- Force majeure events occurring in the natural environment such as drought, flood, fire affect production and business activities, income of customers and banks, thereby reducing the credit quality of commercial banks.

The above are the main factors that affect the quality of TDCN. To manage TD quality, we need to clearly understand the above factors, along with correctly assessing the quality of TDCN, in order to come up with highly feasible solutions.

1.3.4 Indicators for assessing personal credit quality

Maybe you are interested!

-

Credit quality assessment at the Bank for Agriculture and Rural Development, North Song Huong branch, Thua Thien Hue province - 1

Credit quality assessment at the Bank for Agriculture and Rural Development, North Song Huong branch, Thua Thien Hue province - 1 -

Indicators for Assessing the Quality of Short-Term Credit Activities of Banks

Indicators for Assessing the Quality of Short-Term Credit Activities of Banks -

Evaluation of personal credit service quality of Dong A Commercial Joint Stock Bank - Hue Branch - 9

Evaluation of personal credit service quality of Dong A Commercial Joint Stock Bank - Hue Branch - 9 -

Assessment of Credit Scale and Quality for SMEs at Branches of Vietnam Bank for Agriculture and Rural Development in Ho Chi Minh City Through the Model

Assessment of Credit Scale and Quality for SMEs at Branches of Vietnam Bank for Agriculture and Rural Development in Ho Chi Minh City Through the Model -

Identify Rating Levels and Rating Scales

zt2i3t4l5ee

zt2a3gstourism,quan lan,quang ninh,ecology,ecotourism,minh chau,van don,geography,geographical basis,tourism development,science

zt2a3ge

zc2o3n4t5e6n7ts

of the islanders. Therefore, this indicator will be divided into two sub-indicators:

a1. Natural tourism attractiveness a2. Cultural tourism attractiveness

b. Tourist capacity

The two island communes in Quan Lan have different capacities to receive tourists. Minh Chau Commune is home to many standard hotels and resorts, attracting high-income domestic and international tourists. Meanwhile, Quan Lan Commune has many motels mainly built and operated by local people, so the scale and quality are not high, and will be suitable for ordinary tourists such as students.

c. Time of exploitation of Quan Lan Island Commune:

Quan Lan tourism is seasonal due to weather and climate conditions and festivals only take place on certain days of the year, specifically in spring. In Quan Lan commune, the period from April to June and from September to November is considered the best time to visit Quan Lan because the cultural tourism activities are mainly associated with festivals taking place during this time.

Minh Chau island commune:

Tourism exploitation time is all year round, because this is a place with a number of tourist attractions with diverse ecosystems such as Bai Tu Long National Park Research Center, Tram forest, Turtle Laying Beach, so besides coming to the beach for tourism and vacation in the summer, Minh Chau will attract research groups to come for tourism combined with research at other times of the year.

d. Sustainability

The sustainability of ecotourism sites in Quan Lan and Minh Chau communes depends on the sensitivity of the ecosystems to climate changes.

landscape. In general, these tourist destinations have a fairly high level of sustainability, because they are natural ecosystems, planned and protected. However, if a large number of tourists gather at certain times, it can exceed the carrying capacity and affect the sustainability of the environment (polluted beaches, damaged trees, animals moving away from their habitats, etc.), then the sustainability of the above ecosystems (natural ecosystems, human ecosystems) will also be affected and become less sustainable.

e. Location and accessibility

Both island communes have ports to take tourists to visit from Van Don wharf:

- Quan Lan – Van Don traffic route:

Phuc Thinh – Viet Anh high-speed boat and Quang Minh high-speed boat, depart at 8am and 2pm from Van Don to Quan Lan, and at 7am and 1pm from Quan Lan to Van Don. There are also wooden boats departing at 7am and 1pm.

- Van Don - Minh Chau traffic route:

Chung Huong high-speed train, Minh Chau train, morning 7:30 and afternoon 13:30 from Van Don to Minh Chau, morning 6:30 and afternoon 13:00 from Minh Chau to Van Don.

f. Infrastructure

Despite receiving investment attention, the issue of infrastructure and technical facilities for tourism on Quan Lan Island is still an issue that needs to be resolved because it has a direct impact on the implementation of ecotourism activities. The minimum conditions for serving tourists such as accommodation, electricity, water, communication, especially medical services, and security work need to be given top priority. Ecotourism spots in Minh Chau commune are assessed to have better infrastructure and technical facilities for tourism because there are quite complete and synchronous conditions for serving tourists, meeting many needs of domestic and foreign tourists.

3.2.1.4. Determine assessment levels and assessment scales

Corresponding to the levels of each criterion, the index is the score of those levels in the order of 4, 3, 2, 1 decreasing according to the standard of each level: very attractive (4), attractive (3), average (2), less attractive (1).

3.2.1.5. Determining the coefficients of the criteria

For the assessment of DLST in the two communes of Quan Lan and Minh Chau islands, the students added evaluation coefficients to show the importance of the criteria and indicators as follows:

Coefficient 3 with criteria: Attractiveness, Exploitation time. These are the 2 most important criteria for attracting tourists to tourism in general and eco-tourism in particular, so they have the highest coefficient.

Coefficient 2 with criteria: Capacity, Infrastructure, Location and accessibility . Because the assessment area is an island commune of Van Don district, the above criteria are selected by the author with appropriate coefficients at the average level.

Coefficient 1 with criteria: Sustainability. Quan Lan has natural and human-made ecotourism sites, with high biodiversity and little impact from local human factors. Most of the ecotourism sites are still wild, so they are highly sustainable.

