different methods to clarify the relationship between credit risk and the business efficiency of commercial banks, helping commercial banks realize the importance of risk management and bad debt handling to improve operational efficiency. The research results show that risks significantly reduce the business efficiency of commercial banks, the business efficiency of commercial banks in Vietnam is also the cause of changes in credit risk. In the solution section, the author proposes: “With a level of business efficiency set by the bank, the bank can make estimates of future input and output factors. With the change of those factors, the bank determines the acceptable level of credit risk that can be determined to ensure the desired level of business efficiency of the bank. The research results show that when the bank accepts a higher level of credit risk, the bank can fully assess how that change affects its business efficiency. If the decline in the bank's business efficiency is acceptable, it can allow the bank to undertake more risky projects. Thus, when developing a business strategy for a financial company, commercial banks can accept a certain level of credit risk to achieve the proposed business goals. The conclusions in the research can be used as a reference when assessing the current status of risk management at a affiliated financial company, and the evaluation criteria for efficiency and credit risk in the thesis.

- Research work by author Nguyen Ba Dung (2017) on " Application of Big Data in analyzing customer shopping and consumption behavior to promote business activities at Mobifone Telecommunications Corporation ". The work has generalized the theoretical basis of Big Data (concept, characteristics, necessity of application, benefits and overview of technical system of Big Data application) and customer shopping and consumption behavior as well as the trend of applying Big Data in analyzing customer behavior in the world and Vietnam. Based on the actual research on deploying Big Data at Mobifone when building a customer database, technical system, and Big Data application deployment method, the author has evaluated the successes and limitations of Mobifone when applying Big Data to business activities. The solutions are topical and focus on technical systems, database management, and Big Data application models. Although the author has not yet delved into the theoretical basis of Big Data application in the banking industry, specifically at CTTC and the experience of Big Data application in the banking industry worldwide, the research has reference significance in order to build solutions related to Big Data application in terms of data collection and customer information processing, and customer database management in the thesis.

- Author Bui Manh Cuong (2017) when researching " Credit risk management at Home Credit Vietnam Finance Company Limited " clarified the theoretical basis.

Maybe you are interested!

-

Overview of Credit Management of Commercial Banks

Overview of Credit Management of Commercial Banks -

Overview of Credit Activities and Credit Risks at Vietnam Bank for Agriculture and Rural Development

Overview of Credit Activities and Credit Risks at Vietnam Bank for Agriculture and Rural Development -

Solutions for tourism development in Tien Lang - 10

zt2i3t4l5ee

zt2a3gstourism, tourism development

zt2a3ge

zc2o3n4t5e6n7ts

- District People's Committees and authorities of communes with tourist attractions should support, promote, and provide necessary information to people, helping them improve their knowledge about tourism. Raise tourism awareness for local people.

*

* *

Due to limited knowledge and research time, the thesis inevitably has shortcomings. Therefore, I look forward to receiving guidance from teachers, experts as well as your comments to make the thesis more complete.

Chapter III Conclusion

Through the issues presented in Chapter II, we can come to some conclusions:

Based on the strengths of available tourism resources, the types of tourism in Tien Lang that need to be promoted in the coming time are sightseeing and resort tourism, discovery tourism, weekend tourism. To improve the quality and diversify tourism products, Tien Lang district needs to combine with local cultural tourism resources, at the same time combine with surrounding areas, build rich tourism products. The strengths of Tien Lang tourism are eco-tourism and cultural tourism, so developing Tien Lang tourism must always go hand in hand with restoring and preserving types of cultural tourism resources. Some necessary measures to support and improve the efficiency of exploiting tourism resources in Tien Lang are: strengthening the construction of technical facilities and labor force serving tourism, actively promoting and advertising tourism, and expanding forms of capital mobilization for tourism development.

CONCLUDE

I Conclusion

1. Based on the results achieved within the framework of the thesis's needs, some basic conclusions can be drawn as follows:

Tien Lang is a locality with great potential for tourism development. The relatively abundant cultural tourism resources and ecological tourism resources have great appeal to tourists. Based on this potential, Tien Lang can build a unique tourism industry that is competitive enough with other localities within Hai Phong city and neighboring areas.

