CHAPTER 3: ANALYSIS OF FACTORS AFFECTING THE AMOUNT OF SAVINGS DEPOSITS OF INDIVIDUAL CUSTOMERS AT ABBANK CAI RANG BRANCH

3.1. General information about ABBANK Cai Rang

3.1.1. History of formation and development.

3.1.1.1. History of ABBANK Can Tho.

Can Tho City is the economic center of the Mekong Delta. Located in a region with many favorable conditions, Can Tho City has received a lot of investment from the state such as: Can Tho airport, seaport, industry, export processing zones, ... along with a team of management staff with scientific and technical qualifications from universities in the region and a relatively complete infrastructure system.

With the advantages of Can Tho, on March 7, 2006, ABBANK decided to establish a new branch in Can Tho province, and this is the first level branch of ABBANK in Can Tho province. ABBANK Can Tho is headquartered at 02 Hung Vuong, Thoi Binh Ward, Ninh Kieu District, Can Tho City. Until April 7, 2007, ABBANK Can Tho moved to a new location at 74-76 Hung Vuong, Thoi Binh Ward, Ninh Kieu District, Can Tho City. ABBANK Can Tho currently has 3 affiliated transaction offices: ABBANK An Nghiep, ABBANK O Mon, ABBANK Cai Rang.

3.1.1.2. History of ABBANK Cai Rang establishment.

The headquarters of ABBANK Cai Rang Transaction Office is located at 216, National Highway 1A, Le Binh Ward, Cai Rang District, Can Tho City.

An Binh Commercial Joint Stock Bank - Cai Rang Transaction Office is one of three Transaction Offices of ABBANK Can Tho Branch according to Decision No. 03/2009/QD-HDQT of the Board of Directors.

In 2009, in the context of economic development, banks began to expand their scale, which meant expanding more branches and transaction offices. On May 18, 2009, ABBANK Cai Rang Transaction Office was established. ABBANK Can Tho Branch became a Level 1 Branch Bank.

Since its inception, the Bank has always adhered to the industry's ideology, orientation, and goals such as: credit expansion must be consistent with socio-economic development, credit enhancement must be associated with capital enhancement, ensuring debt management and control, and implementing good corporate culture to enhance the ABBANK brand value.

3.1.2. Organizational chart and structure of ABBANK Cai Rang

The organizational structure shows the management hierarchy in the Bank. The organizational structure of the Bank is arranged in a scientific and reasonable manner, suitable for the scale of the unit, meeting the needs of the work, ensuring that the bank's business activities take place smoothly and effectively.

To understand clearly the working relationships in the unit, the unit's organizational structure is presented in the following diagram:

Manager

Vice president

P. Accounting

P. Relationship

client

Accountant

Fund

CV. Relationship

client

(Source: ABBank Cai Rang)

Figure 3.1: Organizational chart of ABBANK Cai Rang.

Functions and tasks of departments

- Director: directly manages and decides on all bank activities, receives instructions and then instructs bank officers, employees and is responsible before the bank and the law for all his decisions.

- Deputy Director : responsible for assisting the Director in organizing and managing all activities of the Transaction Office. Representing the Director in handling work when the Director is absent (if authorized by the Director).

- Customer relations department :

+ Directly participate in the implementation of credit granting operations of the bank.

+ Appraise loan plans and projects according to credit regulations within the scope of the Director's authorization.

+ Guide customers to apply for loans according to current credit rates

onion

- Accounting and treasury department:

+ Perform accounting work, monitor financial business activities, manage capital and assets, report financial accounting activities according to accounting laws.

+ Closely coordinate with the credit department in managing loan records, debt collection, urging overdue debt collection, ensuring debt collection in accordance with regulations.

+ Guide customers to open accounts, set up procedures to receive and pay TGTK, deposits of economic organizations and individuals.

+ Organize the implementation of payment services, domestic and international money transfers through the ABBank system, NHHN, and other banks in the system. Organize the collection and payment of money, and safely preserve money and assets of the bank and customers.

3.1.3. The bank's business performance in recent times

3.1.3.1. Business performance

Why is it necessary to consider business performance in determining factors affecting customer deposits? Because customers' decisions to deposit money are also influenced by the bank. Thus, if a bank operates effectively, it also demonstrates good management ability and demonstrates the bank's reputation with customers.

Table 3.1: Business performance of ABBank Cai Rang from 2013-2015

Unit: million VND

Target

2013 | 2014 | 2015 | Difference 2014/2013 | Difference 2015/2014 | |||

Amount | % | Amount | % | ||||

1. Total income | 7,236 | 8,929 | 10,768 | 1,693 | 23.4 | 1,839 | 20.6 |

- Interest income | 7.113 | 8,741 | 10,283 | 1,628 | 22.9 | 1,542 | 17.6 |

- Non-interest income | 123 | 188 | 485 | 65 | 52.8 | 297 | 157.9 |

2. Total cost | 6.224 | 7,531 | 8,887 | 1,307 | 20.9 | 1,356 | 23.6 |

- Interest expense | 5,658 | 6,944 | 8,205 | 1,286 | 22.7 | 1,261 | 18.2 |

+ Interest on deposits | 1,646 | 1,826 | 2,067 | 216 | 13.1 | 241 | 13.2 |

+ Transferred interest | 4.012 | 5.118 | 6.138 | 1.106 | 27.6 | 1,020 | 19.9 |

- Non-interest expenses | 566 | 587 | 682 | 21 | 3.7 | 95 | 16.2 |

3. Profit | 1,012 | 1,398 | 1,881 | 386 | 38.1 | 483 | 34.5 |

Maybe you are interested!

-

Testing Factors Affecting Customer Satisfaction With Savings Deposit Services At Dong A Bank

Testing Factors Affecting Customer Satisfaction With Savings Deposit Services At Dong A Bank -

Building a Scale and Research Model of Factors Affecting Customers' Decision to Choose a Bank to Deposit Savings at

Building a Scale and Research Model of Factors Affecting Customers' Decision to Choose a Bank to Deposit Savings at -

Results of Linear Regression Analysis on Factors Affecting Land Complaints in Vinh City

Results of Linear Regression Analysis on Factors Affecting Land Complaints in Vinh City -

Exploratory Factor Analysis (EFA) Results for Factors Affecting Customer Satisfaction

Exploratory Factor Analysis (EFA) Results for Factors Affecting Customer Satisfaction -

Proposing Factors Affecting Customer Satisfaction With Savings Deposit Services At Dong A Bank

Proposing Factors Affecting Customer Satisfaction With Savings Deposit Services At Dong A Bank

Source: Accounting Department of ABBank Cai Rang

12000.0

10000.0

8000.0

6000.0

4000.0

2000.0

.0

7236.0

6224.0

8929.0

7531.0

10768.0

8887.0

Unit: million VND

2013 2014 2015

Income Expenses

Source: Accounting Department of ABBank Cai Rang

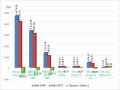

Figure 3.2: Income and expenses of ABBank Cai Rang from 2013 - 2015

Income:

In recent years, the economic situation has had many fluctuations with many adverse impacts on the business activities of commercial banks in general and ABBank Cai Rang in particular. However, with the continuous efforts of the Board of Directors of ABBank Cai Rang and all staff, ABBank Cai Rang has overcome difficulties and achieved quite good results in business activities when the total income item has increased over the years.

In 2013, the bank's total revenue was 7,236 million VND. By the end of 2014, the total revenue had reached 8,929 million VND (an increase of 23.4% compared to 2013). During this period, the bank promptly introduced preferential interest rate policies to support lending to businesses. On the one hand, it helped the bank increase credit growth, on the other hand, it helped businesses overcome difficulties in business, continue to operate, generate income to pay debts and interest to the bank, contributing to limiting overdue debts and bad debts.

In 2015, the economic situation had positive changes, businesses gradually recovered and with good signals, the bank reached 10,768 million VND, an increase of 20.6% compared to 2014. Businesses continued to expand production, so the demand for investment in purchasing machinery, equipment, factories, etc. also increased. In addition, businesses that overcame difficulties became loyal customers of the bank, they made significant contributions to income from credit activities. That achievement was due to the efforts of all transaction office staff, always closely following the market situation to adjust credit activities accordingly to ensure the highest safety and efficiency for all business activities of the bank. In addition, the bank has controlled

Bad debt, the ability to recover principal and interest is increased, also making the bank's income increase significantly.

Cost:

Interest expenses always account for a high proportion of total expenses, most years over 90% because credit activities are the main activities of the bank, so the expenses for credit activities such as paying interest on deposits, paying interest on capital transfers. In which, the cost of paying for capital transferred from branches accounts for a high proportion of interest expenses and increases gradually over the years. Specifically, in 2014, interest transferred from branches was 5,118 million VND, accounting for more than 70% of interest expenses, an increase of 27.6% compared to 2013. Although the bank has strengthened capital mobilization with many positive measures and mobilized capital has increased by 26% compared to 2013, it is still low because depositors have the mentality of depositing in banks with state capital, so capital mobilization is difficult, the bank needs transferred capital to meet lending needs.

In 2015, interest expenses on deposits continued to increase and transfer interest still accounted for a high proportion (74%) and increased by 19.9%, while the cost of paying interest on deposits to customers only increased by 241 million VND, equivalent to 13.2% compared to 2014. Therefore, the bank had to bear a higher transfer interest rate than the interest rate mobilized from customers, which caused annual expenses to increase. The bank can increase capital mobilization from customers with reasonable strategies to reduce the cost of paying interest on money transferred from branches.

Profit:

Although annual costs increase, profits do not decrease. In 2014, ABBank Cai Rang's profit reached 1,398 million VND, an increase of 38.1% compared to 2013. By 2015, profits continued to increase to 438 million VND, reaching 1,881 million VND, an increase of 34.5% compared to 2014. This is an encouraging result and needs to be further promoted. However, this result still has many limitations, high income but costs are a major obstacle, making the actual profits received by the bank insignificant. To overcome this situation, it is necessary to strengthen capital mobilization, attract more capital, idle money with low costs from the population to minimize costs and contribute to increasing profits.

Through the above analysis, we can see that the business performance of ABBank Cai Rang is quite high. To do this, we need to mention the management role of the Branch in general and the Board of Directors of ABBank Cai Rang in particular. Their management ability has helped the bank have appropriate policies and directions in difficult business conditions. In addition, good management will help the bank enhance its reputation in the market. It helps the ABBank Can Tho system create trust from customers as well as partners thanks to

into business strategies to attract customers. Currently, ABBank Cai Rang has a very good deposit relationship with many individuals, demonstrated by the very high amount of deposits over the periods.

3.1.4. Advantages and disadvantages 3.1.4.1.Advantages

ABBANK Can Tho is located in the center of Cai Rang District, where the population density is high, can mobilize many idle capital sources and is very convenient for customers to come and do transactions.

With support from EVN and cooperation from Viettel Military Telecommunications Group, ABBANK has invested heavily in modern technology, developed more convenient products and services for customers, expanded its product range and services along with a dedicated service style to create peace of mind and trust every time customers use ABBANK's services.

The Bank always studies and researches carefully the market demand, customer tastes, and potential customer groups that ABBANK Cai Rang is targeting. At the same time, the Bank also understands the features and utilities of the products it is about to create that are truly suitable for potential customers.

The reputation of ABBANK Cai Rang is increasingly expanded and enhanced. This is the opportunity for the Bank to be known by customers as the brand "An Binh", one of the important tools in establishing relationships and building trust with domestic and foreign customers, whenever customers want to find products and services with the best quality.

On the other hand, the Transaction Office staff is always friendly and supports customers wholeheartedly in transactions, making efforts to improve and update knowledge about ABBANK's new products to satisfy customers when they come to transact here.

3.1.4.2. Difficulties

Unstable prices, inflation as well as instability in the agricultural and aquatic product markets, construction materials, etc. affect the income, ability to accumulate, borrow capital, repay debts and invest in production and business of the majority of people.

On the customer side, the level of education is not high, business is not effective, some customers use capital for the wrong purpose, affecting debt collection.

Market risks increase with financial market liberalization; interest rates, exchange rates and capital account balances are liberalized.

Fierce competition among credit institutions in the same area significantly affects market share and the implementation of target programs and plans of the Bank.

Human resources are easily attracted by other competitors.

3.1.5. Development orientation

By 2020, ABBANK strives to develop in the direction of a multi-functional commercial bank, focusing on retail banking activities, taking customer service and care as the core. ABBANK's motto is high growth but ensuring safe, sustainable and effective development.

ABBANK's operating principles: serving customers with safe, effective and flexible products and services; increasing shareholder benefits; aiming for comprehensive and sustainable development of the bank; investing in human factors as the foundation for long-term development.

ABBANK constantly improves its business organization structure throughout Vietnam, focusing on multi-functional and retail banking business activities; at the same time, it promotes joint venture financial investment activities to ensure maximum profit.

3.1.6. Procedure for performing savings deposit transactions for individual customers

Step 1: Customer requests to open a new account/deposit more money into KKH account.

- The teller receives requests, guides customers to fill out forms, and advises on the sale of savings products and banking services. The teller asks customers to present their identification documents.

+ In case the customer deposits additional money into the KKH account: The sales representative will guide the customer to prepare a deposit slip and present the KKH account.

+ In case the customer opens a new account (CKH account/KKH account): The sales staff will guide the customer in the following 2 ways:

Method 1: Customer creates a deposit slip.

Method 2: The customer creates a deposit statement (if the customer deposits cash) and the transaction officer prints a Savings Deposit Slip on the system in step 6 for the customer to sign and confirm. If the customer is making a transaction for the first time at ABBANK, the transaction officer will instruct the customer to create an additional Account Opening and Service Use Registration Form, photocopy the customer's identification documents to register information and save the file at ABBANK.

Step 2: Check information:

- In case the customer deposits money into the KKH account: The transaction officer checks the validity and accuracy of the information on the KKH account, the customer's documents, identification documents and information on the system.

- In case the customer opens a new account: The transaction officer checks the validity and accuracy of the information on the customer's documents and identification documents.

If there are any errors, discuss with the customer to make adjustments. If correct, proceed to the next step.

The transaction officer continues with step 3 if the customer is making a transaction for the first time, and continues with step 5 if the customer has made a transaction at ABBANK.

Step 3: Perform customer identification referencing the Customer Identification Process (if the customer is transacting for the first time)

Step 4: Customer deposits cash/transfers money from account.

- If the customer deposits cash to open a new account/deposits more money into the customer's account: The transaction officer receives and counts the cash according to the Cash Counting Procedure.

- If the customer transfers money to open a new account/deposits more money into the customer's account: The transaction officer checks the account balance to ensure it is sufficient to carry out the transaction and checks the customer's signature.

Step 5: GDV makes transactions on the system

- The sales representative enters data to create the customer's CIF code on the system (if the customer is transacting with ABBANK for the first time)

- If the customer deposits additional money into the KKH account by cash/transfer: The transaction officer will record a credit to the customer's TGTK account on the system, record the fee (if any), print the document, sign and stamp "Received money"/"Transferred money" on the document. The transaction officer will record the transaction information on the KKH account and transfer it to the controller for approval.

- If the customer opens a new account by cash/transfer: The transaction is made on the system, the customer is asked to sign the Savings Deposit Form (if any), sign and stamp "Received money"/"Transferred money" on the document, the transaction is transferred to the controller and the account is submitted for approval.

- Customer checks and signs the Savings Deposit Form printed from the system (if any)

3.2. Analysis of capital mobilization situation at ABBank Cai Rang

3.2.1. Capital sources of ABBank Cai Rang.

Table 3.2: Capital sources of ABBank Cai Rang from 2013-2015

Unit: million VND

Item

2013 | 2014 | 2015 | Difference 2014/2013 | Difference 2015/2015 | |||

Amount | % | Amount | % | ||||

Capital mobilized | 55,165 | 69,729 | 78,794 | 14,564 | 26 | 9,065 | 13 |

Transferred capital | 113,880 | 129,823 | 144,104 | 15,943 | 14 | 14,281 | 11 |

Total | 169,045 | 199,552 | 222,898 | 30,507 | 18 | 23,346 | 12 |

(Source: Accounting Department of ABBank Cai Rang)