3.2.1.6. Results of DLST assessment on Quan Lan island

a. Assessment of the potential for natural tourism development

For Minh Chau commune:

+ Natural tourism attractiveness is determined to be very attractive (4 points) and the most important coefficient (coefficient 3), so the score of the Attractiveness criterion is 4 x 3 = 12.

+ Capacity is determined as average (2 points) and the coefficient is quite important (coefficient 2), then the score of Capacity criterion is 2 x 2 = 4.

+ Exploitation time is long (4 points), the most important coefficient (coefficient 3) so the score of the Exploitation time criterion is 4 x 3 = 12.

+ Sustainability is determined as sustainable (4 points), the important coefficient is the average coefficient (coefficient 1), so the score of the Sustainability criterion is 4 x 1 = 4 points

+ Location and accessibility are determined to be quite favorable (2 points), the coefficient is quite important (coefficient 2), the criterion score is 2 x 2 = 4 points.

+ Infrastructure is assessed as good (3 points), the coefficient is quite important (coefficient 2), then the score of the Infrastructure criterion is 3 x 2 = 6 points.

The total score for evaluating DLST in Minh Chau commune according to 6 evaluation criteria is determined as: 12 + 4 + 12 + 4 + 4 + 6 = 42 points

Similar assessment for Quan Lan commune, we have the following table:

Table 3.3: Assessment of the potential for natural ecotourism development in Quan Lan and Minh Chau communes

Attractiveness of self-tourismof course

Capacity

Mining time

Sustainability

Location and accessibility

Infrastructure

Result

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

CommuneMinh Chau

12

12

4

8

12

12

4

4

4

8

6

8

42/52

Quan CommuneLan

6

12

6

8

9

12

4

4

4

8

4

8

33/52

b. Assessment of the potential for humanistic tourism development

For Quan Lan commune:

+ The attractiveness of human tourism is determined to be very attractive (4 points) and the most important coefficient (coefficient 3), so the score of the Attractiveness criterion is 4 x 3 = 12.

+ Capacity is determined to be large (3 points) and the coefficient is quite important (coefficient 2), then the score of the Capacity criterion is 3 x 2 = 6.

+ Mining time is average (3 points), the most important coefficient (coefficient 3) so the score of the Mining time criterion is 3 x 3 = 9.

+ Sustainability is determined as sustainable (4 points), the important coefficient is the average coefficient (coefficient 1), so the score of the Sustainability criterion is 4 x 1 = 4 points.

+ Location and accessibility are determined to be quite favorable (2 points), the coefficient is quite important (coefficient 2), the criterion score is 2 x 2 = 4 points.

+ Infrastructure is rated as average (2 points), the coefficient is quite important (coefficient 2), then the score of the Infrastructure criterion is 2 x 2 = 4 points.

The total score for evaluating DLST in Quan Lan commune according to 6 evaluation criteria is determined as: 12 + 6 + 6 + 4 + 4 + 4 = 36 points.

Similar assessment with Minh Chau commune we have the following table:

Table 3.4: Assessment of the potential for developing humanistic eco-tourism in Quan Lan and Minh Chau communes

Attractiveness of human tourismliterature

Capacity

Mining time

Sustainability

Location and accessibility

Infrastructure

Result

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Quan CommuneLan

12

12

6

8

9

12

4

4

4

8

4

8

39/52

Minh CommuneChau

6

12

4

8

12

12

4

4

4

8

6

8

36/52

Basically, both Minh Chau and Quan Lan localities have quite favorable conditions for developing ecotourism. However, Quan Lan commune has more advantages to develop ecotourism in a humanistic direction, because this is an area with many famous historical relics such as Quan Lan Communal House, Quan Lan Pagoda, Temple worshiping the hero Tran Khanh Du, ... along with local festivals held annually such as the wind praying ceremony (March 15), Quan Lan festival (June 10-19); due to its location near the port and long exploitation time, the beaches in Quan Lan commune (especially Quan Lan beach) are no longer hygienic and clean to ensure the needs of tourists coming to relax and swim; this is also an area with many beautiful landscapes such as Got Beo wind pass, Ong Phong head, Voi Voi cave, but the ability to access these places is still very limited (dirt hill road, lots of gravel and rocks), especially during rainy and windy times; In addition, other natural resources such as mangrove forests and sea worms have not been really exploited for tourism purposes and ecotourism development. On the contrary, Minh Chau commune has more advantages in developing ecotourism in the direction of natural tourism, this is an area with diverse ecosystems such as at Rua De Beach, Bai Tu Long National Park Conservation Center...; Minh Chau beach is highly appreciated for its natural beauty and cleanliness, ranked in the top ten most beautiful beaches in Vietnam; Minh Chau commune is also home to Tram forest with a large area and a purity of up to 90%, suitable for building bridges through the forest (a very effective type of natural ecotourism currently applied by many countries) for tourists to sightsee, as well as for the purpose of studying and researching.

Figure 3.1: Thenmala Forest Bridge (India) Source: https://www.thenmalaecotourism.com/(August 21, 2019)

3.2.2. Using SWOT matrix to evaluate Quan Lan island tourism

General assessment of current tourism activities of Quan Lan island is shown through the following SWOT matrix:

Table 3.5: SWOT matrix evaluating tourism activities on Quan Lan island

Internal agent

Strengths- There is a lot of potential for tourism development, especially natural ecotourism and humanistic ecotourism.- The unskilled labor force is relatively abundant.- resource environmentunpolluted, still

Weaknesses- Poorly developed infrastructure, especially traffic routes to tourist destinations on the island.- The team of professional staff is still weak.- Tourism products in general

quite wild, originalintact

general and DLST in particularalone is monotonous.

