equivalent to a growth rate of 27.41%, but in 2008, outstanding credit only increased by 3,593 billion VND, equivalent to a growth rate of 16.52%.

In addition, lending to SMEs at Vietcombank in the period 2005-2008 still accounted for a low proportion (from 22% to 25%) of the bank's total outstanding loans.

Looking at the above data table, I would like to make some comments on the credit structure for SMEs at Vietcombank in the period 2005 - 2008 as follows:

About the structure according to loan term

Total outstanding debt Short term Medium long term

Billion VND

30,000

25,000

20,000

15,000

10,000

5,000

0

2005 2006 2007 2008

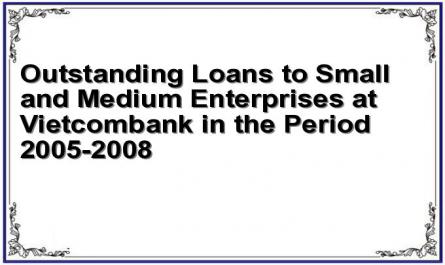

Chart 2 - 5: Outstanding loans to SMEs at Vietcombank in the period 2005-2008

Short-term credit accounts for a larger proportion than medium- and long-term credit in the loan portfolio (short-term credit proportion in 2005: 57.03%, in 2006: 57.02%, in 2007: 56.44%, in 2008: 55.12%). However, the proportion of medium- and long-term credit tends to increase and the proportion of short-term credit tends to decrease. In general, the structure of outstanding loans between short-term and medium- and long-term loans is quite stable and balanced, consistent with the nature of the bank's mobilized capital sources.

According to the policy of the State Bank, commercial banks need to increase medium and long-term loans for SMEs to support these enterprises in long-term investment, expanding the scale of production and business activities and improving scientific and technical level. Thus, the increasing trend of the proportion of medium and long-term credit in

Vietcombank's loan portfolio is completely in line with the policy set by the State Bank. In addition, compared to the outstanding loan structure for SMEs of the entire banking industry (as of July 31, 2008, outstanding medium and long-term credit accounted for 73.05%, outstanding short-term credit accounted for 26.95%), the outstanding loan structure at Vietcombank is more balanced and appropriate.

About the structure by loan type

The data in Table 2-5 show that the proportion of outstanding loans in VND and foreign currency (USD) is relatively even over the years. Due to the characteristics of Vietcombank as the leading bank in the country in international payment activities and foreign currency trading, the proportion of outstanding USD loans in the loan portfolio is often equal to or higher than the proportion of outstanding VND loans. However, in 2008, the proportion of USD loans decreased significantly and was lower than the proportion of VND loans. One reason for this decrease is that the fluctuations in the USD/VND exchange rate in the past year have had many disadvantages for lending activities; in addition, due to the impact of the economic crisis, imported goods have encountered difficulties in consumption, so the import activities of small and medium enterprises have stagnated and there is no need to borrow foreign currency capital. As of December 31, 2008, the structure of outstanding VND/USD loans was 53%/47% respectively.

In addition, the structure of outstanding credit for SMEs by customer, by industry and by geographical region has some main characteristics as follows:

By customer type

Along with the equitization process of SOEs as well as the shift in investment direction, reducing the proportion of loans to weak SOEs, focusing on lending to other types of enterprises, the structure of Vietcombank's outstanding loans has shifted.

This investment shift is also reflected in the structure of outstanding loans to SMEs of banks. In the outstanding loans to SMEs, the proportion of outstanding loans to state-owned enterprises tends to decrease gradually (in 2005: 56%, in 2006: 49%, in 2007: 36%, in 2008: 30%), outstanding loans to non-state enterprises continuously increase in quantity and proportion (in 2005: 44%; in 2006: 51%; in 2007: 64%). In 2008, the proportion of outstanding loans to small and medium-sized enterprises which are non-state enterprises was at 70%, of which limited liability companies and joint stock companies accounted for about 60%, and foreign-invested enterprises accounted for about 10%.

