The parent company is responsible for managing the commercial bank and its subsidiaries through financial investment activities. The commercial bank can carry out some financial management and technical support measures on behalf of the parent company in each field. Parent companies often have the advantage of being able to minimize risks for owners, allowing ownership and control of a number of different companies.

Citigroup and HSBC are financial groups that clearly demonstrate this model. The shareholders of the parent company do not directly manage the activities of the subsidiaries. This model has the advantage of being risky in this field.

no effect on other areas.

1.2.3.3. Parent - subsidiary relationship model

Maybe you are interested!

-

Current Status of Parent Company - Subsidiary Company Model at Emico Corporation

Current Status of Parent Company - Subsidiary Company Model at Emico Corporation -

Recommendations on Perfecting the System of Legal Regulations to Prevent Acts of Exploiting the Company's Shell and Exploiting the Parent Company - Subsidiary Company Model

Recommendations on Perfecting the System of Legal Regulations to Prevent Acts of Exploiting the Company's Shell and Exploiting the Parent Company - Subsidiary Company Model -

Relationship Between Research Variables in the Model

Relationship Between Research Variables in the Model -

Completing the personal credit rating model at Saigon Commercial Joint Stock Bank - 12

Completing the personal credit rating model at Saigon Commercial Joint Stock Bank - 12 -

Building a Scale and Research Model of Factors Affecting Customers' Decision to Choose a Bank to Deposit Savings at

Building a Scale and Research Model of Factors Affecting Customers' Decision to Choose a Bank to Deposit Savings at

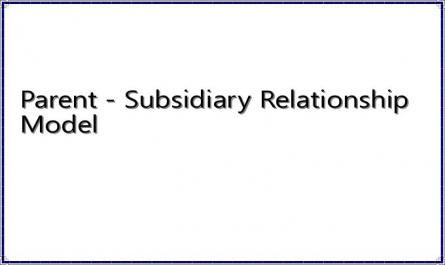

In the parent-subsidiary model, power is concentrated in the “parent company” and indirectly intervenes in the operations of the subsidiary. The role of the board of directors will directly manage the bank and exercise the right to hold shares in the Securities company and the Insurance company. Regarding capital relations, the bank - securities - insurance all hold each other's capital (see figure 1.3).

Figure 1.3: Parent-subsidiary company model

SHAREHOLDERS

PARENT COMPANY

COMMERCIAL BANK

SECURITIES COMPANY

INSURANCE COMPANY

( Source: author's synthesis) [61]

1.2.3.4. Other models

The hybrid model is a blend of the above models, in which the corporate office will participate in deciding on important areas such as strategy, policy and human resources.

There are also a number of other models depending on the organizational capacity and business strategy that corporations can choose, such as the model based on ownership structure from simple ownership to mixed ownership of capital between members. Horizontal, vertical, and mixed multi-industry and multi-sector linkage models to expand investment to related industries and professions or to counter competition and takeover from other corporations.

1.2.4. Comments on the role of TC-NH group

1.2.4.1. For the economy

In terms of the types of services provided by banks, banks are understood as: financial institutions that provide a wide range of financial services, especially credit, savings, payment services, and perform the most financial functions of any business organization in the economy. Therefore, when operating as a financial-banking group, it will enhance the ability of commercial banks to contribute to economic growth through the results of the commercial banks themselves or the group in general. Through research, it is shown that the activities of the commercial banking system or financial-banking groups affect economic growth through capital supply and are expressed through the following factors:

- Encourage savings, contribute to the formation and support of capital flows in the economy.

In the economy, there are always subjects in a state of temporary surplus. They have the need to invest to both preserve capital and make a profit for their capital, but not everyone can do that. Banks

These funds will be mobilized in many forms: receiving deposits, issuing valuable papers, accumulating them and lending them back to the economy. Through the banking system with the basic functions of commercial banks, capital flows are formed and circulated more easily and smoothly in the economy.

