Borrowers create different types of credit risks that can be compared and monitored based on internal credit ratings for customers in different sectors and industries. Banks must have clear processes for credit approval, credit amendments with the participation of marketing departments, credit analysis departments and credit approval departments as well as clear responsibilities of participating departments, and need to develop a team of experienced and knowledgeable credit risk management staff to make prudent judgments in assessing, approving and managing credit risks.

- Maintain a suitable credit management, measurement and monitoring process (10 principles): Banks need to have an up-to-date management system for credit risk portfolios, including updating credit records, collecting current financial information, drafting documents such as loan contracts... according to the size and complexity of the bank. At the same time, this system must be able to grasp and control the financial situation, compliance with customer contracts... to promptly detect problem loans. Banks need to have a system to promptly handle bad loans and manage problem loans.

1.6. Experience of some countries in the world to ensure safety for loans and lessons for Vietnamese commercial banks

1.6.1. Experience of some countries in ensuring loan safety

1.6.1.1. Thailand's experience

After the financial crisis in 1997 and 2008, Thailand is one of the countries that has gained a lot of experience in the issue of risk management of banks. On that basis, Thailand has built an effective measurement and evaluation system to control and minimize possible risks. One of the solutions can be listed as follows:

- The valuation of collateral is agreed upon between the bank and the borrower or by an intermediary organization. Based on the valuation of the collateral, an appropriate provision is made for the loan. In necessary cases such as when a crisis occurs, the Government will establish a financial recovery and development fund, then use that money to prioritize buying shares of banks. In order to

- Investment limit is 10% of borrower's capital and 20% of Bank's capital. Loan limit for customer groups is 5% of Bank's capital, 50% of enterprise's net worth and 25% of debt value. Loan limit for individual customers is 25% of Bank's equity. 5

- The credit information bureau is managed by a private company, all banks report information to the bureau, then the information bureau renders reports on borrowers and loan repayment history every month, does not provide credit appraisal information.

1.6.1.2. China's experience

In China, since the implementation of strong banking system reforms in 1998, the banking system has made significant progress, with the value of assets and profits of banks always increasing. This is due to the important reforms by the government and the China Banking Regulatory Commission to ensure safety in lending activities in particular and credit risk management in general.

- China has issued safety indicators according to Basel II international standards applied to activities to manage risks, ensuring the banking system operates strongly.

- The previous method of setting aside reserves for loans of around 1% and not taking into account risk factors has been replaced by classifying loans into 5 categories based on loan size and quality.

5 Luong Duc Thanh (Thesis - 2006), Ensuring credit safety at the Bank for Foreign Trade of Vietnam.

- Set criteria for loan limits. Limit loans to partners at 5% of the enterprise's net worth. Total outstanding loans to partners must not exceed 10% of the bank's equity. Limit loans to individual customers at 25% of the bank's equity.

- Using the CAMEL model (capital, assets, management, earnings, liquidity) to check and evaluate the operational efficiency of banks.

- Create a synchronous legal and economic environment for banking operations.

1.6.1.3. Singapore's experience

Singaporean banks have a very modern business management perspective, which is banking management based on risk management, effective asset and liability management to achieve maximum profit and ensure safety in banking operations and lending operations in particular. In 2010, Singapore was ranked as one of the top ten financial centers in the world 6 . To reach the top, financial institutions and banks in particular need to operate stably and increasingly strongly based on safety assurance and improved risk management. One of the lessons that countries with underdeveloped financial systems like Vietnam must learn is:

- The assessment of lending risk from customers is mainly carried out by independent credit rating companies such as Moody's or Standard & Poor's. Therefore, based on those measurements, banks will make appropriate lending decisions.

- Banks are not allowed to engage in non-financial activities. They are also not allowed to invest more than 10% of their capital in companies operating non-financial activities. The amount of capital investment in a single company is limited to 2% of the Bank's equity capital. Total investment is limited to 10% of the Bank's equity capital.

6 http://dantri.com.vn/c25/s76-224428/10-trung-tam-tai-chinh-hang-dau-the-gioi.htm

- The unit that organizes and manages credit information from borrowing members is managed by the Banking Association. This facilitates banks in updating customer information for future loans, thereby reducing costs and time in assessing and evaluating borrowers.

1.6.2. Lessons learned for Vietnamese commercial banks

Banking activities are intermediary activities to mobilize capital for lending, therefore, only by ensuring the safety of customers' loans can we limit the liquidity risk, credit risk, etc. of the bank. From studying the experiences of some countries in ensuring safety in lending activities, we can draw some lessons for Vietnamese commercial banks as follows:

- First : Safety ratios in credit activities in general and in lending activities in particular are always strictly regulated and required for commercial banks to comply. The State Bank of Vietnam needs to issue specific regulations as a roadmap for banks to comply with safety ratios. In case of failure to meet the conditions for ensuring safety in lending activities, it is necessary to merge or cease operations.

- Second: To ensure safety in lending activities, commercial banks must select and screen customers, diversify lending objects because currently they still focus mainly on state-owned enterprises and large corporations, so the risk is very high. It is necessary to require customers to borrow capital with 20% to 30% of their own capital, closely monitor loans before, during and after lending. Resolutely handle debts due and proactively set aside provisions according to the regulations of the State Bank. It is necessary to attach importance to information work.

7 Nguyen Tien Chuong (Thesis - 2008), Improving the effectiveness of credit risk management of Vietnam Joint Stock Commercial Bank for Foreign Trade.

customers to grasp information well and promptly handle situations that arise.

- Third: Capital investment and debt restructuring policies are popular in many countries; in capital investment policies and lending strategy development, it is necessary to clearly identify priority sectors and fields, the trend is to select customers and switch to lending according to projects and feasible business plans.

In the process of reviewing and re-evaluating debt and restructuring debt, commercial banks need to boldly recognize and assess the actual quality of debt in order to have appropriate responses to ensure system safety.

- Fourth: When a commercial bank becomes insolvent due to the impact of loan repayments, countries have used many measures to prevent the bank from going bankrupt, such as increasing equity capital, and the State Bank lending to establish development support funds and financial recovery. This is a valuable experience that Vietnamese banks need to learn and apply when necessary.

- Five: Boldly introduce and apply accounting and auditing standards according to international standards. Control, supervision and internal inspection are effective measures in all economic situations. Depending on each specific situation, appropriate forms and inspections should be applied.

CHAPTER 2: SAFETY STATE IN

LENDING ACTIVITIES AT THE BANK FOR INVESTMENT AND DEVELOPMENT OF VIETNAM

2.1. General introduction to Vietnam Development and Investment Bank

2.1.1. The birth and development of the Bank for Investment and Development of Vietnam(BIDV)

BIDV Bank was established under Decision No. 177/TTg dated April 26, 1957 of the Prime Minister with the name of Vietnam Construction Bank. During the process of construction and development, BIDV was given many different names such as: Vietnam Construction Bank: April 26, 1957; Vietnam Investment and Construction Bank June 24, 1981 ; Vietnam Investment and Development Bank November 14, 1990.

Since its establishment and development, BIDV Bank has always affirmed its role in the economic recovery and development. During 37 years (1957-1994), it was the only bank to provide management and loans for basic construction capital through its operations. The bank has contributed to the effective management of investment projects.

Since 1990, implementing the Party and State's renovation policy, in addition to the State budget, the bank has proactively mobilized medium and long-term capital to meet the capital needs for economic reform. BIDV's capital has been invested in many key projects and important fields such as electricity, telecommunications, transportation, cement, etc. During the years of renovation, especially the period of completely shifting to business from 1995 to present, BIDV Bank has made continuous efforts by expanding many capital mobilization channels: from residents, businesses, syndicated loans, import-export financing loans, participating in the stock market, issuing

bonds... Along with diversifying its operations, BIDV Bank has also continuously transformed its service structure to meet the diverse needs of customers, in addition to gradually participating in non-banking fields such as securities insurance, office business and commercial centers. On the other hand, BIDV Bank's business activities also focus on human resource development, and BIDV Bank's staff has continuously grown in quantity and quality.

After 53 years of establishment and development, BIDV Bank has become one of the leading commercial banks in Vietnam with total assets reaching 242,317 billion VND by the end of 2008. Having changed its name twice and witnessed many ups and downs of the economy, BIDV Bank has always fulfilled its tasks excellently and affirmed its leading role in serving investment and development.

2.1.2. Organizational model of the Bank for Investment and Development of Vietnam

In September 2008, BIDV officially operated the new organizational model at the Head Office and specifically implemented the organizational model conversion at the branches, basically meeting the requirements:

- Achieve the goal of transforming from a traditional banking model to a modern, multi-functional commercial bank model oriented towards expanding retail banking activities, creating a foundation for centralizing operations and strengthening centralized management at the Head Office.

- Established an organizational structure following international practices to meet risk management requirements; most operations, especially credit operations, have been implemented and controlled through 3 stages: Proposal - Risk management/ Approval - Operation.

- The conversion has a roadmap and steps that are relatively suitable to the capabilities and actual conditions, promoting BIDV's traditional operations.

Promote the implementation of new operations and products as well as implement the core principles and recommendations of TA2 project consulting.

With the drastic restructuring of the system's operations, BIDV has prepared to equitize the bank and move towards a modern, multi-functional financial group model including 34 departments and centers and divided into 7 functional blocks: Retail Banking Block (4 departments), Retail Banking and Network Block (3 departments), Capital and Capital Trading Block (1 department), Risk Management Block (3 departments), Operations Block (3 departments), Finance - Accounting Block (3 departments) and Support Block (6 departments).

At the grassroots level, BIDV includes 108 branches, arranging and adjusting the functions and tasks of Departments/Groups according to a model designed with 5 blocks:

- Customer Relations Block includes: Customer Relations Departments; Project Finance Department/Team.

- Risk Management Block includes: Risk Management Department.

- Operational Block includes: Credit Management Department, Customer Service Department, Treasury Management and Services Department/Team, International Payment Department/Team.

- Internal Management Block includes: Planning - Synthesis Department, Computer Department/Team, Finance - Accounting Department, Organization - Human Resources Department, Office.

- Affiliated blocks include: Transaction Offices and Savings Funds.

Source: Annual Report 2008 - BIDV

2.1.3. Business performance of the Investment and Development Bank

Vietnam development in 4 years 2005 - 2009

During the years 2005-2008, BIDV Bank continued to achieve significant financial improvements. In particular, by the end of 2008, the deadline for state-owned commercial banks to complete the legal capital of 3,000 billion VND according to Decree No. 141/2006/ND-CP issued by the Government on November 22, 2006 expired. The process of raising charter capital was of course actively implemented by BIDV Bank since 2007, when the economy was still growing strongly. In 2008, the economic crisis occurred, the situation was no longer as favorable as before, however, the Bank made efforts and achieved the required capital level on time.

2.1.3.1. Size of Total Assets and Equity

As of December 31, 2009, the Bank's equity reached VND 11,657 billion, equivalent to USD 687 million, an increase of 16.9% compared to 2008 and an increase of 38.7% compared to 2007.

Table 2.1: Growth scale of total assets and equity of BIDV

Unit: billion VND.

Size and growth

2009 | 2008 | 2007 | 2006 | |

Total assets | 300,214 | 242,316 | 204,511 | 161,223 |

Equity | 11,657 | 9,969 | 8,405 | 4,428 |

Credit Center | 194,361 | 154,176 | 126,616 | 98,453 |

Maybe you are interested!