In recent years, the exploitation of the advantages of resources to develop tourism and build tourist routes in Tien Lang has not been commensurate with the available potential. In terms of quantity, many resource objects have not been brought into the purpose of tourism development. In terms of time, the regular service time has not been extended to attract more visitors. Infrastructure and technical facilities are still weak. The labor force is still thin and weak in terms of expertise. Tourism programs and routes have not been organized properly, the exploitation content is still monotonous, so it has not attracted many visitors. Although resources have not been mobilized much for tourism development, they are facing the risk of destruction and degradation.

2. Based on the results of investigation, analysis, synthesis, evaluation and selective absorption of research results of related topics, the thesis has proposed a number of necessary solutions to improve the efficiency of exploiting tourism resources in Tien Lang such as: promoting the restoration and conservation of tourism resources, focusing on investment and key exploitation of ecotourism resources, strengthening the construction of infrastructure and tourism workforce. Expanding forms of capital mobilization. In addition, the thesis has built a number of tourist routes of Hai Phong in which Tien Lang tourism resources play an important role.

Exploiting Tien Lang tourism resources for tourism development is currently facing many difficulties. The above measures, if applied synchronously, will likely bring new prospects for the local tourism industry, contributing to making Tien Lang tourism an important economic sector in the district's economic structure.

REFERENCES

1. Nhuan Ha, Trinh Minh Hien, Tran Phuong, Hai Phong - Historical and cultural relics, Hai Phong Publishing House, 1993

2. Hai Phong City History Council, Hai Phong Gazetteer, Hai Phong Publishing House, 1990.

3. Hai Phong City History Council, History of Tien Lang District Party Committee, Hai Phong Publishing House, 1990.

4. Hai Phong City History Council, University of Social Sciences and Humanities, VNU, Hai Phong Place Names Encyclopedia, Hai Phong Publishing House. 2001.

5. Law on Cultural Heritage and documents guiding its implementation, National Political Publishing House, Hanoi, 2003.

6. Tran Duc Thanh, Lecture on Tourism Geography, Faculty of Tourism, University of Social Sciences and Humanities, VNU, 2006

7. Hai Phong Center for Social Sciences and Humanities, Some typical cultural heritages of Hai Phong, Hai Phong Publishing House, 2001

8. Nguyen Ngoc Thao (editor-in-chief, Tourism Geography, Hai Phong Publishing House, two volumes (2001-2002)

9. Nguyen Minh Tue and group of authors, Hai Phong Tourism Geography, Ho Chi Minh City Publishing House, 1997.

10. Nguyen Thanh Son, Hai Phong Tourism Territory Organization, Associate Doctoral Thesis in Geological Geography, Hanoi, 1996.

11. Decision No. 2033/QD – UB on detailed planning of Tien Lang town, Hai Phong city until 2020.

12. Department of Culture, Information, Hai Phong Museum, Hai Phong relics

- National ranked scenic spot, Hai Phong Publishing House, 2005. 13. Tien Lang District People's Committee, Economic Development Planning -

Culture - Society of Tien Lang district to 2010.

14.Website www.HaiPhong.gov.vn

APPENDIX 1

List of national ranked monuments

STT

Name of the monument

Number, year of decisiondetermine

Location

1

Gam Temple

938 VH/QĐ04/08/1992

Cam Khe Village- Toan Thang commune

2

Doc Hau Temple

9381 VH/QĐ04/08/1992

Doc Hau Village –Toan Thang commune

3

Cuu Doi Communal House

3207 VH/QĐDecember 30, 1991

Zone II of townTien Lang

4

Ha Dai Temple

938 VH/QĐ04/08/1992

Ha Dai Village –Tien Thanh commune

APPENDIX II

STT

Name of the monument

Number, year of decision

Location

1

Phu Ke Pagoda Temple

178/QD-UBJanuary 28, 2005

Zone 1 - townTien Lang

2

Trung Lang Temple

178/QD-UBJanuary 28, 2005

Zone 4 – townTien Lang

3

Bao Khanh Pagoda

1900/QD-UBAugust 24, 2006

Nam Tu Village -Kien Thiet commune

4

Bach Da Pagoda

1792/QD-UB11/11/2002

Hung Thang Commune

5

Ngoc Dong Temple

177/QD-UBNovember 27, 2005

Tien Thanh Commune

6

Tomb of Minister TSNhu Van Lan

2848/QD-UBSeptember 19, 2003

Nam Tu Village -Kien Thiet commune

7

Canh Son Stone Temple

2160/QD-UBSeptember 19, 2003

Van Doi Commune –Doan Lap

8

Meiji Temple

2259/QD-UBSeptember 19, 2002

Toan Thang Commune

9

Tien Doi Noi Temple

477/QD-UBSeptember 19, 2005

Doan Lap Commune

10

Tu Doi Temple

177/QD-UBJanuary 28, 2005

Doan Lap Commune

11

Duyen Lao Temple

177/QD-UBJanuary 28, 2005

Tien Minh Commune

12

Dinh Xuan Uc Pagoda

177/QD-UBJanuary 28, 2005

Bac Hung Commune

13

Chu Khe Pagoda

177/QD-UBJanuary 28, 2005

Hung Thang Commune

14

Dong Dinh

2848/QD-UBNovember 21, 2002

Vinh Quang Commune

15

President's Memorial HouseTon Duc Thang

177/QD-UBJanuary 28, 2005

NT Quy Cao

Ha Dai Temple

Ben Vua Temple

Tien Lang hot spring

div.maincontent .p { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; } div.maincontent p { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; } div.maincontent .s1 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; font-size: 16pt; } div.maincontent .s2 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s3 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s4 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; font-size: 14pt; } div.maincontent .s5 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; font-size: 14pt; } div.maincontent .s6 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s7 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s8 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; vertical-align: 6pt; } div.maincontent .s9 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 12pt; } div.maincontent .s11 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; tex

Solutions for tourism development in Tien Lang - 10

zt2i3t4l5ee

zt2a3gstourism, tourism development

zt2a3ge

zc2o3n4t5e6n7ts

- District People's Committees and authorities of communes with tourist attractions should support, promote, and provide necessary information to people, helping them improve their knowledge about tourism. Raise tourism awareness for local people.

*

* *

Due to limited knowledge and research time, the thesis inevitably has shortcomings. Therefore, I look forward to receiving guidance from teachers, experts as well as your comments to make the thesis more complete.

Chapter III Conclusion

Through the issues presented in Chapter II, we can come to some conclusions:

Based on the strengths of available tourism resources, the types of tourism in Tien Lang that need to be promoted in the coming time are sightseeing and resort tourism, discovery tourism, weekend tourism. To improve the quality and diversify tourism products, Tien Lang district needs to combine with local cultural tourism resources, at the same time combine with surrounding areas, build rich tourism products. The strengths of Tien Lang tourism are eco-tourism and cultural tourism, so developing Tien Lang tourism must always go hand in hand with restoring and preserving types of cultural tourism resources. Some necessary measures to support and improve the efficiency of exploiting tourism resources in Tien Lang are: strengthening the construction of technical facilities and labor force serving tourism, actively promoting and advertising tourism, and expanding forms of capital mobilization for tourism development.

CONCLUDE

I Conclusion

1. Based on the results achieved within the framework of the thesis's needs, some basic conclusions can be drawn as follows:

Tien Lang is a locality with great potential for tourism development. The relatively abundant cultural tourism resources and ecological tourism resources have great appeal to tourists. Based on this potential, Tien Lang can build a unique tourism industry that is competitive enough with other localities within Hai Phong city and neighboring areas.

In recent years, the exploitation of the advantages of resources to develop tourism and build tourist routes in Tien Lang has not been commensurate with the available potential. In terms of quantity, many resource objects have not been brought into the purpose of tourism development. In terms of time, the regular service time has not been extended to attract more visitors. Infrastructure and technical facilities are still weak. The labor force is still thin and weak in terms of expertise. Tourism programs and routes have not been organized properly, the exploitation content is still monotonous, so it has not attracted many visitors. Although resources have not been mobilized much for tourism development, they are facing the risk of destruction and degradation.