- Effective allocation of capital among industries, production, trade, investment and service sectors of the economy.

Commercial banks are essentially businesses, operating for the purpose of profit and maximizing the value of the owner's assets. Therefore, commercial banks must select businesses or projects that are capable of debt recovery and are effective to lend to. Thanks to the credit screening process, capital in the economy is concentrated in areas with high profitability and many benefits. Inefficient sectors or industries will not receive investment. Thanks to the financial intermediary function of commercial banks, capital is effectively allocated among different sectors and areas of the economy.

- Reduce overall costs for the economy and minimize transaction risks

The transfer of capital takes place directly between subjects with surplus and deficit of capital, which requires a lot of costs for both sides: such as time costs, costs of collecting and processing information and other wastes because in many cases, these needs are not compatible and transactions cannot take place. If calculated in total, such costs cause damage to the entire economy because of waste and loss of resources. Commercial banks, as financial intermediaries, can minimize these costs. Through their activities, commercial banks collect and hold information about customers who need capital as well as others who are willing to provide capital, using technical operations to share needs and disperse risks, monitor credits, reduce moral hazard risks as well as asymmetric information.

- TC-NH Group's sponsorship activities help businesses maintain stable production, invest in technology, change machinery, thereby contributing to improving the production capacity of the economy.

TC-NH Group affects growth by changing the savings rate and through financing enterprises to expand production both in breadth and depth, mainly investing in technology to help enterprises improve their competitiveness.

In addition, consumer lending activities contribute to stimulating consumer demand, thereby contributing to economic growth. TC-NH Group also relies on abundant capital to easily meet all customer needs, ready to provide large credit to help businesses supplement working capital, invest in fixed assets, invest in technology, change machinery, thereby improving the production capacity of businesses, contributing to improving the production capacity of the economy.

- The activities of TC-NH groups contribute to improving the business environment and building a business culture for enterprises.

The TC-NH group's deep participation in economic activities such as capital contribution, consulting, etc. also creates positive effects for the innovation of working style of these entities. The group itself is a professional organization, with a modern technology system and a widespread information network. The dynamism and professional, transparent style of the banking industry indirectly helps other organizations and individuals in the economy to form a professional style and business culture.

- The activities of TC-NH group contribute to reducing the cost of cash circulation in the economy.

With the advantage of experience in currency management and the ability to provide non-cash payment services, TC-NH Group will mobilize a large amount of deposits from group members, partners and economic sectors.

Other to contribute to increasing the amount of deposits, increasing the amount of capital supply for the economy, but with modern transaction tools, the circulation and supply of currency does not generate many related costs, thereby contributing to reducing the cost of cash circulation for the economy, and that is also a way to reduce costs to increase profits for the bank itself.

1.2.4.2. For entities in the TC-NH group

If TC-NH Group does not bring certain benefits to its members, the formation of the group will be meaningless, and the group model cannot exist. Through the survey, it is shown that TC-NH Group has brought positive aspects to the basic participants as follows:

- Enhance the ability to exploit and make good use of resources and resources within the same system

Entities in the same TC-NH group have the opportunity to exploit each other's advantages to increase overall competitiveness, while exploiting the common market and customers to cross-sell products and services. Of course, any incentives, if any, are within the allowable limits because each member has independent business performance, but through exploiting each other's market share, a certain stable market is created for each member, which is an advantage that not every economic entity can have.

- Facilitate the implementation of short-term goals and long-term strategies

Member units within the same TC-NH group should have more possibilities to develop in a common direction, through agreements agreed upon by a group committee, thereby allowing members to coordinate to increase competitiveness as well as easily implement short, medium and long-term goals in a stable manner, less affected by objective factors.

- Increase risk prevention and competitiveness

The goal of safe and sustainable development for all members is always

is also placed at the top because it is the prestige and the common brand of the group. Like other economic groups, in the TC-NH group there is always a specialized risk management committee that will give early warnings to members to increase vigilance and control risks, from subjective risks such as operational risks, business process risks to objective risks such as policy, mechanism and market risks. Good risk management will help members save costs and time, contributing to increasing overall competitiveness.