External agents

Opportunity- Tourism is a key industry in the socio-economic development strategy of the province and Van Don economic zone.- Quan Lan was selected as a pilot area for eco-tourism development within the framework of the green growth project between Quang Ninh province and the Japanese organization JICA.- The flow of tourists and especially ecotourism in the world tends toincreasing

Challenge- Weather and climate change abnormally.- Competition in tourism products is increasingly fierce, especially with other localities in the province such as Ha Long, Mong Cai...- Awareness of tourists, especially domestic tourists, about ecotourism and nature conservation is not high.

Through summary analysis using SWOT matrix we see that:

To exploit strengths and take advantage of opportunities, it is necessary to:

- Diversify products and service types (build more tourism routes aimed at specific needs of tourists: experiential tourism immersed in nature, spiritual cultural tourism...)

- Effective exploitation of resources and differentiated products (natural resources and human resources)

div.maincontent .p { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; } div.maincontent p { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; } div.maincontent .s1 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 13pt; } div.maincontent .s2 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 13pt; } div.maincontent .s3 { color: #0D0D0D; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s4 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s5 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s6 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; vertical-align: -3pt; } div.maincontent .s7 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; vertical-align: -2pt; } div.maincontent .s8 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; vertical-align: -1pt; } div.maincontent .s9 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s10 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s11 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s12 { color: black; font-family:Symbol, serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s13 { color: black; font-family:Wingdings; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s14 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; vertical-align: 5pt; } div.maincontent .s15 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; vertical-align: 5pt; } div.maincontent .s16 { color: black; font-family:Cambria, serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s17 { color: #080808; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s18 { color: #080808; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s19 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 11pt; } div.maincontent .s20 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10pt; } div.maincontent .s21 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 11pt; } div.maincontent .s22 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 11pt; } div.maincontent .s23 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s24 { color: #212121; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; tex

Identify Rating Levels and Rating Scales

zt2i3t4l5ee

zt2a3gstourism,quan lan,quang ninh,ecology,ecotourism,minh chau,van don,geography,geographical basis,tourism development,science

zt2a3ge

zc2o3n4t5e6n7ts

of the islanders. Therefore, this indicator will be divided into two sub-indicators:

a1. Natural tourism attractiveness a2. Cultural tourism attractiveness

b. Tourist capacity

The two island communes in Quan Lan have different capacities to receive tourists. Minh Chau Commune is home to many standard hotels and resorts, attracting high-income domestic and international tourists. Meanwhile, Quan Lan Commune has many motels mainly built and operated by local people, so the scale and quality are not high, and will be suitable for ordinary tourists such as students.

c. Time of exploitation of Quan Lan Island Commune:

Quan Lan tourism is seasonal due to weather and climate conditions and festivals only take place on certain days of the year, specifically in spring. In Quan Lan commune, the period from April to June and from September to November is considered the best time to visit Quan Lan because the cultural tourism activities are mainly associated with festivals taking place during this time.

Minh Chau island commune:

Tourism exploitation time is all year round, because this is a place with a number of tourist attractions with diverse ecosystems such as Bai Tu Long National Park Research Center, Tram forest, Turtle Laying Beach, so besides coming to the beach for tourism and vacation in the summer, Minh Chau will attract research groups to come for tourism combined with research at other times of the year.

d. Sustainability

The sustainability of ecotourism sites in Quan Lan and Minh Chau communes depends on the sensitivity of the ecosystems to climate changes.

landscape. In general, these tourist destinations have a fairly high level of sustainability, because they are natural ecosystems, planned and protected. However, if a large number of tourists gather at certain times, it can exceed the carrying capacity and affect the sustainability of the environment (polluted beaches, damaged trees, animals moving away from their habitats, etc.), then the sustainability of the above ecosystems (natural ecosystems, human ecosystems) will also be affected and become less sustainable.

e. Location and accessibility

Both island communes have ports to take tourists to visit from Van Don wharf:

- Quan Lan – Van Don traffic route:

Phuc Thinh – Viet Anh high-speed boat and Quang Minh high-speed boat, depart at 8am and 2pm from Van Don to Quan Lan, and at 7am and 1pm from Quan Lan to Van Don. There are also wooden boats departing at 7am and 1pm.

- Van Don - Minh Chau traffic route:

Chung Huong high-speed train, Minh Chau train, morning 7:30 and afternoon 13:30 from Van Don to Minh Chau, morning 6:30 and afternoon 13:00 from Minh Chau to Van Don.

f. Infrastructure

Despite receiving investment attention, the issue of infrastructure and technical facilities for tourism on Quan Lan Island is still an issue that needs to be resolved because it has a direct impact on the implementation of ecotourism activities. The minimum conditions for serving tourists such as accommodation, electricity, water, communication, especially medical services, and security work need to be given top priority. Ecotourism spots in Minh Chau commune are assessed to have better infrastructure and technical facilities for tourism because there are quite complete and synchronous conditions for serving tourists, meeting many needs of domestic and foreign tourists.

3.2.1.4. Determine assessment levels and assessment scales

Corresponding to the levels of each criterion, the index is the score of those levels in the order of 4, 3, 2, 1 decreasing according to the standard of each level: very attractive (4), attractive (3), average (2), less attractive (1).

3.2.1.5. Determining the coefficients of the criteria

For the assessment of DLST in the two communes of Quan Lan and Minh Chau islands, the students added evaluation coefficients to show the importance of the criteria and indicators as follows:

Coefficient 3 with criteria: Attractiveness, Exploitation time. These are the 2 most important criteria for attracting tourists to tourism in general and eco-tourism in particular, so they have the highest coefficient.

