Table 4.4. Cost of equity of the parent company - PVN

and the Group's level 1 member enterprises as of December 31, 2012

STT

Business | Equity Cost (*) | |

1 | Parent company - PVN | 11.04% |

2 | DK Exploration and Exploitation Corporation | 11.04% |

3 | Binh Son Refining and Petrochemical Company | 10.33% |

4 | PM Chemicals and Fertilizer Corporation | 10.73% |

5 | Vietnam Gas Corporation | 10.25% |

6 | Vietnam Oil Corporation | 10.50% |

7 | Vietnam Electricity Corporation | 10.25% |

8 | DK Technical Services Corporation | 10.53% |

9 | DK Drilling and Drilling Services Corporation | 10.58% |

10 | DK General Services Corporation | 10.60% |

11 | Oil and Gas Transport Corporation | 10.89% |

12 | Oil and Gas Design Consulting Corporation | 10.86% |

13 | DK Energy Technology Corporation | 10.60% |

14 | Petec Trading and Investment Corporation | 10.50% |

15 | Drilling Fluids and Petroleum Chemicals Corporation | 10.82% |

16 | Oil and Gas Construction Corporation | 11.33% |

17 | Oil and Gas Insurance Corporation | 10.21% |

18 | Dung Quat Shipbuilding Industry Company Limited | 11.22% |

Maybe you are interested!

-

Table Showing the Ratio of Dprr/Total Bad Debt of Branches in the Period 2012 - 2014

Table Showing the Ratio of Dprr/Total Bad Debt of Branches in the Period 2012 - 2014 -

Medium and Long-Term Credit Structure on Total Outstanding Debt in the 2009-2011 Period

Medium and Long-Term Credit Structure on Total Outstanding Debt in the 2009-2011 Period -

Some Key Solutions to Promote Positive Changes and Limit Negative Changes of Socialist Production Relations in

Some Key Solutions to Promote Positive Changes and Limit Negative Changes of Socialist Production Relations in -

Some solutions to limit risks in international goods trading activities of Vietnamese traders - 10

Some solutions to limit risks in international goods trading activities of Vietnamese traders - 10 -

Limiting social insurance debt of businesses by applying sanctions Case study of businesses in Thanh Xuan district, Hanoi city - 12

Limiting social insurance debt of businesses by applying sanctions Case study of businesses in Thanh Xuan district, Hanoi city - 12

(Source: Author's calculation from financial statements of enterprises belonging to the Vietnam National Petroleum Group)

c) Determine the exact cost of borrowing (kd)

Simply put, businesses are currently calculating the cost of borrowing capital in a fairly simple way, including: costs paid to financial institutions or costs paid for issuing bonds. However, there are two issues to note regarding this type of cost: First, businesses must calculate the full "cost of borrowing capital - all in cost" and not just "interest payable". For example, for loans from banks, in addition to interest payable, there are also other types of costs such as consulting fees, legal consulting fees in drafting contracts, due diligence costs for loans.

borrowing..., for bond issuance, the costs other than bond interest are also very large such as: business credit rating costs, issuance underwriting fees, issuance consulting costs, legal consulting costs... Second, the cost of borrowing is not fixed when the level of borrowing of the enterprise increases, in other words, when: (i) the scale of borrowing increases or (ii) the capital structure changes in the direction of increasing the debt/equity ratio, the cost of borrowing will also increase because the lender will bear more risk. At that time, with the cost of borrowing increasing to the level of (kd + ∆) due to the increased risk level of the enterprise due to using more debt, the average cost of capital of the enterprise will be:

WACC = * (kd + ∆)(1-t) + * ke

Thus, for the cost of borrowed capital, determining the exact cost of capital is quite simple compared to the cost of equity capital, but it is necessary to calculate all costs other than interest. At the same time, the cost of borrowed capital is not always fixed for all mobilized capital, but it will increase when the enterprise uses more debt and when it exceeds the optimal capital structure, it will make the cost of capital of the enterprise increase when the cost of borrowed capital increases due to the use of more debt exceeding the tax savings due to the use of that debt.

4.3.1.2. Recommend a method to determine the “safe limit” of capital structure in determining the optimal capital structure

In theory, the capital structure of a business is optimal when: “ PV of tax shield ” = “Cost of financial distress” (“Cost of financial distress ”) at which time the cost of capital of the enterprise is the smallest (WACC min) and the enterprise value is the largest. However, in practice, up to now, no work has quantified the present value of the cost of financial distress. Therefore, to determine the optimal capital structure, in addition to determining the minimum cost of capital of the enterprise, the author recommends applying the “Z-Score” method 3 to determine the capital structure in which the debt ratio is the maximum without the enterprise facing the risk of bankruptcy.

(* Z - Score bankruptcy risk detection tool: Finding a tool to detect signs of bankruptcy has always been one of the top concerns.

of corporate finance researchers. Many tools have been developed to do this. Among them, the Z-index is the most widely recognized and used tool in the world by both academics and practitioners. This index was invented by Professor Edward I. Altman, Leonard N. Stern School of Business, New York University, based on a fairly elaborate study of many different companies in the US. Although this Z-index was invented in the US, most countries can still use it with a fairly high level of reliability. From the original Z-index , Professor Edward I. Altman developed Z' and Z” to be applied to each type and industry of business. The Z-index includes 5 indexes X1, X2, X3, X4, X5: (i) X1 = Working Capitals/Total Assets ratio; (ii) X2 = Retain Earnings/Total Assets; (iii) X3 = Earnings Before Interest and Taxes/Total Assets; (iv) X4 = Market Value of Total Equity / Book values of total Liabilities; (v) X5= Sales/Total Assets. In which the Z'' index can be used for most industries and types of businesses. Because of the large difference in X5 between industries, X5 has been introduced. The formula for calculating the Z'' index is adjusted as follows

Z'' = 6.56x1 + 3.26x2 + 6.72x3 + 1.05x4

If Z'' > 2.6, the enterprise is in the safe zone, not at risk of bankruptcy; If 1.2 < Z'' < 2.6, the enterprise is in the warning zone with risk of bankruptcy; If Z <1.2, the enterprise is in the dangerous zone, at high risk of bankruptcy.) 3 .

Applying this method, to keep the business in the safe zone with no risk of bankruptcy Z” ≥ 2.6, with the coefficients x1, x2, x3 of the business, business operators can determine the maximum Equity/Debt ratio to ensure the business is “safe” from the coefficient x4 = market value of equity/book value of total debt.

Total Debt / Market Value of Equity ≤

For joint stock enterprises, the value of equity is equal to the market value of equity/market price of 1 share. For 100% state-owned enterprises, the market value of equity is equal to the book value of equity.

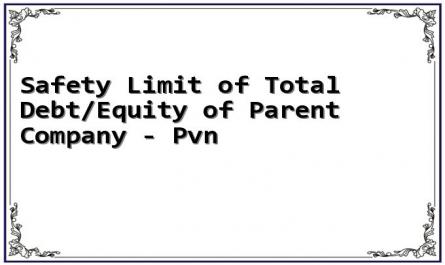

Table 4.5. Safe “limit” of Total Debt/Equity of Parent Company - PVN

and level 1 member enterprises of the Group according to the Z-Score method as of December 31, 2012

Business | (Total debt/Value of assets) VCSH) maximum | (Total Debt/Equity) max | |

1 | Parent company - PVN | 4.44 | 4.44 |

2 | DK Exploration and Exploitation Corporation | 3.56 | 3.56 |

3 | Binh Son Refining and Petrochemical Company | 0.56 | 0.56 |

4 | PM Chemicals and Fertilizer Corporation | 0.58 | 2.06 |

5 | Vietnam Gas Corporation | 0.51 | 1.95 |

6 | Vietnam Oil Corporation | 0.64 | 0.64 |

7 | Vietnam Electricity Corporation | 2.92 | 2.92 |

8 | DK Technical Services Corporation | 0.81 | 1.10 |

9 | DK Drilling and Drilling Services Corporation | 0.58 | 2.16 |

10 | DK General Services Corporation | 1.69 | 2.11 |

11 | Oil and Gas Transport Corporation | 1.02 | 0.42 |

12 | Oil and Gas Design Consulting Corporation | 1.57 | 1.23 |

13 | DK Energy Technology Corporation | 0.71 | 0.71 |

14 | Petec Trading and Investment Corporation | 0.31 | 0.31 |

15 | Drilling Fluids and Petroleum Chemicals Corporation | 4.00 | 5.19 |

16 | Oil and Gas Construction Corporation | 0.34 | 0.18 |

17 | Oil and Gas Insurance Corporation | 2.99 | 4.54 |

18 | Shipbuilding Industry Company Limited Dung Quat | 0.13 | 0.13 |

(Source: Author's calculation from financial reports of enterprises under

(TĐDKQGVN)

4.3.2. Group of support solutions

4.3.2.1. Solutions to impact factors affecting the capital structure of enterprises

a. Changing the awareness and attitude of business leaders (CEO, CFO) about capital structure and capital restructuring. Training and improving the qualifications of staff in general and the qualifications of management staff and financial staff in particular.

Among the factors that determine the success of the capital restructuring process in enterprises, the role of the head of the enterprise is particularly important. For enterprises belonging to the Vietnam National Oil and Gas Group, the results of the test of factors affecting capital structure have shown that "CEO's attitude" is a factor closely related to the capital structure of the enterprise. If the CEO is not willing or does not like to use borrowed capital, then the capital structure of that enterprise will certainly be difficult to reach the optimal capital structure due to the ratio of borrowed capital/equity being too low, or in other words, with the mentality of not accepting the risks brought about by debt or "fear" of borrowing capital, the enterprise will mainly rely on the owner's capital, which has limited the enterprise's capital, limited investment opportunities to expand production and business, and at the same time, stripped away the "tax shield" advantage of borrowed capital, causing the enterprise to pay higher capital costs and the ultimate consequence is to reduce the efficiency of the enterprise's operations. With limited awareness of the optimal capital structure, many business leaders have not seriously raised the issue of the enterprise's capital structure, but the habit is that when there is a need for capital, they will look for sources of capital to finance, first of all, calling for state shareholders' capital according to the mechanism of asking - giving, subsidy. Besides business leaders who are afraid of borrowing capital, afraid of risks when borrowing capital and relying too much on shareholder capital as they did on state capital in the past, some business leaders are too easygoing when borrowing capital and using borrowed capital regardless of safety limits. All of these problems are caused by the awareness and understanding of business leaders about capital structure and the importance of building a capital structure.

The optimal capital structure in corporate financial management is still limited, inaccurate and incomplete. This is also a historical limitation, the fact that the Group's enterprises were previously too dependent on the parent company, which is essentially the State capital, has created a mentality of dependence, not paying attention to planning and actively mobilizing capital of business leaders. This reality requires that the capital restructuring process at the enterprises of the Vietnam National Oil and Gas Group, in order to take place successfully, must first of all renew the awareness and thinking of the leadership team of the enterprises, especially the CEOs and CFOs, about the optimal capital structure, at the same time, new theories on modern financial management and capital management also need to be updated for the leadership team of enterprises in the Group to improve understanding of capital structure and capital restructuring towards optimizing capital structure. In addition, training and improving the qualifications of staff in general and the qualifications of management staff and financial staff in particular is an urgent requirement so that the capital restructuring process can be successfully implemented in practice.

b. Develop risk management policies and improve the enterprise's risk management capabilities and capabilities.

The optimal capital structure will be achieved when the value of the company is the largest, that is, the cost of capital is at the lowest level and thus maximizes the company's profits. In theory, the more debt capital a business uses, the lower the cost of capital will be because the business benefits from the "tax shield". However, there is another principle that the value of a business using debt capital, although it will be increased by tax deductions, will bear financial risk, which will increase with the debt ratio. The value of the business will increase to a certain threshold, then gradually decrease due to increasing financial risk. So, to put it simply, financial risk is an obstacle in the process of the business reaching the optimal capital structure, or in other words, one of the important criteria for an optimal capital structure is that it must be consistent with the policy, level and risk management capacity of the business. Therefore, a strategic solution determines the success of the capital restructuring process at the Group's enterprises.

Vietnam National Oil and Gas Group is that enterprises must necessarily build for themselves a risk management policy and at the same time improve the level and ability of financial risk management of the enterprise. Only then will increasing debt to change the capital structure, towards an optimal capital structure to maximize the value of the enterprise not have to pay the price of risks, financial collapse, liquidity... For Vietnamese economic groups, the case of Vinashin Shipbuilding Industry Group is a valuable lesson about the problem of the ability and level of risk control not meeting the requirements while the proportion of debt is too large in the capital structure of the enterprise, combined with inefficiency in investment, spread out investment... has led to the collapse of a large economic group of the country.

