by the State Audit Office, solutions to improve and enhance the quality of financial statement audits.

+ Questions to evaluate factors affecting the quality of financial statement audits include 3 groups, 12 criteria and 55 questions. The content requires the survey subjects (KTVNN) to indicate their assessment of the level of influence of factors on the quality of audits of banks conducted by the State Audit, with a scale of influence level 1-5, in which 1- Very low, 2- Low, 3- Normal, 4- High, 5- Very high.

(b) In-depth interview questionnaire for leaders of banks audited by the State Audit Office (See Appendix 2)

Maybe you are interested!

-

Detailed Results of Factors Affecting Commercial Banking Service Quality from 30 Managers

Detailed Results of Factors Affecting Commercial Banking Service Quality from 30 Managers -

Research on factors affecting the quality of accounting information systems in Vietnamese traffic construction enterprises - 26

Research on factors affecting the quality of accounting information systems in Vietnamese traffic construction enterprises - 26 -

Research Results of Factors Affecting the Implementation of Management Accounting to Evaluate Operational Efficiency in Travel Enterprises

Research Results of Factors Affecting the Implementation of Management Accounting to Evaluate Operational Efficiency in Travel Enterprises -

Survey of Research Models on Factors Affecting the Decision to Use Internet Banking Services in the World.

Survey of Research Models on Factors Affecting the Decision to Use Internet Banking Services in the World. -

Factors affecting the quality of commercial banking services - 26

Factors affecting the quality of commercial banking services - 26

- The purpose of the questionnaire is to evaluate the quality of financial statement audits of banks conducted by the State Audit Office and solutions to improve management activities at banks based on audit reports.

- The content of the questionnaire is divided into 2 parts:

Part 1: Personal information such as full name, position, work unit, years of work experience.

Part 2: In-depth interview questions include

+ General questions about the quality of financial statement audits are assessed through 4 criteria and a scale of impact from 1 to 5, in which 1- Very low, 2- Low, 3- Normal, 4- High, 5- Very high.

+ Open-ended questions to interview bank leaders to assess the current status of financial statement audits of banks conducted by the State Audit from the perspective of the audited unit, how the results and conclusions of the State Audit affect the current management activities of banks; and based on the audit recommendations of the State Audit, how have banks conducted bank management activities?

3.4.2. Selecting survey subjects

The research sample for sending the survey form is the State Auditors who participated in audit teams or State Auditors who conducted quality reviews of bank audits in the period 2015-2019 and the leaders of 7 banks audited by the State Audit, including: Vietnam Bank for Agriculture and Rural Development (Agribank), Vietnam Joint Stock Commercial Bank for Investment and Development (BIDV), Vietnam Joint Stock Commercial Bank for Industry and Trade (Vietinbank), Vietnam Joint Stock Commercial Bank for Foreign Trade (Vietinbank).

Nam (Vietcombank), Vietnam Development Bank (VDB), Vietnam Bank for Social Policies (VBSP), and Vietnam Cooperative Bank (Co-opBank).

The reason for choosing the State Auditors as the survey subjects is because they are the ones who directly participate in audits or review the quality of bank audits, so they will be the ones with the most experience and understanding of the factors affecting the quality of their own performance. From there, there is a reliable assessment of the level of influence of the factors.

In addition, the subjects are leaders of banks including General Director/Deputy General Director or Head of the Board of Control selected for in-depth interviews with the aim of assessing the quality of financial statement audits from the perspective of satisfaction of users of audit results. From there, we can understand the impact of the results and quality of the State Audit on improving governance activities at banks based on audit reports.

The sample size applied in the study is based on the requirements of exploratory factor analysis (EFA) and multivariate regression which can be calculated in 2 ways as follows:

- First method: Based on the study of Hair, Anderson, Tatham and Black (1998) for reference on expected sample size. Accordingly, the minimum sample size is 5 times the total number of observed variables. This is the appropriate sample size for research using factor analysis (Comrey, 1973; Roger, 2006). n=5*m where m is the number of questions in the test.

- Second way : the minimum sample size required is calculated according to the formula n=50 + 8*m (m: number of independent variables) (Tabachnick and Fidell, 1996). In which: m is the number of independent factors

Thus, the minimum sample size of the study must be 275 ballots because the number of questions in the survey is 55 questions.

3.4.3. Data collection and processing methods

(a) Data collection method

- Collecting primary data: Primary data through questionnaires are conducted directly or indirectly via email/telephone interviews. The survey period is from November 2019 to March 2020. Results, research

Collected 275 response forms from the State Audit Office and 7 in-depth interviews with leaders of banks audited by the State Audit Office.

- Collecting secondary data: In addition to primary data, secondary data is also collected to assess the current status of the quality of financial statement audits of banks performed by the State Audit, including internal documents on audit quality, reports of the Department of Regime and Quality Control on auditing banks, the State Audit's System of Standards, documents and decisions of the State Auditor General related to audit quality in general and audit quality of banks in particular.

(b) Data processing method : After the survey form is collected and checked for information to ensure consistency, the data will be encoded, declared and entered into an Excel file.

CHAPTER 4: RESEARCH RESULTS ON FACTORS AFFECTING THE QUALITY OF AUDITS OF BANKS' FINANCIAL STATEMENTS PERFORMED BY THE STATE AUDITING OFFICE

4.1. Characteristics of financial statement audit activities of banks performed by the State Audit Office

4.1.1. General introduction to State Audit

4.1.1.1. Formation and development process

The State Audit of Vietnam was established under Decree No. 70/CP dated July 11, 1994 of the Government and operates under the Charter on the organization and operation of the State Audit issued together with Decision No. 61/TTg dated January 24, 1995 of the Prime Minister. The State Audit of Vietnam is a completely new agency, without a predecessor organization. Immediately after its establishment, the State Audit of Vietnam has formed an organizational structure, built facilities, recruited and trained staff and auditors, developed standards and auditing procedures and organized the implementation of auditing tasks assigned by the Government and the Prime Minister. The formation and development of the State Audit of Vietnam is an objective necessity that contributes to ensuring the allocation, management and use of state financial resources and public assets in a reasonable, economical and effective manner, preventing negative behaviors, corruption, waste of the state budget, money and assets of the state.

During its operation, the position of the State Audit has been recognized and affirmed by society, increasingly becoming a strong and effective tool of the State and the National Assembly in inspecting and supervising public finance and public assets. On June 14, 2005, the State Audit Law was passed by the 11th National Assembly and took effect from January 1, 2006, opening a new period of development of the State Audit. The Law clearly stipulates that " the State Audit is a specialized agency in the field of state financial inspection established by the National Assembly, operating independently and only complying with the law ", with the functions of auditing financial statements, auditing compliance, and auditing the activities of agencies and organizations managing the use of the State budget, money and assets. With the function of being the national public finance inspection agency, the State Audit Office conducts inspections and confirms the correctness and legality of the State budget settlement data and financial statements of state administrative agencies, enterprises and organizations and units that manage and use state financial resources. Through auditing activities, the State Audit Office provides audit results to the Government.

The National Assembly and State agencies aim to rectify and improve financial management. The State Audit also performs the function of advising and giving advice to audited units so that the quality of financial management can gradually be put into order; making recommendations to State management agencies and the Government to improve the mechanism and policies for financial management and the national budget.

Along with the increasing demand for auditing, it is necessary to improve the legal status and organizational structure of the State Audit. The Standing Committee of the National Assembly has affirmed that the development strategy of the State Audit must thoroughly grasp the following viewpoints:

- Develop the State Audit into an important and effective tool of the Party and State in inspecting and controlling the management and use of the State budget, money and assets; effectively supporting and serving the activities of the National Assembly and People's Councils at all levels in performing the function of supervision and deciding on important issues of the country and localities.

- Developing the State Audit Office ensures thorough understanding and conformity with the Party's viewpoints, policies and guidelines; complies with the provisions of the State's legal system and ensures independence of State Audit Office activities in order to fully perform the functions and tasks of the State Audit Office according to the provisions of law, increasingly better meeting the requirements of managing the State budget, money and assets in the renovation process.

- The development of the State Audit must ensure the thorough understanding of the viewpoints on administrative reform in general and public finance reform in particular, and determine a reasonable scale in each period to meet the requirements of assigned tasks. Step by step build a professional, modern State Audit agency, develop reasonably in quantity and improve in quality, pay great attention to quality, streamline the apparatus, save costs, and operate effectively. Widely apply modern information technology in management and auditing activities.

- The State has policies to appropriately prioritize necessary resources for the organization and operation of the State Audit Office, policies to invest in information technology development, and policies to support training to meet the requirements of international integration.

- The development of the State economy must meet the requirements of international economic integration, in accordance with international principles and practices and the practical conditions of Vietnam.

With that development perspective, the 2013 Constitution stipulated the legal status of the State Audit Office and the State Auditor General in Article 118, marking a turning point in the development path of the State Audit Office.

(a) The State Audit Office is an agency established by the National Assembly, operates independently and only complies with the law, and conducts audits of the management and use of public finance and assets.

(b) The State Auditor General is the head of the State Audit Office, elected by the National Assembly. The term of office of the State Auditor General is prescribed by law. The State Auditor General is responsible for and reports on audit results and work to the National Assembly; during the time the National Assembly is not in session, he is responsible for and reports to the National Assembly Standing Committee.

(c) The specific organization, tasks and powers of the State Audit Office are prescribed by law.

This important event has elevated the State Audit Office from a “Law-prescribed” agency to a “Constitutional” agency; at the same time, it also requires enhancing the role and responsibility of the State Audit Office for the country's socio-economic development, commensurate with its status as an independent constitutional agency.

Along with the 2013 Constitution, the 2015 State Audit Law was promulgated by the National Assembly. This law applies to agencies and organizations managing and using public finance and public assets, the State Audit, other agencies, organizations and individuals related to State Audit activities and takes effect from January 1, 2016. This proves that the formation and development of the State Audit agency to perform the function of inspecting public finance and public assets is in accordance with objective laws, in accordance with the process of integration and economic development of the country with the region and the world.

According to the 2015 State Audit Law, the function of the State Audit is to evaluate, confirm, conclude and make recommendations on the management and use of public finance and public assets. In which:

Public finance includes: State budget; national reserves; extra-budgetary state financial funds; finances of state agencies, people's armed forces units, public service units, service and public goods providers, political organizations, socio-political organizations, socio-political-professional organizations, social organizations, socio-professional organizations using state funds and budgets; state capital in enterprises; public debts.

Public assets include: land; water resources; mineral resources; resources in the sea and airspace; other natural resources; state assets at state agencies, people's armed forces units, public service units, political organizations, socio-political organizations, socio-political-professional organizations, social organizations, socio-professional organizations; public assets assigned to enterprises for management and use; state reserve assets; assets of infrastructure serving public interests and other assets invested in and managed by the State under the ownership of the entire people, represented by the State as the owner and uniformly managed.

4.1.1.2. Organizational structure

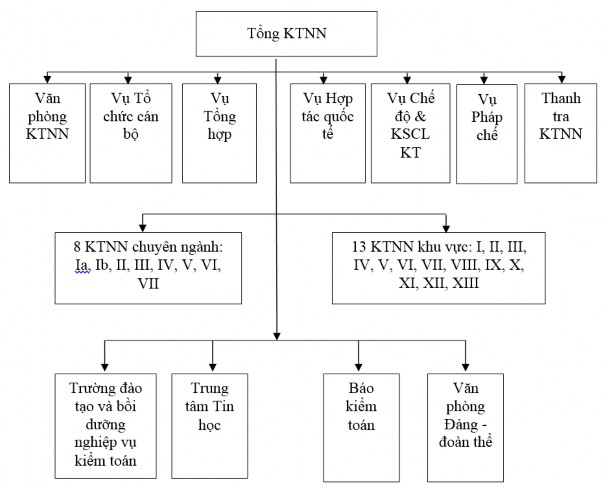

The State Audit Office is organized and managed in a centralized and unified manner, including: the executive apparatus, specialized State Audit Offices, regional State Audit Offices and public service units. The Standing Committee of the National Assembly specifically regulates the organizational structure of the State Audit Office. The State Auditor General specifically regulates the functions, tasks, powers and organizational structure of the units under the State Audit Office. The number of specialized State Audit Offices and regional State Audit Offices in each period is determined on the basis of task requirements submitted by the State Auditor General to the Standing Committee of the National Assembly for decision. Currently, the organizational structure of the State Audit Office includes 32 Departments and units equivalent to Department level as shown in Diagram 4.1.

Each unit has functional departments to perform its tasks. The State Audit Office has its own seal; the regional State Audit and public service units have legal status, their own seals, accounts and headquarters.

Specialized State Audit Offices conduct specialized audits of central agencies and organizations; regional State Audit Offices conduct audits of local agencies and organizations in the region and other audit tasks assigned by the State Auditor General.

Figure 4.1. Organizational structure model of State Audit

Source: Author's own compilation

4.1.1.3. Department of Audit Regime and Quality Control

According to Decision No. 146/QD-KTNN dated February 18, 2014, regulating the functions, tasks, powers and organizational structure of the Department of Regimes and Audit Quality Control, the Department of Regimes and Audit Quality Control is a unit under the State Audit with the function of advising the State Auditor General on the work of developing, promulgating, guiding, inspecting and organizing the implementation of documents on standards, procedures and professional methods of State Audit; the work of developing and promulgating documents guiding and directing professional and internal audit; organizing audit quality control.

In the audit quality control work, the Department of Audit Regime and Quality Control performs a number of tasks as follows: