing money to bring maximum benefits to customers, to attract more customers to deposit money.

Deposit interest rates are one of the decisive factors for customers to choose to use deposit products and have a direct impact on the market share and operational efficiency of the bank. Currently, Vietinbank's lending products are applying quite low preferential interest rates to aim at credit growth. Therefore, Vietinbank Phu Yen currently maintains deposit interest rates lower than other commercial banks in Phu Yen to achieve a suitable FTP buying and selling price difference to ensure costs and profit targets. Vietinbank Phu Yen also complies with the regulations of the head office and the State Bank on the ceiling interest rates for deposits in USD and VND.

In addition to diverse deposit products, promotional programs and communication programs to promote brand image to attract regular deposits are organized such as savings with prizes, savings with preferential interest rates, direct savings with gifts, lucky draws with valuable gifts, birthday gifts, holiday gifts for regular customers, product introduction at businesses, agencies, etc. However, Vietinbank Phu Yen's promotional programs are limited in number, focusing on the priority customer segment, promotional conditions are still high, customers have not yet enjoyed the maximum promotional programs.

47

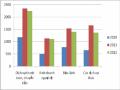

2.3.2.4 Operational network, facilities and information technology system Table 2.3: Operational network of Vietinbank Phu Yen, BIDV Phu Yen, Vietcombank Phu Yen and Agribank Phu Yen as of December 31, 2017

Unit: room, machine

Target

Vietinbank Phu Yen | BIDV Phu Yen | Vietcombank Phu Yen | Agribank Phu Yen | |

Branch | 1 | 1 | 1 | 11 |

PGD | 6 | 3 | 3 | 7 |

ATM | 18 | 13 | 8 | 14 |

(Source: Internal business results report of Vietinbank Phu Yen General Department in 2017)

A bank with a wide network of operations will help customers easily decide to use the service. Expanding the marketing network and ensuring convenience in transactions is very important in mobilizing customer deposits. Vietinbank's network of operations ranks second in Phu Yen. Currently, Vietinbank Phu Yen focuses on developing through the following distribution channels:

- Traditional distribution channel: is the channel for distributing products and services through branches and transaction offices. Currently, Vietinbank Phu Yen has 1 branch and 6 transaction offices operating in Tuy Hoa city and 3 districts of Dong Hoa, Tay Hoa, Song Cau. Traditional network activities contribute increasingly important to the scale and efficiency of commercial banking operations. Regarding the network of branches and transaction offices, Vietinbank Phu Yen is only less than Agribank Phu Yen and higher than other commercial banks in the area.

-Modern distribution channel: is the distribution channel of electronic banking products, mainly through ATM, internet banking...

+ For ATM channel: Currently, in Phu Yen province, Vietinbank is the bank with the largest ATM network in the market in terms of the number of ATMs with 18 ATMs, mainly concentrated in Tuy Hoa city, creating convenience in transactions, attracting an increasing number of customers to deposit money. Thanks to the dense network,

48

Vietinbank Phu Yen has many advantages in deposit mobilization activities, achieving growth in quantity and quality.

+ For Internet banking channel: In 2015-2016, Vietinbank deployed and provided customers with many new products and services with high technology content, with many outstanding utilities such as: SMS banking service, internet banking including Vietinbank Ipay and Ipay mobile. As of December 31, 2016, there were 75 enterprises using Vietinbank Ipay service for corporate customers (Vietinbank eFAST) and 81,920 individual customers using Vietinbank Ipay service with convenient services that best serve customers' product usage needs. These products and services are relatively diverse, meeting the basic and important needs of customers, contributing to enhancing the reputation and brand of Vietinbank Phu Yen. However, because the new system has added many experimental features, the newly converted core banking system often has system errors, transmission errors, and features that do not work properly, so it has not been highly appreciated by customers compared to other banks, and many customer feedbacks complain about service quality. Therefore, in the coming time, it is necessary to continue to improve and upgrade the system to operate better and attract more customers. Another factor

affecting the ability to access banking services is the terrain of Phu Yen province interspersed with many mountains and hills, low population density of 175 people/km2 scattered . Vietinbank Phu Yen also has difficulty attracting potential customers throughout Phu Yen province when the distribution network is still limited, not yet

There are transaction offices in remote districts such as Son Hoa, Song Hinh, Dong Xuan, Phu Hoa.