By industry

The industry structure in Vietcombank's lending to SMEs is quite diverse, but still focuses on a number of industries such as trade (textiles, footwear, transportation, wood products, fertilizers) and processing (aquatic and seafood products)... which do not meet the requirements of risk dispersion in credit investment.

By geographic area

Vietcombank's outstanding loans to SMEs are mainly concentrated in large cities, urban areas, and industrial zones such as Hanoi, Da Nang, Ho Chi Minh City, the Southeast region (Dong Nai, Binh Duong, excluding Ho Chi Minh City) and the Southwest region (Can Tho). Currently, the Small and Medium Enterprise Credit Department model has only been piloted in two locations: Hanoi and Ho Chi Minh City.

Thus, Vietcombank's credit activities for small and medium enterprises in recent years have the following main features: With the policy of focusing on economically dynamic development areas, in Ho Chi Minh City, Hanoi and the Southeast region, outstanding credit has a higher growth rate and proportion; The proportion of outstanding credit for the group of state-owned enterprise customers in the total outstanding debt tends to decrease gradually, the proportion of the group of non-state enterprise customers tends to increase gradually; Credit growth has an even rate for VND and foreign currency; Growth is even for short-term credit and medium- and long-term credit.

3 Status and causes of credit risk

Growth and expansion of credit investment always come with potential risks that may occur in the future. Experience and reality show that hot credit growth at a certain stage often leaves consequences in terms of overdue debt and bad debt ratio in the following years. Vietcombank seems to be unable to escape that harsh rule of the market.

During the period 2005-2007, Vietnam's economy grew strongly, credit activities were also in a period of strong development. But soon after, in 2008, due to the impact of tight monetary policy and unpredictable developments of the global economic crisis, credit activities almost froze for a period of time. Credit quality was also seriously affected. During the period 2005-2007, the ratio of overdue debt and bad debt of Vietcombank was always maintained at a very low level of about

over or under 2% of total outstanding debt; however, in 2008, Vietcombank's credit quality declined, reflected in the increasing ratio of overdue debt and bad debt.

3.1 Overdue debt

In the period 2005-2006, the rate of overdue debt in credit for SMEs at Vietcombank tended to decrease, however, in 2007, especially in 2008, the rate of overdue debt tended to increase. The situation of overdue debt in Vietcombank's SME loans is shown in Table 2-6 below:

Table 2 - 6 Overdue debt (Unit: Billion VND)

Target

2005 | 2006 | 2007 | 2008 | |

Outstanding SME credit | 14,528 | 17,071 | 21,750 | 25,343 |

NQH items | 273 | 203 | 272 | 705 |

% Overdue debt | 1.88% | 1.19% | 1.25% | 2.78% |

Maybe you are interested!

-

Improving the quality of short-term loans for small and medium enterprises - 2

Improving the quality of short-term loans for small and medium enterprises - 2 -

Improving the quality of short-term loans for small and medium enterprises - 12

Improving the quality of short-term loans for small and medium enterprises - 12 -

Characteristics of Business Activities and Business Management Organization at Small and Medium Enterprises in Vietnam

Characteristics of Business Activities and Business Management Organization at Small and Medium Enterprises in Vietnam -

Developing lending to small and medium enterprises at Vietnam Joint Stock Commercial Bank for Industry and Trade - Bac Ninh Branch - 12

Developing lending to small and medium enterprises at Vietnam Joint Stock Commercial Bank for Industry and Trade - Bac Ninh Branch - 12 -

Overview of Research on Factors Affecting the Linkage of Small and Medium Enterprises with Enterprises with Direct Investment Capital

Overview of Research on Factors Affecting the Linkage of Small and Medium Enterprises with Enterprises with Direct Investment Capital

Source: SME credit report of Credit Policy Department, VCB Head Office

In 2006, overdue debt decreased sharply partly because Vietcombank used more than 800 billion in reserves to handle bad debt, clean up the bank's financial statements, and prepare for Vietcombank's equitization. However, the overdue debt ratio in 2007, especially in 2008, tended to increase due to the following reasons:

The rapid growth of SME credit in 2007 resulted in a decline in credit quality in 2008: in 2007, due to fierce competition between banks in the credit market, in order to attract more customers, banks were willing to make loans with many potential risks. Therefore, the rate of overdue debt in 2007 tended to increase. In early 2008, the domestic inflation rate increased, many enterprises encountered difficulties in production and business activities due to increased input costs while output products were difficult to sell. As a result, many enterprises were unable to repay their loans to banks on time, including enterprises that had always had good quality credit.

The global economic crisis that began in the second half of 2008 until now has not only affected the credit growth rate for small and medium enterprises

Vietcombank's credit growth slowed down and credit quality also declined significantly. Most of the customers are small and medium enterprises facing many difficulties in business and therefore cannot pay their debts on time.

In 2008, the rate of overdue debt in loans to small and medium enterprises at Vietcombank increased to an alarming level, so improving credit quality was an urgent requirement for Vietcombank.

3.2 Debt classification

Recent debt classification results further confirm that Vietcombank's credit quality for small and medium enterprises shows signs of decline, and the bad debt ratio tends to increase.

Table 2 - 7 Summary of loan classification for SMEs of Vietcombank (Unit: billion VND)

Target

2005 | 2006 | 2007 | 2008 | |

1. Total outstanding credit | 39,630 | 51,773 | 61,044 | 67,743 |

2. Outstanding loans of SMEs | 14,528 | 17,071 | 21,750 | 25,343 |

- Group 1 | 13,801 | 16,460 | 20,662 | 23,468 |

- Group 2 | 225 | 217 | 351 | 704 |

- Group 3 | 193 | 194 | 382 | 695 |

- Group 4 | 140 | 91 | 213 | 263 |

- Group 5 | 169 | 108 | 141 | 213 |

3. Total bad debt of SMEs | 502 | 394 | 737 | 1,171 |

4. Bad debt ratio of SMEs | 3.46% | 2.31% | 3.39% | 4.62% |

5. (3)/(1) | 1.26% | 0.76% | 1.21% | 1.73% |

Source: Debt Classification Report of Credit Policy Department, VCB Head Office In previous years, Vietcombank was the leading bank among domestic commercial banks in terms of credit quality, with low bad debt ratio and a decreasing trend. However, in recent times (2007, 2008), Vietcombank's bad debt ratio has increased both in absolute and relative terms, even showing signs of increasing higher than that of other commercial banks. As of December 31, 2008, the bad debt ratio of the entire Vietcombank system was 4.5%, the highest ratio of all banks.

commercial in 2008. Of which, bad debt in the credit sector for SMEs had a rate of 4.62%, accounting for 38% of the total bad debt of the whole bank.

Compared to the general bad debt ratio of the entire Vietcombank system (2005: 3.44%, 2006: 2.28%, 2007: 3.38%, 2008: 4.5%), the bad debt ratio in the credit sector for small and medium enterprises tends to be higher. Specifically, the bad debt ratio in the SME sector in 2005: 3.46%, 2006: 2.31%, 2007: 3.39% and 2008: 4.62%. Thus, lending to small and medium enterprises is a risky business that requires a reasonable and separate form of governance. On the other hand, the increase and decrease in the bad debt ratio in the credit sector for small and medium enterprises is similar to the change in the bad debt ratio of the whole system, which shows that credit risk management for small and medium enterprises at Vietcombank must also be closely linked to credit risk management in the whole banking system.

One of the subjective reasons for the high increase in bad debt ratio in 2007 and 2008 was that the bank had classified debt close to international standards; however, Vietcombank still needs to review and re-evaluate the bank's credit risk management: Vietcombank's credit risk management policy is not really effective as well as the human factor does not meet the development requirements, which are the main factors causing the decline in Vietcombank's credit quality.