-

Government's financial and monetary policies for the development of small and medium enterprises. Experiences of countries around the world and lessons for Vietnam - 13

Government's financial and monetary policies for the development of small and medium enterprises. Experiences of countries around the world and lessons for Vietnam - 13 -

Land Clearance and Resettlement Policies of Some Countries in the World

Land Clearance and Resettlement Policies of Some Countries in the World -

Assessment of the World Trade Organization's Dispute Settlement Mechanism for Developing Countries

Assessment of the World Trade Organization's Dispute Settlement Mechanism for Developing Countries -

Research Projects of Regional and World Countries

Research Projects of Regional and World Countries -

Experience in Limiting Risks in Banking Credit Activities of Some Countries in the World

Experience in Limiting Risks in Banking Credit Activities of Some Countries in the World

Source: Compilation of Annual Report – BIDV and Fitch Ratings 2009 report

In addition, BIDV's asset size grew with a reasonable structure. Specifically, BIDV's total assets reached VND300,214 billion, equivalent to USD17.8 billion, holding the second position in the domestic market after the Vietnam Bank for Agriculture and Rural Development. Total assets in 2009 grew by 23.9% compared to 2008 and decreased slightly compared to the average growth rate of 27% in the period from 2004-2007 due to the increasing scale of total assets. And accounted for

The largest proportion of total assets is still credit activities with 64%. This is the activity that brings the main income to the bank.

With such asset growth, BIDV is increasingly demonstrating its strong position in the system of state-owned commercial banks in particular and Vietnamese commercial banks in general.

2.1.3.2. Market share of capital mobilization and lending

Over the years, BIDV has continuously promoted capital mobilization to meet the needs of customers. Capital sources have continuously increased due to the process of expanding the network and implementing many effective forms of capital mobilization.

Chart 2.1. Deposit market share of Vietnamese commercial banks in 2009

Source: Synthesis of some comparative indicators of State-owned commercial banks in 2009 – Vietnam Credit

Capital mobilization activities of Vietnamese commercial banks mainly come from the population, BIDV is no exception. Second only to AGB (22.4%) in terms of deposit mobilization market share with 14.2%, BIDV is increasingly affirming its position in the commercial banking system in Vietnam.

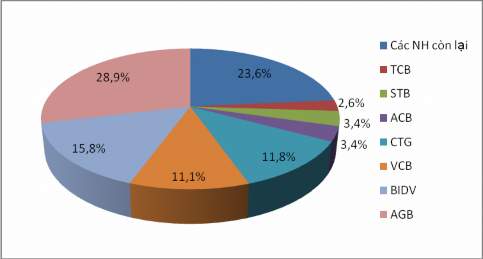

Meanwhile, BIDV's lending market share is 15.8%, ranking second after AGB with a rate of 28.9%. With credit activities being the main area bringing profits to the bank, BIDV has always focused on quality.

loans based on customer assessment and appraisal with strict management supervision. In recent years of implementing the banking restructuring project funded by the World Bank (WB), BIDV has expanded its lending to non-state-owned enterprises, and selected a number of strategic customers and partners to sign comprehensive cooperation agreements to bring about sustainable development in all aspects of operations. However, BIDV still has to regularly control the growth rate of outstanding credit in conjunction with safety and efficiency to ensure credit safety and achieve optimal profit structure in business.

Chart 2.2. Lending market share of Vietnamese commercial banks in 2009

Source: Synthesis of some comparative indicators of State-owned commercial banks in 2009 – Vietnam Credit

2.1.3.3. Interest income and non-interest income

According to the annual report results, BIDV's income is still mainly derived from credit activities - which is a traditional business activity of a bank. However, such income structure is inherently risky and does not ensure sustainable development for the bank. Credit activities are highly dependent on objective conditions. When the economy is growing strongly, businesses have a high demand for loans for production and business, credit will be narrowed, significantly reducing the bank's revenue. Therefore, BIDV is

tend to develop retail banking operations to promote the provision of diverse services to customers. In addition, it also increases income from foreign exchange trading, trading securities or contributing to the purchase of shares.

Table 2.2. BIDV's income structure

Unit: billion VND

Year

Structure

2007 | 2008 | |||

Amount | Proportion | Amount | Density | |

1. Net income from interest | 4,851 | 61.8% | 6,228 | 73.1% |

2. Non-interest net income | 1,138 | 14.5% | 1,492 | 17.5% |

+ Service activities | 624 | 8.0% | 1,003 | 11.8% |

+ Foreign exchange trading activities | 140 | 1.8% | 791 | 9.3% |

+ Trading securities activities | 144 | 1.8% | (723) | -8.5% |

+ Capital contribution activities to buy shares | 17 | 0.2% | (8) | -0.1% |

+ Other activities | 213 | 2.7% | 429 | 5.0% |

3. Collection of off-balance sheet debt | 1,856 | 23.7% | 799 | 9.4% |

4.Total operating income | 7,845 | 100% | 8,520 | 100% |

Source: Annual Report 2008 – BIDV

Not only did it achieve growth in scale, but the structure of income from activities also showed positive changes. The highlight was the growth in revenue and the proportion of non-credit activities. In 2008, net revenue from services and foreign exchange trading reached 1,794 billion, an increase of 764 billion (~134%) compared to 2007, contributing to raising the proportion of revenue from non-credit activities from 14.5% in 2007 to 17.5% of total income. The proportion of extraordinary operating income (off-balance sheet debt collection) decreased to only 9.4% (23.7% in 2007), showing that BIDV's income mainly comes from core business activities with the potential for sustainable growth.

2.2. Current status of safety assurance in BIDV's lending activities

2.2.1. Safety in lending activities

The lending activities of the Bank for Investment and Development of Vietnam have made significant progress after 9 years of implementing the restructuring project, from mainly lending for investment and development according to the state plan to now BIDV has become a multi-functional bank, lending to all economic sectors. BIDV has become an important capital supply channel for the economy and a destination for many businesses.

2.2.1.1. Lending activities situation

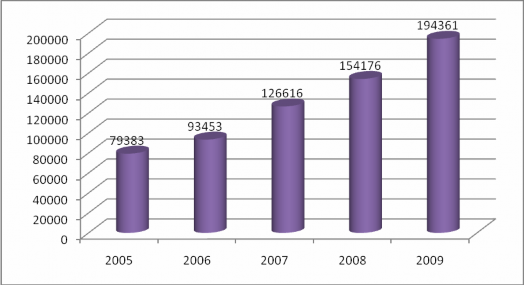

Total outstanding loans of the entire system as of December 31, 2009 reached: 194,361 billion VND, an increase of 26.1% compared to 2008. Credit market share in the entire industry in 2009 was 12.9%, an increase of 0.9% compared to 2008 (12%); second only to AGB with a loan market share of up to 28.86%. 8

Chart 2.3. BIDV's loans and advances to customers (net) in the period 2005 - 2009

Unit: Billion VND

Source : Annual report and summary report – BIDV

8 Source: MHBS compiled from financial reports of banks.

Credit structure continued to improve in a positive direction, total outstanding loans to total assets in 2008 reached 64%, an increase of 6.4% compared to 2007. The proportion of medium and long-term loans reached 40.5%. The proportion of outstanding loans in foreign currencies reached 20.1%. If including outstanding loans in VND converted to USD, the proportion of outstanding loans in foreign currencies reached 21.7%.

a/ Loan structure by ownership form

In order to facilitate the integration and development process, in recent years BIDV has shifted its credit structure in a positive direction to fulfill its commitments to the World Bank and the Bank's overall development plan until 2020. The credit structure is implemented in the direction of reducing the proportion of medium and long-term loans, changing the perspective on the objective approach to non-state economic sectors, focusing on prioritizing investment in projects for the electricity, coal, cement, shipbuilding industries... in addition to adjusting the credit structure that has been invested in the textile, construction, oil and gas industries...

Table 2.3. Outstanding loans by economic sector

Unit: billion VND

Year

Target

2007 | 2008 | 2009 | ||||

Amount | % | Amount | % | Amount | % | |

National economy business | 70,542 | 55.7% | 80,788 | 52.4% | 98,346 | 50.8% |

External economy state-owned | 40,429 | 31.9% | 53,345 | 34.6% | 70,359 | 36.2% |

Enterprises with investment capital foreign | 15,645 | 12.4% | 20,043 | 13% | 25,656 | 13, % |

Total | 126,616 | 100% | 154,176 | 100% | 194,361 | |

Source: Annual report and summary report – BIDV

Looking at the table above, we can see that although BIDV has been proactive in restructuring its lending to fulfill the World Bank's commitments, its credit activities are still mainly focused on the economic sector.