about 60 - 70%, the remaining 30 - 40% will be used to invest in highly liquid instruments, while Vietnamese banks invest entirely in credit. The liquidity of commercial banks is increasingly decreasing, showing that the ratio of total credit/total mobilized capital (as in 2010) is continuously increasing, but the source of mobilized capital is showing signs of decreasing. In addition, this ratio in most Asian countries is lower than 80%, while in Vietnam it was at times up to more than 130%, so the State Bank issued Circular 13/2010/TT-NHNN effective in October 2010, stipulating this ratio at a maximum of 80% for banks and 85% for other credit institutions, but so far this ratio has not decreased and the problem has not been completely resolved. At the same time, the ratio of lending credit/mobilized capital tends to increase, in 2008 it was 0.95%, in 2009 it was 1.01%, in 2010 it was 1.01% and in 2011 it was 1.03% while credit growth was higher than the growth of mobilized capital. This is not good for increasing liquidity in bank lending activities.

Based on the analysis of the current situation of Vietnamese commercial banks above, managers need to take more drastic measures in restructuring, improving the quality of corporate governance, gradually reducing the proportion of credit in total assets, and gradually shifting the income structure to other business investment activities, including bond investment and trading activities to increase competitiveness and ensure profits for banks to adapt to the integration process.

2.2 . CURRENT STATUS OF BONDS INVESTMENT AND TRADING ACTIVITIES OF VIETNAM COMMERCIAL BANKS

2.2.1 . Current status of basic conditions for implementing bond investment and trading activities of Vietnam Commercial Banks

2.2.1.1 . Conditions of Vietnam 's bond market

In fact, in Vietnam, the bond market has been formed and developed over the past 10 years in parallel with the listed stock market [3], [5], [19].

- August 2000: Government bonds were put into trading on the Ho Chi Minh City Stock Exchange, now HOSE. This was the first event marking the Government bonds being traded on the stock market and considered a commodity on the stock market.

- During the period 2004-2009, the government implemented a number of measures with the aim of increasing liquidity in the secondary bond market. Specifically:

+ August 2005: Government bonds were put into trading on the Hanoi Stock Exchange. Since then, Government bonds have been traded in parallel on both Hanoi and Ho Chi Minh City exchanges.

+ In May 2006, the Vietnam Securities Depository was established under Decision 189/2005/QD-TTg of the Prime Minister. Although it is called the Depository Center (depository/custodian), this agency also performs clearing/settlement activities for the two stock exchanges in Ho Chi Minh City and Hanoi. From this point on, this will be the only and mandatory depository for all types of securities in general and bonds in particular. The concentration of post-transaction processing and depository in one place aims to reduce costs and create connectivity between markets, indirectly helping to increase liquidity in the market. This center is also the focal point for issuing ISIN codes for securities in the Vietnamese market.

+ June 2006: Decision No. 2276/QD-BTC on centralizing bidding for government bonds at the Hanoi Securities Trading Center. This decision stipulates that bidding for government bonds, including treasury bonds and investment bonds, will only be centralized at the Hanoi Securities Trading Center from July 1, 2006.

+ January 2008: Decision 86/2008/QD-BTC approved the project to build a specialized Government Bond market. This is considered the most important milestone because it sets out the goals, roadmap and determines the development model of the Government Bond Market. The project is built to create a specialized bond trading market, completely separate from the stock trading market.

+ May 2008: The State Securities Commission decided to transfer government bonds from the Ho Chi Minh City Stock Exchange to be listed on the Hanoi Stock Exchange. According to the decision, from June 2, 2008, all government bonds listed on the HOSE will be officially listed and traded on the Hanoi Stock Exchange.

+ September 2009: Specialized Government Bond trading system officially launched

The Government Bond Market will be put into operation and launched by the Hanoi Stock Exchange on September 24, 2009 with the aim of maximizing the importance of this capital mobilization channel for the economy. The goal of building and developing the Government Bond Market is to expand the market, increase liquidity in the Government Bond Market, link the primary market and the secondary market, and strengthen market supervision.

Regarding the organization of bond issuance, registration, depository, listing and trading: Currently, for government bonds, government-guaranteed bonds and local government bonds, registration and depository are carried out at the Securities Depository Center, and the organization of bidding, listing and trading of bonds is carried out through the Hanoi Stock Exchange (currently abbreviated as HNX). For corporate bonds, they are mainly issued in a private form.