Regarding facilities, Vietinbank Phu Yen built a spacious and modern main branch office in 2015. The facilities are convenient, meeting the needs of work and customers. The service counters are all arranged neatly and cleanly according to 5S standards, creating a professional image and creating comfort for customers.

Regarding the information technology system, switching to the new Sunshine core system with many improvements over the INCAS system has contributed to better customer service.

49

Given the importance of capital mobilization activities with a large and complex customer database, Vietinbank has proactively developed a modern technology platform capable of maximally supporting the bank's operations. To ensure that the system is not interrupted by errors, the computer department of the accounting department ensures data connection, is responsible for installing equipment, and handles technology-related incidents that arise at the branch, avoiding transaction congestion, affecting waiting time and customer psychology. In addition, with a new core banking system with diverse functions, innovation, and timely updating of customer information quickly is also a channel for increasing deposit mobilization.

2.4 Analysis of factors affecting capital mobilization from deposits at Vietnam Joint Stock Commercial Bank for Industry and Trade - Phu Yen Branch

2.4.1 Research design

2.4.1.1 Research process

Theoretical basis, research model, related hypotheses and given scales

Qualitative research and preliminary factor measurement scale, pilot survey

Build formal scales and survey questionnaires, collect data

Data cleaning, descriptive statistics

Data analysis (Cronbach's Alpha reliability coefficient and EFA exploratory factor analysis)

Complete scale

Linear regression analysis, model fit testing, hypothesis testing

Research and evaluation results, providing appropriate solutions

50

2.4.1.2 Preliminary research

The preliminary research was conducted using qualitative methods, aiming to build an official research model. Through synthesizing the hypotheses of previous studies and interviewing the opinions of 10 test survey subjects who are directors, deputy directors and heads of departments at Vietinbank Phu Yen to make appropriate adjustments, eliminating some unimportant factors and factors that are not suitable for the situation in Vietnam. This research step aims to explore, adjust and supplement the factors affecting deposit mobilization activities into the research model as follows:

- Objective factors include: economic development factors and customer factors.

+ The economic development factor includes 4 observed variables: average income per capita in Phu Yen, economic growth rate of Phu Yen, inflation, economic structure of Phu Yen province.

+ Customer factors include 4 observed variables: customers' cash usage habits, level of influence from acquaintances and media, customer loyalty level, customers' saving habits.

- The subjective factors include brand, bank staff, deposit products and promotional programs, operating network, facilities and information technology systems.

+ Brand includes 3 observed variables: bank brand is a reputable and safe brand; Vietinbank brand is a large brand, operating for many years; the bank's brand is widely known and close to customers.

+ Bank staff includes 3 observed variables: staff with good professional ethics; professional service attitude and style; staff with good knowledge, experience and working skills.

+ Deposit products and promotional programs include 4 observed variables: diverse deposit products, meeting customer needs; attractive deposit interest rates;

51

Deposit promotions and communication programs take place regularly, customer care services after deposit are focused on

+ The network of operations, facilities and information technology systems includes 3 observed variables: a widespread network of transaction points (transaction offices, ATMs, etc.) and convenient transaction locations; spacious and clean facilities; modern and secure information technology systems.

The scale used is an ordinal scale with level 1 being no influence and level 5 being the strongest influence (Appendix 02). The questionnaire was designed with 21 scales (Appendix 01), 01 dependent variable scale and 21 independent variable scales measuring factors affecting capital mobilization activities at Vietinbank Phu Yen. Regarding the determination of sample size, according to authors Hoang Trong and Chu Nguyen Mong Ngoc (2008, page 31), the minimum sample size should be 4 or 5 times the number of survey factors. Thus, in this research topic, 22 factors and 120 survey samples are acceptable.

2.4.1.3 Official research

After the preliminary research results and the survey questionnaire were adjusted appropriately, the official research was conducted using quantitative research methods, re-testing the measurement model as well as the theoretical model and hypotheses in the model. The collected data will be cleaned, processed and analyzed with the support of SPSS 20 software. The scale is tested by Cronbach's Alpha reliability coefficient and EFA exploratory factor analysis, regression analysis.

2.4.2 Research model and hypothesis

2.4.2.1 Research model

Based on the research of Wubitu (2012), synthesizing theories and consulting the opinions of the director, deputy director of the branch and the head of the transaction office at Vietinbank Phu Yen in accordance with reality, the multivariate regression model is used as follows:

HĐTG (Deposit mobilization activities) = β0 + β1*(objective factor group) + β2*(subjective factor group) + ε