In addition to the two stock exchanges for listed stocks, the secondary stock exchange for unlisted stocks (OTC) was also officially opened on July 14, 2005 with 6 enterprises participating in stock trading on the exchange. Immediately after the first trading session, the total number of stocks sold was 1,420 billion VND, the value of stock transfers of these 6 enterprises reached 8.3 billion VND. Up to now, stock and bond transactions taking place on this market have been quite active. By the end of 2007, there were about 350 types of stocks and bonds of 30 commercial banks, nearly 340 enterprises, with a total capitalization value of about 500,000 billion VND being traded.

After nearly 10 years of operation, the Vietnamese stock market has achieved the following results[40,84]:

2.1.2.1. On scale of operations

When the stock market started operating, only the shares of 2 joint stock companies were listed, SAM and REE, traded at the Ho Chi Minh City Stock Exchange with a total listed capital value of 270 billion VND. By the end of 2007, there were 775 types of securities listed and registered for trading in the organized market, with a total volume of more than 4,304.72 million securities and a total value of more than 147,761.97 billion VND. Of which, the number of listed shares was 207 (Hanoi Stock Exchange had 91 listed companies, Ho Chi Minh City Stock Exchange had 116 listed companies) with a total listed volume of nearly 3,082.37 million shares and a listed value of more than 30,823.697 billion VND. In addition, there are 566 types of government bonds and corporate bonds (159 bonds listed at the Hanoi Stock Exchange and 407 bonds listed at the Ho Chi Minh City Stock Exchange) with a total listing volume of about 1,122.35 million bonds and a total listing value of about VND 155,938.27 billion.

It can be said that the years 2006 and 2007 marked the "explosion" of the Vietnamese stock market. By the end of 2006, the market capitalization value reached the equivalent of 22.4% of GDP, an increase of about 20 times compared to 2005. In 2007, the total value of securities transactions reached nearly 40,000 billion VND, an increase of more than 3 times compared to the total value of transactions in the whole year of 2006. The total market value in 2007 had some days reaching a high level, equivalent to 38% of GDP. The Vn-index increased from 307.5 points at the end of 2005 to 809.86 points in the session on December 20, 2006 and broke through to a record level of 1,174.22 points in the session on March 12, 2007. The HASTC-Index at the end of December 2006 stopped at 242.89 points and reached a record.

459.36 points in the session on March 19, 2007, a three-fold increase in just three months. The total capital mobilized through the stock market in 2005 reached over 7,000 billion VND, after one year it increased four-fold, of which over 18,000 billion VND was the value of shares of state-owned enterprises auctioned after equitization. In addition, nearly 500 types of government bonds were mobilized and listed on the stock market with a total value of over 81,000 billion VND, accounting for 8.4% of GDP in 2006. The appearance of CCQDT with a total value of 1,000 billion VND and 3,550 billion VND of bonds from Vietcombank and BIDV banks have made the goods on the stock market even more abundant. From July 2002 to the end of 2007, the Ho Chi Minh City Stock Exchange organized 1,690 trading sessions and the Hanoi Stock Exchange organized 523 safe and continuous trading sessions [40]. With the above growth rate and basic indicators, the Vietnamese stock market in 2007 was assessed as the fastest growing in Asia and attracted the attention of many investors.

Table 2.3: Listed volume and trading value of listed securities on the entire market as of the end of 2007

Target

Total | Share | Bonds | CCQDT | Other husband | ||

Listed volume | Stock Exchange HN | 1,746,156,937 | 1,134,850,978 | 611.305.968 | 0 | 0 |

Stock Exchange Ho Chi Minh City | 2,558,564,700 | 1,947,517,830 | 511,046,870 | 100,000,000 | 0 | |

Total | 4,304,721,646 | 3,082,368,808 | 1,122,352,865 | 100,000,000 | 0 | |

Proportion | 100% | 71.6% | 26.08% | 2.32% | 0% | |

Listed value (million VND) | Stock Exchange HN | 72,479,099.47 | 11,348,509.87 | 61,130,589.60 | 0 | 0 |

Stock Exchange Ho Chi Minh City | 75,282,874.87 | 19,475,187.87 | 54,807,687.00 | 1,000,000.00 | 0 | |

Total | 147,761,947.34 | 30,823,697.74 | 115,938,276.60 | 1,000,000.00 | 0 | |

Proportion | 100% | 20.86% | 74.46% | 0.68% | 0% |

Maybe you are interested!

-

Concept and Characteristics of Trading Listed Stocks on the Centralized Stock Market

Concept and Characteristics of Trading Listed Stocks on the Centralized Stock Market -

The impact of financial market development on the capital structure of listed enterprises in the ASEAN Economic Community - 28

The impact of financial market development on the capital structure of listed enterprises in the ASEAN Economic Community - 28 -

The impact of financial market development on the capital structure of listed enterprises in the ASEAN Economic Community - 2

The impact of financial market development on the capital structure of listed enterprises in the ASEAN Economic Community - 2 -

Factors affecting the liquidity of stocks listed on the Vietnamese stock market - 4

Factors affecting the liquidity of stocks listed on the Vietnamese stock market - 4 -

Compare Listed and Trading Bond Values at Hanoi Stock Exchange

Compare Listed and Trading Bond Values at Hanoi Stock Exchange

Source: Author's own compilation based on reports of the State Securities Commission, 2003, 2004, 2005, 2006, 2007.

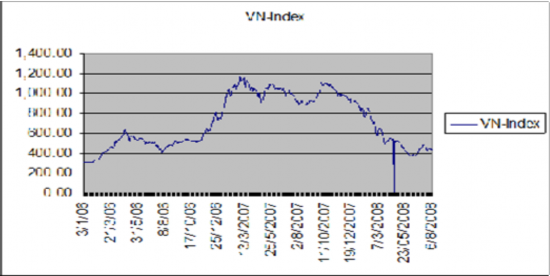

In 2008, due to the impact of the global financial crisis and tight monetary policy to control inflation, the Vietnamese stock market had many fluctuations. The highest Vn-Index was 921 points (January) and the lowest was on December 10.

only 286 points. The transaction value of the two markets Hose and Hastc also affected the ups and downs of the Vn-Index and Hastc-Index. The average transaction value of stocks and fund certificates in 2008 was 745 billion VND/session. The transaction value gradually decreased from January to June, the average transaction value of stocks and fund certificates per session was 945 billion VND in January, down to 250 billion VND in May. From June, the transaction value gradually increased, the average in June was 631 billion VND/session and reached 1,240 billion VND/session in September. From October to December, the transaction value continuously decreased to 620 billion VND/session. The average bond transaction in 2008 was 875 billion VND/session, a significant increase compared to 470 billion VND/session in 2007. The value of bond transactions increased sharply in June, October and November (each month reached over 1,000 billion VND). During this time, foreign investors increased their transactions, mainly selling.

As of December 31, 2008, market capitalization was 19.76% of GDP, a significant decrease compared to 40% in 2007. The capital mobilized by the stock market in 2008, including initial auctions, issuances, and bidding for government bonds, only reached nearly 27.8 trillion VND, much lower than 127 trillion VND in 2007. The number of listed companies was 342, an increase of 89 companies compared to the end of 2007. The number of investor accounts reached over 500 thousand accounts, an increase of 200 thousand accounts compared to 2007 [84].

Chart 2.6: VN-Index developments from January 3, 2006 to August 6, 2008

Source: [84] State Securities Commission, 2008

In 2009, it can be affirmed that the loose fiscal and monetary policies and the Government's economic stimulus package were the main driving forces for the stock market to recover. In terms of growth rate, the Vietnamese stock market in 2009 was considered to have a very high growth rate, up to 60-70%, specifically: In the first 9 months of 2009, the Vietnamese economy had a recovery due to the effect of the Government's stimulus package. The Vietnamese stock market had strong growth again, the Vn-Index increased from 234 points (February 24, 2010) to 633.2 points (October 23, 2010). However, at the end of 2009, due to tensions in the foreign exchange market, the risk of inflation and increasing government debt, in the last two months of 2009, monetary policy began to show signs of tightening. Furthermore, since the second half of October 2009, the State Bank of Vietnam has required banks to stop lending securities. Demand on the stock market has been strongly affected by the above adjustments and has led to a decrease in market liquidity, as well as excessive psychological impacts that have caused stock indices to fall into a downward cycle from November 2009 until the end of the year. The VN-Index fell sharply from its peak of 633.2 points on October 23 to 434.87 points on December 17. Trading volume from November to the end of the year has decreased sharply (more than 20%) compared to September and October. As the year ends, market liquidity becomes more and more worrisome. By the end of 2009, although the market had made further progress, the VN-Index still failed to reach the 500-point mark when it closed (December 31, 2009) at 494.77 points.

However, by the end of 2009, there were 447 stocks and fund certificates listed, an increase of more than 30% compared to 2008. The total market capitalization reached more than 669 trillion VND (39 billion USD), equivalent to 55% of GDP in 2008. This capitalization level increased nearly 3 times compared to 225 trillion at the end of 2008. The number of investor accounts was 739,000 accounts, an increase of more than 50% compared to 2008 [84]. The portfolio value of foreign investors in the stock market as of December 2009 reached nearly 6.6 billion USD, an increase of nearly 1.5 billion USD... With these results, according to the assessment of the State Securities Commission (SSC), the Vietnamese stock market has had strong growth due to the positive impact of the improving macro economy and the continuously positive performance of listed enterprises. On the other hand, the international economy and stock market have recovered from the most difficult period, so it has also had a positive impact on the Vietnamese stock market[84].

A highlight of the Vietnamese stock market in 2009 was the launch of the UPCoM exchange. On June 24, 2009, the UPCoM exchange was launched, which can be considered a transitional step from the OTC market to the official listed market, creating a favorable environment for buying/selling and transferring securities of unlisted public companies. Securities traded on the UPCoM exchange include shares of public companies that are unlisted or have been delisted on the two exchanges HaSTC or HoSE; convertible bonds of public companies that are unlisted or have been delisted. Initially, only 6 public companies participated, but to date, 34 types of stocks have been traded on the UPCoM exchange [84].

2.1.2.2. About the subjects participating in the stock market

In addition to the listed companies mentioned above, the system of securities trading organizations is a very important financial institution, so the development in quantity and quality of them has a great influence on the operation of the stock market. Therefore, by the end of 2009, the State Securities Commission has licensed 103 securities companies, of which there are currently more than 90 companies in operation, 43 fund management companies (MFCs), more than 60 securities investment funds and 6 commercial banks licensed to operate as securities depository banks (including 2 domestic commercial banks and 4 foreign bank branches) [84]…

In the early days, securities companies mainly performed brokerage services, but now, most securities companies have implemented proprietary trading, underwriting, portfolio management and financial consulting services.

Currently, there are foreign investment management companies participating in activities on the Vietnamese stock market such as Dragon Capital, Mekong Capital, PXP, Finasa, Indochina... (including 4 joint venture investment management companies and 2 investment management companies belonging to foreign life insurance companies). Regarding securities investment funds, the capital scale of more than 60 foreign investment funds participating in the Vietnamese stock market is more than 4 billion USD, there are nearly 50 foreign investment organizations opening accounts or managing investment trusts on the Vietnamese stock market. Among them are the world's leading financial institutions and banks such as JP Morgan, Merrill Lynch, City Group, Nomura Securities,...

Recently, Vietcombank is the first commercial bank to be permitted by the State Securities Commission to deploy the service of supervising securities investment funds, specifically the VF1 fund. To deploy this service, Vietcombank has carried out the custody of securities and contracts.

economic documents related to VF1 fund assets, performing net asset valuation of VF1 Fund and VF1 Fund Management Company.

In addition, the State Securities Commission has only selected the Bank for Investment and Development of Vietnam (BIDV) as the designated bank for securities settlement. BIDV opens cash payment accounts for the Securities Trading Center and depository members to serve the purpose of cash payment for securities transactions.

In recent years, the number of stock investors has increased rapidly due to the state's regulations on stock investment by organizations and individuals being more open and favorable. Therefore, in 2005, there were over 31,000 trading accounts in the organized market, and by the end of 2006, this number was 106,393 accounts. In 2007, the stock market had about 243,809 accounts, an increase of 2.3 times compared to 2006 (106,393 accounts), including 242,624 accounts of individual investors and 1,185 accounts of institutional investors. In 2008, the number of investor accounts reached over 500,000 accounts, nearly double that of 2007. Statistics from the State Securities Commission show that, as of December 2009, the number of investor accounts opened at securities companies had reached a record high of 739,000 accounts[84].

2.1.2.3. On opening up to foreign investors

Currently, foreign investors are allowed to hold up to 49% of the total number of shares listed on the Vietnamese stock market. Since June 2009, the ownership ratio of foreign investors in unlisted public companies has increased from 30% to 49%. A recent highlight is the strong participation of foreign investors with

5,568 trading accounts (5,353 individual accounts and 215 institutional accounts).

As of December 31, 2008, the portfolio value of foreign investors in the stock market (both official and unofficial) had only reached nearly 4.5 billion USD [83]. However, as of August 31, 2009, the portfolio value of foreign investors in the stock market had increased sharply with a total of nearly 1,090 billion VND (nearly 6.4 billion USD), of which investment in stocks was 950 trillion VND (5.5 billion USD), bonds were 14.5 trillion VND (843 million USD) and fund certificates were 980 billion (57 million USD). As of December 2009, the portfolio value of foreign investors reached nearly 6.6 billion USD, an increase of nearly 1.5 billion USD compared to 2008... Thus, the portfolio value of foreign investors increased nearly 1.5 times compared to the time from December 31, 2008 [84].

2.2 THE ROLE OF THE STATE IN THE FORMATION AND DEVELOPMENT OF VIETNAM'S FINANCIAL MARKET

2.2.1 The role of the State in the formation and development of the monetary market in Vietnam

2.2.1.1 The state's efforts in the process of forming and developing the monetary market

Before 1990, the Vietnamese banking system was a one-tier system, with only the State Bank performing both the function of State management of currency and credit and the business function. The capital surplus or shortage of branches was transferred from other branches or satisfied by the issuance fund. Therefore, the TTTT did not have the conditions to form.

In May 1990, the promulgation of two banking ordinances, the State Bank Ordinance and the Ordinance on Banks, Credit Cooperatives and Finance Companies, marked the formation of a two-tier banking system with the establishment of commercial banks of many economic sectors such as State-owned commercial banks, joint-stock commercial banks, foreign joint-venture banks, and foreign bank branches in Vietnam. This is a necessary and sufficient condition for the formation of Vietnam's financial market.

However, the Vietnamese market only really operated and developed after the Governor of the State Bank issued Directive No. 07/CT-NH dated October 7, 1992 on credit relations between credit institutions, allowing credit institutions to borrow and lend to each other. Since then, the scale of the market has continuously increased, and important parts of the market have gradually been formed. These are the traditional short-term credit market, the interbank domestic currency market (established under Decision No. 136/QD-NHNN dated March 10, 1993), the interbank foreign currency market (established under Decision No. 203/QD-NHNN dated October 20, 1994), and the Treasury bill bidding market (established under Decision No. 61-QD/NH19 dated March 8, 1995). Thus, by 1995, the capital market had basically formed parts of the market, contributing to promoting capital exchange for the economy. However, the new types of capital markets were still in their infancy, the market scope was still limited within the scope of the banking system and activities only took place in the primary market, there was no secondary capital market.

On July 12, 2000, after a long period of preparation, the State Bank officially launched open market operations and began operations. This event marked an important turning point in the market, the market was expanded across the entire economy. At the same time, open market operations promoted the repurchase and resale of short-term debt instruments, initially forming a secondary market - a new qualitative development of the Vietnamese market. Since then, market participants, goods traded on the market as well as market turnover have been gradually expanded, and the activities of the market have been gradually modernized.

The role of the state in forming and developing the component markets of the information technology sector is specifically demonstrated:

(i) For short-term credit markets.

Since August 2000, the State Bank has replaced the ceiling interest rate management mechanism with the basic interest rate management mechanism for loans in Vietnamese Dong. Accordingly, credit institutions (CIs) lend to customers based on the basic interest rate announced by the State Bank according to the principle that the lending interest rate does not exceed the basic interest rate and the margin prescribed by the Governor of the State Bank in each period. The basic interest rate and the margin are announced periodically every month, and if necessary, the State Bank will announce timely adjustments to the interest rate. However, for a long time, the basic interest rate has not really kept up with the fluctuations in the market and is often quite far from the common interest rate at commercial banks. In reality, the basic interest rate is only the reference interest rate for the operations of credit institutions.

Since June 2002, the State Bank has decided to implement negotiated interest rates to begin the process of interest rate liberalization. Accordingly, credit institutions are allowed to set their own deposit interest rates and lending interest rates based on capital supply and demand and the creditworthiness of customers. The State Bank has partly stopped intervening in credit institutions' business interest rates, creating conditions for credit institutions to be more proactive in their activities. Therefore, in terms of capital purchase and sale by commercial banks and other credit institutions, in recent years there has been an increase in quantity (an average increase of 22% - 30% compared to the previous year) [35], a rich variety of types and a constant improvement in quality. This shows that this is the main capital supply market for the economy.