In addition to subjective factors, there are objective factors, which are the hot credit growth in 2007, the impacts of the economic crisis in 2008 (as explained in the overdue debt section) and some shortcomings that still exist in the debt classification according to Decision 493 and Decision 18 of the State Bank. These factors also contribute to the increase in the bad debt ratio in the credit sector for

SMEs in

Billion VND

1400

1200

1000

800

600

400

200

0

2006 | 2007 | 200 6 8 3 | |

Bad debt | Overdue debt |

Chart 2 - 6: Comparison of overdue debt and bad debt in credit for SMEs in the period 2005-2008

Vietcombank.

Decision 493 and Decision 18 of the State Bank regulate debt classification, provisioning and use of reserves to handle credit risks in banking activities.

of credit institutions. The practical application of debt classification according to these Decisions at Vietcombank results in the bad debt ratio always being much higher than the overdue debt ratio.

Bad debt mainly includes debts overdue for more than 90 days and extended debts. Debts overdue for less than 90 days are not classified as bad debt. Thus, the large difference between bad debt and overdue debt is because all extended debts are classified as bad debt (group 3, 4, 5).

Overdue debts are classified into different groups depending on the overdue period (overdue less than 10 days is classified into group 1 debt, overdue from 10-90 days is classified into group 2 debt, overdue from 91-180 days is classified into group 3 debt...); If the debt is extended, it is not based on the extension period but only based on the number of extensions to classify into different debt groups (first extension is classified into group 3 debt, second extension is classified into group 4 debt...).

However, the provisions of Decision 493 and Decision 18 are not suitable because not all extended debts are bad; on the other hand, there are debts extended for a very short period of less than 1 month - even some are extended for only 1 or 2 weeks - and then the customers pay their debts in full and on time, but all outstanding debts of the customers with the above extended debts are transferred to the bad debt group (because according to the regulations, when a customer has 1 debt transferred to the bad debt group, all remaining debts must also be transferred to the bad debt group) and it takes a probationary period of at least 3 months to be upgraded to the normal debt group.

3.3 Causes of credit risks for small and medium enterprises during the economic crisis

The results of the analysis of the current status of credit activities for small and medium enterprises at Vietcombank show that the economic crisis from the end of 2008 until now has had many negative impacts on the business situation of the bank, causing credit activities for small and medium enterprises to decline.

A major impact of the economic crisis is that it has created many risks for small and medium-sized enterprise credit activities. Recognizing signs that can lead to risks is an important task in order to take effective preventive and handling measures.

The following are 9 groups of potential risk signs mainly from the customer side , arranged in order of frequency from high to low:

One is due to customers using capital for the wrong purpose. This risk is often seen in loans with the following characteristics:

- The customer has implemented many production and business plans but due to the impact of the crisis, they have encountered many difficulties. Risk: The customer can use the expected revenue from the business plan that is funded by the bank to repay the debt for other business plans.

- It is difficult to accurately decide the credit limit granted to customers because the risk level and quality of customers cannot be fully assessed. Risk: granting too high a credit limit to customers and customers will use it for other purposes.

- The loan amount is too large compared to the customer's actual working capital needs. Risk: the customer uses the loan for other purposes.

- Customers borrow from many credit institutions at the same time. Risk: unable to control the bank's cash flow.

- Loan terms (especially working capital loans) are longer than necessary compared to the cash flow cycle. Risk: customers temporarily use money before the due date for repayment to the bank, that money is at risk when the economy is in crisis.

Second, customers have their capital misappropriated or lose capital. This risk is often seen in loans with the following characteristics:

- Customers do not have good policies and measures to manage receivables.

Risk: customers have difficulty or cannot collect receivables.

- Due to the impact of the crisis, customers are facing difficulties. Risk: other investors previously contributed capital in assets, then sought to withdraw capital in cash.

Third, customers cannot consume the product. This risk is often seen in loans with the following characteristics:

- Customers borrow money to import goods for domestic consumption, using imported goods as collateral. Risk: domestic consumption declines, goods cannot be sold.

- Appraisal for loans without really understanding the basic technical and technological content of the product and the business characteristics of the item. Risk: goods are difficult to sell or cannot be sold.