- Expand distribution channels and international markets

Like other economic groups, TC-NH groups will develop in the direction of multinational corporations, present in potential countries and regions outside the territory. The activities of member companies and banks are always the basis for each other to gain the best competitive advantage, so group members will have the opportunity to expand potential markets, expand distribution channels as well as investment cooperation relationships to exploit commercial advantages and increase investment opportunities to seek the best profits.

1.3. BASIC CONDITIONS PROMOTING THE FORMATION OF TC-NH GROUP

Any economic form or economic entity that appears in the economy must have the necessary basic conditions as a basis, as a driving force, as a foundation for its formation and development. In the field of finance and banking, to develop into a corporation, it is also necessary to fully converge the necessary basics, which can be called the "necessary" and "sufficient" conditions for the birth of a corporation. Through research, it has been shown that these conditions are as follows:

1.3.1. “Necessary” conditions for the formation and development of TC-NH group

1.3.1.1. First of all, it is an inevitable development movement, especially in the context of an economy developing according to market trends.

The formation and development of the commercial banking system is an inevitable product of

economy. The appearance and existence come from the objective requirement of resolving the conflict between the need and the ability to supply large capital in the economy. In the economy, there are always two opposing states between the need and the ability to supply capital. This contradiction is initially resolved through the activities of banks with the role of intermediaries in the borrowing relationship between those with capital and those who need capital. When the commodity economy and the market develop highly with many intertwined relationships and deep integration between countries, the activities of the banking system are also raised to a new level to suit the form and content of activities, including service provision to meet the increasingly developing needs of the market. This movement can be seen as an inevitable development movement in accordance with the law of economic development in general and the market in particular. In other words, in the interactive relationship, it is the development of the commodity and monetary economy, the peak of which is the market economy, that gives rise to a new form of banking activities to serve the market economy.

1.3.1.2. The trend of global economic globalization has promoted the formation of TC-NH groups.

The trend of global economic globalization has an objective and strong impact on the formation of TC-NH groups. Economic globalization leads to the formation of common markets in each region, or globally, making the transfer of resources between countries and territories more and more diverse. Capital circulation is faster and wider due to increasingly strong multinational investment, thereby requiring the formation of a financial and banking entity with a new model capable of providing better and more competitive financial services to customers and to the globalized economy. Commercial banks with advantages in capital, management and relationships in the financial and banking sector will be able to do this, and TC-NH groups will be one of the appropriate models to help these entities.

Commercial banks both meet customer needs and have the ability to compete and integrate globally.

The globalization trend that promotes the emergence of TC-NH groups is also reflected in the aspect of compliance with international principles and standards, that is, countries commit to complying with a number of principles on operational safety and banking risk supervision such as the Basel Convention to avoid bank failures or illegal transactions that affect the economy, and to meet these strict standards, only large banks and large financial groups are able to meet them.

1.3.1.3. Development of financial and monetary markets

The development of the market and financial products and services is one of the factors contributing to the formation of TC-NH groups. The world economy develops in the direction of the market, giving rise to the financial market, including the currency market and the capital market. The currency market was initially simple with the primary market, and has developed a secondary market. The financial market with the capital market has more and more derivative instruments such as: securities, stocks, bonds... combined with the currency market to create a rich, diverse financial and monetary market, developing increasingly strongly, contributing to the formation of large financial and monetary groups in the world to meet international payment relations and multinational investment.

1.3.2. “Sufficient” conditions for the formation and development of TC-NH group

1.3.2.1- The legal environment plays an important role in the establishment of TC-NH group.

The legal environment can promote or hinder the formation and development of TC-NH groups, especially the legal regulations governing financial, banking and securities activities. The Central Bank plays a direct management role and adopts policies directly or indirectly through the open market, through the stock market, through different capital distribution channels with the loosening of