Table 25: Results of regression analysis after factor removal

Model

Unstandardized regression coefficients | Standardized regression coefficient | t | Sig. | |||

B | Standard deviation | Beta | ||||

1 | (Constant) | 0.631 | 0.164 | 3,838 | 0.000 | |

HH | 0.227 | 0.040 | 0.338 | 5,629 | 0.000 | |

TC | 0.261 | 0.041 | 0.360 | 6,300 | 0.000 | |

LS | 0.069 | 0.032 | 0.135 | 2,128 | 0.035 | |

DU | 0.122 | 0.043 | 0.178 | 2,816 | 0.006 | |

NV | 0.118 | 0.054 | 0.147 | 2,201 | 0.029 | |

a. Dependent Variable: Y | ||||||

Maybe you are interested!

-

Evaluating customer satisfaction with savings deposit services at National Citizen Commercial Joint Stock Bank NCB Tan Huong Transaction Office - 3

Evaluating customer satisfaction with savings deposit services at National Citizen Commercial Joint Stock Bank NCB Tan Huong Transaction Office - 3 -

Testing Factors Affecting Customer Satisfaction With Savings Deposit Services At Dong A Bank

Testing Factors Affecting Customer Satisfaction With Savings Deposit Services At Dong A Bank -

Assessing customer satisfaction with the quality of medical examination and treatment at Ba Ria General Hospital - 11

Assessing customer satisfaction with the quality of medical examination and treatment at Ba Ria General Hospital - 11 -

The impact of online banking service quality of Vietnam Development Investment Bank on customer satisfaction in Ho Chi Minh City market - 14

The impact of online banking service quality of Vietnam Development Investment Bank on customer satisfaction in Ho Chi Minh City market - 14 -

Factors affecting customer satisfaction with the quality of international money transfer services at Dong A Commercial Joint Stock Bank - 1

Factors affecting customer satisfaction with the quality of international money transfer services at Dong A Commercial Joint Stock Bank - 1

(Source: Results of survey data processing)

Thus the regression function has the following form:

Y = 0.631+ 0.227 HH + 0.261 TC + 0.069 LS + 0.122 DU + 0.118 NV

Through the regression coefficients, we know the importance of the factors participating in the equation. Specifically, the factor "trust factor" has the greatest influence (B=0.261) and followed by the factors "tangible factor", "employee factor", "responsiveness factor", respectively. The factor "interest rate factor" is the factor with the lowest influence (B=0.069). However, in general, all of the above factors have an influence on the dependent variable. If any factor changes, especially the factor "trust " , it can create a change in customer satisfaction with using savings deposit services at the bank.

And when looking at the regression equation above, we see that the coefficient Bo = 0.631 means that when all other coefficients are equal to 0 or customer satisfaction with deposit services is not affected by the above factors, the customer himself is also affected to a certain extent, and this influence is positive, it encourages the customer's decision.

Therefore, banks should rely on the level of influence of factors on customer satisfaction with savings deposit services to propose solutions to further improve customer satisfaction.

2.4.7. Customer assessment of deposit quality on satisfaction scale

In the customer survey, to measure customer satisfaction, the topic used the Likert scale with 5 levels, from 1 point - showing the level of Completely disagree to 5 points - showing the level of completely agree. So when we take the average value for 5 intervals, the corresponding distance in each interval is 0.8 units. On that basis, to facilitate the assessment of the average value (GTTB) of the components, we make the following convention:

Average value 1 to 1.8: bad rating

Average value from 1.8 - below 2.6: bad rating

Average value from 2.6 - below 3.4: average rating

Average value from 3.4 - below 4.2: good rating

Average value from 4.2 - 5: good rating

-Tangible factors

Pair of hypotheses to test:

Table 26: One_Sample_T_test results for tangible factors

Testing factor

GTTB | GTKD | Sig. | |

Banks use modern technology | 3,1818 | 3.18 | 0.984 |

Agribank Phu Vang space is spacious and airy cool | 3,3357 | 3.34 | 0.962 |

Safe and convenient parking | 3,2797 | 3.28 | 0.997 |

Agribank Phu Vang arranges transaction counters, The tables and shelves are very scientific. | 3.3776 | 3.38 | 0.979 |

