+ Ratio of outstanding loans to total deposits (%)

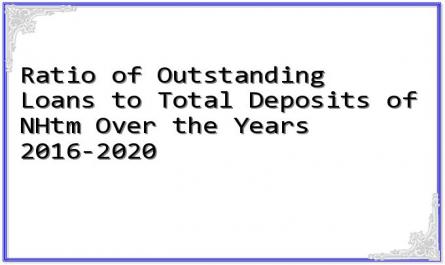

Table 3.10. Ratio of outstanding loans to total deposits of commercial banks over the years 2016-2020

Unit: %

2016 | 2017 | 2018 | 2019 | 2020 | |

Vietinbank | 88.0 | 88.34 | 87.96 | 88.10 | 86.10 |

BIDV | 80.8 | 81.78 | 86.00 | 87.95 | 86.98 |

Vietcombank | 67.9 | 68.87 | 70.57 | 72.41 | 73.45 |

Agribank | 83.7 | 84.01 | 87.86 | 85.76 | 83.33 |

Maybe you are interested!

-

Outstanding Debt and Proportion of Outstanding Debt for Personal Loans at Joint Stock Commercial Bank for Foreign Trade of Vietnam - Thanh Xuan Branch

Outstanding Debt and Proportion of Outstanding Debt for Personal Loans at Joint Stock Commercial Bank for Foreign Trade of Vietnam - Thanh Xuan Branch -

Credit risk management for personal loans at Nam A Commercial Joint Stock Bank - Quang Ninh Branch - 13

Credit risk management for personal loans at Nam A Commercial Joint Stock Bank - Quang Ninh Branch - 13 -

Completing the appraisal of loans for additional working capital for corporate customers at Vietnam Joint Stock Commercial Bank for Industry and Trade - Dong Anh Branch - 5

Completing the appraisal of loans for additional working capital for corporate customers at Vietnam Joint Stock Commercial Bank for Industry and Trade - Dong Anh Branch - 5 -

Proportion of Highly Liquid Assets Before and After Deducting Loans from State Bank and Commercial Banks in the Market of Some Commercial Banks

Proportion of Highly Liquid Assets Before and After Deducting Loans from State Bank and Commercial Banks in the Market of Some Commercial Banks -

Quality of corporate customer loans at Saigon Thuong Tin Commercial Joint Stock Bank - Bac Ninh Branch - 13

Quality of corporate customer loans at Saigon Thuong Tin Commercial Joint Stock Bank - Bac Ninh Branch - 13

Source: Annual reports of credit institutions from 2016-2020

The ratio of outstanding loans to total deposits of Vietcombank from 2016-2020 tended to increase over the assessment periods, from 67.9% in 2016 to 73.45% in 2020. In 2020, this ratio reached 73.45% and was at the lowest level among the 4 state-owned commercial banks. BDV was at the top, followed by Vietinbank, Agribank, and Vietcombank.

+ Bad debt ratio

In the 10 years from 2010 to 2020, Vietcombank's bad debt ratio tended to decrease sharply, from 2.83% in 2010 to 0.62% in 2020. In terms of credit quality, Vietcombank's bad debt ratio from 2017-2020 was the lowest among the four banks mentioned above, with the bad debt ratio in 2020 being 0.62%.

One of the factors that helps Vietcombank achieve a low bad debt ratio is the improved quality of appraisal work and the selection of customers with good financial and business capacity to grant credit. Vietcombank's credit scale is the lowest among the four state-owned joint stock commercial banks, Vietcombank's bad debt ratio is low, leading to Vietcombank's bad debt scale being the lowest among the four banks.

Thus, Vietcombank's credit quality has been improved for 10 consecutive years. From 2017 to present, Vietcombank's bad debt ratio is the lowest.

Table 3.11. Bad debt ratio of commercial banks over the years 2010-2020

Bad debt

Vietcombank | AGRB | BIDV | VTB | |

2010 | 2.83 | 3.75 | 3.00 | 0.66 |

2011 | 2.03 | 6.10 | 2.96 | 0.75 |

2012 | 2.40 | 5.80 | 2.90 | 1.35 |

2013 | 2.73 | - | 2.37 | 0.82 |

2014 | 2.31 | 4.46 | 2.03 | 0.90 |

2015 | 1.79 | 2.01 | 1.68 | 0.73 |

2016 | 1.46 | 1.89 | 1.99 | 0.93 |

2017 | 1.11 | 1.54 | 1.62 | 1.13 |

2018 | 0.97 | 1.51 | 1.90 | 1.60 |

2019 | 0.78 | 1.46 | 1.75 | 1.20 |

2020 | 0.62 | 1.66 | 1.54 | 0.85 |

Source: Annual reports of credit institutions from 2010-2020

Conclusion: Through financial indicators and assessment of competitiveness in the past years 2014 - 2020, it shows that Vietcombank has had a very high breakthrough growth. However, in terms of capital scale, assets, mobilization and lending, Vietcombank still ranks behind in the group of state-owned commercial banks and is higher than most of the remaining private commercial banks. Vietcombank's Car safety ratio is at the top of the group of 4 state-owned commercial banks but is still lower than some joint-stock commercial banks. In terms of credit quality, Vietcombank's bad debt is very low, asset quality is assessed as good.

3.2.2. Network operations

Leading in the number of branches among the four state-owned commercial banks is Agribank with about 940 type 1 and type 2 branches. However, unlike the model of other joint stock commercial banks, Agribank classifies branches differently. If in other commercial banks, the model is divided as follows: Head office, branch, transaction offices under the branch. However, at Agribank, the model is different as follows: Head office, type 1 branch, type 2 branch and transaction offices under this branch.

Table 3.12. Network of commercial banks' branches over the years 2014 - 2020

Year

VIETCOMBANK | AGRIBANK | BIDV | VIETINBANK | |||||

Quantity | Increase growth (%) | Quantity | Increase growth (%) | Quantity | Increase growth (%) | Quantity | Increase growth (%) | |

2014 | 89 | 940 | 135 | 149 | ||||

2015 | 96 | 8 | 940 | 0.0 | 182 | 35 | 149 | 0 |

2016 | 101 | 5 | 942 | 0.2 | 190 | 4 | 155 | 4 |

2017 | 101 | 0 | 942 | 0.0 | 190 | 0 | 155 | 0 |

2018 | 106 | 5 | 946 | 0.4 | 190 | 0 | 155 | 0 |

2019 | 111 | 5 | 940 | -0.6 | 190 | 0 | 155 | 0 |

2020 | 116 | 5 | -100.0 | 190 | 0 | 155 | 0 | |

Source: Annual reports of credit institutions for the years 2014 - 2020. BIDV ranks second in terms of branch network system with 190 domestic and foreign branches. Vietinbank ranks third with 155 branches. Finally

same as Vietcombank with 116 branches.

Vietcombank is the bank with the least number of branches and transaction offices of the above 4 commercial banks. However, Vietcombank's growth rate in the number of branches is the highest. On average, in recent years, the number of Vietcombank branches has increased by about 5%/year. This shows that Vietcombank still has a lot of room for growth and Vietcombank's business results are favorable to be licensed to add more branches and transaction offices.

Among the 4 State-owned commercial banks mentioned above, Vietcombank is the bank with the lowest number of branches and transaction offices. Along with that, the number of employees of Vietcombank is also the lowest among the 4 banks above. However, the scale of profit of Vietcombank is the highest among the 4 banks, therefore, the working efficiency per employee of Vietcombank is the highest among the 4 commercial banks above, even leading among commercial banks in Vietnam.

Table 2.13. Profitability based on number of employees of 4 commercial banks

Unit: billion VND

STT

Bank | Quantity staff | Benefits before tax | Proportion Profit before tax/employee | |

1 | Vietcombank | 20,062 | 23,044 | 1,149 |

2 | Vietinbank | 24,480 | 17,070 | 0.697 |

3 | BIDV | 26,752 | 9,213 | 0.344 |

4 | Agribank | 37,738 | 12,896 | 0.342 |

Source: 2020 Financial Reports of Commercial Banks

As of December 31, 2020, Vietcombank's total number of employees reached 20,062, the lowest among the four state-owned commercial banks. However, Vietcombank's pre-tax profit in 2020 ranked first among the four commercial banks, reaching VND 23,044 billion. Vietcombank's pre-tax profit per employee reached VND 1,149 million/employee, ranking first in efficiency among the four banks. Vietinbank ranked second with 24,480 employees and VND 697 million/employee - in 2020. BIDV and Agribank ranked third and fourth with efficiency of VND 344 million and VND 342 million.

3.2.3 Products and services

In Vietnam, commercial banks are classified into two main groups: State-owned commercial banks and private commercial banks. State-owned commercial banks include Vietcombank, Vietinbank, BIDV, Agribank, typical private commercial banks are VPB, TCB, ACB, Sacombank, SHB, etc. The products and services between these two groups of commercial banks are also different. Some typical differences between these two groups of commercial banks are as follows:

Table 3.14. Comparison of strengths and weaknesses of the two banking groups

State-owned commercial banks | Remaining joint stock commercial banks | |

Strengths | - Lower lending interest rates, high interest rate support. More competitive foreign exchange rates. - Large financial potential, providing enough capital for large projects, so the strength is that SP finances projects - High quality human resources. | - Payment service is free for customers, attracting many customers to make transactions. - Fast and convenient transaction processing time - Simple and convenient SPDV implementation procedures - High mobilization interest rates, especially terms over 6 months, do not violate the ceiling interest rate of the State Bank. - Young staff, dynamic, high pressure |

Limit | - Long transaction processing time, through many steps - SPDV still depends a lot on people, the level of processing through IT systems is even lower. - There are still many procedures, not convenient compared to joint stock banks - Low interest rates | - Loan interest rates are often higher than those of state-owned commercial banks. - Foreign currency sources are not as diverse as those of large commercial banks, and commercial products are less competitive. - Limited network of commercial banks comparison of four state-owned commercial banks |

Source: Author's synthesis

From the above product and service characteristics, the business performance of these two banking groups will be differentiated according to the product and service characteristics. Accordingly, the group of state-owned commercial banks will usually have a higher proportion of income from credit activities than the group of private-owned commercial banks. On the contrary, the group

Commercial banks with private capital often have a higher proportion of income from service activities than the remaining group.

* Compare Vietcombank and TCB

VCB is in the group of joint stock commercial banks with State capital, so it also has the strengths and weaknesses of these two groups of banks. To clarify, the author would like to take data from two typical banks representing the two groups, Vietcombank and TCB. Data from 2010 - 2020, specifically as follows:

Table 3.15. Vietcombank's income structure from 2010-2020

Unit: %

Vietcombank

2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | |

Net interest income | 71.1 | 83.5 | 72.6 | 69.5 | 68.0 | 72.9 | 74.5 | 74.6 | 72.3 | 75.6 | 73.9 |

Net profit/loss from operations DV | 12.3 | 10.2 | 9.1 | 10.4 | 10.2 | 8.8 | 8.5 | 8.6 | 8.7 | 9.4 | 13.5 |

Net profit/loss from business forex and gold | 4.9 | 7.9 | 9.9 | 9.2 | 7.8 | 7.4 | 7.4 | 6.9 | 5.8 | 7.4 | 8.0 |

Net gain/loss from purchase sell CKKD | 0.2 | 0.0 | 0.5 | 0.1 | 1.2 | 0.8 | 2.0 | 1.6 | 0.6 | 0.3 | 0.0 |

Net gain/loss from purchase sell investment securities | 2.3 | 0.2 | 1.4 | 1.0 | 1.3 | 0.8 | -0.4 | -0.1 | 0.0 | 0.0 | 0.0 |

Net profit/loss from operations other | 5.0 | -8.5 | 3.5 | 6.0 | 10.3 | 9.0 | 7.7 | 7.1 | 8.2 | 6.7 | 3.7 |

Income from contributions capital, stock purchase | 4.3 | 6.7 | 3.1 | 3.6 | 1.2 | 0.2 | 0.3 | 1.1 | 4.4 | 0.5 | 0.9 |

Total | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 |

Source: Vietcombank Annual Report

In the 10 consecutive years from 2010-2020, the proportion of Vietcombank's net interest income tended to fluctuate between 68% -73.9%. In recent years, the proportion of net interest income has tended to increase, in 2020 this segment reached 73.9% of total annual income. Vietcombank's service income in 10 years has improved significantly, increasing from 12.3% in 2010 to 13.5% in 2020. In 2020, service income increased significantly compared to 2019, increasing from 9.4% to 13.5%. The trend of reducing dependence on income from credit activities, increasing income from

Service activities are the trend of many banks today in Vietnam and around the world.

Table 3.16. Techcombank's income structure from 2010-2020

Unit: %

TCB

2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | |

Interest income pure | 67.5 | 79.5 | 88.8 | 76.8 | 81.2 | 77.1 | 68.3 | 54.6 | 60.6 | 67.7 | 69.3 |

Net profit/loss from DV | 19.7 | 17.3 | 9.8 | 13.0 | 15.8 | 12.2 | 16.4 | 23.3 | 19.3 | 15.4 | 15.5 |

Net profit/loss from foreign business money and gold | -1.9 | -10.5 | -2.4 | -2.2 | 0.3 | -2.1 | 2.0 | 1.7 | 1.3 | 0.5 | 0.0 |

Net profit/loss from sales CKKD | -1.5 | -0.8 | 0.0 | 1.9 | 1.4 | 3.2 | 1.0 | 2.4 | 0.9 | 1.9 | 1.2 |

Net profit/loss from sales Investment securities | 3.4 | 6.2 | -3.0 | 2.8 | 1.1 | -1.6 | 4.0 | 5.2 | 4.1 | 5.9 | 5.5 |

Net profit/loss from other contracts | 11.2 | 8.2 | 6.3 | 7.3 | 0.1 | 11.0 | 8.2 | 10.5 | 8.9 | 8.6 | 8.4 |

Income from contribute capital, buy shares | 1.7 | 0.1 | 0.5 | 0.3 | 0.1 | 0.1 | 0.0 | 2.2 | 4.9 | 0.0 | 0.0 |

Total | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 |

Source: Techcombank Annual Report

Activities from trading, securities investment, capital contribution and share purchase have a smaller proportion than the two main segments above and tend to decrease over the years. The total proportion of the remaining segments outside the two core business segments in 2010 was 16.7%, decreasing to 12.6% in 2020. Thus, over the past 10 years, Vietcombank has shifted its income structure towards increasing the proportion of interest income and service income segments. Of which, service income tends to increase the fastest. Vietcombank aims to transform itself towards a modern retail bank, fully meeting the needs of customers for products and services.

In the recent period, TCB has shown that it is a young bank with

strong growth in market share and profit. TCB was established in 1993, after 28 years of formation and development, TCB has shown impressive achievements, currently TCB is known as the private joint stock commercial bank with the largest profit scale in Vietnam. TCB's products have many outstanding advantages and are highly competitive with state-owned commercial banks. One of TCB's outstanding products is payment products with attractive incentives for customers such as free interbank transfers, free card issuance, free annual credit card fees, free ATM withdrawals, etc. TCB's main target customers are the individual customer segment, focusing on the priority customer segment. The goal of TCB's payment policies is to increase the source of non-term deposits for the bank (also known as casa) and increase market share, promote products to customers.

Vietnam Technological and Commercial Joint Stock Bank (TCB), in 10 consecutive years from 2010 to 2020, the income structure has changed in a trend, slightly increasing the proportion of net interest income, decreasing the proportion of income from services. However, in 2020, the structure of income from net interest and service activities of TCB was 69.3% and 15.5% respectively. Compared with the income structure of VCB, the income structure of TCB has a lower proportion of net interest than Vietcombank and a higher proportion of income from service activities than Vietcombank.

TCB's strong product and direction is to expand the scale and proportion of the service sector. In 2020, TCB's proportion of service income was higher than Vietcombank's, the proportion of service income of TCB and Vietcombank was 15.5% and 13.5% respectively. Thus, TCB's competitive product against state-owned commercial banks in general and Vietcombank in particular is payment products. Through the structure of income proportion of Vietcombank and TCB, we can see this more clearly.

* Compare Vietcombank and BIDV

In the group of state-owned commercial banks, products