Coefficient 2 with criteria: Capacity, Infrastructure, Location and accessibility . Because the assessment area is an island commune of Van Don district, the above criteria are selected by the author with appropriate coefficients at the average level.

Coefficient 1 with criteria: Sustainability. Quan Lan has natural and human-made ecotourism sites, with high biodiversity and little impact from local human factors. Most of the ecotourism sites are still wild, so they are highly sustainable.

3.2.1.6. Results of DLST assessment on Quan Lan island

a. Assessment of the potential for natural tourism development

For Minh Chau commune:

+ Natural tourism attractiveness is determined to be very attractive (4 points) and the most important coefficient (coefficient 3), so the score of the Attractiveness criterion is 4 x 3 = 12.

+ Capacity is determined as average (2 points) and the coefficient is quite important (coefficient 2), then the score of Capacity criterion is 2 x 2 = 4.

+ Exploitation time is long (4 points), the most important coefficient (coefficient 3) so the score of the Exploitation time criterion is 4 x 3 = 12.

+ Sustainability is determined as sustainable (4 points), the important coefficient is the average coefficient (coefficient 1), so the score of the Sustainability criterion is 4 x 1 = 4 points

+ Location and accessibility are determined to be quite favorable (2 points), the coefficient is quite important (coefficient 2), the criterion score is 2 x 2 = 4 points.

+ Infrastructure is assessed as good (3 points), the coefficient is quite important (coefficient 2), then the score of the Infrastructure criterion is 3 x 2 = 6 points.

The total score for evaluating DLST in Minh Chau commune according to 6 evaluation criteria is determined as: 12 + 4 + 12 + 4 + 4 + 6 = 42 points

Similar assessment for Quan Lan commune, we have the following table:

Table 3.3: Assessment of the potential for natural ecotourism development in Quan Lan and Minh Chau communes

Attractiveness of self-tourismof course

Capacity

Mining time

Sustainability

Location and accessibility

Infrastructure

Result

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

CommuneMinh Chau

12

12

4

8

12

12

4

4

4

8

6

8

42/52

Quan CommuneLan

6

12

6

8

9

12

4

4

4

8

4

8

33/52

b. Assessment of the potential for humanistic tourism development

For Quan Lan commune:

+ The attractiveness of human tourism is determined to be very attractive (4 points) and the most important coefficient (coefficient 3), so the score of the Attractiveness criterion is 4 x 3 = 12.

+ Capacity is determined to be large (3 points) and the coefficient is quite important (coefficient 2), then the score of the Capacity criterion is 3 x 2 = 6.

+ Mining time is average (3 points), the most important coefficient (coefficient 3) so the score of the Mining time criterion is 3 x 3 = 9.

+ Sustainability is determined as sustainable (4 points), the important coefficient is the average coefficient (coefficient 1), so the score of the Sustainability criterion is 4 x 1 = 4 points.

+ Location and accessibility are determined to be quite favorable (2 points), the coefficient is quite important (coefficient 2), the criterion score is 2 x 2 = 4 points.

+ Infrastructure is rated as average (2 points), the coefficient is quite important (coefficient 2), then the score of the Infrastructure criterion is 2 x 2 = 4 points.

The total score for evaluating DLST in Quan Lan commune according to 6 evaluation criteria is determined as: 12 + 6 + 6 + 4 + 4 + 4 = 36 points.

Similar assessment with Minh Chau commune we have the following table:

Table 3.4: Assessment of the potential for developing humanistic eco-tourism in Quan Lan and Minh Chau communes

Attractiveness of human tourismliterature

Capacity

Mining time

Sustainability

Location and accessibility

Infrastructure

Result

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Quan CommuneLan

12

12

6

8

9

12

4

4

4

8

4

8

39/52

Minh CommuneChau

6

12

4

8

12

12

4

4

4

8

6

8

36/52

Basically, both Minh Chau and Quan Lan localities have quite favorable conditions for developing ecotourism. However, Quan Lan commune has more advantages to develop ecotourism in a humanistic direction, because this is an area with many famous historical relics such as Quan Lan Communal House, Quan Lan Pagoda, Temple worshiping the hero Tran Khanh Du, ... along with local festivals held annually such as the wind praying ceremony (March 15), Quan Lan festival (June 10-19); due to its location near the port and long exploitation time, the beaches in Quan Lan commune (especially Quan Lan beach) are no longer hygienic and clean to ensure the needs of tourists coming to relax and swim; this is also an area with many beautiful landscapes such as Got Beo wind pass, Ong Phong head, Voi Voi cave, but the ability to access these places is still very limited (dirt hill road, lots of gravel and rocks), especially during rainy and windy times; In addition, other natural resources such as mangrove forests and sea worms have not been really exploited for tourism purposes and ecotourism development. On the contrary, Minh Chau commune has more advantages in developing ecotourism in the direction of natural tourism, this is an area with diverse ecosystems such as at Rua De Beach, Bai Tu Long National Park Conservation Center...; Minh Chau beach is highly appreciated for its natural beauty and cleanliness, ranked in the top ten most beautiful beaches in Vietnam; Minh Chau commune is also home to Tram forest with a large area and a purity of up to 90%, suitable for building bridges through the forest (a very effective type of natural ecotourism currently applied by many countries) for tourists to sightsee, as well as for the purpose of studying and researching.

