production and business and nature of operations; ownership structure and owners; products and services provided by the business; main customers, etc.

o Cash flow – Borrower’s cash flow: mainly includes cash flow from sales revenue or income. There are also sources such as cash flow from asset sales; other sources of capital mobilization and indicators of payment capacity.

Banks evaluate customers' ability to repay debts through financial capacity and business results from past data. Evaluation information from the company's financial statements: Business performance report, balance sheet, cash flow statement and financial statement notes. Banks collect information on cash flow generated from sales revenue or income to consider the source of funds to repay loans to the bank.

o Collateral – Loan guarantee:

The bank will consider factors such as: Asset value; Legal status of the asset; Potential obsolescence or depreciation; Whether the asset is being used as collateral for another loan; Whether the asset is insured; The bank's position with respect to proceeds from the liquidation of the collateral.

o Conditions – Other conditions:

The customer's current competitive position;

The client's business performance compared to other competitors in the industry;

Product competition situation;

Customer sensitivity to business cycles and technological changes;

Labor market conditions/status in the industry or market area in which the client operates;

The future of the industry;

Objective factors affecting the customer's business and industry activities such as: politics, law, society, technology, environment.

c) Model 6C:

The 6C model includes 5 elements of the 5C model and adds the Control element, including control before, during and after lending:

Current laws, regulations and statutes relating to the credit under consideration.

Completeness of documents for control work.

Loan and disbursement documents must be complete and signed by all parties.

The loan's compliance with the bank's rules and regulations.

Opinions of economic and technical experts on the industry environment, on the product, and on other factors that may affect the loan.

Control the use of loan capital and the purpose of capital use.

Appendix 2: Set of 17 Basic Principles of Risk Management according to Basel II:

Group

STT | Contents of the principles | |

Establishing an appropriate credit risk environment fit | 1 | Identify the board's responsibilities in risk management |

2 | Identify the board of directors' responsibilities in managing RRTD | |

3 | Banks need to identify and manage risk in all their products and activities. | |

Operate under a sound credit granting process | 4 | Banks need to conduct credit operations according to appropriate standards. with target market and thorough understanding of borrowers |

5 | The bank must establish an overall credit limit at the customer level. individual customers and related customer groups. | |

6.7 | Banks need to establish clear credit procedures for approving new credit as well as adjusting and extending credit facilities. existing. | |

Maintain appropriate management, measurement and monitoring processes | 8 | Banks must have a system to regularly monitor and manage credit portfolios have different risks. |

9 | Banks must have a system to monitor the status of loans. Personal use includes reserves and contingencies. | |

10 | Banks are encouraged to build and use the system. Internal assessment for risk management. | |

11 | Banks must have information systems and analytical tools to help RRTD measurement management. | |

12 | The bank has a comprehensive system of monitoring the composition and quality of credit amount | |

13 | Banks must assess significant changes in conditions. |

Maybe you are interested!

-

Applying Basel II to credit risk management at Saigon Thuong Tin Commercial Joint Stock Bank - 2

Applying Basel II to credit risk management at Saigon Thuong Tin Commercial Joint Stock Bank - 2 -

Assessment of credit risk management according to Basel II Agreement at Vietnam Joint Stock Commercial Bank for Investment and Development - 1

Assessment of credit risk management according to Basel II Agreement at Vietnam Joint Stock Commercial Bank for Investment and Development - 1 -

Credit risk management according to Basel II agreement at Saigon Thuong Tin Commercial Joint Stock Bank Sacombank - 1

Credit risk management according to Basel II agreement at Saigon Thuong Tin Commercial Joint Stock Bank Sacombank - 1 -

Assessment of Credit Risk Management Status According to Basel II Standards at Vietinbank Vinh Long

Assessment of Credit Risk Management Status According to Basel II Standards at Vietinbank Vinh Long -

Credit risk management according to Basel 2 Agreement at Vietnam Bank for Agriculture and Rural Development - 1

Credit risk management according to Basel 2 Agreement at Vietnam Bank for Agriculture and Rural Development - 1

economics when evaluating credits. | ||

RRTD control system | 14 | The bank must establish an independent, regular assessment system. throughout the risk management process. |

15 | Banks must ensure that the credit approval function properly managed, RRTD is at a level compatible with prudential standards and within the limits permitted by the bank. | |

16 | Banks need to have systems in place to identify and respond quickly to credit problem | |

RRTD monitoring | 17 | Supervisors conduct independent assessments of banks' strategies, policies, procedures and compliance. relating to credit granting and risk management. |

Source: Basel Committee

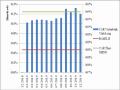

Appendix 3: Debt structure classified by debt group at Sacombank in the period 2012-2018

Outstanding debt classified by debt group at Sacombank in the period 2012 - Quarter 1/2019

Unit: Billion VND

2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | Q1/2019 | |

Group 1 debt | 93933 | 108176 | 125986 | 181666 | 182519 | 211643 | 250054 | 263856 |

Group 2 debt | 429 | 780 | 507 | 802 | 2595 | 899 | 1141 | 1354 |

Group 3 debt | 312 | 170 | 103 | 231 | 2613 | 1475 | 194 | 495 |

Group 4 debt | 764 | 422 | 414 | 147 | 2622 | 627 | 311 | 249 |

Group 5 debt | 897 | 1018 | 1006 | 3071 | 8510 | 8303 | 4922 | 5066 |

Total outstanding debt | 96335 | 110566 | 128016 | 185917 | 198859 | 222947 | 256622 | 271020 |

Source: Sacombank Financial Report 2012-2018 Proportion of overdue debt of each debt group to total overdue debt at Sacombank in the period 2012- Quarter 1/2019

Unit: %

2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | Q1/2019 | |

Group 2 debt | 17.86 | 32.64 | 24.98 | 18.87 | 15.88 | 7.95 | 17.37 | 18.90 |

Group 3 debt | 12.99 | 7.11 | 5.07 | 5.43 | 15.99 | 13.05 | 2.95 | 6.91 |

Group 4 debt | 31.81 | 17.66 | 20.39 | 3.46 | 16.05 | 5.55 | 4.74 | 3.48 |

Group 5 debt | 37.34 | 42.59 | 49.56 | 72.24 | 52.08 | 73.45 | 74.94 | 70.71 |

Source: Author compiled from Sacombank Financial Report 2012-2018

Appendix 4: Sacombank's formation and development process

December 21, 1991: Sacombank was one of the first joint stock commercial banks established in Ho Chi Minh City with initial charter capital of 3 billion VND.

Since its establishment, Saigon Thuong Tin Commercial Joint Stock Bank has had a sustainable and impressive development journey:

1993: The first joint stock commercial bank of Ho Chi Minh City opened a branch in Hanoi.

1995: Implemented Bank reform according to advanced management model. This was a turning point that opened an important period of innovation in the development process of Sacombank.

1996: The first bank to issue public shares with a par value of VND 200,000/share to increase charter capital to VND 71 billion with nearly 9,000 shareholders contributing capital.

1997: The Bank was the pioneer in establishing a credit group outside the area (where there was no Sacombank branch): Lai Uyen credit group, Song Be province (currently Binh Duong province) to bring capital to rural areas, contributing to improving the lives of farmers and limiting usury in the economy.

1999: Inauguration of the headquarters building at 278 Nam Ky Khoi Nghia, District 3, Ho Chi Minh City.

2001: Received capital contributions from foreign shareholders. The first was Dragon Financial Holding Group (UK) contributing 10% of charter capital. This capital contribution paved the way for International Finance Corporation (IFC) and ANZ Bank, increasing the equity capital of foreign shareholders to 30% of charter capital.

2002: Established the first subsidiary company - Sacombank Debt Management and Asset Exploitation Company - SBA, initially implementing the strategy of diversifying comprehensive financial service products.

2003: The first bank to be allowed to establish the Vietnam Securities Investment Fund Management Joint Venture Company (VietFund Management - VFM), a joint venture between

Sacombank (holding 51% of charter capital) and Dragon Capital (holding 49% of charter capital).

2004: Signed a contract to deploy the T-24 Corebanking system with Temenos (Switzerland) to improve the quality of operations, management and development of electronic banking services.

2005: Established 8/3 Branch, the first bank model dedicated to women in Vietnam, operating with the mission of advancing modern Vietnamese women.

2006: Being the first joint stock commercial bank in Vietnam to pioneer in listing shares on HOSE with a total listed capital of 1,900 billion VND. At the same time, establishing affiliated companies including: Sacombank-SBR Remittance Company, Sacombank-SBL Financial Leasing Company, Sacombank-SBS Securities Company.

2007: Covering the network of activities in the provinces and cities of the Southwest, Southeast, South Central and Central Highlands.

2008: Built and put into operation the most modern Data Center in the region, established Sacombank-SBJ Gold and Gemstone Company. At the end of 2018, became the first Vietnamese joint stock commercial bank to open a branch in Laos.

2009: Sacombank's STB shares were honored as one of 19 golden shares of Vietnam. Since its official listing on the Ho Chi Minh City Stock Exchange, STB has always been in the group of shares that have received the attention of domestic and foreign investors. In June, opened a branch in Phnom Penh, completed the expansion of the network in the Indochina region, actively contributing to the economic trade of enterprises between the three countries of Vietnam, Laos and Cambodia. In September, officially completed the conversion and upgrade of the core banking system from Smartbank to T24, version R8 at all domestic and foreign transaction points.

2010: Successfully completed the development goals for the period 2001 - 2010 with an average growth rate of 64%/year; at the same time, successfully implemented the restructuring program in parallel with building a solid operating foundation, preparing sufficient resources to successfully implement the development goals for the period 2011 - 2020.

2011: Sacombank established a 100% foreign-owned bank in Cambodia, marking a new phase of development strategy and enhancing Sacombank's operational capacity in Cambodia in particular and the Indochina region in general. On December 20, 2011, Sacombank was honored to receive the Third Class Labor Medal from the President for its outstanding achievements in the period 2006-2010, contributing to the cause of building socialism and defending the Fatherland according to Decision No. 2413/QD-CTN dated December 15, 2011.

2012: Implemented Bank reform according to advanced management model. This was a turning point opening an important period of innovation in Sacombank's development process.

2013: “Best Domestic Bank in Vietnam” and “Best Retail Bank in Vietnam 2013” voted by The Asset Magazine and International Finance Magazine (IFM). These awards have affirmed Sacombank’s prestige, outstanding competitiveness and effective operating strategy over the years.

2014: On March 25, 2014, at the 2014 Annual General Meeting of Shareholders, Sacombank approved the business plan, charter capital increase plan and use of equity capital in 2014; approved the resignation of members of the Board of Directors and the policy for Southern Commercial Joint Stock Bank to merge into Sacombank as well as contents related to operations and management. At the same time, Sacombank cooperated with the international card organization MasterCard to deploy the service of Accepting cards via smartphones (Sacombank mPOS). In order to provide customers with more modern, convenient and safe payment methods, in October 2014, Sacombank officially launched the Sacombank Laos domestic payment card, the Sacombank Laos Visa international payment card and the Sacombank Laos Visa international credit card. 2014 marked