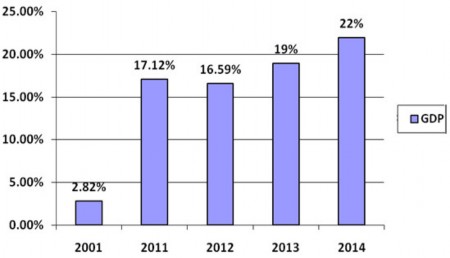

Chart 2.1 : Size of Vietnam 's bond market ( % GDP ) in the period 2001-2014

Source : Ministry of Finance

In general, the bond market in general and the government bond market in particular in Vietnam have made great strides in terms of scale and quality, becoming an important channel in mobilizing capital for the state budget and supporting bond investment and trading activities of the commercial banking system. Specifically, by the end of 2014, the size of the Vietnamese bond market reached the equivalent of 22% of GDP instead of 16.59% of GDP in 2012 and 17.12% of GDP in 2011 or 2.82% of GDP in 2001. In addition, government bonds were issued

Issued bonds include standard maturities, of which the under 5-year maturity currently has the largest proportion, accounting for about 90% of the total volume of issued bonds. However, the proportion of Government bonds issued with long maturities of 5 years or more tends to increase, accounting for 44.5% of the total volume of Government bonds issued in 2014.

Up to now, the total value of Government bonds in circulation has reached approximately 680 trillion VND, an increase of more than 4 times compared to 2009. The size of the Government bond market has achieved an average growth rate of 23%/year over the past 5 years, and is considered to have the leading growth rate among emerging economies in the East Asia region as well as the ASEAN + 3 region. The liquidity of the bond trading market in 2014 increased more than 20 times compared to 2009, from 166 billion VND/session in 2009, to an average trading value of more than 100 billion VND/session in 2014.

3,400 billion VND/session in 2014 [13], [29].

Chart 2.2 : Average bond trading value / session in the period 2009-2014

Unit : Billion VND

Source : HNX

Since August 2012, Treasury bills auctioned through the State Bank have been traded centrally on the specialized Government bond trading system, contributing to the unification of the long-term and short-term debt markets. The liquidity index of Treasury bills has increased 6 times after listing [29]. The programs of issuing large-lot Government bonds and exchanging bonds in coordination with the State Treasury implemented over the past 3 years have

bringing positive changes in bond code structure and maturity structure. Along with the birth of the yield curve system since 2013, the Vietnamese government bond market is gradually improving and becoming more attractive, continuously being assessed as having the fastest growth rate in East Asia in recent years [29].

In addition, the launch of the electronic bidding system at HNX starting from August 2012 also created many advantages for members. Through this system, market members can enter bids remotely, quickly edit and cancel bids, receive instant bidding results, track payment progress, look up, export statistical data and make reports right on the system. The digitization of the entire bidding process from the beginning to the end of the bidding session on the one hand helps members reduce unnecessary paperwork, participate in bidding more quickly and effectively; on the other hand, it helps the operating agency significantly shorten the time for bid evaluation and determination of bidding results compared to before; at the same time, it contributes to ensuring the transparency of bidding activities; and helps management agencies to be able to issue reasonable interest rate policies, as well as monitor the performance of members more proactively.

Besides, the structure of Vietnam's bond market so far has a government bond ratio of more than 96% of the total issued bonds.

Table 2.5 : Structure of Vietnam 's bond market in the period 2009-2014

2009 | 2010 | 2011 | 2012 | 2013 | 2014 | |||||||

Mass (Ratio) USD) | Proportion (%) | Mass (Ratio) USD) | Proportion (%) | Mass (Ratio) USD) | Proportion (%) | Mass (Ratio) USD) | Proportion (%) | Mass (Ratio) USD) | Proportion (%) | Mass (Ratio) USD) | Proportion (%) | |

Total | 11.8 | 100% | 15.5 | 100% | 17 | 100% | 25 | 100% | 28.7 | 100% | 40.6 | 100% |

TPCP | 10.8 | 91.5% | 14 | 90.3% | 15 | 88.2% | 24 | 96% | 28 | 97.5% | 40 | 98.5% |

TPDN | 1 | 8.5% | 1.5 | 9.7% | 2 | 11.8% | 1 | 4% | 0.7 | 2.5% | 0.6 | 1.5% |

Maybe you are interested!