Figure 3.1: Thenmala Forest Bridge (India) Source: https://www.thenmalaecotourism.com/(August 21, 2019)

3.2.2. Using SWOT matrix to evaluate Quan Lan island tourism

General assessment of current tourism activities of Quan Lan island is shown through the following SWOT matrix:

Table 3.5: SWOT matrix evaluating tourism activities on Quan Lan island

Internal agent

Strengths- There is a lot of potential for tourism development, especially natural ecotourism and humanistic ecotourism.- The unskilled labor force is relatively abundant.- resource environmentunpolluted, still

Weaknesses- Poorly developed infrastructure, especially traffic routes to tourist destinations on the island.- The team of professional staff is still weak.- Tourism products in general

quite wild, originalintact

general and DLST in particularalone is monotonous.

External agents

Opportunity- Tourism is a key industry in the socio-economic development strategy of the province and Van Don economic zone.- Quan Lan was selected as a pilot area for eco-tourism development within the framework of the green growth project between Quang Ninh province and the Japanese organization JICA.- The flow of tourists and especially ecotourism in the world tends toincreasing

Challenge- Weather and climate change abnormally.- Competition in tourism products is increasingly fierce, especially with other localities in the province such as Ha Long, Mong Cai...- Awareness of tourists, especially domestic tourists, about ecotourism and nature conservation is not high.

Through summary analysis using SWOT matrix we see that:

To exploit strengths and take advantage of opportunities, it is necessary to:

- Diversify products and service types (build more tourism routes aimed at specific needs of tourists: experiential tourism immersed in nature, spiritual cultural tourism...)

- Effective exploitation of resources and differentiated products (natural resources and human resources)

div.maincontent .p { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; } div.maincontent p { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; } div.maincontent .s1 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 13pt; } div.maincontent .s2 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 13pt; } div.maincontent .s3 { color: #0D0D0D; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s4 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s5 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s6 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; vertical-align: -3pt; } div.maincontent .s7 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; vertical-align: -2pt; } div.maincontent .s8 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; vertical-align: -1pt; } div.maincontent .s9 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s10 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s11 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s12 { color: black; font-family:Symbol, serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s13 { color: black; font-family:Wingdings; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s14 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; vertical-align: 5pt; } div.maincontent .s15 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; vertical-align: 5pt; } div.maincontent .s16 { color: black; font-family:Cambria, serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s17 { color: #080808; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s18 { color: #080808; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s19 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 11pt; } div.maincontent .s20 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10pt; } div.maincontent .s21 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 11pt; } div.maincontent .s22 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 11pt; } div.maincontent .s23 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s24 { color: #212121; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; tex

1.3.4.1 From the banking perspective

Group of indicators on loan sales and debt collection sales of science and technology

- Personal customer loan sales

This indicator reflects the amount of money that the bank has disbursed to lend to the business during a certain period of time, regardless of whether the loan has been recovered or not. DSCV is usually determined by month, quarter, year, it shows the scale, the trend of expanding or narrowing the business. Depending on the characteristics, potential of the bank, the economic situation to make reasonable comments.

DSCVCN in the period = DNCN at the end of the period + DSTNCN in the period - DNCN at the beginning of the period

- Personal customer debt collection turnover

This turnover reflects the amount of money that the Bank collects from customers who have borrowed capital from the Bank. High debt collection turnover shows that the Bank's debt collection ability is good as well as the customer's debt repayment situation is bright.

DSTNCN in the period = DNCN at the beginning of the period + DSSCVCN in the period - DNCN at the end of the period

Personal credit balance indicators

- Personal credit balance

Is the debt lent to KHCN but not yet collected, this amount is within the loan term is called the outstanding debt within the loan term, outside the loan term is called the overdue debt. This indicator reflects the expansion in scale of personal credit activities.

Ending debt balance = Beginning debt balance + Period's total debt balance - Period's total debt balance

- Personal credit growth rate

TDCN growth rate = (DNCN next period - DNCN previous period)/DNCN previous period

- If this ratio >1: personal credit balance has growth. The larger this ratio is, the larger the personal credit scale is.

- If this ratio = 1: credit scale of the next period is the same as the previous period

- If this ratio <1: credit scale in the next period will narrow compared to the previous period.

- Personal credit balance ratio

CN debt

KHCN debt ratio =

Total outstanding credit

This ratio reflects the proportion of outstanding loans of the bank in total outstanding loans of the bank. The higher this ratio, the larger the scale of outstanding loans of the bank.

Overdue debt indicators

Overdue debt of a customer is the amount of money that the customer borrows but does not pay or has not been able to pay when the payment deadline comes, if the bank director does not allow the debt to be extended.

- Overdue debt ratio:

Overdue debt

Overdue debt ratio =

Total outstanding credit

This ratio reflects the safety in the operations of banks. According to the regulations of the State Bank, this ratio below 3% will ensure the health of credit activities.

- Rate of overdue debt of science and technology

KHCN overdue debt ratio =

Overdue debt of science and technology

Total outstanding debt of science and technology

Determining the overdue debt ratio is a very important factor in assessing the quality ofThe bank's TDCN volume reflects loans that are likely to be repaid.poor repayment. If this ratio is low it is good, most of the credit is profitable and has the potential torecovery ability. Conversely, if this ratio is high, the bank needs to have control measures.Control overdue debt, limit risks of capital loss.

Indicators on medium and long-term credit operating profits.

This indicator reflects the profitability of the bank's credit facilities, indicating how much profit each dong of outstanding loans for customers brings. A high ratio shows that credit facilities profit is large and of high quality.