Bank working hours are convenient for Friend | 3.3776 | 3.38 | 0.978 |

(Source: Results of survey data processing)

The results in the table above show that the observed significance level Sig. is greater than the confidence level of 0.05) which means that we do not have enough basis to reject the hypothesis H0, which means that these average values can be extrapolated to be the average value of the whole. So we see that the level of customer agreement with the tangible factor is in the range (2.6

- 3.4), meaning that the level of customer satisfaction is neutral. According to personal observations during the internship, the reason why customers are still not satisfied with tangible factors is due to the following reasons:

- The technology system being used at the bank is not modern, some machines are still damaged during the working process and serving customers.

- Customers coming to the bank to do transactions have to park their vehicles outdoors, although the bank has built a parking lot for customers, but because there is no clear instruction board, it is easy to mislead customers. Moreover, the parking location is not convenient for customers to park their vehicles.

- The transaction counters are arranged in a messy and unscientific manner. Moreover, the systems of tables and document shelves are also sketchy and unscientific. This is a subjective factor because the banking system has a small number of employees, so there is not enough time to perform all the tasks of customer service and table design.

-The trust factor

Pair of hypotheses to test:

Table 27: One_Sample_T_test results for the reliability factor

Testing factor

GTTB | GTKD | Sig. | |

You trust the information provided by Agribank Phu Vang give you | 3,4196 | 3.42 | 0.996 |

Agribank Phu Vang provides services as promised. introduce | 3.4895 | 3.48 | 0.995 |

Agribank Phu Vang performs transactions accurately, no error | 3.5175 | 3.52 | 0.971 |

Agribank Phu Vang secures customer information well. row | 3.4545 | 3.45 | 0.953 |

(Source: Results of survey data processing)

From the test results, we see that with the observed significance level, the value of sig. > 0.05, so from that result, we are not qualified to reject the hypothesis H0 that the average value of the population is equal to the average value of the survey sample and is in the range (3.4 - 4.2). In other words, the level of customer agreement with the reliability factor is satisfactory. Customers are quite satisfied with this factor, to achieve this, the bank always ensures information security factors, providing information to customers accurately. In addition, it also organizes professional testing sessions for bank employees to create professionalism, avoiding errors in the process of dealing with customers.

-Interest factor

Pair of hypotheses to test:

Table 28: One_Sample_T_test results for interest rate factor

Testing factor

GTTB | GTKD | Sig. | |

Agribank Phu Vang's deposit interest rate is very reasonable. rational, optimal, creating effective profitability | 3,8881 | 3.89 | 0.982 |

Agribank Phu Vang's deposit interest rate is very high. stable | 3.8112 | 3.81 | 0.989 |

Agribank Phu Vang's interest calculation is very clear. and exactly | 3,8392 | 3.84 | 0.992 |

(Source: Results of survey data processing)

Based on the table above, we see that the sig. value is greater than the 0.05 confidence level, so there is not enough basis to reject H0. This shows that the mean value of the sample is the mean value of the population.

The overall average value is between (3.4 - 4.2), which means that customers are satisfied with the interest rate factor. This is also easy to explain because at Agribank Phu Vang, although Agribank Phu Vang branch is a state-owned bank directly managed, the interest rate factor is still considered important and guaranteed by the bank. The bank's interest rate is still stable and competitive compared to other joint stock banks. That is the reason why most customers are satisfied with the bank's interest rate factors.

-Responsiveness factor

Pair of hypotheses to test:

Table 29: One_Sample_T_test results for the responsiveness factor

Testing factor

GTTB | GTKD | Sig. | |

Short transaction waiting time | 3,5944 | 3.59 | 0.952 |

Transaction procedures at Agribank Phu Vang are very simple. | 3.5734 | 3.57 | 0.958 |

Easily find information about deposit services at Agribank Phu Vang | 3,5804 | 3.58 | 0.995 |

(Source: Results of survey data processing) Regarding the customer satisfaction factor, according to the test table, the value is found to be

Sig. > 0.05, from which we see that there is no basis to reject H0, so the average value of the population is within the range of assessing the level of customer satisfaction.

