will affect the quality of audit reports. For the State Audit Office, the working conditions of the State Audit Office are reflected in the following criteria:

- Personal working equipment of KTVNN: basic inspection equipment and means for field inspection, means of transport, ...

- Applying information technology in auditing activities such as audit logs

maths;

- Business trip allowance regime for KTVNN;

- Reward regime for KTVNN;

- Sanctions for violations of KTVNN;

- Cultural environment in the Audit Team.

(b) Audit Approach

Auditing methods refer to auditing processes, procedures, and techniques.

designed by the audit unit to collect evidence about the appropriateness or effectiveness of the audited units. Some researchers believe that observing the audit method implemented will be a measure of audit quality. The research results of Wooten (2003) show that when the auditor is equipped with the most modern and advanced audit methods, it can detect material errors in the financial statements of the enterprise. According to the audit quality model of the Financial Reporting Council FRC (2008), an effective audit process has a positive impact on audit quality when the audit methods and tools applied in the audit process are well organized and provide a template or procedure to obtain appropriate and sufficient evidence for the audit. The audit method is also mentioned by many other international accounting and auditing organizations as a factor that has a great influence on the quality of the audit, both in terms of detecting errors in the accounting system and in terms of satisfying the users of the audit results. The International Auditing and Assurance Standards Board (IAASB) (2013) clearly states the time for the audit, the effectiveness of the audit procedures, the audit process and supervision.

Quality control is an important factor affecting audit quality.

According to Francis (2011), Knechel et al. (2013), the audit process is one of four groups of criteria for assessing audit quality. Contents

of the audit process including evaluation methods in the audit process, risk assessment, analysis process, etc.

(c) Quality Control

Similar to the audit method/process factor, the internal quality control system is also a factor that many scholars and auditing organizations assess as having an impact on audit quality. Accordingly, auditing companies with good internal quality control policies and procedures and operating effectively will be able to perform good quality audits. Cushing (1989) believes that material misstatements in financial statements can be more easily detected for auditing companies with good internal quality control policies and procedures. Francis (2011), Knechel et al. (2013) emphasize that regular quality control and inspection during the audit process is an important factor in ensuring audit quality.

In the auditing standards of many countries, this factor is also considered important and is required to be implemented in the auditing standards. International Auditing Standard No. 220 (ISA 220) and Quality Control Standard No. 1 (ISQC1) also clearly stipulate the contents related to the internal quality control system of the auditing company. In the system of State Auditing standards, auditing standard 40 clearly stipulates that the audit quality control system includes 6 factors as follows:

- Responsibilities of the State Auditor General, unit heads, audit team leaders and audit team leaders;

- Requirements on professional ethics of KTVNN;

- Develop policies and procedures to ensure audit quality;

- Adequate human resources, with capacity and ability to ensure audit quality;

- Develop and issue policies and procedures to ensure the implementation of auditing activities.

- Monitor audit activities.

2.3.3. External factors

While most of the studies surveyed confirmed the important role of factors related to the auditor and the audit unit in the quality of the audit, some studies also mentioned other factors. These are

External factors that are not related to the auditor or the audit firm but have an impact on audit quality. These factors are often specific to each country and each business sector.

(a) Factors pertaining to the audited entity

Regarding audited entities, factors related to the capacity, qualifications and awareness of the business management are considered to have an impact on the quality of the audit. FRC (2008) affirmed that the corporate governance of the audited entity has a certain impact on the financial statements and therefore also affects the audit quality. In addition, the size and characteristics of the business sector also indirectly affect the audit quality. Francis (2011), Knechel et al. (2013) when presenting the framework for audit quality also affirmed that the audit quality will depend on the characteristics of the audit client.

Research by Bui Thi Thuy (2014) also suggests that the more the management of the audited unit is aware of and appreciates the role of auditing for the unit, the more they will support and cooperate with the auditor, thereby creating an open and effective audit. Units with simpler, more focused business activities and a coherent and stable internal management system will help the audit process to be carried out more effectively, and the ability to detect and report violations to the enterprise's accounting system will be higher.

(b) Factors relating to the legal environment for auditing activities

Factors related to the legal environment for auditing activities include the system of accounting and auditing standards and regimes and related legal documents, which create the basis and guide the auditor's auditing work. In countries with a systematic and complete system of accounting and auditing standards, the auditing process will be smoother and more effective. These are often countries where accounting and auditing activities have been managed and developed for a long time, such as the UK, the US, and Australia. The Financial Reporting Association FRC (2008), when proposing a model for auditing quality, stated that the legal environment related to auditing will have a positive impact on auditing quality. Francis (2011), Knechel et al. (2013) proposed two models based on the systematization of previous studies, while expanding DeAngelo's (1981) definition of audit quality.

Scholars agree that the legal system is an important factor affecting the quality of financial statement audits.

(c) Other external factors

Macroeconomic environment such as growth, inflation and interest rates are important factors that directly affect enterprises in general and units audited by the State Audit Office in particular. Bui Thi Thuy (2014) and other researchers have analyzed that when macroeconomic conditions are unfavorable, it will negatively affect the financial situation and enterprises will have the motivation to beautify their financial statements. This will put pressure and difficulty on auditors in detecting and reporting violations of the audited units and affect the quality of audit reports.

In addition, according to IAASB (2013), national culture is considered to have a direct impact on the attitudes of the board of directors and corporate administrators towards corporate financial reporting as well as their interactions with auditors. Therefore, it will indirectly affect the output of the audit process. Therefore, auditors need to clearly understand the differences in cultural factors to plan and conduct the audit appropriately, to ensure consistent audit quality.

CHAPTER 3: RESEARCH METHODOLOGY

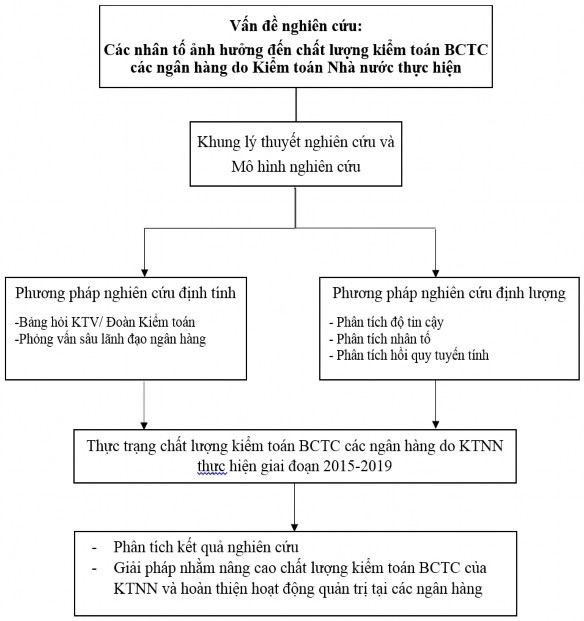

3.1. Research process

To answer the proposed research questions and achieve the research objectives, the thesis is carried out through the following 5 steps: (1) Building a theoretical framework, (2) Building a research model and method, (3) Assessing the current situation, (4) Analyzing research results, and (5) Solutions.

Figure 3.1. Research process

Source: Author's own construction

Step 1: Build a theoretical framework

The study builds a theoretical framework on audit quality and factors affecting the quality of financial statement audits of the State Audit Office based on the synthesis of theories from many domestic and international sources, especially based on the State Audit Office's Auditing Standards System. This is the general theoretical basis for building a research model in the next step.

Step 2: Build a model and research method

This is an important step and a tool for the research to achieve the set objectives. The research model is built based on the theoretical framework and research gaps that have been clarified in step 1. Based on the research model, appropriate research methods are selected. In addition to statistical, analytical, comparative and synthetic methods, qualitative and quantitative methods are two important methods used. In the qualitative method, the thesis conducts two types of questionnaires: (1) questionnaire for State Auditors to assess the quality of audits and factors affecting the quality of financial statements audits of banks conducted by the State Audit, (2) questionnaire for in-depth interviews with bank leaders about solutions to improve governance activities at banks based on audit reports. The survey data from the questionnaire will be processed and used in the quantitative method (linear regression method) to determine the factors affecting the quality of audits.

Step 3: Assess the current status of financial statement audit quality of banks conducted by the State Audit Office

Based on internal documents of the State Audit Office as well as through survey results, the study assesses the current status of financial statement audit quality of banks conducted by the State Audit Office in the period 2015-2019. From there, the study points out the successes as well as limitations and causes of the research problem.

Step 4: Analyze the results of the research model on factors affecting the quality of financial statement audits of banks conducted by the State Audit Office.

To identify and analyze factors affecting the quality of financial statement audits of banks conducted by the State Audit Office, the study used SPSS 26.0 software to run linear regression models.

Step 5: Solutions to improve the quality of bank audits conducted by the State Audit Office and management activities at banks

The research results in steps 3 and 4 will be the basis for research and proposal of some solutions to improve the quality of financial statement audits of banks conducted by the State Audit Office and management activities at banks based on audit reports in the near future.

3.2. Research model and research hypothesis

3.2.1. Research model

The basis for determining the groups of factors includes: Firstly, based on domestic and foreign studies on factors affecting the quality of financial statement audits presented in Chapter 2, typically the studies of DeAngelo (1981), Francis (2011), Knechel et al. (2013), and the audit quality models of FRC (2008), IAASB (2013); Secondly, based on the State Audit Standards System issued under Decision No. 02/2016/QD-KTNN dated July 15, 2016 of the State Auditor General; Thirdly, combined with the characteristics of financial statement audits at banks by the State Audit. Thus, a system of 12 factors (divided into 3 groups A, B, C) with 55 influencing criteria is built to determine the factors affecting the quality of financial statement audits of banks performed by the State Audit (See table 3.1)

Table 3.1. Factors affecting the quality of financial statement audits of banks conducted by the State Audit Office

Grouping

Factor | Symbol | Number of criteria | Source | |

A. Auditor factors (6 factors - 24 criteria) | 1. Professional capacity | Energy | 4 | DeAngelo (1981), Richard (2006), Boon et al. (2008), FRC (2008), IAASB (2013) |

2. Professional skills | Specialization | 4 | DeAngelo (1981), Boon et al. (2008), Maletta and Wright (1996), Balsam et al. (2203), FRC (2008), IAASB (2013) |

Maybe you are interested!

-

Detailed Results of Factors Affecting Commercial Banking Service Quality from 30 Managers

Detailed Results of Factors Affecting Commercial Banking Service Quality from 30 Managers -

Research Results on Factors Affecting the Quality of Auditing Financial Statements of Banks Conducted by the State Audit

Research Results on Factors Affecting the Quality of Auditing Financial Statements of Banks Conducted by the State Audit -

Factors affecting the quality of commercial banking services - 26

Factors affecting the quality of commercial banking services - 26 -

Group of Factors Belonging to Auditing Firms Affecting the Quality of Financial Statement Audits

Group of Factors Belonging to Auditing Firms Affecting the Quality of Financial Statement Audits -

Some Factors Affecting the Quality of Short-Term Loan Services for Business Customers of Commercial Banks

Some Factors Affecting the Quality of Short-Term Loan Services for Business Customers of Commercial Banks

3. Work experience | Experience | 5 | Carcello et al. (1992), Aldhizer et al. (1995), Behn et al. (1997), Boon et al. (2008), FRC (2008), IAASB (2013) | |

4. Compliance with State Audit standards | Week | 5 | Treadway (1987), Wooten (2003) | |

5. Professional discretion and information security | Thantrong | 5 | Carcello et al. (1992), Boon et al. (2008) | |

6. Integrity, independence and objectivity | Doclap | 4 | DeAngelo (1981), Richard (2006), Boon et al. (2008) | |

B. Factors belonging to the audit unit (3 factors - 15 criteria) | 7. Working conditions of KTVNN | DKLV | 6 | New Development |

8. Auditing Method/Procedure | method | 4 | Wooten (2003), FRC (2008), IAASB (2013), Francis (2011), Knechel et al. (2013) | |

9. Audit quality control system | KSCL | 6 | Cushing (1989), Francis (2011), Knechel and partner (2013) | |

C. External factors (3 factors - 12 criteria) | 10. Factors relating to audited banks | Bank | 6 | New Development |

11. Factors related to the legal environment for auditing activities | French | 4 | FRC (2008), IAASB (2013) | |

12. Other external factors | Other | 2 | IAASB (2013), Bui Thi Thuy (2014) | |

Total: 12 factors | 55 |

Source: Author's proposal