Profit from TDCN activities

TDCN contribution level =

Total profit before tax of the bank

This indicator shows the level of contribution of credit activities to the overall business performance of the bank. If this ratio is high, it reflects positive credit quality but also means that the bank accepts to face potential risks.

To evaluate the quality of TDCN, it is impossible to rely on a single indicator but must use a system of indicators to draw the most accurate and authentic conclusions.

1.3.4.2 From the customer perspective

To evaluate the quality of personal credit from the customer's perspective, we will evaluate customer satisfaction with personal credit.

a. Definition of customer satisfaction

Satisfaction is the customer's response to the difference between expectations and perceived performance after using a product or service (Tse and Wilton, 1988) or satisfaction is the consumer's response when expectations are met (Oliver, 1997).

b. Product quality, service and customer satisfaction

According to Cronin and Taylor (1992); Yavas et al (1997); Ahmad and Kamal (2002): Product and service quality is the factor that has the greatest impact on customer satisfaction. Therefore, to improve customer satisfaction, service providers must improve product and service quality - which is created first and determines customer satisfaction. Spreng and Mackoy (1996) also pointed out that service quality is the premise of customer satisfaction.

In addition, according to Cronin and Taylor (1992): factors such as customer perception of price will affect customer satisfaction. Price is considered as the consumer's perception of giving up or sacrificing something to own a product or service (Zeithaml, 1988). In the context of increasingly competitive markets and changing customer perceptions of products and services, researchers have determined that price and customer satisfaction are closely related (Patterson et al, 1997). Zeithaml and Bitner (2000) believe that the price of a service can greatly affect the perception of service quality, satisfaction and value. Because service products are intangible and are often difficult to evaluate before purchase, price is often seen as a substitute tool that affects the satisfaction with the service that consumers use.

We establish a model that considers the key factors affecting customer satisfaction as service quality followed by price.

c. Research model

The selected service quality measurement model is the SERVPERF model, a variation of the SERQUAL model.

The SERVQUAL model (Parasuraman, Zeithaml & Berry 1988) is a popular service quality research model and is most widely applied in marketing research to generalize service quality measurement criteria. In which, service quality depends on customers' perception of the service and this perception is considered on many factors forming a scale of five criteria:

- Reliability: the ability to provide accurate, timely and reputable services, respect commitments, and keep promises to customers.

- Responsiveness: ability to solve problems quickly, handle complaints effectively, be willing to help customers and meet customer requests.

- Tangibles: are the external images of facilities, equipment, tools, etc.

- Assurance: is a factor that creates trust for customers, perceived through professional service, good expertise, polite style and good communication skills of service staff, thanks to which customers feel secure every time they use the bank's services, creating trust for customers.

- Empathy: is the care and concern for each individual customer, helping customers feel like "honored guests" of the bank.

Reliability

Responsiveness Tangibles Assurance

Empathy

Level of feeling

receive

Periodic value

hope

Perceived service quality

Figure 1. SERVQUAL Model (Parasuraman, Zeithaml & Berry, 1988)

SERVQUAL is built on the perspective that perceived service quality is a comparison between expected values and the values that customers perceive when using the service: Service quality = Perceived level - Expected value

SERVQUAL is recognized as a scale with theoretical and practical value after many studies and applications. However, the SERVQUAL measurement procedure is lengthy. Therefore, a variation of SERVQUAL has appeared, SERVPERF, the perception model.

The SERVPERF model introduced by Cronin & Taylor (1992, cited in Thongsamak, 2001) determines service quality by measuring only perceived service quality. Service quality is best reflected by perceived quality without the need for expected quality or weighting of the five components.

Service quality = Perception level

Reasons for choosing the SERVPERF model: compared to SERVQUAL, the SERVPERF model has more outstanding advantages such as:

- The customer expectation part of the SERVQUAL model does not add any information from the customer perception part (Babakus and Boller, 1992). Perception can be easily defined and measured based on the customer's belief about the services they have used while expectation can be understood in many ways and can be interpreted differently by different authors and researchers (Dasholkar, 2000; Babakus and Boller, 1992; Teas, 1993).

- Empirical evidence from Cronin and Taylor when conducting comparative studies in four fields of banking, pest control, drying and fast food; and Parasuraman's studies also showed that SERVPERF is better than SERVQUAL.

- The questionnaire according to the SERVPERF model is half as concise as SERVQUAL, not boring and time-consuming for respondents. The concept of expectation is also quite vague for respondents (Phong and Thuy, 2007).

- Measuring customer expectations is very difficult.

From the above analysis, the research model evaluates customer satisfaction with personal credit of Asia Commercial Bank, Hue branch based on 6 influencing factors.

The 24 observed variables 6 include 5 factors of service quality (reliability, tangibles, service efficiency, empathy, assurance) and price factor.

Questionnaire design: The questionnaire is designed with 2 parts:

- Part 1: Some personal information of the customer and information about participating in TDCN

- Part 2: Collecting customer assessments of service quality and customer satisfaction . Measurement scale: The measurement form used in quantitative research is the scale introduced by Rennis Likert (1932), a popular 5-level scale from 1-5 to find out the level of assessment of respondents.

Sampling method : Random sampling technique.

-Some studies on personal credit, previous science and technology loans

Previous topics (see Appendix 3) have systematized the theory of bank credit, credit for science and technology and issues of credit quality; raised the current situation and evaluated the quality of credit activities at the research bank through a series of indicators or analyzed real situations, thereby proposing specific solutions to contribute to improving the quality and expanding credit. However, these studies only stopped at evaluating the quality and effectiveness of credit from the bank's perspective, not evaluating customer satisfaction when participating in credit at the bank. Therefore, in this research topic, I will evaluate the quality of credit for science and technology from both the bank's perspective and the customer's perspective.