This result can be explained as follows:

- Customers coming to the bank to do transactions usually only wait for 5-10 minutes. However, on some days like Monday, the number of customers coming to do transactions is often quite large. Therefore, some customers have not been served in time.

- Procedures have been minimized by the bank to create simplicity and speed for customers.

-Employee factor

Pair of hypotheses to test:

Table 30: One_Sample_T_test results for employee factor

Testing factor

GTTB | GTKD | Sig. | |

Staff are dressed politely | 3,8042 | 3.80 | 0.955 |

Staff clearly answer and guide your questions about the service. | 3,3986 | 3.40 | 0.983 |

Staff are polite, attentive to you, and have good professional qualifications. | 3,3846 | 3.38 | 0.944 |

Knowledgeable staff to advise you | 3.2727 | 3.27 | 0.970 |

Staff have professional working style | 3.5105 | 3.51 | 0.994 |

(Source: Results of survey data processing)

Similar to the above factors, the observed variables of the staff factor also have an observation level Sig. > 0.05, so there is no basis to reject H0. With the factors "Staff are politely dressed", "Staff answer and clearly guide your questions about the service" and "Staff have a professional working style" the mean is in the satisfaction range. As for the two factors "Staff are polite, attentive to you, have good professional qualifications" and "Staff have knowledge to advise you" the mean is in the neutral range. The reasons why customers are not satisfied with these two factors are:

- Some employees working at the bank are not yet solid in their expertise because they were transferred from other departments, or their training was not in the right field of finance and banking, so their expertise is not good. However, each individual working in the bank constantly studies to improve their expertise and service quality.

- This shows that the staff working at the bank have basically met the requirements of customers well, satisfying customers. However, the number of staff serving at the counter is quite small, so when there are many customers, sometimes some staff are tired, so the service attitude is not attentive and thoughtful.

-Customer care factor

Pair of hypotheses to test:

Table 31: One_Sample_T_test results for customer care factor

Testing factor

GTTB | GTKD | Sig. | |

Agribank Phu Vang has a customer care program. goods on important holidays | 3.6224 | 3.62 | 0.972 |

Agribank Phu Vang has many promotion programs. forever attractive | 3,4406 | 3.44 | 0.994 |

Agribank Phu Vang has many incentives for customers | 3,6084 | 3.60 | 0.981 |

(Source: Results of survey data processing) Looking at the processing table, we can see that with the observed significance level Sig. greater than 0.05. From here, we have no basis to reject H0, so the average value of the population is in the range (3.4 - 4.2), which means that customers coming to transact are satisfied with the customer care factor. On important holidays such as Tet, founding anniversary

Bank...... However, customers are still not completely satisfied because:

- The program can only invite certain large customers and media customers, but cannot be applied to all customers who have participated in deposit activities at the bank due to many different objective factors.

- Promotional activities are still few and not diverse.

- Has not attracted customer attention.

- Many promotional programs are still unknown to customers due to lack of advertising, and employees are not popular with customers, especially with customers with low education levels.

2.4.8. Verify customer evaluation of "quality of deposit service" when classified by customer group

-Testing for gender group differences

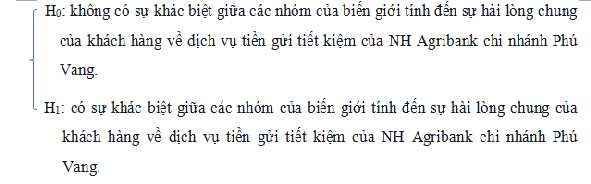

To see if there is a difference in the evaluation of savings deposit services of Agribank Phu Vang branch between male and female customers. The pair of hypotheses are set out in turn:

Table 32: Results of Independent-Sample T - test on differences with gender variable

Savings deposit service review

Levene's Test for Equality of Variances | t-test for Equality of Means | ||||

F | Sig. | T | Df | Sig. (2-tailed) | |

Equal variances assumed | 0.492 | 0.484 | 0.477 | 141 | 0.634 |

Equal variances not assumed | .478 | 132,156 | 0.280 | ||

(Source: Results of survey data processing)

The test results show that the sig. value in T is greater than the significance level of 0.05, so we do not have enough basis to reject the hypothesis H 0 , meaning that there is no difference in the evaluation of savings deposit services of the two groups of male and female customers.