-

Research Model of the Impact of Bond Investment Activities on Business Results of Commercial Banks

Research Model of the Impact of Bond Investment Activities on Business Results of Commercial Banks -

Current Status of Management of Economic Development Investment Activities

Current Status of Management of Economic Development Investment Activities -

Bond investment activities of Vietnamese commercial banks 1683880233 - 27

Bond investment activities of Vietnamese commercial banks 1683880233 - 27 -

Current Status of Foreign Exchange Trading Activities at NHtmcp Ctvn

Current Status of Foreign Exchange Trading Activities at NHtmcp Ctvn -

Import-export and investment activities at Vietnam Paper Corporation in recent years - Current situation and solutions - 14

Import-export and investment activities at Vietnam Paper Corporation in recent years - Current situation and solutions - 14

Source : Asian Bond Monitor 2009-2014

This ratio is considered equivalent to less developed markets in the region such as Indonesia and the Philippines. However, in general, the size and scope of the market is still small, liquidity

not high compared to bond markets in other Asian countries such as Korea, Malaysia, Singapore, Japan etc.

In addition, the bond market structure is not complete, the investor system (especially long-term investment institutions) is still thin, and the service infrastructure system for the market is still underdeveloped. In addition, the Vietnamese bond market has the following limitations:

- Firstly, the goods on the market are still monotonous: the market still lacks trading products, the investor structure is not diversified, affecting the diversification of trading products as well as the lack of incentive mechanisms, support for investment entities or the lack of support for risk prevention operations. These factors partly reduce the attraction of investors to actively participate in the government bond market. In addition, the product term is mainly concentrated in short-medium term, there is no diversification to products with long-term terms. Specifically, at December 31, 2014, the proportion of bonds with remaining terms from 6 months to 5 years accounted for 71.43% of the total number of bonds traded, of which the remaining term of 1 year accounted for 23.51%, the 2-year type accounted for 20.33%, the remaining term of 3 years accounted for 9.56%, the remaining term of 5 years accounted for 7.01%.

- Second, the total outstanding debt of the corporate bond market is still quite modest, very small compared to the potential and markets of countries in the region. By the end of 2014, the total outstanding debt was only about 1.5-2% of GDP. Meanwhile, corporate bonds in developed markets are the main long-term capital channel for enterprises, but in Vietnam, the corporate debt market is still in its infancy, not attracting professional investors such as funds, large financial institutions and individual investors.

In general, the bond market is playing an important role in the public debt market, becoming an important capital mobilization and capital allocation channel for the country's economic development. In addition, with the expectation of organizing a more professional, stable and effective bond market, on September 24, 2009, the specialized government bond market was officially put into operation with the main goal of organizing a government bond market under the management of the State, as a capital mobilization channel for the state budget to serve development investment and diversify products on the Vietnamese stock market.

Thus, the Vietnamese bond market has been supporting the formation and development of bond investment and trading activities of the Vietnamese commercial banking system.

2.2.1.2 . Legal conditions for bond investment and trading activities of Vietnam Commercial Bank

- Basically, since its establishment, the legal framework for bond market operations has been continuously issued and revised to comply with international market practices to facilitate market participants. Specifically:

- 2003: The Government issued Decree 141/2003/ND-CP on the issuance of Government bonds, Government-guaranteed bonds and local government bonds in Vietnamese Dong and foreign currencies nationwide.

Accordingly, Government bonds issued by the Government include: Treasury bills, Treasury bonds, Central project bonds, investment bonds, foreign currency bonds and national construction bonds.

Government-guaranteed bonds have a term of one year or more, are issued by enterprises to raise capital for investment projects as designated by the Prime Minister and are issued for each specific project. The total value of bonds issued for a project must not exceed the total value of the project and the specific issuance level for each project must be decided by the Prime Minister.

Also with a term of over 1 year, local government bonds are issued by the provincial People's Committee authorized by the State Treasury or local financial and credit institutions to mobilize capital for projects and works from the local budget investment capital source that are included in the plan but have not been allocated budget capital in the year.

- During the period 2004-2009, the government issued a number of important documents. Specifically:

+ The Ministry of Finance also issued Decision 46/2006/QD-BTC on the Regulations on the issuance of Government bonds in large lots. The issuance of Government bonds in large lots aims to increase the ability to mobilize capital and for investment.

development, while enhancing the liquidity of government bonds in the trading market and creating the ability to form benchmark interest rates for debt instruments.

