Utilities

Loan currency: VND

Loan term: up to 60 months.

Loan amount: up to 80% of cost.

Interest rates: fixed and floating; overdue interest rate up to 150% of in-term interest rate.

Loan security: with/without collateral or third party guarantee.

Disbursement: one time or multiple times.

Repayment of principal and interest: repayment of principal once or several times, repayment of interest monthly or periodically as agreed.

Loan conditions

Age from 21-55 for Female and 60 for Male by the end of the loan term

Have household registration/temporary residence book (KT3) at the place of borrowing

Have worked at current agency for at least 12 months or more

Have at least 24 months of work experience

Not in the police and military with a rank on his shoulders

Have a labor contract or decision to appoint a position (for management level)

Salary transfer at Bank Loan procedures

Loan application and repayment plan (according to bank form)

Copy of ID card/Passport and household registration book/KT3 at the place of loan registration

Salary account statement of the last 3 months with confirmation from the issuing bank

Copy of Labor Contract (or other documents of equivalent value such as: Decision on establishment, Decision on job transfer, Decision on transfer of civil servant rank...)

Electricity, water and landline bills at current address

Copy of collateral related documents

Disbursement method

Customers are disbursed one or more times for the entire limit for

Consumer loan products in two forms:

- In cash.

- By transferring money to the customer's account opened at NHNT. Payment method:

Principal and interest repayment cycle: equal monthly payments. The periodic debt collection amount is determined as follows:

- For loans with interest calculated on actual outstanding balance: Principal is calculated for the number of months of loan, interest is calculated on the actual outstanding balance and the actual number of days of capital use in the month.

- For loans with interest calculated on the original principal balance:

Customers pay principal and interest in equal amounts every month. Debt repayment amount

Each month is calculated as follows:

+ Periodic debt collection amount =

Original principal balance + Total interest payable

Number of repayment periods

In which: Total interest payable = Principal * Loan interest rate * Number of loan months

Loan interest rate is determined as a monthly percentage

Repayment period: The customer's monthly repayment date coincides with the date the customer receives his/her regular salary through the Bank for Agriculture and Rural Development. Other cases are subject to agreement with the customer.

Early repayment: The Bank for Agriculture and Rural Development allows customers to repay their debts early.

limited but must pay the prescribed fee.

*Loan situation for consumer credit products and services at State Bank

& PTNT Truong An Branch - Hue City

Table 2.4: Consumer credit situation at the Bank for Agriculture and Rural Development

Truong An Branch – Hue City

Unit: Million VND

Target

Year 2010 | Year 2011 | Year 2012 | Compare | ||||

2011/2010 | 2012/2011 | ||||||

+/- | % | +/- | % | ||||

Loan Sales | 34,278 | 44,545 | 58,520 | 10,267 | 29.95 | 13,974 | 31.37 |

Debt collection turnover | 29,517 | 38,581 | 44,227 | 9,064 | 30.71 | 5,645 | 14.63 |

Outstanding debt | 18,249 | 24,213 | 38,506 | 5,963 | 32.68 | 14,292 | 59.02 |

Maybe you are interested!

-

Investment Situation in Non-Credit Services at Saigon Commercial Joint Stock Bank in the Period of 2015-2019

Investment Situation in Non-Credit Services at Saigon Commercial Joint Stock Bank in the Period of 2015-2019 -

Credit risk at Bank for Investment and Development of Vietnam: Current situation and preventive solutions - 11

Credit risk at Bank for Investment and Development of Vietnam: Current situation and preventive solutions - 11 -

Personal Customer Credit Activity Situation at Dong A Joint Stock Commercial Bank, Hue Branch

Personal Customer Credit Activity Situation at Dong A Joint Stock Commercial Bank, Hue Branch -

Analysis of Credit Situation and Credit Risk Management of Vietnam Bank for Agriculture and Rural Development, Vinh Thuan Branch - Kien Giang

Analysis of Credit Situation and Credit Risk Management of Vietnam Bank for Agriculture and Rural Development, Vinh Thuan Branch - Kien Giang -

Credit risk management at the branch of the Bank for Agriculture and Rural Development of Kon Tum province - current situation and solutions - 2

Credit risk management at the branch of the Bank for Agriculture and Rural Development of Kon Tum province - current situation and solutions - 2

(Source: Vietnam Bank for Agriculture and Rural Development, Truong An Branch - Hue City)

Loan turnover

The data in Table 2.4 shows that the consumer credit turnover of the branch has increased over the past 3 years, the growth rate of each year is higher than the previous year, specifically in 2011, the value of consumer loan turnover reached 44,545 million VND, an increase of 29.95% equivalent to 10,267 million VND compared to 2010. In 2012, it increased over the same period last year by 31.37% equivalent to 13,974 million VND. The increase in loan turnover over the past 3 years shows that the branch has done a good job of promoting its consumer credit products and services, at the same time demonstrating the prestige of the branch, more and more customers are coming to the bank to borrow capital. This is a good achievement of the bank. The increase in loan sales during the difficult economic period, affected by the global economic crisis and the negative impact of high inflation, is due to the fact that the staff of the branch always improves their skills and expertise to best serve customers.

Debt collection turnover

For lending operations, debt collection is the most important issue, playing a key role in generating income as well as ensuring cash flow in banking operations.

Along with the increase of DSCV, DSTN also increased continuously, in 2011 it was 38,581 million VND, an increase of 30.71% compared to the previous year (2010). And the debt collection turnover in 2012 was 44,227 million VND, an increase of 5,645 million VND, corresponding to a rate of

14.63% compared to 2011. Thus, the debt collection revenue structure also fluctuates according to the fluctuation of loan revenue. However, because credit services also depend on the loan term, the bank can collect a lot of revenue this year but less in the following year, so the increase in DSTN in 2012 is lower than in 2011. This is a positive signal for the whole branch. The above results are due to the branch always focusing on promoting this work with a team of credit officers with good professional skills as well as proposing effective debt collection control policies such as debt collection of due debts, regularly checking and urging customers to pay on time.

In addition, the customer's debt repayment characteristics also play a significant role in increasing the bank's debt collection revenue. Because the customers using this product and service are mostly employees with stable monthly salaries, the monthly debt repayment and interest are mostly deducted from the salary by the treasurer of the agencies where they work before paying the employees, so debt collection is largely guaranteed and increases with the loan revenue, in addition, paying salary by card helps the bank do this job better.

Outstanding loans

The growth rate of outstanding loans over the years of the branch is relatively even, each year increases more than the previous year, correspondingly in 2011 it increased by 5,963 million VND compared to 2010 and in 2012 this figure was 14,292 million VND. The annual increase in total outstanding loans shows that the bank has many effective loan recovery measures, on the other hand it also shows that the bank always has regular, stable customers and the measures to attract more customers have been effective.

In general, the consumer lending situation at the Bank for Agriculture and Rural Development, Truong An Branch - Hue City in the past three years has been very good. It has increasingly met the increasing demand for loans from customers.

2.2 Customer reviews on the quality of consumer credit services of the Bank for Agriculture and Rural Development, Truong An branch - Hue city

2.2.1 Characteristics of research subjects

2.2.1.1 Characteristics of the research sample

According to the selected sample structure, we conducted direct interviews with customers, the number of ballots issued was 210, the number of ballots received was 190. Through the processing, we eliminated 28 ballots because they were invalid. The final number of ballots for analysis was 162.

The research sample has the following characteristics:

Table 2.5: Characteristics of the study sample

Sample characteristics

Quantity | Percent | ||

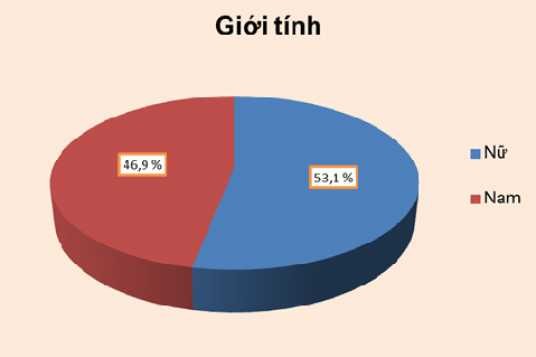

Sex | Female | 86 | 53.1 % |

Male | 76 | 46.9 % | |

Age | Under 25 years old | 11 | 6.8 % |

25 - 40 years old | 71 | 43.8 % | |

41 - 50 years old | 69 | 42.6 % | |

Over 50 years old | 11 | 6.8 % | |

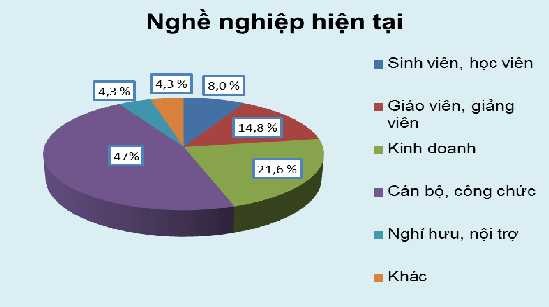

Current occupation | Students | 12 | 8.0 % |

Teacher, lecturer | 24 | 14.8 % | |

Business | 36 | 21.6 % | |

Officials and civil servants | 76 | 46.9 % | |

Retired, housewife | 7 | 4.3 % | |

Other | 7 | 4.3 % | |

Average monthly income | Under 3 million VND / month | 25 | 15.5 % |

From 3 - 6 million VND / month | 118 | 72.8 % | |

Over 6 million VND / month | 19 | 11.7 % |

(Source: Customer survey data)

a. Sample characteristics by gender

Figure 2.1: Sample characteristics by gender

(Source: Customer survey data)

In terms of gender structure, there is a very small difference between male and female customers. The number of male customers using the branch's consumer credit services is 76 customers, accounting for 46.9%, and the number of female customers is 86 customers, accounting for 53.1%. Thus, we can see that when customers using consumer credit services of the Bank for Agriculture and Rural Development, Truong An branch, when classified by gender, there are more women than men, but this difference is not significant. This also shows that women today are more confident in using banking services in general and credit in particular, because in the past, when thinking about borrowing from a bank, it was usually men.

b. Sample characteristics by age

Figure 2.2: Sample characteristics by age

(Source: Customer survey data)

In terms of age, the statistical results show that the most common age group of customers using the Bank's consumer credit services is from 25 to 40 years old, accounting for 43.8%, equivalent to 71 customers, followed by the age group of 41 - 50 years old with 69 customers (equivalent to 42.6%), the two groups of customers under 25 years old and over 50 years old have the same number of customers, 11 people, accounting for 6.8%. Thus, it can be seen that the main customer group is from 25 to 50 years old, who are adults, have the ability to earn money, have a stable income, are mostly married, have large consumption needs for life, accounting for over 86%, so their demand for loans is often high. This group of customers contributes greatly to the revenue of the current branch's consumer credit service business, so it needs to be given due attention so that customers are increasingly satisfied with this service. For the group of customers under 25 years old, most of them are students, so their income is often not high, unstable and partly still depends on the support of their families. Therefore, their current demand for consumer credit services is not very high. However, in the future, they will be the ones with high income.

With stable and high income and higher spending needs, building a position for the bank in the hearts of customers now will bring great benefits to the bank in the future.

c. Sample characteristics by occupation

Figure 2.3: Sample characteristics by occupation

(Source: Customer survey data)

In terms of occupation, the survey results show that there is a large difference between the target groups, the group of civil servants accounts for a large proportion, up to 47% (ie 76 people), the group of business people also accounts for a much larger proportion than other groups, accounting for 21.6% (ie 35 people), the group of teachers and lecturers accounts for 14.8%, or 24 people, followed by students and trainees with 13 people, retired, housewives and other occupations each have 7 people. The reason is that the group of civil servants are the ones with a fairly stable income but the income level is quite normal, so the demand for using consumer credit services to serve work and life is quite high. In addition, this group of customers will be a solid foundation to help develop other services of the bank. Customers in the business group are also potential customers because they have stable income and a relatively high income level, so this is one of the groups that branches need to pay more attention to.