2. Based on the results of investigation, analysis, synthesis, evaluation and selective absorption of research results of related topics, the thesis has proposed a number of necessary solutions to improve the efficiency of exploiting tourism resources in Tien Lang such as: promoting the restoration and conservation of tourism resources, focusing on investment and key exploitation of ecotourism resources, strengthening the construction of infrastructure and tourism workforce. Expanding forms of capital mobilization. In addition, the thesis has built a number of tourist routes of Hai Phong in which Tien Lang tourism resources play an important role.

Exploiting Tien Lang tourism resources for tourism development is currently facing many difficulties. The above measures, if applied synchronously, will likely bring new prospects for the local tourism industry, contributing to making Tien Lang tourism an important economic sector in the district's economic structure.

REFERENCES

1. Nhuan Ha, Trinh Minh Hien, Tran Phuong, Hai Phong - Historical and cultural relics, Hai Phong Publishing House, 1993

2. Hai Phong City History Council, Hai Phong Gazetteer, Hai Phong Publishing House, 1990.

3. Hai Phong City History Council, History of Tien Lang District Party Committee, Hai Phong Publishing House, 1990.

4. Hai Phong City History Council, University of Social Sciences and Humanities, VNU, Hai Phong Place Names Encyclopedia, Hai Phong Publishing House. 2001.

5. Law on Cultural Heritage and documents guiding its implementation, National Political Publishing House, Hanoi, 2003.

6. Tran Duc Thanh, Lecture on Tourism Geography, Faculty of Tourism, University of Social Sciences and Humanities, VNU, 2006

7. Hai Phong Center for Social Sciences and Humanities, Some typical cultural heritages of Hai Phong, Hai Phong Publishing House, 2001

8. Nguyen Ngoc Thao (editor-in-chief, Tourism Geography, Hai Phong Publishing House, two volumes (2001-2002)

9. Nguyen Minh Tue and group of authors, Hai Phong Tourism Geography, Ho Chi Minh City Publishing House, 1997.

10. Nguyen Thanh Son, Hai Phong Tourism Territory Organization, Associate Doctoral Thesis in Geological Geography, Hanoi, 1996.

11. Decision No. 2033/QD – UB on detailed planning of Tien Lang town, Hai Phong city until 2020.

12. Department of Culture, Information, Hai Phong Museum, Hai Phong relics

- National ranked scenic spot, Hai Phong Publishing House, 2005. 13. Tien Lang District People's Committee, Economic Development Planning -

Culture - Society of Tien Lang district to 2010.