+ July 2008: Decision No. 46/2008/QD-BTC promulgating the Regulation on management of Government bond transactions at HNX. This Regulation regulates the activities of registration for listing, information disclosure, members trading Government bonds (G-bonds), trading and management of transactions of listed G-bonds at HNX. This Regulation regulates Members trading G-bonds at HNX; G-bond trading system; Listing price; Execution price; Regular members; Special members; Regular transactions; and Repurchase transactions.

Since 2010, the legal framework for the issuance of government bonds has been studied for further innovation. In particular, the listing and centralized trading of treasury bills at HNX has created an overall picture of the secondary trading situation of government bonds, improving the efficiency of market operations, creating favorable conditions for the State Treasury to increase its ability to mobilize capital for the state budget and for development investment. In addition, the system of legal documents from Laws, Decrees, Circulars has fully regulated and guided the process and procedures for issuance, registration, depository, listing and trading of all types of government bonds, government-guaranteed bonds, local government bonds and corporate bonds. Specifically:

- In the primary market : with the promulgation of the Law on Public Debt Management, the Law amending and supplementing a number of articles of the Securities Law (2010 ) , the Government has issued many Decrees replacing the above legal documents to manage the Vietnamese bond market, including Decree No. 01/2011/ND-CP on the issuance of Government bonds, Government-guaranteed bonds and local government bonds. Decree No. 15/2011/ND-CP on Government issuance and guarantee, Decree No. 58/2012/ND-CP detailing and guiding the implementation of a number of articles of the Securities Law and the Law amending and supplementing a number of articles of the Securities Law. In addition, Decree 90/2011/ND-CP on corporate bond issuance was issued in 2011 to replace the previous Decree 52/2006/ND-CP to create a more open legal corridor for corporate bond issuance.

- In the secondary market : to regulate market operations in compliance with

In compliance with legal regulations, HNX's transaction guidance documents and Vietnam Securities Depository (VSD)'s clearing and settlement guidance documents were also issued to systematize standards for the government bond market.

In 2012, the Ministry of Finance issued all circulars guiding Decree 01/2011/ND-CP and Decree 90/2011/ND-CP to complete the legal framework for the issuance of government bonds, government-guaranteed bonds, local government bonds, treasury bills and corporate bonds, specifically: Circular No. 17/2012/TT-BTC dated February 8, 2012 on the issuance of government bonds in the domestic market; Circular No. 34/2012/TT-BTC dated March 1, 2012 on the issuance of government-guaranteed bonds; Circular No. 81/2012/TT-BTC dated May 22, 2012 on the issuance of local government bonds; Joint Circular No. 106/TTLT/BTC-NHNN dated June 28, 2012 on the issuance of treasury bills through the State Bank; Circular No. 211/2012/TT-BTC dated December 5, 2012 on issuance of corporate bonds.

In August 2012, for the first time, State Treasury bills were listed on the stock exchange, which was considered a plus point, a “highlight” of the Vietnamese bond market. This made the bills more attractive in the primary market, facilitating the Government’s short-term capital mobilization.

On February 1, 2013, the Minister of Finance signed and issued Decision No. 261/QD-BTC approving: "Roadmap for developing Vietnam's bond market to 2020" with specific orientations, goals, and solutions for developing Vietnam's bond market in the coming time.

In 2015, the Ministry of Finance issued the second generation of Circulars guiding Decree No. 01/2011/ND-CP on the issuance of government bonds, government-guaranteed bonds and local government bonds to conform to market development and international practices, creating favorable conditions for entities to mobilize capital in the bond market, specifically as follows:

+ For Government bonds: Circular No. 111/2015/TT-BTC has stipulated improved contents such as: (i) One step higher on the rights and obligations of

bidding members; (ii) Allow the issuance of new products such as zero-coupon bonds; (iii) Complete the process of underwriting and bidding for the issuance of government bonds (time of notification, payment, registration, depository, listing and trading of bonds) to shorten the time for registering, depository, listing and trading of bonds; (iv) Improve the bidding schedule and maturity date of government bonds to facilitate investors in participating in bidding and support the treasury management of the State Treasury; (v) Provide detailed regulations on the method of retailing bonds.

+ For Government-guaranteed bonds: Circular No. 99/2015/TT-BTC has improved contents such as (i) More detailed regulations on bond issuance guarantee dossiers; (ii) Completing regulations on registration for depository and listing of Government-guaranteed bonds; (iii) clearly regulating the content of information disclosure, time limit for information disclosure and method of information disclosure of Government-guaranteed bond issuers to increase transparency and create favorable conditions for investors when participating in bond purchases.