6 See Appendix 1: Survey Form

Chapter 2: Evaluation of the quality of TDCN at Asia Commercial Joint Stock Bank, Hue branch

2.1. OVERVIEW OF ASIA COMMERCIAL BANK – ACB

2.1.1 A brief overview of Asia Commercial Bank – ACB

Asia Commercial Joint Stock Bank (ACB) was established under license number 0032/NH-GP issued by the Governor of the State Bank of Vietnam on April 24, 1993 and the government

Officially put into operation on June 4, 1993. As of December 31, 2011, ACB's charter capital is VND 9,376,965,060,000.

Since its inception, ACB has continuously expanded its scale with a widespread network of 345 branches.

branches and transaction offices in developed economic regions nationwide. As of August 31, 2012, the total number of employees of Asia Commercial Bank was 10,309 people. Staff with university and post-graduate degrees accounted for 93%, and were regularly trained in professional skills at ACB's own training center.

With the vision of becoming the leading retail joint stock commercial bank in Vietnam and the strategy of competing through differentiation, ACB has now become the leading retail bank in Vietnam with more than 200 products and services, considered one of the banks providing rich services based on modern technology platforms.

ACB's main products and services include:

- Mobilizing capital (receiving deposits) in Vietnamese Dong, foreign currency and gold.

- Use capital (credit provision, investment, joint venture capital contribution) in Vietnamese Dong, foreign currency and gold.

- Intermediary services (domestic and international payments, treasury services, overseas remittances and express money transfers, life insurance via banks).

- Foreign currency and gold trading.

- Issuance and payment of credit cards and debit cards.

ACB has been affirming itself as one of the leading commercial joint stock banks in Vietnam, through many awards and certificates of merit voted by the State and prestigious newspapers such as: Second-class Labor Medal awarded by the President; Competition flag

Competition of the Government, State Bank; "Best Bank in Vietnam" voted by Euromoney magazine 7 times in 1997, 2006, 2008, 2009, 2011, 2012; awards from prestigious international magazines Global Finance, The Asian Banker, AsiaMoney, FinanceAsia, The Asset, World Finance voted as "Best Bank in Vietnam" and "Strongest Bank in Vietnam" in 3 years 2009, 2010, 2011.

ACB continuously improves service quality, connects with customers through the quality of service provided, offers different product bundles suitable for each customer group, and increases many utilities for customers through technology investment. ACB also puts into operation risk management, financial management and human resource management functions and implements the information technology strategy for the period 2011-2020 with the criteria of "safe operation and rapid development".

2.1.2 Asia Commercial Joint Stock Bank – Hue Branch

Asia Commercial Joint Stock Bank, Hue Branch was established under Decision No. 904/QD-BPC dated November 29, 2002. On June 24, 2005, the Bank was granted a business license and officially began operating on July 22, 2005.

Address: 01 Tran Hung Dao, Hue City, Thua Thien Hue Province Phone: 0543.571175 Fax: 0543.571234

At that time, in Thua Thien Hue province, there were four State-owned banks and several other commercial banks operating, so the competitive pressure was quite high. ACB always tried to improve, perfect, and launch new products to meet customer needs and became known as a trustworthy brand. ACB increasingly affirmed its position, the bank continued to open two more transaction offices in Phu Hoi (September 30, 2008) and An Cuu (June 9, 2011) to bring the bank closer to customers.

* Phu Hoi Transaction Office – Hue:

+ Address: 30 Hung Vuong, Phu Hoi Ward, Hue City

+ Phone: 054.3936639 + Fax: 054.3936937

* An Cuu Transaction Office - Hue

+ Address: 100 Hung Vuong, Phu Nhuan Ward, Hue City

The 7 Awards are selected based on the following criteria: transaction turnover; innovation and leadership; credit rating; asset quality and earnings; and operating efficiency ratios .

+ Phone: 054.388369 + Fax: 054.3883696

Organization and functions, tasks of departments:

Organizational structure of ACB bank, Hue branch (see organizational chart in Appendix 4)

+ Board of Directors: manages all branch activities, builds, implements, and checks action programs to complete the plans assigned by the General Director.

+ Customer Service Department, including the Personal Financial Consulting Department (PFC): completes and develops products and services for customers: Makes business plans, searches for customers, discovers customer needs to advise on suitable products and services, evaluates customers, collects initial information to serve future appraisal, introduces customers to products and services and advertises the Bank's and branch's brands, guides customers to complete procedures quickly and conveniently.

+ Corporate Customer Department: provides products and services for corporate and private enterprises such as opening accounts and making payments, lending for production and business, providing international payment services, domestic guarantees, etc. This department will make business plans, find customers, and evaluate corporate customers.

+ Business support department: performs professional support functions for departments: Tracking loan records, managing customers, consulting on loan and deposit products for customers, preparing and executing contracts, appraising collateral, handling NQH, etc.

+ Transaction office - Treasury: consists of two main departments: Accounting - Treasury, with the function of contacting and transacting with customers, performing collection and payment; trading in gold, foreign currencies and directly accounting, statistical accounting and payment according to regulations.

+ Administrative Department: with the main functions of developing regulations for the bank's organization, managing the quantity, quality, and records of all officers and employees; developing labor and salary plans; managing the bank's salary fund, developing labor regulations, collective labor agreements, etc. Accounting Department: directly accounting and statistical accounting.

+ Internal audit department: sent by the Head Office to perform the following tasks: monitor activities at the unit, inspect operations, prepare reports...