14.Website www.HaiPhong.gov.vn

APPENDIX 1

List of national ranked monuments

STT

Name of the monument

Number, year of decisiondetermine

Location

1

Gam Temple

938 VH/QĐ04/08/1992

Cam Khe Village- Toan Thang commune

2

Doc Hau Temple

9381 VH/QĐ04/08/1992

Doc Hau Village –Toan Thang commune

3

Cuu Doi Communal House

3207 VH/QĐDecember 30, 1991

Zone II of townTien Lang

4

Ha Dai Temple

938 VH/QĐ04/08/1992

Ha Dai Village –Tien Thanh commune

APPENDIX II

STT

Name of the monument

Number, year of decision

Location

1

Phu Ke Pagoda Temple

178/QD-UBJanuary 28, 2005

Zone 1 - townTien Lang

2

Trung Lang Temple

178/QD-UBJanuary 28, 2005

Zone 4 – townTien Lang

3

Bao Khanh Pagoda

1900/QD-UBAugust 24, 2006

Nam Tu Village -Kien Thiet commune

4

Bach Da Pagoda

1792/QD-UB11/11/2002

Hung Thang Commune

5

Ngoc Dong Temple

177/QD-UBNovember 27, 2005

Tien Thanh Commune

6

Tomb of Minister TSNhu Van Lan

2848/QD-UBSeptember 19, 2003

Nam Tu Village -Kien Thiet commune

7

Canh Son Stone Temple

2160/QD-UBSeptember 19, 2003

Van Doi Commune –Doan Lap

8

Meiji Temple

2259/QD-UBSeptember 19, 2002

Toan Thang Commune

9

Tien Doi Noi Temple

477/QD-UBSeptember 19, 2005

Doan Lap Commune

10

Tu Doi Temple

177/QD-UBJanuary 28, 2005

Doan Lap Commune

11

Duyen Lao Temple

177/QD-UBJanuary 28, 2005

Tien Minh Commune

12

Dinh Xuan Uc Pagoda

177/QD-UBJanuary 28, 2005

Bac Hung Commune

13

Chu Khe Pagoda

177/QD-UBJanuary 28, 2005

Hung Thang Commune

14

Dong Dinh

2848/QD-UBNovember 21, 2002

Vinh Quang Commune

15

President's Memorial HouseTon Duc Thang

177/QD-UBJanuary 28, 2005

NT Quy Cao

Ha Dai Temple

Ben Vua Temple

Tien Lang hot spring

div.maincontent .p { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; } div.maincontent p { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; } div.maincontent .s1 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; font-size: 16pt; } div.maincontent .s2 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s3 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s4 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; font-size: 14pt; } div.maincontent .s5 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; font-size: 14pt; } div.maincontent .s6 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s7 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s8 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; vertical-align: 6pt; } div.maincontent .s9 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 12pt; } div.maincontent .s11 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; tex -

Overview of the Economic, Social and Educational Situation of Dak Glong District, Dak Nong Province

Overview of the Economic, Social and Educational Situation of Dak Glong District, Dak Nong Province -

Overview of Materials Used in the Project

Overview of Materials Used in the Project

on credit risk and credit risk management from the perspective of financial institutions including: concepts, characteristics, risk classification, assessment index, content and meaning of risk management, influencing factors and international practices on risk management. Based on the assessment of the current status of risk management at Home Credit through the assessment of credit structure, bad debt situation, causes of risk, content of risk management and risk management policy in the period 2014-2016, summarize the successes and limitations of risk management at Home Credit. These limitations mainly stem from unstable human resources, difficulties in verifying customer information, weak information technology systems, and lack of determination in debt handling. Solutions to focus on handling Home Credit's limitations include: perfecting the risk management apparatus, improving the quality of human resources, perfecting the risk management framework, developing credit risk management policies, and perfecting the IT system. However, the project has not yet delved into the theoretical framework of the credit risk management model and risk management strategy currently being applied by financial companies, the credit risk management model and strategy suitable for types of financial companies, combined with an analysis of the current situation of Home Credit to find a suitable model and help the proposed solutions to be feasible. However, the project has general reference significance when conducting thesis research.

- Office of the Comptroller of the Currency (2018), “ Comptroller's Handbook, Installment Lending Version 1.3 - Installment Lending Handbook, Version 1.3 ”. The study revolves around the contents related to installment credit, risks arising in the installment credit method and risk management methods according to international practices. Installment credit is implemented on a cyclical basis, depending on technology, automation and continuous innovation. Types of risks include credit risk, interest rate risk, liquidity risk, price risk, compliance risk, strategic risk and reputation risk. Credit risk is the most significant risk and is inherent in all stages of the credit granting and implementation process. The study also mentions risk management methods such as automatic risk management systems, management models, credit scoring... The study has reference significance for considering the risk aspect when implementing TDTD in the thesis.

- Doctoral thesis of author Nguyen Thi Minh (2019) " Developing consumer credit products at the Bank for Agriculture and Rural Development of Vietnam ". The thesis has established a fairly complete theoretical system on developing consumer credit products at commercial banks, in which the author puts forward a scientific argument on developing consumer credit products as "increasing in scale, improving product quality associated with enhancing community responsibility to develop sustainable consumer credit products"; the system of indicators to evaluate the effectiveness of consumer credit product development includes consumer credit market share indicators, income indicators from

