* Regarding the issuance of a copy of the BHTG CNTG: The BHTG TCTG must request the BHTGVN to issue a copy of the BHTG CNTG for posting according to regulations when establishing branches and transaction points that accept deposits.

* Regarding re-issuance of BHTG CNTG: According to current regulations, BHTG depository institutions will be re-issued BHTG CNTG in the following cases: (i) The activity of receiving deposits from individuals is restored; (ii) The BHTG CNTG is lost, torn, or damaged; (iii) The name of the activity changes, including the case of changing the name of the activity when the BHTG depository institution receives a merger.

* Regarding temporary revocation of deposit insurance certificates: Deposit insurance certificates will be temporarily revoked when the State Bank has a document temporarily suspending deposit receiving activities according to the provisions of law.

* Regarding the revocation of the BHTG CNTG: The BHTG TCTG will have its BHTG CNTG revoked when the State Bank issues a document revoking the License to establish and operate in accordance with the provisions of law in case of dissolution, bankruptcy, consolidation or merger.

1.1.3.2. Deposits that are and are not insured

Maybe you are interested!

-

Current status of deposit insurance policy - 3

Current status of deposit insurance policy - 3 -

Vietnam deposit insurance activities after the deposit insurance law - 2

Vietnam deposit insurance activities after the deposit insurance law - 2 -

Issuance and Revocation of Deposit Insurance Participation Certificates

Issuance and Revocation of Deposit Insurance Participation Certificates -

Analysis of Factors Affecting the Amount of Savings Deposits of Individual Customers at Abbank Cai Rang Branch

Analysis of Factors Affecting the Amount of Savings Deposits of Individual Customers at Abbank Cai Rang Branch -

Perfecting Vietnam's deposit insurance law in the current period - 1

Perfecting Vietnam's deposit insurance law in the current period - 1

* Deposits are insured

Insured deposits are deposits in Vietnamese Dong of individuals deposited at the BHTG in the form of term deposits, non-term deposits, savings deposits, deposit certificates, promissory notes, treasury bills and other forms of deposits as prescribed by the Law on Credit Institutions (except for the types of deposits prescribed in Section 3.2.2).

* Deposits are not insured

Deposits at credit institutions of individuals who own more than 5% of the charter capital of that credit institution. Deposits at credit institutions of individuals who are members of the Board of Members, members of the Board of Directors, members of the Supervisory Board, General Director (GD), Deputy General Director (VP) of that credit institution; deposits at foreign bank branches of individuals who are General Directors (GD), Deputy General Directors (VP) of that foreign bank branch. Money to buy anonymous valuable papers issued by the deposit insurance organization.

1.1.3.3. Deposit Insurance Fee

* Concept of Deposit Insurance Premium

Deposit insurance fee is the amount of money that the Deposit Insurance Corporation must pay to the Deposit Insurance Corporation of Vietnam to insure the deposits of insured persons at the Deposit Insurance Corporation. The Prime Minister stipulates.

Deposit insurance fee framework as proposed by the State Bank of Vietnam; The State Bank of Vietnam stipulates specific deposit insurance fee levels for deposit insurance organizations based on the results of assessment and classification of these organizations. Deposit insurance fees are calculated and paid periodically every quarter during the fiscal year, and are accounted for in the operating costs of deposit insurance organizations.

* Insurance premium calculation method

The basis for calculating the deposit insurance premium is the average balance of insured deposits and the deposit insurance premium as prescribed. The average balance of insured deposits is the total average balance of all types of deposits insured by the deposit insurance fund of the quarter preceding the premium collection quarter.

Formula for calculating quarterly insurance premiums (attached appendix)

1.1.3.4. Deposit Insurance Payment

* Time of arising of the obligation to pay insurance

The obligation to pay insurance premiums arises from the time the State Bank of Vietnam issues a document terminating the KSDB or a document terminating the application or not applying the measures to restore solvency while the credit institution being the insured depository institution is still in a state of bankruptcy or the State Bank of Vietnam issues a document determining that the foreign bank branch being the insured depository institution is unable to pay deposits to depositors.

* Insurance payment period

Within 60 days from the date the obligation to pay insurance arises, the deposit insurance organization is responsible for paying insurance money to the insured person.

* Insurance payment limit

The insurance payment limit is the maximum amount that the deposit insurance organization will pay for all insured deposits of a person at a deposit insurance organization when the insurance payment obligation arises. The Prime Minister shall prescribe the insurance payment limit upon the proposal of the State Bank in each period.

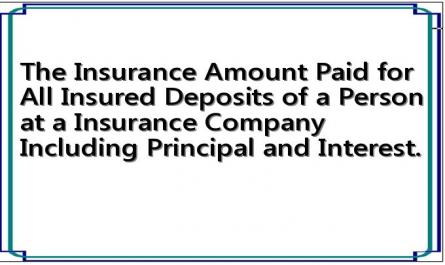

* Amount of insurance paid

1.The insurance amount paid on all insured deposits of a person at a deposit insurance company includes principal and interest.

2.The insurance amount paid in case of multiple joint owners of insured deposits is prescribed as follows:

a) The insurance amount paid for all insured deposits of multiple co-owners at a deposit insurance institution includes principal and interest. The insurance amount paid will be divided according to the agreement of the co-owners; in case there is no agreement or no agreement between the co-owners, the matter will be resolved according to the provisions of law;

b) In case one of the co-owners has another insured deposit at the same BHTG, the total insurance amount paid to a co-owner shall not exceed the insurance payment limit.

3. In case the insured depositor has a debt at the Deposit Insurance Corporation, the insured deposit amount is the remaining amount after deducting that debt.

* Insurance payment procedure

Within 10 working days from the date of the insurance payment obligation, the Deposit Insurance Corporation must send a request for insurance payment to the Deposit Insurance Corporation. The request for insurance payment includes a written request for insurance payment, a list of insured persons, the deposit amount of each insured person and the insurance amount requested to be paid by the Deposit Insurance Corporation. Within 05 working days from the date of receipt of the complete application, the Deposit Insurance Corporation shall examine the documents and books to determine the payment amount. Within 10 working days from the date of completion of the inspection, the Deposit Insurance Corporation must have a plan to pay insurance money to the insured person. Upon receiving the insurance money, the insured person must present original documents proving legal ownership of the insured deposits at the Deposit Insurance Corporation. The Deposit Insurance Organization directly pays insurance money to the insured person or authorizes another Deposit Insurance Organization to do so.

* Handling of deposits exceeding the insurance payment limit

The deposit amount of the insured depositor, including principal and interest, exceeding the insurance payment limit will be resolved during the asset handling process of the Deposit Insurance Corporation according to the provisions of law.

* Recover the insurance amount payable from TCTG BHTG

The Deposit Insurance Organization becomes the creditor of the Deposit Insurance Corporation for the insurance money payable to the insured person from the date of payment of the insurance money. The Deposit Insurance Organization is divided into

Divide the value of the assets in the same order as the depositors and recover the insurance amount payable during the process of handling the assets of the BHTG according to the provisions of law.

1.1.3.5. Inspection and supervision of organizations participating in deposit insurance

* Check TCTG BHTG

The inspection of deposit insurance organizations is one of the most important tasks of the Vietnam Deposit Insurance and has been carried out since its establishment. Regarding the content and scope of inspection according to the Law on Deposit Insurance, the Vietnam Deposit Insurance is responsible for "monitoring and inspecting the implementation of legal regulations on deposit insurance; recommending the State Bank to handle violations of legal regulations on deposit insurance".

On-site inspection activities of BHTGVN contribute to raising awareness of BHTG organizations about BHTG policies, self-consciousness in complying with legal regulations on BHTG and regulations and instructions of BHTGVN.

* TCTG BHTG Supervision

The supervision of deposit-receiving institutions by the deposit insurance organization plays an important role in preventing negative consequences from the collapse of these institutions, and at the same time contributes significantly to limiting moral risks in the operations of deposit-receiving institutions. Currently, the supervision of deposit-receiving institutions is officially legalized and implemented by the State Bank of Vietnam through the Inspection and Supervision Agency under the State Bank of Vietnam. However, this regulation has led to overlaps in the functions of competent agencies in supervising the operations of deposit-receiving institutions.

The monitoring function of the BHTG is to synthesize, analyze and process information about the BHTG to detect and recommend the SBV to promptly handle violations of regulations on banking safety and risks causing insecurity in the banking system. BHTGVN has conducted regular and continuous monitoring of 100% of the

TCTG BHTG. BHTGVN has compiled, analyzed and processed information on TCTG BHTG to detect and recommend the State Bank to promptly handle violations of regulations on safety in banking operations, which pose potential risks to the safety of the banking system. Through monitoring reports, BHTGVN has discovered many cases of credit institutions violating regulations on safety in banking operations, which pose potential risks.

can cause insecurity in the banking system. BHTGVN has sent a report and recommended that the State Bank handle the violations.

1.1.3.6. Operating and investment capital

* BHTG's operating capital

The operating capital of the Vietnam Deposit Insurance includes: The charter capital of the deposit insurance organization provided by the state budget, revenue from deposit insurance fees, revenue from investment activities of the deposit insurance organization's temporarily idle capital, and other revenue sources as prescribed by law.

* Investment activities of deposit insurance

The Deposit Insurance Organization is allowed to use temporarily idle capital to buy government bonds, SBV bills and deposit money at SBV.

1.1.3.7. Participate in special control

Special control is when a credit institution is placed under the direct control of the State Bank due to the risk of insolvency, insolvency or serious violation of the law leading to the risk of unsafe operations. Based on the financial status, level of risk and violation of the law of the credit institution, the State Bank of Vietnam considers and decides to place the credit institution under special supervision or comprehensive control.

1.2. International experience in social insurance

The deposit insurance system in the world continues to play an active role in handling crises and resolving difficulties of the banking system of countries. The legal basis, mechanisms and policies for international deposit insurance activities continue to be strengthened to suit the reality, better protect depositors, maintain trust, and contribute to ensuring the stability of the financial and banking system.

1.2.1. US deposit insurance activities

1.2.1.1. General

The United States is the first country in the world to build a deposit insurance system and has a long history of experience in the field of deposit insurance. After the global economic crisis of 1929-1933, the US economy, like other economies, fell into a severe recession. The US government took measures to restore the economy such as lowering interest rates, providing preferential loans, and subsidizing production. The construction of a national deposit insurance system

is considered a policy to strengthen public confidence, attract idle money to focus on investment and development, and restore the national payment network. Initially, the US deposit insurance system consisted of many separate state-owned deposit insurance funds such as the Deposit Insurance Fund of the Federal Home Loan Bank Council, the Federal Savings and Loan Insurance Corporation, and the Federal Deposit Insurance Corporation. According to US government regulations, all organizations permitted to mobilize deposits must participate in at least one deposit insurance fund.

The Federal Deposit Insurance Corporation (FDIC), established on January 1, 1934, had 13,201 participating banks at the time of FDIC's inauguration, including 12,987 commercial banks (accounting for 90% of the total number of commercial banks in operation) and 214 savings banks (accounting for 36% of the total number of savings banks in operation). FDIC was the first place to implement deposit insurance activities, a typical organization in synchronously implementing three types of operations and maximizing the effectiveness of deposit insurance policies in protecting the interests of depositors, controlling risks in banking activities, and is a model that many countries in the world refer to in establishing and improving deposit insurance activities. The success of deposit insurance policies in the US can be summarized in some of the following highlights:

Firstly, the birth and implementation of the deposit insurance policy in the US has affirmed the great capacity of the deposit insurance policy to control banking risks according to the full functional model: From October 1929 to the end of 1933, the time of birth of the FDIC, there was

4,000 banks failed. During the period from 1934 to 1941, 370 banks closed, but the FDIC created conditions for these banks to withdraw from the banking sector without affecting other banks. During the period from 1982 to 1991, more than 1,400 banks were in a critical situation, which could lead to closure, thanks to the financial support of the FDIC, 131 of these banks overcame the difficulties and maintained their operations.

Second, the interests of depositors are protected in a timely manner, reducing losses for depositors, banks and the economy: From 1934 to 1997, in the US, 2,192 banks failed, which were quickly resolved by the FDIC, minimizing the impact on the US banking system. In the $700 billion financial rescue plan passed by Congress on October 1, 2008, the FDIC raised the deposit insurance limit from $100,000 to $100,000.

USD up to 250,000 USD, to strengthen depositors' confidence in the financial system, FDIC also committed to maintaining the payment level of 250,000 USD long-term, until new regulations are in place.

Third, the US pays much attention to banking supervision: Immediately after its establishment, the FDIC sent 4,000 inspectors to inspect and supervise banks to assess the criteria for FDIC membership.

Fourth, the resources for implementing the deposit insurance policy in the US are invested heavily: there is a strong legal basis (the Deposit Insurance Law) from the beginning and it is adjusted promptly during the implementation process; there are large financial resources and a financial mobilization mechanism that is suitable for the characteristics and important role of the deposit insurance policy in resolving risks in the financial and banking sector; there are large human resources to meet the implementation requirements of the policy. The FDIC's capital is not provided by the budget but is formed from insurance premiums and investment profits in bonds of the Ministry of Finance.

1.2.1.2. FDIC's operating situation

Based on a recent survey by the International Association of Deposit Insurers (IADI), the percentage of deposit insurers that play a significant role in bank resolution increased from approximately 50% in 2005 to nearly 65% in 2011. In the US alone, during the period 2010–2014, the FDIC resolved 342 failed deposit insurers with an estimated loss after resolution of $29,310,206,000 without using the state budget. This demonstrates the important role of effective deposit insurers in the national financial safety net.

* Deposit Insurance Fees: FDIC's fee policy not only establishes a deposit insurance fund to serve

deposit insurance payment service, but also helps improve the business performance of deposit insurance organizations, especially after changing the flat fee to a risk-based fee (1993).

Some important milestones in FDIC's deposit insurance fee policy (attached appendix).

* Inspection and supervision: The objective of the inspection, supervision and early warning function is to promptly detect and handle problems as soon as they arise; determine the priority, scope and frequency of supervision; and intervene before it is too late to minimize risks. To ensure effective supervision, the BHTG system needs to have full, accurate and timely access to information sources from the BHTG TCTG or

through data sharing with other supervisors. In practice, most banking supervisors and deposit insurers operate under a risk mitigation model that uses a combination of qualitative and quantitative methods to identify weak banks that pose a threat to the financial soundness of depository institutions. The United States uses the CAEL supervisory rating system and typically relies on both on-site examination results and off-site analysis of management and other available information, including on-site examination reports. Based on supervisory and market information, the FDIC develops risk detection models (attached), prepares summary analytical reports and other reports, and evaluates the risk ratings of insured depository institutions to rate and take supervisory action against these institutions. In addition, the FDIC collects information on insured depository institutions and coordinates with the federal banking agencies when problems are identified. If the agency fails to take action, the FDIC may take action on its own initiative if necessary.

* FDIC in the Reorganization of Weak Financial Institutions: To protect depositors, the FDIC responds immediately when a bank or thrift fails. These institutions are typically closed by a state regulator or the Office of the Comptroller of the Currency (OCC). The FDIC may choose to resolve a failed institution in a number of ways, but the most common is to sell the failed institution's deposits and liabilities to another institution. The failed institution's customers become customers of the acquiring institution . Most of the time, this transition is done without any disruption to customers.

Figure 1.2.1: Processing and reception timeline (attached appendix)

Figure 1.2.2: FDIC's process for handling failed banks (attached appendix)

The most common restructuring method the FDIC uses:

- Purchase & Assumption (P&A): All deposits or insured deposits are assumed. Additionally, the receiver is encouraged to purchase as many assets as possible, with some exceptions such as non-marketable securities or impaired loans. This approach facilitates the FDIC in the subsequent liquidation process. The FDIC and the receiver share losses. The FDIC accepts a portion of the actual loss on a particular asset class to preserve its value and maintain the asset in the future.