BIDV's creditworthiness is still low, because it still has the advantage of lending to businesses (supply side). These loans have a larger loan size (tens of billions of VND or more) than loans to meet the housing needs of businesses, and the appraisal of customers and control of loan use is much easier. On the contrary, CVNO activities incur more costs than loans to finance real estate investment projects of businesses. This activity also has many potential risks when the appraisal of creditworthiness of businesses is difficult, there is no updated information, control and sharing from the system of other commercial banks and credit information providers. In addition, the units in the retail sector as units advising the Board of Directors on the design of retail products including CVNO products, building policy mechanisms and organizing the implementation of CVNO products are sometimes inadequate, not meeting market requirements, not close to business practice. These are the main factors that make BIDV not pay enough attention to this activity compared to the potential that the bank can meet.

The retail business model at branches has not really been standardized and has not promoted retail activities, and the sales organization is not professional. Branches have not arranged staff reasonably, still focusing on operations, and the number of customer service managers is small. The functions and tasks of customer service managers are still linked to bad debt and risk management, which has limited the sales work of staff in terms of both time and motivation. The KPI system for staff is still simple (mainly indicators on credit scale, credit classification, etc.) and has not really created sales motivation for staff.

(2) Credit mechanisms and policies have not yet met the requirements of CVNO operations.

Administrative procedures related to credit granting are still cumbersome (too many signatures, credit granting forms, especially the TSDB file). With strict requirements from the bank, to borrow money at BIDV, customers must meet the loan conditions and must prepare the correct documents, so they have to go back and forth many times and spend a lot of time to complete the loan application. This causes fear, reducing the desire of customers to go to the bank to borrow money. Currently, BIDV's processing time for a complete application is 7 working days, in which ACB only takes 24h - 48h, Ban Viet Bank only needs 4h to decide whether to accept or not. This shows that if BIDV does not care about shortening the decision-making time, it will directly affect the outstanding CVNO debt at BIDV.

Incentive mechanisms for science and technology (through direct channels), brokerage commissions for investors/residential real estate businesses (through indirect channels), and commissions for units in the chain of modern distribution channels in housing credit activities are slow to adjust, not creating motivation to promote the development of CVNO scale.

108

The CVNO policy is reflected in the low loan amount and loan term and is not suitable for the needs of customers. With the home repair loan product at BIDV, the common loan term is 5 years, the maximum home purchase loan term is only up to 20 years while many commercial banks have implemented home purchase loans with loan terms up to 25 years. With the form of unsecured loans for employees, the loan amount is still low, the loan term is too short. Meanwhile, with the ACB employee loan product, the loan amount can be up to 250 million VND with a loan term of up to 36 months. For employees, the demand for consumer loans is very large, but with a maximum loan amount of 50 million VND, implementing large spending plans such as buying a house, buying land to build a house and housing-related needs is very difficult. (The maximum loan amount that branches apply to employees is only 50 million VND and the maximum loan term is 36 months). If the bank increases the loan limit and extends the loan term, it will meet a larger number of customer needs, helping to increase sales and outstanding loans.

(3) Limited human resources

This is a significant obstacle to BIDV's market share development. The human factor plays a key role, deciding the success or failure, the development of an industry, a field, an enterprise. Most credit officers, although well-trained in banking, are young officers, have little experience, and have low self-training ability. This will affect the quality of transactions and customer service. The ability to meet staff standards in the context of deep integration is still low. Some branch officers do not have good sales and customer persuasion skills, and branches have not arranged enough departments to advise customers to improve service quality. The branch leadership team still lacks business experience and customer relations, and focuses on operations, leading to limitations in the scale and business efficiency of the branches.

(4) Technology projects are slow to deploy (through many levels of approval), so support for CVNO operations is limited, service quality and labor productivity are not high.

Modern technology projects and distribution channels have not been implemented much, market share is still low, CVNO activities in the form of using short-term capital have not been applied through modern channels through overdraft accounts but mainly still perform loans by item. The Corebanking system is in the process of being considered for replacement, operations at branches must go through many processes affecting labor productivity and customer service quality. Technology increases automation, supports improving labor productivity, and risk management in CVNO activities for customers is still poor.

(5) Underdeveloped bank marketing activities

The method of introducing CVNO products is still passive and unprofessional. Currently, BIDV mainly implements through quite classic methods such as introducing CVNO products through banners at transaction points, billboards on the road, through VOV traffic radio waves, through some popular websites. BIDV has not promoted cooperation with real estate companies and real estate agents as intermediaries in CVNO. BIDV has not yet fully exploited the advantages of internet and media communications that BIDV has invested in, the website interface is not as attractive as that of other commercial banks, such as: the interface on HSBC Vietnam's website helps customers easily satisfy the need for basic information about loans to meet the accommodation needs provided by the bank. This has reduced competitiveness as well as not increased sales and outstanding loans of CVNO.

(6) The quality of CVNO services to meet customers' needs is only average, not commensurate with the expectations of a leading bank in the banking industry regarding CVNO.

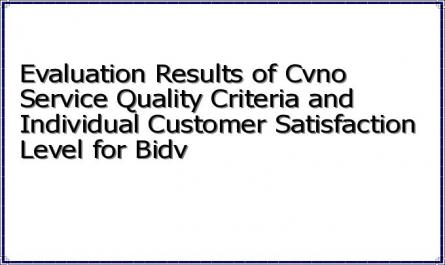

Through the survey and analysis of primary data of NCS on CVNO quality criteria according to SERVQUAL (see Appendix 4), the results obtained show that the evaluation scores of CVNO service quality criteria do not differ much between factors. The highest evaluation score belongs to TG (transaction time) (µ = 3.2; SD = 0.83278) and the lowest is DC (empathy) (µ = 3.0738, SD = 0.70179); the level of customer satisfaction with BIDV CVNO service is quite good (µ = 3.1411, SD = 0.59616) (Table 3.10).

Table 3.18. Results of evaluation of CVNO service quality criteria and individual customer satisfaction with BIDV

Research variables

Average (µ) | Standard deviation (SD) | |

TC | 3.3223 | .67524 |

DC | 3.0738 | .70179 |

NL | 3.1238 | .65620 |

TG | 3.2000 | .83278 |

HL | 3.1411 | .59616 |

Maybe you are interested!

-

Solutions for tourism development in Tien Lang - 10

zt2i3t4l5ee

zt2a3gstourism, tourism development

zt2a3ge

zc2o3n4t5e6n7ts

- District People's Committees and authorities of communes with tourist attractions should support, promote, and provide necessary information to people, helping them improve their knowledge about tourism. Raise tourism awareness for local people.

*

* *

Due to limited knowledge and research time, the thesis inevitably has shortcomings. Therefore, I look forward to receiving guidance from teachers, experts as well as your comments to make the thesis more complete.

Chapter III Conclusion

Through the issues presented in Chapter II, we can come to some conclusions:

Based on the strengths of available tourism resources, the types of tourism in Tien Lang that need to be promoted in the coming time are sightseeing and resort tourism, discovery tourism, weekend tourism. To improve the quality and diversify tourism products, Tien Lang district needs to combine with local cultural tourism resources, at the same time combine with surrounding areas, build rich tourism products. The strengths of Tien Lang tourism are eco-tourism and cultural tourism, so developing Tien Lang tourism must always go hand in hand with restoring and preserving types of cultural tourism resources. Some necessary measures to support and improve the efficiency of exploiting tourism resources in Tien Lang are: strengthening the construction of technical facilities and labor force serving tourism, actively promoting and advertising tourism, and expanding forms of capital mobilization for tourism development.

CONCLUDE

I Conclusion

1. Based on the results achieved within the framework of the thesis's needs, some basic conclusions can be drawn as follows:

Tien Lang is a locality with great potential for tourism development. The relatively abundant cultural tourism resources and ecological tourism resources have great appeal to tourists. Based on this potential, Tien Lang can build a unique tourism industry that is competitive enough with other localities within Hai Phong city and neighboring areas.

In recent years, the exploitation of the advantages of resources to develop tourism and build tourist routes in Tien Lang has not been commensurate with the available potential. In terms of quantity, many resource objects have not been brought into the purpose of tourism development. In terms of time, the regular service time has not been extended to attract more visitors. Infrastructure and technical facilities are still weak. The labor force is still thin and weak in terms of expertise. Tourism programs and routes have not been organized properly, the exploitation content is still monotonous, so it has not attracted many visitors. Although resources have not been mobilized much for tourism development, they are facing the risk of destruction and degradation.

2. Based on the results of investigation, analysis, synthesis, evaluation and selective absorption of research results of related topics, the thesis has proposed a number of necessary solutions to improve the efficiency of exploiting tourism resources in Tien Lang such as: promoting the restoration and conservation of tourism resources, focusing on investment and key exploitation of ecotourism resources, strengthening the construction of infrastructure and tourism workforce. Expanding forms of capital mobilization. In addition, the thesis has built a number of tourist routes of Hai Phong in which Tien Lang tourism resources play an important role.

Exploiting Tien Lang tourism resources for tourism development is currently facing many difficulties. The above measures, if applied synchronously, will likely bring new prospects for the local tourism industry, contributing to making Tien Lang tourism an important economic sector in the district's economic structure.

REFERENCES

1. Nhuan Ha, Trinh Minh Hien, Tran Phuong, Hai Phong - Historical and cultural relics, Hai Phong Publishing House, 1993

2. Hai Phong City History Council, Hai Phong Gazetteer, Hai Phong Publishing House, 1990.

3. Hai Phong City History Council, History of Tien Lang District Party Committee, Hai Phong Publishing House, 1990.

4. Hai Phong City History Council, University of Social Sciences and Humanities, VNU, Hai Phong Place Names Encyclopedia, Hai Phong Publishing House. 2001.

5. Law on Cultural Heritage and documents guiding its implementation, National Political Publishing House, Hanoi, 2003.

6. Tran Duc Thanh, Lecture on Tourism Geography, Faculty of Tourism, University of Social Sciences and Humanities, VNU, 2006

7. Hai Phong Center for Social Sciences and Humanities, Some typical cultural heritages of Hai Phong, Hai Phong Publishing House, 2001

8. Nguyen Ngoc Thao (editor-in-chief, Tourism Geography, Hai Phong Publishing House, two volumes (2001-2002)

9. Nguyen Minh Tue and group of authors, Hai Phong Tourism Geography, Ho Chi Minh City Publishing House, 1997.

10. Nguyen Thanh Son, Hai Phong Tourism Territory Organization, Associate Doctoral Thesis in Geological Geography, Hanoi, 1996.

11. Decision No. 2033/QD – UB on detailed planning of Tien Lang town, Hai Phong city until 2020.

12. Department of Culture, Information, Hai Phong Museum, Hai Phong relics

- National ranked scenic spot, Hai Phong Publishing House, 2005. 13. Tien Lang District People's Committee, Economic Development Planning -

Culture - Society of Tien Lang district to 2010.

14.Website www.HaiPhong.gov.vn

APPENDIX 1

List of national ranked monuments

STT

Name of the monument

Number, year of decisiondetermine

Location

1

Gam Temple

938 VH/QĐ04/08/1992

Cam Khe Village- Toan Thang commune

2

Doc Hau Temple

9381 VH/QĐ04/08/1992

Doc Hau Village –Toan Thang commune

3

Cuu Doi Communal House

3207 VH/QĐDecember 30, 1991

Zone II of townTien Lang

4

Ha Dai Temple

938 VH/QĐ04/08/1992

Ha Dai Village –Tien Thanh commune

APPENDIX II

STT

Name of the monument

Number, year of decision

Location

1

Phu Ke Pagoda Temple

178/QD-UBJanuary 28, 2005

Zone 1 - townTien Lang

2

Trung Lang Temple

178/QD-UBJanuary 28, 2005

Zone 4 – townTien Lang

3

Bao Khanh Pagoda

1900/QD-UBAugust 24, 2006

Nam Tu Village -Kien Thiet commune

4

Bach Da Pagoda

1792/QD-UB11/11/2002

Hung Thang Commune

5

Ngoc Dong Temple

177/QD-UBNovember 27, 2005

Tien Thanh Commune

6

Tomb of Minister TSNhu Van Lan

2848/QD-UBSeptember 19, 2003

Nam Tu Village -Kien Thiet commune

7

Canh Son Stone Temple

2160/QD-UBSeptember 19, 2003

Van Doi Commune –Doan Lap

8

Meiji Temple

2259/QD-UBSeptember 19, 2002

Toan Thang Commune

9

Tien Doi Noi Temple

477/QD-UBSeptember 19, 2005

Doan Lap Commune

10

Tu Doi Temple

177/QD-UBJanuary 28, 2005

Doan Lap Commune

11

Duyen Lao Temple

177/QD-UBJanuary 28, 2005

Tien Minh Commune

12

Dinh Xuan Uc Pagoda

177/QD-UBJanuary 28, 2005

Bac Hung Commune

13

Chu Khe Pagoda

177/QD-UBJanuary 28, 2005

Hung Thang Commune

14

Dong Dinh

2848/QD-UBNovember 21, 2002

Vinh Quang Commune

15

President's Memorial HouseTon Duc Thang

177/QD-UBJanuary 28, 2005

NT Quy Cao

Ha Dai Temple

Ben Vua Temple

Tien Lang hot spring

div.maincontent .p { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; } div.maincontent p { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; } div.maincontent .s1 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; font-size: 16pt; } div.maincontent .s2 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s3 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s4 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; font-size: 14pt; } div.maincontent .s5 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; font-size: 14pt; } div.maincontent .s6 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s7 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s8 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; vertical-align: 6pt; } div.maincontent .s9 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 12pt; } div.maincontent .s11 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; tex

Solutions for tourism development in Tien Lang - 10

zt2i3t4l5ee

zt2a3gstourism, tourism development

zt2a3ge

zc2o3n4t5e6n7ts

- District People's Committees and authorities of communes with tourist attractions should support, promote, and provide necessary information to people, helping them improve their knowledge about tourism. Raise tourism awareness for local people.

*

* *

Due to limited knowledge and research time, the thesis inevitably has shortcomings. Therefore, I look forward to receiving guidance from teachers, experts as well as your comments to make the thesis more complete.

Chapter III Conclusion

Through the issues presented in Chapter II, we can come to some conclusions:

Based on the strengths of available tourism resources, the types of tourism in Tien Lang that need to be promoted in the coming time are sightseeing and resort tourism, discovery tourism, weekend tourism. To improve the quality and diversify tourism products, Tien Lang district needs to combine with local cultural tourism resources, at the same time combine with surrounding areas, build rich tourism products. The strengths of Tien Lang tourism are eco-tourism and cultural tourism, so developing Tien Lang tourism must always go hand in hand with restoring and preserving types of cultural tourism resources. Some necessary measures to support and improve the efficiency of exploiting tourism resources in Tien Lang are: strengthening the construction of technical facilities and labor force serving tourism, actively promoting and advertising tourism, and expanding forms of capital mobilization for tourism development.

CONCLUDE

I Conclusion

1. Based on the results achieved within the framework of the thesis's needs, some basic conclusions can be drawn as follows:

Tien Lang is a locality with great potential for tourism development. The relatively abundant cultural tourism resources and ecological tourism resources have great appeal to tourists. Based on this potential, Tien Lang can build a unique tourism industry that is competitive enough with other localities within Hai Phong city and neighboring areas.

In recent years, the exploitation of the advantages of resources to develop tourism and build tourist routes in Tien Lang has not been commensurate with the available potential. In terms of quantity, many resource objects have not been brought into the purpose of tourism development. In terms of time, the regular service time has not been extended to attract more visitors. Infrastructure and technical facilities are still weak. The labor force is still thin and weak in terms of expertise. Tourism programs and routes have not been organized properly, the exploitation content is still monotonous, so it has not attracted many visitors. Although resources have not been mobilized much for tourism development, they are facing the risk of destruction and degradation.

2. Based on the results of investigation, analysis, synthesis, evaluation and selective absorption of research results of related topics, the thesis has proposed a number of necessary solutions to improve the efficiency of exploiting tourism resources in Tien Lang such as: promoting the restoration and conservation of tourism resources, focusing on investment and key exploitation of ecotourism resources, strengthening the construction of infrastructure and tourism workforce. Expanding forms of capital mobilization. In addition, the thesis has built a number of tourist routes of Hai Phong in which Tien Lang tourism resources play an important role.

Exploiting Tien Lang tourism resources for tourism development is currently facing many difficulties. The above measures, if applied synchronously, will likely bring new prospects for the local tourism industry, contributing to making Tien Lang tourism an important economic sector in the district's economic structure.

REFERENCES

1. Nhuan Ha, Trinh Minh Hien, Tran Phuong, Hai Phong - Historical and cultural relics, Hai Phong Publishing House, 1993

2. Hai Phong City History Council, Hai Phong Gazetteer, Hai Phong Publishing House, 1990.

3. Hai Phong City History Council, History of Tien Lang District Party Committee, Hai Phong Publishing House, 1990.

4. Hai Phong City History Council, University of Social Sciences and Humanities, VNU, Hai Phong Place Names Encyclopedia, Hai Phong Publishing House. 2001.

5. Law on Cultural Heritage and documents guiding its implementation, National Political Publishing House, Hanoi, 2003.

6. Tran Duc Thanh, Lecture on Tourism Geography, Faculty of Tourism, University of Social Sciences and Humanities, VNU, 2006

7. Hai Phong Center for Social Sciences and Humanities, Some typical cultural heritages of Hai Phong, Hai Phong Publishing House, 2001

8. Nguyen Ngoc Thao (editor-in-chief, Tourism Geography, Hai Phong Publishing House, two volumes (2001-2002)

9. Nguyen Minh Tue and group of authors, Hai Phong Tourism Geography, Ho Chi Minh City Publishing House, 1997.

10. Nguyen Thanh Son, Hai Phong Tourism Territory Organization, Associate Doctoral Thesis in Geological Geography, Hanoi, 1996.

11. Decision No. 2033/QD – UB on detailed planning of Tien Lang town, Hai Phong city until 2020.

12. Department of Culture, Information, Hai Phong Museum, Hai Phong relics

- National ranked scenic spot, Hai Phong Publishing House, 2005. 13. Tien Lang District People's Committee, Economic Development Planning -

Culture - Society of Tien Lang district to 2010.

14.Website www.HaiPhong.gov.vn

APPENDIX 1

List of national ranked monuments

STT

Name of the monument

Number, year of decisiondetermine

Location

1

Gam Temple

938 VH/QĐ04/08/1992

Cam Khe Village- Toan Thang commune

2

Doc Hau Temple

9381 VH/QĐ04/08/1992

Doc Hau Village –Toan Thang commune

3

Cuu Doi Communal House

3207 VH/QĐDecember 30, 1991

Zone II of townTien Lang

4

Ha Dai Temple

938 VH/QĐ04/08/1992

Ha Dai Village –Tien Thanh commune

APPENDIX II

STT

Name of the monument

Number, year of decision

Location

1

Phu Ke Pagoda Temple

178/QD-UBJanuary 28, 2005

Zone 1 - townTien Lang

2

Trung Lang Temple

178/QD-UBJanuary 28, 2005

Zone 4 – townTien Lang

3

Bao Khanh Pagoda

1900/QD-UBAugust 24, 2006

Nam Tu Village -Kien Thiet commune

4

Bach Da Pagoda

1792/QD-UB11/11/2002

Hung Thang Commune

5

Ngoc Dong Temple

177/QD-UBNovember 27, 2005

Tien Thanh Commune

6

Tomb of Minister TSNhu Van Lan

2848/QD-UBSeptember 19, 2003

Nam Tu Village -Kien Thiet commune

7

Canh Son Stone Temple

2160/QD-UBSeptember 19, 2003

Van Doi Commune –Doan Lap

8

Meiji Temple

2259/QD-UBSeptember 19, 2002

Toan Thang Commune

9

Tien Doi Noi Temple

477/QD-UBSeptember 19, 2005

Doan Lap Commune

10

Tu Doi Temple

177/QD-UBJanuary 28, 2005

Doan Lap Commune

11

Duyen Lao Temple

177/QD-UBJanuary 28, 2005

Tien Minh Commune

12

Dinh Xuan Uc Pagoda

177/QD-UBJanuary 28, 2005

Bac Hung Commune

13

Chu Khe Pagoda

177/QD-UBJanuary 28, 2005

Hung Thang Commune

14

Dong Dinh

2848/QD-UBNovember 21, 2002

Vinh Quang Commune

15

President's Memorial HouseTon Duc Thang

177/QD-UBJanuary 28, 2005

NT Quy Cao

Ha Dai Temple

Ben Vua Temple

Tien Lang hot spring

div.maincontent .p { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; } div.maincontent p { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; } div.maincontent .s1 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; font-size: 16pt; } div.maincontent .s2 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s3 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s4 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; font-size: 14pt; } div.maincontent .s5 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; font-size: 14pt; } div.maincontent .s6 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s7 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s8 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; vertical-align: 6pt; } div.maincontent .s9 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 12pt; } div.maincontent .s11 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; tex -