TDTD products, TDTD cost indicators, TDTD bad debt risk indicators, community benefit indicators and social responsibility of TDTD products; factors affecting the development of TDTD products include subjective factors (development orientation of the bank, TDTD policy of the bank, capital scale and potential of the bank, credit information system and distribution network, capital mobilization situation...) and objective factors (economic environment, political, social and cultural environment, legal environment, competitors, customer factors). The experience of some commercial banks in the world in developing TDTD products is also analyzed and summarized in detail, drawing lessons for Vietnam. However, the research is applied to TDTD activities of commercial banks, TDTD products are researched and proposed for individual customers who meet the lending conditions of commercial banks, customers who have difficulty accessing TDTD products of commercial banks are not the subjects of the research. The work has reference value when conducting general theoretical research on TDTD, TDTD development methods in TDTD product content, system of indicators and factors affecting TDTD development in the thesis.

- Doctoral thesis by author Phan Thi Hong Thao (2019) " Financial efficiency of official microfinance institutions in Vietnam" . The thesis summarizes the theory of financial efficiency, and at the same time builds a set of criteria to measure financial efficiency, a model of factors affecting the financial efficiency of microfinance institutions. The study has reference significance when building a set of evaluation criteria and factors affecting the development of TDTD in the thesis.

- Doctoral thesis by author Nguyen Thu Ha (2019), " Improving business performance efficiency at the Military Commercial Joint Stock Bank ". The thesis provides a theoretical overview of business performance at commercial banks: concepts and contents of business performance efficiency from the perspective of commercial banks on profitability, safety and from the social perspective on contribution to socio-economic development goals. The author of the thesis proposes a system of indicators to evaluate the business performance of commercial banks from the perspective of ensuring safety and implementing an analysis of the impact of the fourth scientific revolution (revolution 4.0) on the business performance of commercial banks quite clearly. The results of this research have practical significance in evaluating the efficiency of credit activities in the period of the 4.0 technology revolution in the thesis.

- Doctoral thesis by author Tran Khanh Duong (2019) " Prevention and limitation of credit risks at Vietnam Joint Stock Commercial Bank for Investment and Development ". The thesis has built a systematic and updated theoretical framework on credit risks in the context that commercial banks in Vietnam have been perfecting the risk management framework.

credit risk according to Basel II Agreement. The theoretical framework focuses on the following contents: commercial bank operations (concepts, credit classification, operational characteristics, roles); theory of credit risk and credit risk prevention; credit risk measurement criteria including direct measurement indicators (overdue debt ratio, bad debt and bad debt ratio to total outstanding debt, credit risk provisioning ratio...) and indirect measurement indicators through credit scale (debt outstanding ratio to total assets, credit structure, profit criteria). The content of risk prevention and risk limitation of commercial banks is demonstrated through risk management strategies, related credit regulations/processes, centralized credit information system, centralized risk management model and risk management measurement. From the experience of risk management of commercial banks in the world and in Vietnam, the author believes that "commercial banks in Vietnam need to be flexible in choosing a risk prevention and mitigation management model that is suitable to their conditions and internal strength, moving towards a model that meets international standards". Based on the assessment of the current status of the risk prevention and mitigation system at BIDV in the period of 2014-2018, the author has pointed out the limitations and causes of the limitations, which are the basis for proposing solutions to improve risk management at BIDV by 2030. The solutions focus on the content of building and perfecting the risk management strategy, perfecting the risk management model, improving the quality of information collection and processing, applying information technology in preventing and minimizing credit risks... The research results have practical significance for building a theoretical framework to assess the current status of implementation of the organization and management work to ensure the effectiveness of credit in the thesis.

- Doctoral thesis by author Le Thi Hanh (2019) on " Credit risk management at Vietnam Joint Stock Commercial Bank for Foreign Trade according to Basel II standards ". In this thesis, the author has systematized the theoretical basis of risk, credit risk and credit risk management of commercial banks according to Basel II standards, especially the need to meet Basel II standards of commercial banks. The author has identified limitations in implementing credit risk management according to Basel II standards at Vietcombank such as the content of implementing Basal II standards in banking activities is quite complicated, Vietcombank has not met some standard conditions on human resources, database system, professional credit rating organization and monitoring capacity. The limitations and causes of limitations provide suggestions for Vietcombank to plan risk management strategies and policies according to Basel II standards. Although the research is from the perspective of risk management of commercial banks, it has reference significance in the scope and content of the work of organizing and managing the quality assurance of credit in the thesis.