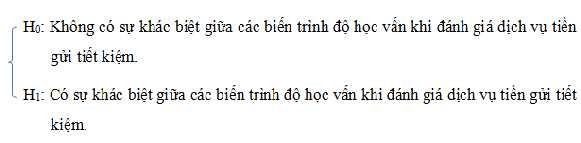

-Testing for differences by educational attainment

Usually, at different educational levels, the perspective of perceiving and evaluating an issue is more or less different. Therefore, the author conducts a test to see whether or not there is a difference between the educational level factor and the customer's evaluation of the service.

Hypothesis pair:

Table 33: ANOVA test results of customers with different education levels

General customer reviews of the service

Sum of Squares | Df | Mean Squares | F | Sig. | |

Between Groups | 2,282 | 3 | .761 | 3.375 | .020 |

Within Groups | 31,331 | 139 | .225 | ||

Total | 33,613 | 142 |

(Source: Results of survey data processing)

Based on the table above, it shows that the sig. value in T is smaller than the significance level of 0.05, so we have enough basis to reject H 0 and accept hypothesis H 1, which means that there is a difference in the evaluation of savings deposit services of Agribank Phu Vang branch for customer groups with different education levels.

Table 34: Average rating of savings deposit services by education level.

Level

N | GTTB | |

High school or lower | 52 | 3.5192 |

Secondary, College | 26 | 3.5000 |

University | 31 | 3.2366 |

Postgraduate | 34 | 3.2843 |

Total | 143 | 3.3986 |

(Source: Results of survey data processing)

Looking at the table above, we can see that the overall satisfaction level of customers with the savings deposit service of Agribank Phu Vang branch is usually the highest among high school graduates or lower. The second highest are customers with intermediate and college degrees. And the two groups of customers with university or postgraduate degrees are the two groups with the lowest overall satisfaction level.

This can be easily explained because the higher the level of education of customers, the more difficult it is to evaluate the quality of service. And the group with lower education level will have an easier time evaluating the quality of service. Based on this result, the bank can adjust the related factors to suit each of the above customer groups to get a higher appreciation from customers for the savings deposit service.

CHAPTER 3

SOME SOLUTIONS TO IMPROVE THE QUALITY OF SAVINGS DEPOSITS AT AGRIBANK PHU VANG BRANCH

3.1. Orientation in capital mobilization in the coming time at the Bank for Agriculture and Rural Development of Thua Thien Hue - Phu Vang branch

In the operation of commercial banks, capital mobilization and capital use are two main operations and decide the existence of the bank. Capital mobilization is the condition and premise for performing capital use operations and if the capital use is effective, it will have a positive impact on the capital mobilization of the bank.

Through practical analysis, we can see that in recent years, capital mobilization at the bank has achieved many successes and encouraging results. And to achieve even greater results in the following years, the bank needs to orient and develop solutions as follows:

- Successfully complete all political tasks of the bank, pay more attention to personnel work. Maintain opening of professional training courses to improve professional qualifications for staff to meet the requirements of the industry.

- Raise awareness of compliance with policies and mechanisms, strengthen internal inspection and control, and minimize risks.

- Actively promote capital mobilization measures to maintain and develop capital sources, gradually improve and create a balanced and stable capital structure.

- Further enhance the bank's products and services, renew the utilities for its traditional products.

- Continue to promote the Party's leadership role in directing the implementation of all business tasks. Develop practical competition criteria associated with all activities of the organization to create a vibrant competitive atmosphere in the agency, contributing to promoting business development.

- Develop a plan to implement fast money transfer, Western Union, and ATM card opening at all transaction points, along with promoting new products to everyone.