+ For local government bonds: Circular No. 100/2015/TT-BTC has improved contents such as (i) More detailed regulations on dossiers and projects for issuing local government bonds; (ii) Regulations on methods of buying back and exchanging local government bonds; (iii) Regulations on information disclosure regime before and after issuing local government bonds. All new regulations aim to facilitate localities to mobilize capital through bond issuance, while enhancing the transparency of local governments through bond issuance to attract investors.

+ For corporate bonds: In 2014, the Ministry of Finance submitted to the Government for signing and promulgation Decree No. 88/2014/ND-CP on credit rating services to promote the development of the corporate bond market. On that basis, the Prime Minister issued Decision No. 507/QD-TTg dated April 7, 2015 on the Planning for the Development of Credit Rating Services to 2020, with a vision to 2030.

- Regarding the legal framework for this banking activity, during the time

Recently, the authorities have issued a number of legal documents with quite strict regulations as follows:

- Regarding corporate bond investment and trading :

+ According to the content of Circular 28/2011/TT-NHNN dated September 1, 2011, the calculation of outstanding debt for purchasing corporate bonds into outstanding credit is implemented according to the regulations of the State Bank. In other words, the total investment in corporate bonds is calculated into the total outstanding credit for a customer, for a customer and related persons according to the provisions of Article 128 of the Law on Credit Institutions and related regulations of the State Bank of Vietnam. In addition, commercial banks are only allowed to purchase corporate bonds when they meet the following conditions:

a. Established and operating under the provisions of the Law on Credit Institutions.

b. The establishment and operation license issued by the State Bank of Vietnam includes the content of purchasing corporate bonds.

c. Ensure safety ratios in operations according to regulations of the State Bank of Vietnam.

d. Have a system and implement internal credit ratings, including credit ratings for bond-issuing enterprises.

e. Issue regulations on purchasing corporate bonds in accordance with relevant legal provisions, including: Process, procedures for appraisal and decision to purchase bonds; responsibilities and authority of individuals and units in reviewing and deciding to purchase bonds; types and characteristics of bonds purchased by credit institutions and foreign branches; conditions of corporate bonds purchased by credit institutions and foreign bank branches; credit management policies and limits, risk measurement and management systems, risk handling measures and processes; implementation of safety ratios in business operations; internal control of bond purchasing activities.

+ According to the content of Circular 34/2013/TT-NHNN dated December 31, 2013 and some other documents, commercial banks are not allowed to invest in purchasing corporate bonds issued for the first time in the primary market.

- Regarding the term trading of bonds : According to the content of the circular

Circular No. 21/2012/TT-NHNN and Circular No. 01/2013/TT-NHNN stipulate the conditions for commercial banks when conducting term bond trading activities as follows:

a. Have technical infrastructure (machinery, equipment, software programs) that meet the requirements of transactions in the currency market, ensuring full, accurate and timely updating of transaction data for each transaction of the credit institution and foreign bank branch with customers;

b. Have a team of qualified and professional staff to conduct transactions in this field.

c. Have internal regulations on business processes and risk management processes.

d. Not subject to any restriction, suspension or temporary suspension by the State Bank of the purchase and sale of term bonds on the interbank market at the time of the transaction.

e. At the time of transaction, the commercial bank must not have overdue debts of 10 days or more at other credit institutions or foreign bank branches.

- Regarding open market participation activities : according to the regulations of the State Bank , commercial banks wishing to participate in open market operations with the State Bank must first be granted a certificate of recognition as members participating in the open market. To be granted this certificate, commercial banks established and operating under the Law on Credit Institutions must meet the following conditions:

a. Have a deposit account at the State Bank (State Bank Transaction Office or State Bank branch in province or city);

b. Have sufficient means necessary to participate in open market operations including FAX machine and computer with internet connection.

- Regarding other activities ( bidding activities , participation in investment and trading of listed bonds on the secondary market at HNX ) : Commercial banks can directly conduct bidding transactions , self -trading order transactions (if they become special members according to regulations of the Ministry of Finance and are members of the VSD depository center), or indirectly through securities companies (which are members directly participating in transactions at HNX and are members of the VSD depository center).

Thus, based on the above regulations, Vietnamese commercial banks have had the following provisions: