According to the 2012 report, DATC achieved total revenue of 492 billion VND, equal to 109% of the plan; pre-tax profit was estimated at 184 billion VND, reaching 122% of the plan.

In debt trading activities, in 2012, the Company signed 17 contracts with debt value of 705 billion VND. Accumulated from 2008 to 2012, DATC implemented 128 debt trading plans in the form of agreement and appointment to handle financial restructuring of enterprises and debt recovery. The book value of the debts was 8,579 billion VND, the recovery rate reached 106.5% compared to the debt purchase price.

In the debt trading activities associated with corporate restructuring in 2012, the Company successfully traded debts, handled finances, and restructured 9 enterprises, including converting 5 SOEs into joint stock companies and restructuring 4 joint stock enterprises, which were equitized from SOEs. Accumulated from 2008 to 2012, DATC purchased debts, handled finances, and restructured 54 enterprises, including successfully converting 28 enterprises into joint stock companies and restructuring 26 joint stock enterprises, which were equitized from SOEs.

In the work of handling assets and recovering debts excluded from the enterprise value when equitizing state-owned enterprises, in 2012, the Company signed the minutes of handover and receipt of assets and debts excluded from the enterprise value when equitizing state-owned enterprises, with the receipt value of 97 billion VND. Accumulated from 2008 to 2012, DATC received assets and debts excluded from the enterprise value when equitizing state-owned enterprises of 2,410 enterprises (including 976 central enterprises and 1,434 local enterprises), with the receipt value of 3,379 billion VND.

Maybe you are interested!

-

Bad Debt Management Vietnam Joint Stock Commercial Bank for Industry and Trade

Bad Debt Management Vietnam Joint Stock Commercial Bank for Industry and Trade -

Bad debt management at Lao People's Democratic Republic Commercial Bank 1669778721 - 30

Bad debt management at Lao People's Democratic Republic Commercial Bank 1669778721 - 30 -

Bad debt management at Vietnam Joint Stock Commercial Bank for Industry and Trade - Thang Long Branch - 14

Bad debt management at Vietnam Joint Stock Commercial Bank for Industry and Trade - Thang Long Branch - 14 -

Credit risk management at Vietnam International Commercial Joint Stock Bank - Hanoi Branch - 12

Credit risk management at Vietnam International Commercial Joint Stock Bank - Hanoi Branch - 12 -

Factors affecting the debt repayment ability of corporate customers at Vietnam Joint Stock Commercial Bank for Investment and Development - Long An Branch - 1

Factors affecting the debt repayment ability of corporate customers at Vietnam Joint Stock Commercial Bank for Investment and Development - Long An Branch - 1

Some successful debt trading deals that DATC has participated in: DATC purchased 180 billion VND of NQH from banks, erased a portion of the debt payable corresponding to the negative equity for Sadico to balance its finances, participated in consulting and discussing solutions for Bianfishco and SHB to restructure the Company, Kontum Sugar Joint Stock Company and Son La Sugar Cane Joint Stock Company were restructured by DATC and have been operating normally...

DATC has helped speed up debt trading activities, helping commercial banks quickly handle a large volume of outstanding debt, contributing to improving and enhancing financial capacity to

Prepare for equitization, enhance the safety of the banking and financial system in the process of reform and integration. Enterprises have the conditions to continue operating, restore the ability to repay debts to banks.

On July 29, 2013, the Debt and Asset Trading Company (DATC) held a signing ceremony of a Cooperation Agreement with the Korea National Asset Management Company (Kamco). Cooperating with Kamco in debt settlement activities helps DATC learn and accumulate more experience in the process of operation and development.

2.2.3.7 Establishment of debt management and asset exploitation companies

Debt management and asset exploitation have always received special attention from commercial banks. Each commercial bank has policies, systems and risk management processes. However, the establishment of AMCs to specialize in debt management, bad debt handling and restructuring of bank debts is a practical and essential need. Therefore, AMCs were established with the following main purposes:

- To professionalize the management and handling of overdue debt of the entire system;

- Contribute to handling bad debt quickly and effectively; Restructuring outstanding debt, taking over management of outstanding debts of banks by measures: debt extension, interest rate exemption and reduction, additional investment, converting debt into contributed capital...

- Gradually develop debt trading activities; asset management and trading (leasing, buying and selling, exploitation)

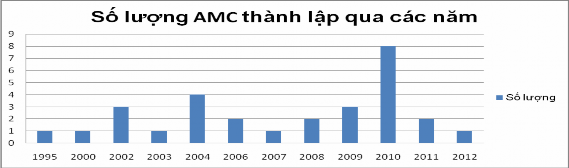

According to statistics, by the end of 2011, there were 27 AMCs under commercial banks. AMCs under commercial banks operate under the model of single-member LLCs.

Figure 2.8: Number of AMCs established up to 2012

Unit: Company

Source: statistics of State Bank of Vietnam

In addition, there is an AMC under the Ministry of Finance, DATC, and many private/joint stock companies were established to perform some functions of the AMC such as: consulting on debt collection procedures, debt settlement, debt collection, etc.

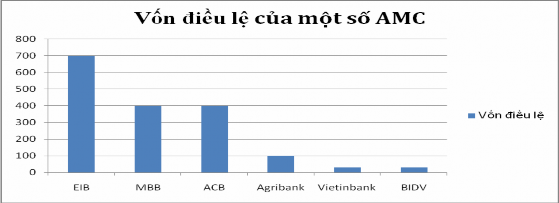

Figure 2.9: Charter capital of some AMCs upon establishment

Unit: billion VND

Source: statistics of State Bank of Vietnam

By the end of 2012, debt settlement activities of AMCs still achieved many positive results, many bad debts were handled, significantly reducing the bad debt balance at AMCs.

Commercial banks. AMCs support banks in implementing debt settlement measures such as filing lawsuits, auctioning assets, and proposing debt settlement plans for each customer. In 2012, ACBA (ACB Debt Management Company) handled about 100 billion bad debts by applying measures such as filing lawsuits, auctioning assets, etc.

However, many AMCs were established whose main job was not to manage debt, handle debt or manage assets, but to legalize lending at interest rates exceeding the ceiling of commercial banks. Some AMCs did not apply a combination of debt handling methods but only focused on foreclosing assets and then filing lawsuits, so the effectiveness was not high.

The number of AMCs also decreased, by the end of 2012 there were only about 20 AMCs in operation. At the same time, the scale of AMCs is not proportional when the capital of AMCs is only a few hundred billion. Besides, AMCs with high charter capital mainly belong to joint stock commercial banks such as Eximbank, ACB, MBB while state-owned commercial banks do not really participate such as CTG, VCB, Agribank, BIDV (charter capital under 100 billion).

On the morning of July 26, 2013, at the Headquarters of the State Bank of Vietnam (SBV), the inauguration ceremony of the Vietnam Asset Management Company (VAMC) with a charter capital of VND500 billion was held. The establishment of VAMC will help SBV have another tool to handle bad debts. The goal set for VAMC in 2013 is to handle VND40,000 - 70,000 billion of bad debts. Specifically, in September 2013, VAMC will buy about VND10,000 billion of bad debts from commercial banks by issuing special bonds. Currently, there is one commercial bank that has agreed to sell bad debts to VAMC for about VND1,500 billion, that is ACB.

2.2.3.8 Debt restructuring and debt forgiveness.

Debt restructuring means lending new loans to pay off old debts. Thus, the total outstanding debt remains unchanged, but the time of the loan may change, leading to a change in the time of debt repayment. Debt restructuring helps banks “clean up” as well as “virtually improve” the credit quality of loans. Debt restructuring loans make bad debts not reflect the true nature.

As mentioned, debt restructuring loans are just a way to beautify the indicators. Therefore, some commercial banks have decided to continue debt forgiveness. Debt forgiveness is a form of temporary suspension of the obligation to repay the remaining debt of the borrower, until at some point in the future, the debt will continue to be paid as agreed in the old loan contract. At the same time, the bank will continue to provide capital to businesses to restore business, complete investment projects to create a source of money to repay the bank.

In 2013, the State Bank also said that banks need to pay attention to debt forgiveness measures. Banks need to carefully consider the customer's situation. If they see that the customer is still capable of recovering production and business, they will continue to provide capital. When the business develops, the bank will have the opportunity to recover the capital. This requires that the financial statements of businesses must be transparent and must be audited by an independent organization. This is a difficult problem for Vietnamese businesses because the costs are high, and at the same time, the audit will expose all weaknesses.

2.2.3.9 Debt collection from handling secured assets

Collateral will become the next source of debt recovery for commercial banks when customers are no longer able to repay their debts to the bank. The methods of handling collateral often applied by commercial banks are:

Persuade customers to liquidate their mortgaged or pledged assets to pay off debts by advertising assets for sale in newspapers, real estate companies under commercial banks, and brokering for customers in the system when needed...

If the customer is not willing and commits fraud, the bank will proceed to auction the property through lawsuits and transfer the property to an auction center. This is usually done by AMCs under commercial banks.

For collateral assets such as valuable papers, savings books, term deposits, the bank relies on the authorization commitments in the credit contract.

used to collect debt. For assets mortgaged for receivables and inventories, the bank can, based on the factoring contract or inventory mortgage contract, take measures to keep the warehouse for use, or request the buyer to repay the debt.

The bank can also buy back the real estate collateral used as the business headquarters. Other collateral assets will be bought back at market price and with the customer's consent.

Most of the bank loans are secured by real estate. However, with the current state of the real estate industry, it takes several years to process a real estate. The amount of bad debt processed from liquidation of collateral assets is only 10% of the total bad debt processed.

In 2012, with Project 254 on the Government buying back some projects and real estates that are mortgaged to banks that are about to be completed or have been completed but not yet sold, in order to serve the purpose of social security and the operations of state agencies, it will be possible to handle some of the real estates currently mortgaged at commercial banks.

2.2.3.10 File a lawsuit according to the provisions of law

After applying all debt restructuring measures and reducing interest rates for customers but the customers still cannot repay the debt, and the secured assets have not been put up for sale during the debt settlement period, the commercial bank will initiate a lawsuit according to regulations. The commercial bank will also initiate a lawsuit when it discovers cases of risks such as customers avoiding debt repayment responsibilities, intentionally defrauding, absconding, businesses dissolving and going bankrupt, etc. This is a civil case due to disputes over the rights and obligations of the parties in the credit contract, with the purpose of debt recovery. However, the processing time of lawsuits is often very long due to many cumbersome procedures and processes, low debt recovery rates due to handling the assets of the business in the form of auctioning off assets (with a roadmap for reducing the selling price) and paying court fees. Another issue that deserves attention is that the legal corridor on debt collection lawsuits still has many loopholes. A typical example is that at the end of 2012, Military Bank

The team (MB) initiated proceedings to sue a customer to seize and dispose of the collateral to recover debt. Previously, this customer had settled abroad (Canada). The court returned the lawsuit to the bank on the grounds that it did not meet the conditions for filing a lawsuit because one of the conditions was that the plaintiff must provide the defendant's address.

2.2.3.11 Debt cancellation for customers

The fact that banks carry out debt forgiveness will cause banks' profits to decrease, which can cause losses and reduce the banks' equity. However, this is still a measure applied by commercial banks in debt settlement. Banks will write off debts for irrecoverable credits or special cases as directed by the Government and the State Bank. Banks also consider writing off debts where the cost of recovery is greater than the value of the debt that can be recovered. Banks have had to account for huge losses due to recording costs arising from writing off debts for customers.

2.2.3.12 Conducting mergers and consolidations of commercial banks

The Vietnamese banking system has experienced a period of hot credit development of banks, which has led to an increase in bad debts, and some banks are at risk of losing liquidity. Therefore, the merger and consolidation of weak commercial banks is a necessary task. After a series of arrangements, mergers and acquisitions with initial results, helping the banking industry overcome difficulties and making the financial system healthy. Since then, mergers and consolidations have been considered an important stage in the restructuring process to ensure competitiveness and reduce bad debts in a volatile economic environment. The first bank merger was the voluntary merger of three banks: De Nhat Bank, Vietnam Tin Nghia Bank, and Saigon Commercial Joint Stock Bank. After 1 year of merger, SCB had a profit of 82 billion VND in 2012, and the bad debt ratio has gradually improved. By 2012, Habubank proactively requested to merge with SHB. As of the first quarter of 2013, SHB had a profit of 217 billion VND and the bad debt ratio had decreased to 8.4%, much lower than the previous figure.

13.23% at the time of merger. In addition, Gia Dinh Commercial Joint Stock Bank was changed to Viet Capital Bank or TienPhongBank, after selling shares to Doji Group, and has been operating strongly again with credit growth reaching 15% and bad debt falling below 5%.

2.2.3.13 Other debt settlement methods

Commercial banks also apply different methods to each specific case of bad debt of customers. ACB and Sacombank have plans to consider converting debt into equity for large enterprises, or to acquire reputable and branded enterprises to restore business operations. In 2013, ACB also reached an agreement with a number of enterprises with bad debts on assigning people to monitor the business operations of the enterprise and control cash flow. For cases of bankrupt or absconding enterprises, many commercial banks have transferred loans from enterprises to individuals and guarantors to create conditions for customers to repay their debts. Applying many methods of handling bad debts helps commercial banks recover debts better.

2.3 ASSESSMENT OF BAD DEBT HANDLING AT VIETNAMESE COMMERCIAL BANKS

2.3.1 Results and indicators for evaluating the results of bad debt settlement achieved

Bad debt has shown signs of decreasing up to now .

By the end of May 2013, the bad debt ratio of banks was 4.65%, down about 2% compared to the end of 2012. There are about 30/124 credit institutions with bad debt ratios currently above 3%. The average growth rate of bad debt is 3.94%/month as of May 2013. These are positive signs for bad debt handling of commercial banks in 2013. The indicators for evaluating the results of bad debt handling have also improved. The ratio of group 2-5 debt is only 10.25% because commercial banks actively handle group 2 debts, limiting the increase in debt groups. The debt cancellation rate is 0.55%. With the provisioning level up to May 2013 corresponding to 10.33% of overdue debt, commercial banks mainly use it to handle bad debts that are difficult to collect.