Identify Rating Levels and Rating Scales

zt2i3t4l5ee

zt2a3gstourism,quan lan,quang ninh,ecology,ecotourism,minh chau,van don,geography,geographical basis,tourism development,science

zt2a3ge

zc2o3n4t5e6n7ts

of the islanders. Therefore, this indicator will be divided into two sub-indicators:

a1. Natural tourism attractiveness a2. Cultural tourism attractiveness

b. Tourist capacity

The two island communes in Quan Lan have different capacities to receive tourists. Minh Chau Commune is home to many standard hotels and resorts, attracting high-income domestic and international tourists. Meanwhile, Quan Lan Commune has many motels mainly built and operated by local people, so the scale and quality are not high, and will be suitable for ordinary tourists such as students.

c. Time of exploitation of Quan Lan Island Commune:

Quan Lan tourism is seasonal due to weather and climate conditions and festivals only take place on certain days of the year, specifically in spring. In Quan Lan commune, the period from April to June and from September to November is considered the best time to visit Quan Lan because the cultural tourism activities are mainly associated with festivals taking place during this time.

Minh Chau island commune:

Tourism exploitation time is all year round, because this is a place with a number of tourist attractions with diverse ecosystems such as Bai Tu Long National Park Research Center, Tram forest, Turtle Laying Beach, so besides coming to the beach for tourism and vacation in the summer, Minh Chau will attract research groups to come for tourism combined with research at other times of the year.

d. Sustainability

The sustainability of ecotourism sites in Quan Lan and Minh Chau communes depends on the sensitivity of the ecosystems to climate changes.

landscape. In general, these tourist destinations have a fairly high level of sustainability, because they are natural ecosystems, planned and protected. However, if a large number of tourists gather at certain times, it can exceed the carrying capacity and affect the sustainability of the environment (polluted beaches, damaged trees, animals moving away from their habitats, etc.), then the sustainability of the above ecosystems (natural ecosystems, human ecosystems) will also be affected and become less sustainable.

e. Location and accessibility

Both island communes have ports to take tourists to visit from Van Don wharf:

- Quan Lan – Van Don traffic route:

Phuc Thinh – Viet Anh high-speed boat and Quang Minh high-speed boat, depart at 8am and 2pm from Van Don to Quan Lan, and at 7am and 1pm from Quan Lan to Van Don. There are also wooden boats departing at 7am and 1pm.

- Van Don - Minh Chau traffic route:

Chung Huong high-speed train, Minh Chau train, morning 7:30 and afternoon 13:30 from Van Don to Minh Chau, morning 6:30 and afternoon 13:00 from Minh Chau to Van Don.

f. Infrastructure

Despite receiving investment attention, the issue of infrastructure and technical facilities for tourism on Quan Lan Island is still an issue that needs to be resolved because it has a direct impact on the implementation of ecotourism activities. The minimum conditions for serving tourists such as accommodation, electricity, water, communication, especially medical services, and security work need to be given top priority. Ecotourism spots in Minh Chau commune are assessed to have better infrastructure and technical facilities for tourism because there are quite complete and synchronous conditions for serving tourists, meeting many needs of domestic and foreign tourists.

3.2.1.4. Determine assessment levels and assessment scales

Corresponding to the levels of each criterion, the index is the score of those levels in the order of 4, 3, 2, 1 decreasing according to the standard of each level: very attractive (4), attractive (3), average (2), less attractive (1).

3.2.1.5. Determining the coefficients of the criteria

For the assessment of DLST in the two communes of Quan Lan and Minh Chau islands, the students added evaluation coefficients to show the importance of the criteria and indicators as follows:

Coefficient 3 with criteria: Attractiveness, Exploitation time. These are the 2 most important criteria for attracting tourists to tourism in general and eco-tourism in particular, so they have the highest coefficient.

Coefficient 2 with criteria: Capacity, Infrastructure, Location and accessibility . Because the assessment area is an island commune of Van Don district, the above criteria are selected by the author with appropriate coefficients at the average level.

Coefficient 1 with criteria: Sustainability. Quan Lan has natural and human-made ecotourism sites, with high biodiversity and little impact from local human factors. Most of the ecotourism sites are still wild, so they are highly sustainable.

3.2.1.6. Results of DLST assessment on Quan Lan island

a. Assessment of the potential for natural tourism development

For Minh Chau commune:

+ Natural tourism attractiveness is determined to be very attractive (4 points) and the most important coefficient (coefficient 3), so the score of the Attractiveness criterion is 4 x 3 = 12.

+ Capacity is determined as average (2 points) and the coefficient is quite important (coefficient 2), then the score of Capacity criterion is 2 x 2 = 4.

+ Exploitation time is long (4 points), the most important coefficient (coefficient 3) so the score of the Exploitation time criterion is 4 x 3 = 12.

+ Sustainability is determined as sustainable (4 points), the important coefficient is the average coefficient (coefficient 1), so the score of the Sustainability criterion is 4 x 1 = 4 points

+ Location and accessibility are determined to be quite favorable (2 points), the coefficient is quite important (coefficient 2), the criterion score is 2 x 2 = 4 points.

+ Infrastructure is assessed as good (3 points), the coefficient is quite important (coefficient 2), then the score of the Infrastructure criterion is 3 x 2 = 6 points.

The total score for evaluating DLST in Minh Chau commune according to 6 evaluation criteria is determined as: 12 + 4 + 12 + 4 + 4 + 6 = 42 points

Similar assessment for Quan Lan commune, we have the following table:

Table 3.3: Assessment of the potential for natural ecotourism development in Quan Lan and Minh Chau communes

Attractiveness of self-tourismof course

Capacity

Mining time

Sustainability

Location and accessibility

Infrastructure

Result

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

CommuneMinh Chau

12

12

4

8

12

12

4

4

4

8

6

8

42/52

Quan CommuneLan

6

12

6

8

9

12

4

4

4

8

4

8

33/52

b. Assessment of the potential for humanistic tourism development

For Quan Lan commune:

+ The attractiveness of human tourism is determined to be very attractive (4 points) and the most important coefficient (coefficient 3), so the score of the Attractiveness criterion is 4 x 3 = 12.

+ Capacity is determined to be large (3 points) and the coefficient is quite important (coefficient 2), then the score of the Capacity criterion is 3 x 2 = 6.

+ Mining time is average (3 points), the most important coefficient (coefficient 3) so the score of the Mining time criterion is 3 x 3 = 9.

+ Sustainability is determined as sustainable (4 points), the important coefficient is the average coefficient (coefficient 1), so the score of the Sustainability criterion is 4 x 1 = 4 points.

+ Location and accessibility are determined to be quite favorable (2 points), the coefficient is quite important (coefficient 2), the criterion score is 2 x 2 = 4 points.

+ Infrastructure is rated as average (2 points), the coefficient is quite important (coefficient 2), then the score of the Infrastructure criterion is 2 x 2 = 4 points.

The total score for evaluating DLST in Quan Lan commune according to 6 evaluation criteria is determined as: 12 + 6 + 6 + 4 + 4 + 4 = 36 points.

Similar assessment with Minh Chau commune we have the following table:

Table 3.4: Assessment of the potential for developing humanistic eco-tourism in Quan Lan and Minh Chau communes

Attractiveness of human tourismliterature

Capacity

Mining time

Sustainability

Location and accessibility

Infrastructure

Result

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Quan CommuneLan

12

12

6

8

9

12

4

4

4

8

4

8

39/52

Minh CommuneChau

6

12

4

8

12

12

4

4

4

8

6

8

36/52

Basically, both Minh Chau and Quan Lan localities have quite favorable conditions for developing ecotourism. However, Quan Lan commune has more advantages to develop ecotourism in a humanistic direction, because this is an area with many famous historical relics such as Quan Lan Communal House, Quan Lan Pagoda, Temple worshiping the hero Tran Khanh Du, ... along with local festivals held annually such as the wind praying ceremony (March 15), Quan Lan festival (June 10-19); due to its location near the port and long exploitation time, the beaches in Quan Lan commune (especially Quan Lan beach) are no longer hygienic and clean to ensure the needs of tourists coming to relax and swim; this is also an area with many beautiful landscapes such as Got Beo wind pass, Ong Phong head, Voi Voi cave, but the ability to access these places is still very limited (dirt hill road, lots of gravel and rocks), especially during rainy and windy times; In addition, other natural resources such as mangrove forests and sea worms have not been really exploited for tourism purposes and ecotourism development. On the contrary, Minh Chau commune has more advantages in developing ecotourism in the direction of natural tourism, this is an area with diverse ecosystems such as at Rua De Beach, Bai Tu Long National Park Conservation Center...; Minh Chau beach is highly appreciated for its natural beauty and cleanliness, ranked in the top ten most beautiful beaches in Vietnam; Minh Chau commune is also home to Tram forest with a large area and a purity of up to 90%, suitable for building bridges through the forest (a very effective type of natural ecotourism currently applied by many countries) for tourists to sightsee, as well as for the purpose of studying and researching.

Figure 3.1: Thenmala Forest Bridge (India) Source: https://www.thenmalaecotourism.com/(August 21, 2019)

3.2.2. Using SWOT matrix to evaluate Quan Lan island tourism

General assessment of current tourism activities of Quan Lan island is shown through the following SWOT matrix:

Table 3.5: SWOT matrix evaluating tourism activities on Quan Lan island

Internal agent

Strengths- There is a lot of potential for tourism development, especially natural ecotourism and humanistic ecotourism.- The unskilled labor force is relatively abundant.- resource environmentunpolluted, still

Weaknesses- Poorly developed infrastructure, especially traffic routes to tourist destinations on the island.- The team of professional staff is still weak.- Tourism products in general

quite wild, originalintact

general and DLST in particularalone is monotonous.

External agents

Opportunity- Tourism is a key industry in the socio-economic development strategy of the province and Van Don economic zone.- Quan Lan was selected as a pilot area for eco-tourism development within the framework of the green growth project between Quang Ninh province and the Japanese organization JICA.- The flow of tourists and especially ecotourism in the world tends toincreasing

Challenge- Weather and climate change abnormally.- Competition in tourism products is increasingly fierce, especially with other localities in the province such as Ha Long, Mong Cai...- Awareness of tourists, especially domestic tourists, about ecotourism and nature conservation is not high.

Through summary analysis using SWOT matrix we see that:

To exploit strengths and take advantage of opportunities, it is necessary to:

- Diversify products and service types (build more tourism routes aimed at specific needs of tourists: experiential tourism immersed in nature, spiritual cultural tourism...)

- Effective exploitation of resources and differentiated products (natural resources and human resources)

div.maincontent .p { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; } div.maincontent p { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; } div.maincontent .s1 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 13pt; } div.maincontent .s2 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 13pt; } div.maincontent .s3 { color: #0D0D0D; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s4 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s5 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s6 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; vertical-align: -3pt; } div.maincontent .s7 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; vertical-align: -2pt; } div.maincontent .s8 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; vertical-align: -1pt; } div.maincontent .s9 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s10 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s11 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s12 { color: black; font-family:Symbol, serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s13 { color: black; font-family:Wingdings; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s14 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; vertical-align: 5pt; } div.maincontent .s15 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; vertical-align: 5pt; } div.maincontent .s16 { color: black; font-family:Cambria, serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s17 { color: #080808; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s18 { color: #080808; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s19 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 11pt; } div.maincontent .s20 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10pt; } div.maincontent .s21 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 11pt; } div.maincontent .s22 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 11pt; } div.maincontent .s23 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s24 { color: #212121; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; tex

Identify Rating Levels and Rating Scales

zt2i3t4l5ee

zt2a3gstourism,quan lan,quang ninh,ecology,ecotourism,minh chau,van don,geography,geographical basis,tourism development,science

zt2a3ge

zc2o3n4t5e6n7ts

of the islanders. Therefore, this indicator will be divided into two sub-indicators:

a1. Natural tourism attractiveness a2. Cultural tourism attractiveness

b. Tourist capacity

The two island communes in Quan Lan have different capacities to receive tourists. Minh Chau Commune is home to many standard hotels and resorts, attracting high-income domestic and international tourists. Meanwhile, Quan Lan Commune has many motels mainly built and operated by local people, so the scale and quality are not high, and will be suitable for ordinary tourists such as students.

c. Time of exploitation of Quan Lan Island Commune:

Quan Lan tourism is seasonal due to weather and climate conditions and festivals only take place on certain days of the year, specifically in spring. In Quan Lan commune, the period from April to June and from September to November is considered the best time to visit Quan Lan because the cultural tourism activities are mainly associated with festivals taking place during this time.

Minh Chau island commune:

Tourism exploitation time is all year round, because this is a place with a number of tourist attractions with diverse ecosystems such as Bai Tu Long National Park Research Center, Tram forest, Turtle Laying Beach, so besides coming to the beach for tourism and vacation in the summer, Minh Chau will attract research groups to come for tourism combined with research at other times of the year.

d. Sustainability

The sustainability of ecotourism sites in Quan Lan and Minh Chau communes depends on the sensitivity of the ecosystems to climate changes.

landscape. In general, these tourist destinations have a fairly high level of sustainability, because they are natural ecosystems, planned and protected. However, if a large number of tourists gather at certain times, it can exceed the carrying capacity and affect the sustainability of the environment (polluted beaches, damaged trees, animals moving away from their habitats, etc.), then the sustainability of the above ecosystems (natural ecosystems, human ecosystems) will also be affected and become less sustainable.

e. Location and accessibility

Both island communes have ports to take tourists to visit from Van Don wharf:

- Quan Lan – Van Don traffic route:

Phuc Thinh – Viet Anh high-speed boat and Quang Minh high-speed boat, depart at 8am and 2pm from Van Don to Quan Lan, and at 7am and 1pm from Quan Lan to Van Don. There are also wooden boats departing at 7am and 1pm.

- Van Don - Minh Chau traffic route:

Chung Huong high-speed train, Minh Chau train, morning 7:30 and afternoon 13:30 from Van Don to Minh Chau, morning 6:30 and afternoon 13:00 from Minh Chau to Van Don.

f. Infrastructure

Despite receiving investment attention, the issue of infrastructure and technical facilities for tourism on Quan Lan Island is still an issue that needs to be resolved because it has a direct impact on the implementation of ecotourism activities. The minimum conditions for serving tourists such as accommodation, electricity, water, communication, especially medical services, and security work need to be given top priority. Ecotourism spots in Minh Chau commune are assessed to have better infrastructure and technical facilities for tourism because there are quite complete and synchronous conditions for serving tourists, meeting many needs of domestic and foreign tourists.

3.2.1.4. Determine assessment levels and assessment scales

Corresponding to the levels of each criterion, the index is the score of those levels in the order of 4, 3, 2, 1 decreasing according to the standard of each level: very attractive (4), attractive (3), average (2), less attractive (1).

3.2.1.5. Determining the coefficients of the criteria

For the assessment of DLST in the two communes of Quan Lan and Minh Chau islands, the students added evaluation coefficients to show the importance of the criteria and indicators as follows:

Coefficient 3 with criteria: Attractiveness, Exploitation time. These are the 2 most important criteria for attracting tourists to tourism in general and eco-tourism in particular, so they have the highest coefficient.

Coefficient 2 with criteria: Capacity, Infrastructure, Location and accessibility . Because the assessment area is an island commune of Van Don district, the above criteria are selected by the author with appropriate coefficients at the average level.

Coefficient 1 with criteria: Sustainability. Quan Lan has natural and human-made ecotourism sites, with high biodiversity and little impact from local human factors. Most of the ecotourism sites are still wild, so they are highly sustainable.

3.2.1.6. Results of DLST assessment on Quan Lan island

a. Assessment of the potential for natural tourism development

For Minh Chau commune:

+ Natural tourism attractiveness is determined to be very attractive (4 points) and the most important coefficient (coefficient 3), so the score of the Attractiveness criterion is 4 x 3 = 12.

+ Capacity is determined as average (2 points) and the coefficient is quite important (coefficient 2), then the score of Capacity criterion is 2 x 2 = 4.

+ Exploitation time is long (4 points), the most important coefficient (coefficient 3) so the score of the Exploitation time criterion is 4 x 3 = 12.

+ Sustainability is determined as sustainable (4 points), the important coefficient is the average coefficient (coefficient 1), so the score of the Sustainability criterion is 4 x 1 = 4 points

+ Location and accessibility are determined to be quite favorable (2 points), the coefficient is quite important (coefficient 2), the criterion score is 2 x 2 = 4 points.

+ Infrastructure is assessed as good (3 points), the coefficient is quite important (coefficient 2), then the score of the Infrastructure criterion is 3 x 2 = 6 points.

The total score for evaluating DLST in Minh Chau commune according to 6 evaluation criteria is determined as: 12 + 4 + 12 + 4 + 4 + 6 = 42 points

Similar assessment for Quan Lan commune, we have the following table:

Table 3.3: Assessment of the potential for natural ecotourism development in Quan Lan and Minh Chau communes

Attractiveness of self-tourismof course

Capacity

Mining time

Sustainability

Location and accessibility

Infrastructure

Result

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

CommuneMinh Chau

12

12

4

8

12

12

4

4

4

8

6

8

42/52

Quan CommuneLan

6

12

6

8

9

12

4

4

4

8

4

8

33/52

b. Assessment of the potential for humanistic tourism development

For Quan Lan commune:

+ The attractiveness of human tourism is determined to be very attractive (4 points) and the most important coefficient (coefficient 3), so the score of the Attractiveness criterion is 4 x 3 = 12.

+ Capacity is determined to be large (3 points) and the coefficient is quite important (coefficient 2), then the score of the Capacity criterion is 3 x 2 = 6.

+ Mining time is average (3 points), the most important coefficient (coefficient 3) so the score of the Mining time criterion is 3 x 3 = 9.

+ Sustainability is determined as sustainable (4 points), the important coefficient is the average coefficient (coefficient 1), so the score of the Sustainability criterion is 4 x 1 = 4 points.

+ Location and accessibility are determined to be quite favorable (2 points), the coefficient is quite important (coefficient 2), the criterion score is 2 x 2 = 4 points.

+ Infrastructure is rated as average (2 points), the coefficient is quite important (coefficient 2), then the score of the Infrastructure criterion is 2 x 2 = 4 points.

The total score for evaluating DLST in Quan Lan commune according to 6 evaluation criteria is determined as: 12 + 6 + 6 + 4 + 4 + 4 = 36 points.

Similar assessment with Minh Chau commune we have the following table:

Table 3.4: Assessment of the potential for developing humanistic eco-tourism in Quan Lan and Minh Chau communes

Attractiveness of human tourismliterature

Capacity

Mining time

Sustainability

Location and accessibility

Infrastructure

Result

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Quan CommuneLan

12

12

6

8

9

12

4

4

4

8

4

8

39/52

Minh CommuneChau

6

12

4

8

12

12

4

4

4

8

6

8

36/52

Basically, both Minh Chau and Quan Lan localities have quite favorable conditions for developing ecotourism. However, Quan Lan commune has more advantages to develop ecotourism in a humanistic direction, because this is an area with many famous historical relics such as Quan Lan Communal House, Quan Lan Pagoda, Temple worshiping the hero Tran Khanh Du, ... along with local festivals held annually such as the wind praying ceremony (March 15), Quan Lan festival (June 10-19); due to its location near the port and long exploitation time, the beaches in Quan Lan commune (especially Quan Lan beach) are no longer hygienic and clean to ensure the needs of tourists coming to relax and swim; this is also an area with many beautiful landscapes such as Got Beo wind pass, Ong Phong head, Voi Voi cave, but the ability to access these places is still very limited (dirt hill road, lots of gravel and rocks), especially during rainy and windy times; In addition, other natural resources such as mangrove forests and sea worms have not been really exploited for tourism purposes and ecotourism development. On the contrary, Minh Chau commune has more advantages in developing ecotourism in the direction of natural tourism, this is an area with diverse ecosystems such as at Rua De Beach, Bai Tu Long National Park Conservation Center...; Minh Chau beach is highly appreciated for its natural beauty and cleanliness, ranked in the top ten most beautiful beaches in Vietnam; Minh Chau commune is also home to Tram forest with a large area and a purity of up to 90%, suitable for building bridges through the forest (a very effective type of natural ecotourism currently applied by many countries) for tourists to sightsee, as well as for the purpose of studying and researching.

Figure 3.1: Thenmala Forest Bridge (India) Source: https://www.thenmalaecotourism.com/(August 21, 2019)

3.2.2. Using SWOT matrix to evaluate Quan Lan island tourism

General assessment of current tourism activities of Quan Lan island is shown through the following SWOT matrix:

Table 3.5: SWOT matrix evaluating tourism activities on Quan Lan island

Internal agent

Strengths- There is a lot of potential for tourism development, especially natural ecotourism and humanistic ecotourism.- The unskilled labor force is relatively abundant.- resource environmentunpolluted, still

Weaknesses- Poorly developed infrastructure, especially traffic routes to tourist destinations on the island.- The team of professional staff is still weak.- Tourism products in general

quite wild, originalintact

general and DLST in particularalone is monotonous.

External agents

Opportunity- Tourism is a key industry in the socio-economic development strategy of the province and Van Don economic zone.- Quan Lan was selected as a pilot area for eco-tourism development within the framework of the green growth project between Quang Ninh province and the Japanese organization JICA.- The flow of tourists and especially ecotourism in the world tends toincreasing

Challenge- Weather and climate change abnormally.- Competition in tourism products is increasingly fierce, especially with other localities in the province such as Ha Long, Mong Cai...- Awareness of tourists, especially domestic tourists, about ecotourism and nature conservation is not high.

Through summary analysis using SWOT matrix we see that:

To exploit strengths and take advantage of opportunities, it is necessary to:

- Diversify products and service types (build more tourism routes aimed at specific needs of tourists: experiential tourism immersed in nature, spiritual cultural tourism...)

- Effective exploitation of resources and differentiated products (natural resources and human resources)

div.maincontent .p { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; } div.maincontent p { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; } div.maincontent .s1 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 13pt; } div.maincontent .s2 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 13pt; } div.maincontent .s3 { color: #0D0D0D; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s4 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s5 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s6 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; vertical-align: -3pt; } div.maincontent .s7 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; vertical-align: -2pt; } div.maincontent .s8 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; vertical-align: -1pt; } div.maincontent .s9 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s10 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s11 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s12 { color: black; font-family:Symbol, serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s13 { color: black; font-family:Wingdings; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s14 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; vertical-align: 5pt; } div.maincontent .s15 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; vertical-align: 5pt; } div.maincontent .s16 { color: black; font-family:Cambria, serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s17 { color: #080808; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s18 { color: #080808; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s19 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 11pt; } div.maincontent .s20 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10pt; } div.maincontent .s21 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 11pt; } div.maincontent .s22 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 11pt; } div.maincontent .s23 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s24 { color: #212121; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; tex -

Evaluation Results of Quality Indicators and Importance of Each Indicator

Evaluation Results of Quality Indicators and Importance of Each Indicator -

Detailed Results of Factors Affecting Commercial Banking Service Quality from 30 Managers

Detailed Results of Factors Affecting Commercial Banking Service Quality from 30 Managers -

Evaluation of personal credit service quality of Dong A Commercial Joint Stock Bank - Hue Branch - 9

Evaluation of personal credit service quality of Dong A Commercial Joint Stock Bank - Hue Branch - 9

Source: Analysis results from SPSS, Appendix 4

The research results show that the satisfaction level of the Science and Technology group is above average, with an average rating of 3.1411 points on the 5-point Likert scale.

The low standard deviation shows that there is a similarity in customer perceptions in different areas of BIDV's operations. The quality criteria groups of reliability (TC), empathy (DC), staff capacity (NL) and transaction time (TG) of BIDV are all rated above average by customers. This is also consistent with the current status of these loans at BIDV, which is still very modest. However, the DC factor is rated at near average (3.0738 points), which shows that BIDV has not created empathy with customers. The NL criterion is also rated by customers at above average (3.1238), which is also an issue that BIDV needs to pay attention to when coming up with solutions.

Regarding the level of influence of factors on customer satisfaction, it shows that the greatest influence belongs to the TC factor, followed by the DC factor. Accordingly, the TC and DC factors have the same impact on the level of customer satisfaction.

b/ Causes from the customer side

(1) Customers are still hesitant to approach the lender to access loans. In addition, satisfying the necessary conditions makes it difficult for many customers.

(2) The financial capacity of customers is often unpredictable and can fluctuate highly because most customers have little asset management skills, income is greatly affected by health, the business situation of the hiring unit, unusual spending and marital status.

(3) Customers tend not to disclose their income and health status, because if their income is too low/health status is not guaranteed, they will not be able to borrow money from the bank. Therefore, if the credit officer is inexperienced, the possibility of moral hazard and adverse selection is very high.

c/ Causes from the business environment

(1) The economic environment has not escaped recession, growth is poor

Vietnam's economy has been affected by the global economic crisis, since 2008 our country has fallen into deflation and economic recession. The real estate market has frozen, prices have increased and real income of the people has decreased. Although the Government, the State Bank and the authorities have taken many positive measures to get the economy out of the crisis and the real estate market back to normal. However, the response of the market and the economy has not really improved. Prices of essential goods such as gasoline, electricity, water, gas have fluctuated continuously, the USD and gold prices have increased and fluctuated abnormally... affecting people's lives and the whole economy. Therefore, real income of the people has decreased. In addition, the cut

lending to the real estate investment sector under the Government's directive has caused many residential real estate projects to fall into an "unfinished" state for many years due to lack of capital. Along with that, individuals/households have cut spending, no longer considering housing investment as a top priority due to "belt tightening". They also see the prospect of "unfinished" real estate projects for a long time, so individuals/households do not have the need to use housing credit from banks. Therefore, although BIDV's CVNO outstanding debt has grown, it is still at a low level.

