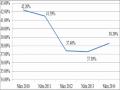

If we look at the debt-to-exports graph (Chart 3.2), the curves have a decreasing slope from left to right, indicating that the graph will go down when it crosses the inflection point. With a = 0.99, the debt-to-exports ratio was held at 0.854 in 2011. This is a completely acceptable level because it is far from the level of unstable debt (debt-to-exports ratio of 2).

2,200

Maybe you are interested!

-

Institutional Framework for Foreign Debt Management in Vietnam

Institutional Framework for Foreign Debt Management in Vietnam -

Scientific basis for perfecting state policies on foreign invested economy (FIE) in Vietnam - 2

Scientific basis for perfecting state policies on foreign invested economy (FIE) in Vietnam - 2 -

Bad Debt Management Vietnam Joint Stock Commercial Bank for Industry and Trade

Bad Debt Management Vietnam Joint Stock Commercial Bank for Industry and Trade -

Strengthening state management by law in the field of road traffic in Vietnam today - 10

Strengthening state management by law in the field of road traffic in Vietnam today - 10 -

Perfecting the interest rate management mechanism of the State Bank of Vietnam in the conditions of a market economy - 30

Perfecting the interest rate management mechanism of the State Bank of Vietnam in the conditions of a market economy - 30

2,000

1,800

1,600

1,400

1,200

1,000

0.800

0.600

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

0.400

Debt-to-export ratio with b = 1, 2006-2011

`

b=1; a=0.88 b=1; a=0.92 b=1; a=0.96 b=1.00; a=0.99

Source: Table 3.3 Debt to Export Ratio, 2006-2011

Figure 3-3 Debt-to-export ratio with b = 1, 2006-2011

Figure 3.3 shows the debt-to-export trend with b = 1 (imports increase at the same rate as exports). In this case, the debt-to-export ratio has a clear increasing trend. Vietnam is a country with a current account that does not include interest rates in a deficit (v 0 > 1), so the debt-to-export ratio does not decrease along the line b = 1. The increase in the debt-to-export ratio

The debt-to-export ratio depends on the increase in the debt-to-export ratio and the export growth rate a. The larger a, the higher the growth rate of debt-to-exports. With interest rates significantly lower than export growth (a = 0.92), even at a = 0.88, the debt-to-export ratio still tends to explode, but not to a large extent and can be contained. Because the initial debt-to-export ratio is low (d 0 = 0.522), the medium-term debt-to-export level is not high. However,

Debt to export ratio with b=1.02, 2006-2011

2,000

1,800

1,600

1,400

1,200

1,000

0.800

0.600

0.400

0.200

-

2006 2007 2008 2009 2010 2011

If interest rates are approximately equal to the rate of increase in exports (a = 0.99), the debt-to-export ratio will increase almost linearly. In 2011, the debt-to-export ratio will be about 1.309.

b=1.02; a=0.88 b=1.02; a=0.92 b=1.02; a=0.96

b=1.02; a=0.99

Source: Table 3.3 Debt to Export Ratio, 2006-2011

Figure 3-4 Debt-to-export ratio with b = 1.02, 2006-2011

With b > 1, the Vietnamese economy will be in Zone 4 of the Jaime De Pinies coordinate system. The debt-to-export ratio tends to increase and explode at a rapid rate.

increasing degree, depending on the magnitude of the ratio of interest rate to export growth a. We will consider two cases, the first case, b=1.02 and the second case, b=1.05. The first case is shown in Figure

3.4 with the debt-to-export ratio graphs all sloping upward. With imports growing about 2% faster than exports (b = 1.02) and interest rates lower than export growth by about 12% (a = 0.88), the initial debt-to-export ratio will more than double after 5 years.

Figure 3.5 shows that if imports grow about 5% faster than exports (b = 1.05) and interest rates are about 12% lower than export growth (a = 0.88), the initial debt-to-export ratio will nearly triple and reach 1.911 after 5 years.

Debt to export ratio with b = 1.05, 2006-2011

3,000

2,500

2,000

1,500

1,000

0.500

2006

2007 2008 2009 2010

b=1.05; a=0.88 b=1.05, a=0.92

b=1.05; a=0.99

b=1.05, a=0.96

2011

Source: Table 3.3 Debt to Export Ratio, 2006-2011

Figure 3-5 Debt-to-export ratio with b = 1.05, 2006-2011

The analysis of the Jaime De Pinies model shows that debt sustainability in Vietnam depends largely on the correlation between import growth and export growth. Vietnam will always ensure its ability to pay in the current conditions if it maintains a lower import growth rate than the export growth rate. Then, the debt-to-export ratio will tend to decrease or be contained in the medium term.

In the case that imports increase at the same rate as exports, Vietnam will become sensitive to changes in interest rates. If interest rates increase to a level that is approximately equal to the export growth rate (a = 0.99), it could lead to a linear increase in debt-to-exports and reach twice its current value by 2011.

Import growth outpacing exports is an undesirable trend because the current account deficit excluding interest rates will accumulate rapidly, worsening short-term solvency. In this case, the debt-to-export ratio tends to explode, especially when interest rates rise close to the growth rate of exports.

Application of Jaime De Pinies model on Vietnam data

The results from the 1995-2005 period show that although the debt-to-export ratio is still low, as a country with a current account that does not include a permanent interest rate deficit, Vietnam needs to maintain an import growth rate that does not exceed the export growth rate to ensure the sustainability of foreign debt in the medium term.