- Google, Temasek and Bain & Company (2019), the topic " Fulfilling its Promise - The future of Southeast Asia's digital financial services " research on subprime customers showed that more than 70% of the population in Southeast Asia is classified as "underbanked" or "unbanked" and has difficulty accessing financial services. However, this group of customers is the driving force for growth thanks to technology-based business models. The research points out the potential of digital lending activities with an expected compound growth rate of 29% from now to 2025. Besides the potential of subprime customers, the research also points out the challenges that digital financial services will face such as low financial literacy and building credit ratings for disadvantaged customers. However, data for scoring loan customers can come from cooperation between telecommunications companies and Fintech companies. Telecommunications companies own the customer data system using telecommunications services, this data is the input for Fintech companies to deploy customer scoring. The research has reference value on opportunities and challenges when deploying digital products, optimal connection between product and service providers and Fintech companies.

- In the topic " New credit-risk models for the unbanked" by Tobias Baer et al. (2019), the authors studied risk models for customers who do not have access to banking services, including households and small businesses. Two popular business models for this customer group include the traditional consumer finance model (with high interest rates and high penalties) and the microfinance model. The study shows that neither of these models is a sustainable business model when meeting the diverse needs of low-income customers. However, lenders can achieve sustainable development goals by using computing power and increasingly abundant information/data sources (including mobile phone user data, bill payment history, etc.) to build better risk models. Lenders can use Big Data mining and processing techniques to provide huge statistical samples to analyze consumer behavior according to their goals. The research has a reference meaning on the application of Big Data in analyzing customer behavior of the affiliated financial company in the thesis.

1.1.3. Conclusions drawn from the overview of the research situation

From the overview of the research situation, it can be seen that due to differences in topics, contexts, time, and research space, published research works still have the following limitations and gaps:

- There has been no research to build a theoretical framework on financial companies affiliated with commercial banks, on credit and credit development of affiliated financial companies for sub-prime customers, characteristics of credit according to the model of financial companies affiliated with commercial banks, advantages and disadvantages of this model, factors affecting the development of credit of affiliated financial companies for sub-prime customers. Necessary conditions for affiliated financial companies to successfully implement digital business model transformation in the era of industry 4.0.

- The peer-to-peer lending model of affiliated financial companies and the conditions for affiliated financial companies to successfully implement the peer-to-peer lending model and achieve the goal of developing safe and sustainable credit institutions have not been clarified by any research.

- There has been no in-depth research on the development of credit institutions under commercial banks. Thesis-level research on the development of credit institutions' credit services and other credit institutions in Vietnam for the scientific and technological subjects is still relatively few. Some studies on the development of credit institutions' credit institutions in Vietnam were conducted quite a long time ago, so the conclusions may no longer be suitable for current practical conditions.

- Conditions and solutions for financial companies under commercial banks in Vietnam to self-deploy to become Fintech like the case of Alibaba ecosystem in China (Alipay is now Ant Finance, Taobao).

Based on the limitations and research gaps, in his thesis, the author focuses on the following issues:

- Develop a theoretical framework on credit risk and credit risk development of financial companies for sub-prime customers, characteristics of credit risk development of financial companies under commercial banks, criteria for evaluating credit risk development and factors affecting credit risk development of financial companies under commercial banks for sub-prime customers.

- Learn lessons on developing credit institutions for financial companies under commercial banks in Vietnam from financial companies around the world, and lessons on state management on developing credit institutions for Vietnam from the experiences of EU countries and Japan.

- Analyze the current status of credit development of financial companies under commercial banks in Vietnam in the period of 2014-2019, draw conclusions about successes and limitations, causes of successes and limitations in credit development of financial companies under commercial banks in Vietnam.

- Analyze the opportunities and challenges that affiliated financial companies face, forecast trends and development orientations of credit institutions under commercial banks in Vietnam in the era of industry 4.0. Propose solutions and recommendations to develop safe and sustainable credit institutions on a digital platform in the era of industry 4.0.