First of all, in terms of awareness, it must be agreed that risk management is determining the level of risk that the enterprise desires, identifying the current level of risk that the enterprise is currently bearing and using derivatives or other financial instruments to adjust the target level of risk that the enterprise desires. Within the scope of risk management solutions for the capital restructuring process of enterprises belonging to the Oil and Gas Group, the author focuses on recommending that enterprises focus on managing risks related to financial risks with the implication of managing financial distress risk states (i.e. risks from factors such as interest rates, exchange rates, commodity prices, securities affecting the income of enterprises) and risks due to enterprises using financial leverage - borrowed capital in production and business activities through a system of tools such as swaps (including interest rate swaps, currency swaps, securities swaps, commodity swaps, etc.), tools to control and manage the liquidity, solvency, etc. of enterprises.

c. Promoting stable growth and development in business scale Between stable growth, development in business scale and restructuring

Capital success has a two-way relationship, on the one hand businesses aim for structure

Optimal capital is to ensure that businesses develop and grow effectively, stably and sustainably, but at the same time, the capital restructuring process will be carried out more easily and smoothly in businesses with growth and scale.

large scale. In recent years, besides the enterprises of the Group that have always maintained a fast and stable growth rate, many enterprises, due to the impact of the recession and the difficulties of the economy in general and the issue of corporate governance itself, have had almost no growth, or have increased in scale but the operating efficiency is too low, with many potential risks (a manifestation of hot growth and spread investment). Therefore, one of the important prerequisites for enterprises in the Vietnam National Oil and Gas Group to successfully restructure capital is to promote stable growth and development in scale of enterprises.

d. Develop business development orientation and strategy in a focused and closely linked direction with the Group's main production and business areas.

In addition to innovating and rearranging enterprises in the whole Group towards focusing on the Group's main production and business fields, each enterprise in the Group itself needs to identify and rebuild its own strategic development orientation towards closely following and linking with the Group's main production and business fields. That means that enterprises need to divest capital from projects, production and business activities outside the main business fields of the enterprise. In the past few years, many enterprises of the Group, although operating in the Group's 5 main production and business fields, still had projects and investment activities outside such as real estate, finance, banking, securities, etc., or service enterprises that did not focus all their resources on the oil and gas service field but developed non-traditional services, services unrelated to the Group's main production and business fields. These limitations have not only led to extremely serious consequences such as resource dispersion, inefficient investment and operation, but also greatly affected the capital structure of enterprises because accessing loans for investment projects outside the main field is relatively difficult, affecting the reputation and brand of enterprises.

4.3.2.2. Solutions on business administration

a. Establish and enhance the role and operational efficiency of the Group's investment capital management and business unit in enterprises.

The model of a department to manage and operate the Group's investment capital in member enterprises with capital contributions from the Group is a strategic solution for the management of the Group's capital - State capital invested in enterprises. At the same time, the operation of this department also creates motivation and mandatory conditions for enterprises receiving investment capital from the Group to use capital effectively, with the cost of State capital as well as capital of other shareholders must be calculated correctly, fully, accurately reflecting the expected rate of return of the Group as a shareholder when investing capital in enterprises. In addition to the function of managing the Group's investment capital in enterprises, ensuring that the investment capital is fully collected, this department has a particularly important function, which is that at each point in time, depending on the performance of the enterprises (the efficiency of capital investment brought to the Group), depending on the strategy and development orientation of each field of operation of the enterprises in the Group and especially depending on the conditions of the financial market and the stock market, it decides to invest more capital in enterprises or reduce investment capital through flexibly increasing or decreasing the holding ratio in enterprises. This move by the Group's investment capital management and business department, on the one hand, creates pressure on enterprises to improve the efficiency of capital use, thereby maximizing the profitability of State capital, and on the other hand, forces enterprises to be fully aware of their capital structure. The accuracy and transparency in calculating the cost of State equity capital puts pressure on enterprises to build an optimal capital structure to minimize capital costs, maximize enterprise value and be proactive in planning and mobilizing capital for the enterprise. Therefore, in the process of restructuring capital at enterprises under the Vietnam National Oil and Gas Group in terms of the organizational structure of the Group, establishing and enhancing the role and operational efficiency of the Group's investment capital management and trading department in enterprises is a strategic and extremely necessary solution.

b. Develop and comply with the enterprise's capital structure planning process

- Alternative investment - Expansion investment - Modernization - Cut investment | ||

Decision Budget | ||

For the capital restructuring process at enterprises of the Oil and Gas Group to be successful, one of the solutions is that enterprises need to establish and comply with a capital structure planning process for the enterprise. The capital structure planning process is a chain that includes many stages and steps from deciding on the budget according to investment needs, production and business needs; designing the target capital structure, determining the impact of capital costs, dividend payment policies on the target capital structure; determining the feasibility of mobilizing capital sources (internal capital sources, external capital sources, shareholder capital, etc.); determining the impact of the target capital structure on risks, on profits, etc., thereby establishing the optimal capital structure, the ultimate goal of which is enterprise value.

- Internal capital needs

- External loan capital

- N/c additional equity capital issued to Shareholders

winter outside

Generate demand fundraising | |

Existing capital structure

Target capital structure design

Dividend payment policy

Capital structure design

Impact on profits

Enterprise Value

Impact on risk

Target capital structure design

Impact on capital expenditure - WACC

Capital Structure Planning Process Flow Chart

c. Investing in science and technology, improving technical facilities at enterprises

The capital restructuring process is a very difficult and complicated process, because in essence this is a process of perfecting the financial management and administration mechanism of the enterprise, so for this process to be successful, in addition to human factors, mechanism factors... it is necessary to have the support of a system of system management software, advanced technology solutions. Currently at the Vietnam National Oil and Gas Group, a few enterprises are starting to deploy the ERP (Enterprise Resource Planning) system to strengthen system management, improve the efficiency of enterprise resources, including capital resources. However, this implementation is only in a few enterprises and has just begun, to have a complete and effective ERP system requires a huge investment in both human resources and costs, especially the commitment and determination of the enterprise's leaders. Building a target capital structure for a business requires quantitative calculations based on a system of financial statistics over a long period of time in the past, and also requires financial forecasts in the future... and also requires running forecasting models, economic models with complex variables, so it will be very difficult to succeed without the support of modern technical facilities (both software and hardware). Therefore, investing in science, technology, and improving technical facilities at the business is an urgent requirement that determines the success of the business's capital restructuring.

4.3.3. Debt restructuring solution group

4.3.3.1. Improve access to and diversify channels for mobilizing long-term loans

One of the factors that determines the success of the capital restructuring process at enterprises under the Vietnam National Oil and Gas Group is to ensure the “feasibility” in achieving the optimal capital structure. That is, along with determining the optimal capital structure - the target capital structure, the problem of enterprises

It is necessary to have effective solutions to mobilize loan capital to achieve that optimal capital structure. As analyzed in the current capital mobilization situation of enterprises under the Vietnam National Oil and Gas Group, the mobilization of loans and capital mobilization channels of enterprises are still very limited, leading to the situation where the capital structure of enterprises is still unreasonable and not optimal. Therefore, improving the ability to access and diversify long-term loan mobilization channels is one of the leading solutions to ensure the success of the capital restructuring process at enterprises under the Vietnam National Oil and Gas Group. To do so, first of all, enterprises need to be healthy and transparent in their financial situation, improve the efficiency of their operations, only then will the ability to access loan capital of enterprises be improved. On the other hand, enterprises cannot depend on a few sources of capital, a form, a channel for mobilizing loans, but must diversify sources of capital, forms of capital and channels of capital mobilization. In the current context, enterprises under the Oil and Gas Group only borrow capital from banks (mainly domestic banks, accounting for nearly 60%) in the form of commercial loans (accounting for nearly 85% in the loan structure), depending too much on conventional commercial loans from domestic banks with limited capacity (mainly short-term capital), small scale is extremely disadvantageous for expanding and increasing loans, especially long-term loans in the capital structure of enterprises. Therefore, in order to diversify channels and forms of capital mobilization, enterprises under the Oil and Gas Group must have a serious strategy, a long-term program with methodical steps in mobilizing loan sources for enterprises.

Regarding the capital mobilization channel from credit institutions, expanding and promoting borrowing from foreign credit institutions is mandatory for enterprises in the context of very limited capital sources from domestic banks. On the other hand, in addition to the traditional form of borrowing, which is commercial borrowing, it is necessary to choose and develop other forms of borrowing from international banks depending on the situation and characteristics of each enterprise and each investment project that needs to borrow capital.