The application of the Jaime De Pinies model shows that using modeling tools will be very useful for assessing and forecasting debt sustainability in Vietnam, and is also completely feasible for debt management agencies.

Conclude

Based on the analysis of the current situation of foreign debt management in Vietnam during the period

In the period 1995-2005, the thesis has proposed a number of suggested solutions to strengthen foreign debt management in Vietnam. The solutions focus on further improving the legal framework and organizational system for foreign debt management in Vietnam, and on continuing to strengthen the capacity of the management staff.

The thesis also proposes to apply the model of assessing the sustainability of foreign debt in Vietnam and apply this model based on foreign debt data for the period 1995-2005 to forecast the sustainability of foreign debt in Vietnam in the medium term (2006-2010), thereby drawing conclusions about the sustainability of foreign debt in Vietnam and proposing import-export policies to ensure the sustainability of foreign debt in Vietnam in the coming period.

The advantage of the Jaime De Pinies model is that it combines factors such as initial debt, interest rates, and import-export growth rates to determine an economy's future debt capacity.

Conclude

For developing countries, foreign loans are an important supplementary resource for economic development and domestic consumption regulation. Foreign loans create opportunities for investment and development at a higher level than domestic savings can provide, while at the same time ensuring current consumption levels of the population, creating conditions for social stability. Developing countries with market economies all choose to borrow from abroad to

investment to develop the economy in the early stages, and repay the debt with domestic savings in the later stages. Borrowing for development is essentially a method of balancing current and future national consumption. Therefore, to borrow from abroad effectively, it is necessary to ensure that current borrowing does not seriously affect the consumption of future generations.

Debt management plays a decisive role in ensuring the effectiveness of foreign borrowing. Debt management includes two types of functions – recording and management. Recording includes controlling loans, collecting debt data, statistical analysis and accounting for debt. Debt management includes planning debt policies, outlining operational strategies to implement those policies, analyzing debt policies and managing risks. If recording is an important type of function in the stage

In the early stages of building a debt management system, management is an essential function for the maturity stage of the debt management system, when the borrowing country can proactively plan and regulate the borrowing programs not only of the Government and the public sector, but also of the large private sector in the market economy.

To manage debt effectively, it is necessary to build effective debt management institutions and mechanisms. The institutional framework stipulates the basic functions of debt management.

how it is allocated to government agencies. The debt management mechanism includes the processes and procedures for control, monitoring, analysis and reporting

so that debt management agencies can ensure the completion of assigned debt management functions.

The foreign debt management system in our country is in the process of formation and development. In recent years, the institutional framework for foreign debt management has been continuously innovated to better meet the requirements of national debt management and to be more consistent with international practice. Currently, the transitional and inconsistent nature of the foreign debt management system is still evident. The parallel existence of regulations on the management of official development assistance (ODA) capital and regulations on foreign debt management in general leads to

to some overlap in the implementation of debt management functions of the Ministry of Finance, the Ministry of Planning and Investment and the State Bank.

The analysis shows that in reality, the current external debt management system only partially performs the debt management functions that a country with a developed market economy needs. In particular, there is no state committee with a unified debt management function for general monitoring. Although exchanges and joint work among ministries assigned to debt management take place regularly, there is a lack of specific official mechanisms to coordinate between ministries and branches assigned to perform different areas of debt management, reducing the ability to cover, unify and update the debt situation. International experience shows that a unified debt management agency is essential to have the capacity to monitor and balance the country's debt.

Assessing the sustainability of foreign debt is an important part of debt management functions. Assessing the sustainability of foreign debt is

assess the ability of the debtor country to meet its debt service obligations in a timely manner. This should be done regularly to anticipate and detect problems early.

debt problems that may arise and timely corrective measures. Debt sustainability analysis can also help the borrowing country to identify the requirements

Excessive regulation by credit providers harms the development of the borrowing country.

Tools to assess debt sustainability can be macroeconomic indicators, debt indicators such as debt to GDP ratio, public debt to GDP ratio, net present value of debt to exports, annual debt service to exports.

Analysis of Vietnam's foreign debt situation shows that

Up to now, debt indicators are in a favorable area. The total debt to GDP ratio in 2005 was about 32%, lower than that in 1995 (35%). Of which, public debt accounts for over 80% of total foreign debt. Compared to the practice of countries in the world and the assessments of multilateral organizations, this debt to GDP ratio is not high.

The net present value (NPV) of debt to GDP is estimated at around 70%, equal to the average of developing countries in the region.

The East Asia and Pacific region is well below the average for all developing countries. Thanks to strong export growth, the debt-to-export ratio has fallen from around 17% in 1995 to 6% in 2005.

The Jaime De Pinies model is a tool for assessing the debt sustainability of a borrowing country over a given period. By using the characteristics of the balance of payments to forecast the debt-to-export ratio, the model is useful in analyzing the sensitivity of the borrowing country to changes in external conditions such as interest rates, changes in terms of exports and imports, and other changes that affect the growth of imports and exports. The model shows the importance of current account deficits

for the debt repayment capacity of the borrowing country while allowing to determine an allowable deficit level to be able to develop domestically and still ensure the ability to pay before credit suppliers.