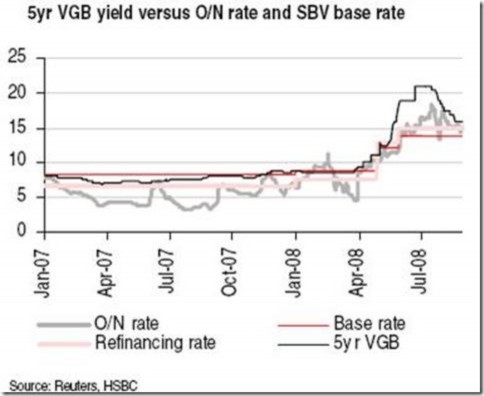

Chart 3: Vietnam bond interest rates

2.2.2. Bond trading situation

Maybe you are interested!

-

Current status of investment activities in bond trading of Vietnam Commercial Bank

Current status of investment activities in bond trading of Vietnam Commercial Bank -

Research Projects on Cultural Heritage Values and Tourism Development in Hanoi Capital

Research Projects on Cultural Heritage Values and Tourism Development in Hanoi Capital -

Concept and Characteristics of Trading Listed Stocks on the Centralized Stock Market

Concept and Characteristics of Trading Listed Stocks on the Centralized Stock Market -

Listed Volume and Trading Value of Listed Securities in the Whole Market as of the End of 2007

Listed Volume and Trading Value of Listed Securities in the Whole Market as of the End of 2007 -

Learn about the historical and cultural values of Lo Khe Ca Tru village, Lien Ha commune, Dong Anh district, Hanoi - 4

Learn about the historical and cultural values of Lo Khe Ca Tru village, Lien Ha commune, Dong Anh district, Hanoi - 4

Capital mobilization in the form of issuing government bonds is an activity of the primary market. However, the primary market has a close relationship with the secondary market. Capital mobilization for development investment can only be effective if there is a complete and truly liquid secondary market. Before July 2000, there was almost no secondary market in Vietnam. Bond transfer activities were carried out at the State Treasury where the bonds were issued, not in a market nature. Bond custody, payment and transfer activities were not organized. Since July 2000, the secondary market for government bonds under a centralized model has been put into operation with the establishment of the Ho Chi Minh City Securities Trading Center. Although there are still many limitations, the opening of the secondary market has created conditions for government bonds to be able to buy and sell and price according to market mechanisms, contributing to promoting support for the primary market. During the period 2000-2002, bond trading activities in general

In general, and TPCP in particular, trading was very sparse. During this period, the number of bonds listed on the Ho Chi Minh City Stock Exchange was very small, mainly TPCP, with about 40 types. Bondholders tended to hold bonds until maturity rather than trading on the market. Therefore, during this period, the volume and value of TPCP traded on the market were insignificant, the ratio of TPCP trading value to listed TPCP value was low. Since 2001, the Stock Exchange has opened a mechanism for negotiated trading for large lots, but due to price range control and lack of professional bond traders, trading results have been limited. From 2003 to present, the value of TPCP trading has increased sharply. Due to the significant increase in the number of listed TPCP. On the other hand, due to the application of regulations such as not limiting the holding ratio of bonds of organizations and individuals to promote bond trading. On the other hand, securities companies have implemented repurchase (repo) operations for bonds, which has greatly increased the volume of bond transactions. Since 2003, the Stock Exchange has eliminated price bands for bond transactions [15; pages 90-92]. In 2008, the transaction volume had the highest increase in the region, increasing by 98.11%, compared to the average of 21.1% for East Asian countries ( Source: ADB - Asian bond monitor November 2008).

Before 2002, the main participants in government bond transactions were commercial banks and securities companies [15; page 93]. Up to now, investment funds, insurance companies, financial companies and other entities have participated in government bond transactions more actively; especially with the participation of foreign bond investment organizations. Since 2005, the Vietnamese bond market has attracted the attention of international bond investment funds (Source: Hanoi Stock Exchange).

Chart 4: Comparison of listed and traded bond values at Hanoi Stock Exchange

Volume (Billion VND)

160000

140000

120000

Listed value

Transaction value

100000

80000

60000

40000

20000

0

2005 2006 2007 2008 Year

Source: Hanoi Stock Exchange

Corporate bond trading is also very weak. Most bond investors consider it as a savings and often hold it until maturity. Therefore, the scarce goods on the secondary market become even scarcer. The secondary bond market is underdeveloped, so corporate bonds are less liquid and less attractive to investors, creating a sense of apprehension for businesses when considering debt financing.

2.3. Assessment of the performance of Vietnam's bond market

2.3.1. General assessment

Although the Vietnamese bond market has only recently been established and developed, it has initially achieved important results, contributing to the formation of an important and effective capital mobilization channel for investment activities in the socio-economic development of our country. According to the assessment of the Ministry of Finance, the bond market has had remarkable developments in recent times, specifically in terms of the system of mechanisms and policies for bond market activities, which have been issued relatively fully, covering most bond issuance and trading activities, creating the necessary foundation to encourage, promote and diversify forms of medium and long-term capital mobilization through bond issuance to serve investment goals; in terms of market organization, it has created the most favorable conditions for market development. The Vietnamese bond market has completed its structure. The issuance market has had innovations in issuance methods, organizations participating in bond issuance, and a secondary market has been formed to help improve liquidity for bonds on the market. The number of types of bonds has continuously increased in variety, especially the development of corporate bonds. Enterprises and investors have begun to pay attention to this market. This is reflected in the number of corporate bonds issued continuously increasing over the years, the number of investors participating in the market has increased more than before. Especially, there is the participation of foreign investors, although the number is still limited. The value of issued bonds and bonds traded has increased rapidly. By the end of March 2009, the Hanoi Stock Exchange had 531 listed bond codes, with a total value of about 165,938.6 billion VND (Source: www.hastc.org.vn/Quymo_niemyet.asp ). In 2008, the TTTP market was assessed to have grown in both institutional framework and issuance and trading results. In 2007, the total market size compared to GDP was 13.72%, of which corporate bonds accounted for about 15% of the total market capacity.

Market transactions achieved the highest growth rate in the region, specifically in 2007, they increased by 98.11% compared to the average of 21.1% in emerging East Asian countries. The trading volume in the first 9 months of 2008 reached 1,370 million bonds, an increase of 21% compared to the whole year of 2007 [16; page 3] . The above results have contributed to making the bond market an important capital mobilization channel in the economy.

In addition to the achievements, the development of the bond market in recent times still has some limitations, causing difficulties in mobilizing long-term capital, especially for enterprises, and has not facilitated the participation of financial institutions. In addition, the overheating of the stock market, specifically the stock market in recent times, has caused enterprises and investors to ignore the very potential bond market. The Vietnamese bond market is currently quite small and individual, mainly government bonds while corporate bonds are very few. The corporate bond market in Vietnam has not developed because the trust of most enterprises towards investors is not high. For small markets, investors often worry about liquidity. While government bonds have a low payment risk, creating trust, investors are quite cautious with corporate bonds. Although it has increased in quantity, the Vietnamese bond market is not rich because the number of issuers is small, the number of bonds issued is still low, so investors have very few choices, not meeting the needs of socio-economic development and the potential of our country. The commodity structure in the market is not reasonable. According to ADB, in 2007, the growth rate of Vietnam's bond market was the highest in the region, but the transaction value (a measure of liquidity) of the Vietnamese bond market was among the lowest among emerging markets in East Asia. Most of it is concentrated in the primary market, in the secondary market the volume of bond transactions is very small. Although the corporate bond market has made some progress, especially the

Although there were many corporate bond issuances in the primary market in 2007, the corporate bond market in the secondary market has hardly developed. In general, the corporate bond market is still considered to be almost underdeveloped. Investors mainly buy and hold bonds until maturity. Related services to support the market are almost non-existent. From the perspective of enterprises, capital mobilized from bonds is still considered a Tier 2 capital source. The biggest concern now is how to encourage enterprises to use this market effectively in their capital mobilization plans.

2.3.2. Results achieved

2.3.2.1. About the issuer

Government Bonds

In general, the government bond market has gone through many ups and downs. Issuing government bonds has become an effective capital mobilization channel. The value of mobilized government bonds has increased over the years, the quantity and terms of government bonds have been more diversified; especially in 2007, the Government organized the issuance of bonds in large lots to increase liquidity, making the situation of government bond transactions increase significantly. Through the practice of issuing large lots of government bonds, the number of types of government bonds circulating on the market will be reduced, helping investors as well as intermediary organizations to easily monitor and grasp the price movements of government bonds. This is the basis for setting buying and selling prices. On the other hand, the large issuance volume has created conditions for many investors to own the same type of bond, increasing the liquidity of the bond, thereby attracting the attention of investors and the Government can mobilize a large amount of capital for the State budget. The method of bidding for bonds through the stock market has been applied according to international practices and has also achieved encouraging results. The market participants are also increasingly diverse. In addition, the application of the negotiated transaction method has made investors completely proactive in transactions, which has

positively impact on bond trading activities. In the current government bond market, the most welcomed and attractive to investors are bonds issued in foreign currencies on the international market. Along with the establishment of two securities trading centers in Ho Chi Minh City and Hanoi, especially the specialized bond market officially put into operation since June 2008, it has created conditions for government bonds to be traded on the market in a concentrated manner.

Corporate bonds

The corporate bond market has developed, enterprises have paid more attention to issuing bonds, contributing to reducing the pressure of borrowing from commercial banks and creating a bond supply source for the market. After Decree 52/ND-CP, allowing enterprises to issue bonds in a private form, it has contributed to creating more capital mobilization channels for enterprises. Bond issuance turnover has grown strongly. According to the data given above, we can see that the value of corporate bonds issued increased from 5 million USD issued by Refrigeration Electrical Engineering Corporation (REE) in 1996 to about 1.56 billion USD in 2008.

2.3.2.2. About the issuance method

Bond issuance can now be done in many ways. Not only retail through the State Treasury system as in the first phase, but now it can also be issued through bidding, underwriting, and issuing agents.

* The Ho Chi Minh City Stock Exchange, which came into operation in July 2000, created an organized secondary market for bond trading, helping to improve bond liquidity and promote investment and trading activities in the market. In March 2005, the Hanoi Stock Exchange officially came into operation. This is an important event that not only creates conditions for organizations and small and medium enterprises to participate in bond issuance and bond listing on the centralized market, but also facilitates investors in trading in the market.

* Goods on the market are quite diverse and always being improved. The form of bonds has changed a lot. Many types of bonds have been issued on the market such as: registered bonds, anonymous bonds, bonds mobilized in VND, bonds mobilized in USD... Previously, bonds were paid where they were purchased, now investors can pay in many places. Bond terms have also changed a lot. From only issuing short-term treasury bills (3, 6, 9 months), bonds now have longer terms, making the types of bond terms more diverse, including: short-term (under 1 year), medium-term (1, 2, 3 years), long-term (over 5 years).

Currently, there are corporate bonds on the market. Bonds are increasingly standardized, meeting the conditions to be listed on the centralized securities trading market. Through bond issuance, issuers have provided a large amount of important goods to the capital market, especially in the conditions where the Vietnamese securities market has just started operating, and the amount of goods on the market is still small.

* The number of members participating in the market is increasing.

Thanks to the results in terms of market organization, capital goods on the market, and increased convenience in the market, the number of investors participating in the market has changed significantly. The number of investors participating in the market has increased significantly compared to before. In particular, there has been the participation of foreign investors, although the number is still limited. Currently, the market has formed organized investors, with professional nature such as investment funds, securities companies performing self-trading tasks...

In addition to the Government participating in issuing government bonds to offset budget deficits and meet capital needs for investment in developing public works and social welfare, localities across the country and enterprises have now participated in issuing bonds to raise capital for their operations.