1.2. Thesis research method

1.2.1. Research process

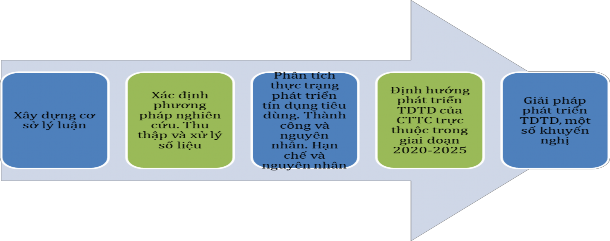

To study the development of TDTD of financial companies under commercial banks in Vietnam, the research process is shown in Figure 1.1:

Figure 1.1: Research process

Source: Author's own construction

1.2.2. Data collection method

To serve the research information collection, the author uses the following data collection methods:

- Desk research: In order to assess the current status of consumer finance development of financial companies under commercial banks, the author collected and synthesized data in the period of 2014-2018 from the Vietnam Consumer Finance Report 2018 of Stoxplus Joint Stock Company, the Full-year 2018 Consumer Finance Report of FiinGroup, 2019 data compiled by the author, forecasts from the database of the period 2014-2018, consumer finance growth forecasts and data achieved up to June 30 or September 30 published in magazines, websites... The author also referred to a number of legal documents, consumer finance development orientations of legal agencies related to consumer finance activities. In addition, the author also used information collected from the internet, newspapers, publications of FE Credit, Mcredit, HD Saison, SHB Finance to serve the desk research work.

- Expert method: To assess the level of development of consumer credit and some factors affecting the development of consumer credit of financial companies under commercial banks, the author conducted in-depth interviews with professional staff of financial companies under commercial banks, focusing on the following 6 groups of issues: consumer credit products, distribution and marketing channels, and models.

credit risk management, business strategy, human resources, and information technology. Corresponding to the 6 groups of issues above, the author conducted interviews with 6 groups of 8 people each (at least at 3 financial companies under the commercial bank). To design a set of questions for the group of professional staff, the author consulted with the leaders of the professional departments at the affiliated financial companies on the content to be interviewed, conducted a trial interview and completed the official set of interview questions. The set of interview questions includes all the questions for the professional departments in the affiliated financial companies, but when conducting the official interview, the author used the set of questions corresponding to the expertise of the interview group instead of interviewing all the questions. For example: The set of questions on TDTD products only applies to the group of professional staff on products or the leadership of the Business Division of the financial company and does not interview other questions. The interview method includes 2 methods: i) Telephone interview: the author calls the professional staff, introduces the purpose of the call, the desired time of the interview and asks the order of each question for each professional group;

ii) Direct interview: the author conducts the interview at the professional staff's office or at a location agreed by the professional staff. The total expected interview time is maximum: 30 minutes and will be conducted from February 2020 to March 2020. Sample interview questions see Appendix 03: Interview questions for professional staff of the affiliated CTTC. At the request of the information provider, the author cannot provide the identity of the provider in the thesis. The author will prepare a separate report to submit to the training institution for inspection (if any).

- Sociological survey method: To assess the impact of some factors (service quality, customer knowledge...) on the development of consumer credit of financial companies under commercial banks, the author conducted a survey to collect opinions of customers using consumer credit products of 4 financial companies under commercial banks in large areas such as Ho Chi Minh City and Hanoi. According to the study of Hair, Anderrson, Tatham and Black (1998), the minimum sample size needs to be 5 times the total number of observed variables. Formula to determine the expected number of samples: N=5*m, in which m is the number of questions in the survey. In the customer opinion survey of the affiliated financial company, the total number of questions is 20, so the number of samples that need to be surveyed according to the standard to be achieved is 5*20 = 100 samples. Research on sample size conducted by Roger (2006) shows that the minimum number of samples in practical research projects must be from 150-200 samples. To ensure the survey is objective and covers the customers of affiliated financial companies, the author deployed a sample size 3 times the standard sample size according to the formula.