(2) Socio-cultural environment

Socio-cultural factors are one of the main factors affecting the credit activities of banks, especially CVNO activities. The low scale of CVNO activities, the difficulty in developing new products... are due to many reasons, but one of them is the habits and consumer psychology of Vietnamese people. Vietnamese consumers often do not like to be in debt and bear the heavy psychological burden of debt when investing in buying/building houses. Most people still think that when borrowing money from banks, they become debtors, making them feel uncomfortable and skeptical about the benefits that banks bring to them through their funding.

Vietnamese people tend to accumulate and save to buy and repair their houses rather than buying/repairing their houses first and then saving to pay off debts. When banks develop CVNO, they often encounter the above habits of the people. Therefore, to develop CVNO effectively, the first thing BIDV must do is to influence the psychology and consumption habits of the people, convince them by bringing them many benefits from CVNO activities, and dispel the above conservative and inherent psychology and habits.

In addition, the population distribution in our country is uneven, big cities such as Hanoi, Ho Chi Minh City, Da Nang... have limited land area but concentrate a large number of people. At the same time, the living standards, income and spending ability of people between regions have large differences, creating an increasingly large gap between rich and poor. The population in the middle and high income groups is concentrated in urban areas, accounting for a small proportion (about 25% of the population), the remaining 75% of the population lives in rural areas (where income levels are still low), so the demand for housing is uneven between areas. Therefore, the CVNO customer segment that the bank targets is only within the above 25% of the population, somewhat limiting BIDV's CVNO market share.

(3) Incomplete legal environment

Housing credit for science and technology is still a new activity in Vietnam, so the legal conditions for the existence and development of this business are

are still general and not clearly specific. Currently, banks only rely on Laws, Decisions, and General Guidelines on lending operations and guarantees when granting credit to customers such as the Law on Credit Institutions, Decision 1627/2001/QD - NHNN on lending regulations of credit institutions to customers and documents amending and supplementing Decision 1627... Because there is no specific, unified legal document guiding the implementation of CVNO operations, banks are not confident in investing and developing this activity strongly, but are only operating very cautiously because banks are afraid that mechanisms, policies, and legal regulations may change unexpectedly. Furthermore, Vietnam's legal documents are overlapping, the latter document negates the former, such as before 2008, CVNO activities in particular and lending activities in the residential real estate sector were encouraged by the Government and the State Bank, but by the end of 2009 and early 2010, investment in this sector was suddenly restricted because it was considered a non-production sector, which needed to be cut to fight the crisis. This has caused banks to be confused, disoriented, and limited their initiative in business, which is an important factor determining the success or failure of a business strategy.

(4) Competitive factors

The fierce competition in the market of banks has caused the "cake" of services to finance the housing development needs of the industrial sector to be divided into many parts. On the threshold of integration, the domestic market has heated up a lot. With the loosening of credit mechanisms in recent years, many banks have penetrated into most new business fields with high income rates to attract more and more customers. Most joint stock commercial banks provide CVNO services because they grasp the rapidly increasing needs of customers in this field. Many banks minimize procedures in loan appraisal and have attractive brokerage and customer introduction commission mechanisms, so BIDV branches face many difficulties in competition due to the reward mechanism, uncompetitive customer policies, and complicated administrative procedures.

Chapter 3 Conclusion

In chapter 3, the thesis has introduced an overview of the current situation of the housing credit market in Vietnam, drawing some conclusions about the housing credit activities of commercial banks such as the outstanding balance of CVNO tends to increase, commercial banks play an important role in credit financing for corporate customers and gradually increase their influence on the private customers. However, the quality of CVNO is not high, this activity only focuses on the private customers who have high and stable income. The lending interest rate is relatively high, the loan term is not long, commonly limited to 15 years.

Based on the theoretical basis mentioned in chapter 2, in chapter 3, the thesis collected and analyzed the current situation of BIDV's CVNO in the 5 years from 2010 to 2016 on the following aspects:

(1) Current status of organization and management of CVNO;

(2) Current status of applying CVNO development methods;

(3) Current status of applying CVNO risk control measures.

The thesis has surveyed and collected primary data on the assessment of the impact of factors causing RRCVNO; evaluated the CVNO service quality criteria according to the SERVQUAL model. The synthesis of primary and secondary data analysis results helps the researcher draw assessments of the current situation on two aspects with 2 (two) successes and 3 (three) limitations, with 13 causes in CVNO activities for BIDV's KHCN.

The research results on the current status of CVNO development in Chapter 3 are important practical arguments for proposing solutions to develop CVNO activities for BIDV's science and technology in the coming time.

CHAPTER 4

ORIENTATION AND SOLUTIONS FOR DEVELOPING HOUSING LOANS FOR INDIVIDUAL CUSTOMERS OF THE JOINT STOCK COMMERCIAL BANK FOR INVESTMENT AND

VIETNAM DEVELOPMENT

4.1. Orientation and viewpoints on housing lending development for individual customers of Vietnam Joint Stock Commercial Bank for Investment and Development in the period of 2016 - 2020, vision to 2025

4.1.1. Forecasting housing credit demand in Vietnam

In recent times, commercial banks have actively contributed to financing the housing real estate market and helped this market develop. However, by stopping, reducing and limiting housing real estate loans, refusing new loan contracts... with the aim of curbing the "overheating" development of the market, focusing on debt collection measures has negatively impacted the real estate market, causing the housing real estate market to decline and "freeze". However, the reality shows that, although the current market situation is gloomy, high-end housing real estate projects are still being implemented. Mid-range and low-end housing real estate is still at a high price (although the price has decreased by 50-60% compared to before), making the ability to buy a house of those with real needs very low. This shows that speculation in the housing real estate market is very high, about 80% of housing real estate investors (Ho Chi Minh City) and about 70% of housing real estate investors (Hanoi) are for speculative purposes. While the housing needs of the majority of consumers are still not really satisfied, the demand for real estate credit is still growing. Furthermore, on the part of commercial banks, housing real estate loans are still an important business segment in the structure of commercial bank loans, so in the coming time, commercial banks will continue to pay attention to developing it. However, the demand for housing credit will have some changes as follows:

(1) The demand for housing and residential land of Vietnamese people is still very large, especially in urban areas, suburban areas and industrial zones. However, due to the low income of individuals and households, the budget for investing in residential real estate is small. Currently, the trend of people with real needs is to choose residential real estate such as affordable apartments and townhouses with a cost of less than 2.5 billion VND. This shows that the residential real estate market will develop strongly in the mid-range and low-end segments; the liquidity of goods in this segment will be high.

(2) To satisfy the demand for residential real estate, individuals/households have now changed their perspective of only using their own savings and borrowing from relatives by increasing the use of commercial bank loans. According to VNR's report [33], the rate of choosing