2.1.3 Business performance results of ACB Bank, Hue branch in the period 2008-2012

Thousand Dong

160,000,000

137,965,942

89,898,209

74,296,040

81,725,644

64,266,075

118,591,000

54,140,873

62,590,604

68,849,665

75,734,631

54,140,873 11,705,436 12,875,980 14,163,578 19,104,172

140,000,000

120,000,000 Income

100,000,000

80,000,000

60,000,000

40,000,000

20,000,000

0

2.008 2.009 2.010 2.011 2.012

Expense

Total profit before tax

Year

Figure 2.1: Profit chart of ACB Bank - Hue 2008-2012

Looking at the profit chart of ACB bank - Hue branch in the period of 2008-2012, we can see that the branch's income has been increasing continuously every year. Specifically, in 2009, income increased by 15.6% compared to 2008 (equivalent to 10,029.9 million VND). In the period of 2009-2011, it increased at a fairly stable rate, increasing by 10% each year. In 2011, the branch's income reached 89,898.2 million VND. By 2012, income increased by more than 48 billion VND compared to 2011 (equivalent to 53.47%).

In terms of costs, in 2009, the total costs of ACB-Hue Bank were 62,590.6 million VND, an increase of 8,449.7 million VND compared to 2008, equivalent to 15.6%. Like income, costs in the period 2009-2011 increased quite evenly, each year costs increased by 10%. Total costs in 2011 were 75,734.6 million VND, in 2012 costs increased compared to 2011 by 56.6% (equivalent to 4,940.6 million VND).

About profit:

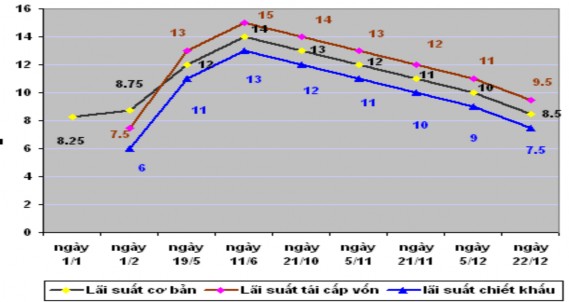

2008: The economic crisis has created great pressure on the operations of banks, including ACB-Hue Bank. High inflation (2008: 19.89%) and the rapid and large fluctuations in interest rates during the year have put banks in a passive position. In the first months of the year, interest rates increased continuously with the peak lending interest rate reaching 23%-24%/year and the peak mobilization interest rate also reaching 20%/year in the middle of the year. But by the end of the year, interest rates decreased rapidly. The State Bank has 8 times

Adjust the basic interest rate after 2 years and 2 months to maintain the basic interest rate at 8.25% (from December 1, 2005 to February 1, 2008). Despite this difficult situation, ACB in general and Hue branch in particular always adapt quickly to the market, maintain the initiative, implement synchronous solutions to develop and ensure payment capacity, moreover, the bank has seriously implemented the direction of the government and the State Bank to control inflation. The total pre-tax profit of the branch this year reached 10,125.2 million VND.

Figure 2.2: Interest rate developments in 2008

2009: The success of the Vietnamese economy this year was to control inflation (less than 7%), however, maintaining the basic interest rate at 7% for quite a long time made banking activities very difficult at times due to the low difference between input and output in credit activities. However, the banking system still tried to promote its role as a capital transmission channel for the economy, with the loose monetary policy and the government's economic and financial stimulus measures requiring banks to have a process of strictly controlling capital efficiency and being more cautious with loans. At the end of the fiscal year, the total pre-tax profit of ACB-Hue Bank was 11,705 million VND, an increase of 15.6% compared to 2008 (equivalent to 1.58 billion VND).

2010: Inflation during the year was at double digits (11.75%), domestic economy grew strongly. In the first 10 months of the year, the basic interest rate and refinancing interest rate were stable at 8%/year, the State Bank flexibly operated open market operations and supervised the implementation of safety ratios of credit institutions, and regulated deposit and lending interest rates.

gradually decreased according to the Government's direction (by the end of October, the average VND mobilization interest rate was 10.44%/year, lending 13.18%/year). In the last two months of the year, the State Bank adjusted the basic interest rate and refinancing rate to increase by 1%/year, combined with tight management of the money supply, and stipulated a ceiling interest rate of VND mobilization at 14%/year to stabilize the monetary market, which increased market interest rates and reduced credit demand. The branch's total pre-tax profit reached 12,876 million VND, an increase of 1,170.5 million compared to 2009.

Figure 2.3: Vietnam inflation chart 2011-2012

2011: The State Bank of Vietnam cut money supply and credit growth suddenly, causing high lending interest rates and bad debts, strained liquidity in the banking system, exhausted stock market, frozen real estate market, but actual inflation remained too high (over 18%). However, overcoming challenges, the bank still maintained its position, maintaining a profit growth rate of 10% compared to 2010.

2012: The economic situation has improved significantly compared to 2011. Inflation has decreased significantly, giving the government the basis to lower interest rates 6 times during the year. The budget deficit and devaluation of the dong have also been almost controlled. Asia Commercial Bank Hue's profit increased by 34.9% compared to 2011, with total pre-tax profit reaching more than 19 billion VND.

In summary, in the period of 2008-2012, in the context of many difficulties in the Vietnamese and world economies, but with the direction of the State Bank, the synchronous solutions of the bank, the efforts of all leaders and employees, the bank still achieved positive business results and good growth. This is an encouraging result and partly demonstrates the potential and prestige of ACB bank - Hue branch.