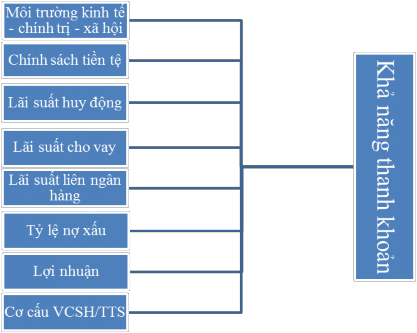

Figure 1.1: Research model of factors affecting liquidity at Vietnam Thuong Tin Commercial Joint Stock Bank

In which, two factors were eliminated: Development of other markets and Competition between banks compared to the theoretical content mentioned above. The reason for not following these two factors in the model is because the factors are not quantifiable, thus it can lead to inaccurate and non-objective results for the study.

In addition, the bank size factor (quantified by taking the logarithm of total assets) was also eliminated compared to the research content of Vodova (2011) because in fact Vodova researched a large number of banks in the Czech Republic, so there were differences in size. In this study, the author only specifically considered VIETBANK, with the bank size over the years not changing much.

In the above model, the Economic - Political - Social Environment factor is measured by three variables: inflation rate, economic growth rate, unemployment rate and dummy variable on the impact of financial crisis; the Monetary Policy factor is measured by open market interest rate.

Chapter 1 Conclusion:

Liquidity is a matter of great concern in the management and business operations of banks. The liquidity of a bank not only directly affects the business operations of that bank but also affects the entire banking system and the development of the national economy.

Chapter 1 aims to outline the theory of liquidity, the causes of liquidity loss, quantitative indicators measuring the liquidity of a bank, factors affecting the liquidity of a bank and research models of factors affecting liquidity in the world in recent years. Thereby, a proposed model is proposed to study the factors affecting the liquidity of Vietnam Thuong Tin Commercial Joint Stock Bank.

The theoretical basis presented in Chapter 1 also creates the premise for assessing the liquidity situation at commercial banks in Vietnam as well as the liquidity of VIETBANK in the next chapter. In addition, the research model proposed at the end of the chapter will be presented specifically in Chapter 3 when conducting specific quantitative research.

CHAPTER 2: CURRENT STATE OF LIQUIDITY AT VIETNAM THUONG TIN COMMERCIAL JOINT STOCK BANK

2.1. GENERAL LIQUIDITY SITUATION OF THE CURRENT VIETNAMESE COMMERCIAL BANKING SYSTEM

The author proposes to review the data as of December 31, 2013 of some of the following banks to assess the liquidity situation of this group of banks, thereby seeing the general liquidity situation of the Vietnamese banking system.

Table 2.1: Data on indicators measuring liquidity of banks

Bank

Minimum capital adequacy ratio | Cash position index | Lending capacity index | Total Outstanding Loans/Customer Deposits Index | Deposit structure index | |

VCB | 14.83% | 24.10% | 53.10% | 66.70% | 43.20% |

ACB | 11.15% | 9.30% | 64.40% | 74.10% | 10.70% |

EXIMBANK | 16.38% | 32.20% | 51.00% | 76.30% | 9.20% |

VIB | 19.43% | 7.50% | 48.60% | 82.40% | 14.60% |

NAMABANK | 19.21% | 18.40% | 44.40% | 60.70% | 18.90% |

VIETBANK | 19.24% | 17.50% | 46.92% | 61.20% | 17.38% |

Maybe you are interested!

-

Current status of credit risk at Saigon Thuong Tin Commercial Joint Stock Bank, Lam Dong branch - 1

Current status of credit risk at Saigon Thuong Tin Commercial Joint Stock Bank, Lam Dong branch - 1 -

Current Status of Ownership Structure and Performance of Vietnam's Banking Industry

Current Status of Ownership Structure and Performance of Vietnam's Banking Industry -

Current status of investment activities in bond trading of Vietnam Commercial Bank

Current status of investment activities in bond trading of Vietnam Commercial Bank -

Current Status of Credit Risk Management at Vietnam Bank for Agriculture and Rural Development

Current Status of Credit Risk Management at Vietnam Bank for Agriculture and Rural Development -

Current Status of Fixed Asset Accounting Organization at Sanofi-Aventis Vietnam Company Limited:

Current Status of Fixed Asset Accounting Organization at Sanofi-Aventis Vietnam Company Limited:

(Source: Compiled from 2013 financial statements of banks)

According to table 2.1, at the end of 2013, commercial banks in Vietnam all achieved the minimum capital safety ratio in accordance with the regulations of the State Bank (not lower than 9%). This shows that banks have a reasonable ratio between equity capital and the level of risk in using assets. However, there are banks with extremely high minimum capital safety ratios: VIB 19.43% and NAMABANK 19.21%; this ratio is too safe, which means that the bank's business operations are ineffective, directly affecting profits. In addition, this is also a sign that the bank's liquidity has problems, or the

Banks are in a state of not being able to mobilize deposits, or banks are unable to lend or do not want to lend.

Next is the cash position index, this high index ensures the ability to meet the bank's immediate liquidity needs and this index is at least 5%. According to table 2.1, ACB and VIB are the two banks with the lowest cash position index in the evaluated group and still maintain it at the allowable level. With the figures of 9.3% for ACB and 7.5% for VIB, it shows that the bank still has good liquidity, does not hoard too much cash but uses that money to invest in other businesses. However, to maintain it at the necessary level, when a large liquidity need arises in a short time, the bank is forced to borrow capital from the market at high interest rates. Besides, NAMABANK, VCB and especially EXIMBANK have very high cash position indexes, respectively: 18.4%, 24.1% and 32.2%. When a bank maintains this index at a high level, it is not necessarily good. A high index shows that the bank has a high amount of idle money, which means that the bank is not using capital effectively.

Because outstanding loans are the least liquid assets of a bank, when a bank's total outstanding loans account for a large proportion of its total assets or the bank's lending capacity index is high, it means that the bank is closer to liquidity risk. In recent years, banks have focused on credit development, so it is not surprising that this index is high. Among the banks considered, NAMABANK is the bank with the lowest lending capacity index (44.4%) because compared to the whole group, this is the bank with the smallest scale and lowest reputation. For large banks such as VCB, ACB, EXIMBANK, this ratio is over 50%.

The next indicator to be considered is the total outstanding loan/customer deposit ratio, which shows how much money the bank has lent out and has mobilized from customers. Previously, on May 20, 2010, the State Bank of Vietnam issued Circular 13/2010/TT-NHNN, which regulated the credit ratio from mobilized capital and was amended in Circular 19/2010/TT-NHNN issued on September 27, 2010, which limited the lending ratio from mobilized capital of a bank to a maximum of 80%. However, on August 30, 2011, Circular 22/2011/TT-NHNN was issued, abolishing the ratio.

has been stipulated in the two above-mentioned documents to create capital circulation and regulation between the interbank market and the capital market mobilized from organizations and individuals, between banks with excess capital and banks lacking capital, in order to help banks lacking capital have conditions to increase credit growth. According to data table 2.1, it is easy to see that up to December 31, 2013, most banks still maintained the loan-to-deposit ratio of customers at no more than 80%, except for VIB with a slightly higher rate of 82.4%. In addition, NAMABANK and VCB are the two banks with the lowest total outstanding loan/customer deposit ratio in the group, corresponding to 60.7% and 66.7%. However, according to the author's comments, these two figures come from two different causes. For NAMABANK, at the time of reviewing the data, the bank was having difficulty in lending to customers, credit did not really develop. As for VCB, a bank with its existing reputation has mobilized a large amount of deposits, much exceeding VCB's demand for residential loans. This is also the reason why VCB lends more in the interbank market than other banks.

The bank's deposit structure index reflects the stability of liquidity supply, the lower this ratio shows the higher liquidity supply capacity and vice versa. However, maintaining the deposit structure index at a low level can affect the bank's profits because of high mobilization costs, since the cost of mobilizing term deposits is always higher than non-term deposits. At the end of 2013, VCB had a deposit structure index of 43.2%, showing that the amount of non-term deposits at VCB is high, ensuring profits for VCB, but it is also a factor that can lead to high liquidity risk when the banking system has incidents. On the contrary, we see that EXIMBANK maintains the ratio between demand deposits and term deposits at a very low level of 9.2%, showing that EXIMBANK wants to ensure safety from customer withdrawals. On the other hand, EXIMBANK has to bear high mobilization costs. In case the market develops badly and lending is difficult, this also leads to liquidity risk for EXIMBANK.

Thus, through the analysis, we see that the banks considered above are maintaining their liquidity indicators at a relatively good level. However, banks should also pay more attention and care to liquidity to ensure the safety of banks and the Vietnamese banking system from negative impacts from the external environment. The State Bank also contributes significantly in supporting banks to manage and maintain their liquidity.

2.2. CURRENT LIQUIDITY SITUATION OF VIETNAM THUONG TIN JOINT STOCK COMMERCIAL BANK

2.2.1. General introduction about Vietnam Thuong Tin Commercial Joint Stock Bank

Vietnam Thuong Tin Commercial Joint Stock Bank was established in February 2007 during the period of strong development of the Vietnamese banking and financial system. With founding shareholders having strong financial potential and rich experience in financial and business management, VIETBANK has been well prepared in terms of financial capacity, human resources and technological level, firmly facing the difficulties in the period of international economic integration.

At the end of 2010, VIETBANK increased its charter capital to VND3,000 billion and its total assets to VND17,265 billion. VIETBANK has also continuously expanded its network of operations (from February 2009 to present) with 95 transaction points located in key economic regions across the country and recruited more than 1,400 young, dynamic, creative and highly responsible employees, ready to meet all customer requirements.

During the development process, VIETBANK has invested in improving the quality of its information technology system through the construction of a data center and a core banking system. In addition, VIETBANK has implemented a quality management system according to ISO 9001:2008 standards to control and improve the quality of management and customer service. The VIETBANK brand is also gradually becoming familiar to customers through a system of rich products and services, serving the diverse needs of each specific customer group. In addition, flexible policies in business operations are also one of VIETBANK's strengths in response to the increasingly diverse needs of customers.

Strategic vision: Continuously improve quality in all aspects to become one of the prestigious brands in the banking and finance sector in Vietnam.

Mission: To build VIETBANK into a dynamic, modern retail bank with top service quality in Vietnam, capable of competing and developing in the new period.

Core values:

- Highly qualified, experienced and enthusiastic human resources.

- Modern information technology system.

- Scientific organization and management model.

Formation and development process:

- On February 2, 2007, VIETBANK was officially established at 35 Tran Hung Dao, Soc Trang city, Soc Trang province, creating the premise for the development of a nationwide network.

- February 18, 2009, opened Ho Chi Minh City branch at 02 Thi Sach, Ben Nghe ward, District 1 - the first branch of VIETBANK in Ho Chi Minh City market.

- February 26, 2009, opened Hanoi branch - the first branch of VIETBANK in the Northern region.

- As of November 1, 2014, VIETBANK has 95 transaction points in all key economic regions nationwide. This is a testament to the sustainable development of VIETBANK in the current context.

Operating status:

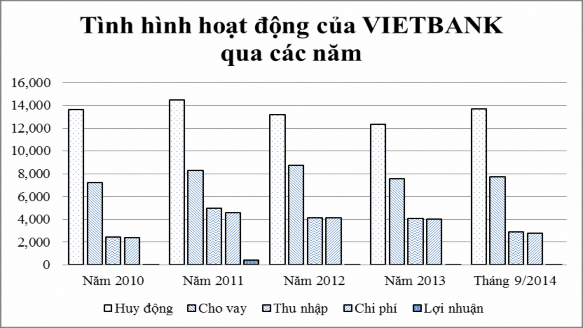

Table 2.2 General performance of VIETBANK from 2010 to September 2014 – Unit: billion VND

Criteria

2010 | 2011 | 2012 | 2013 | September 2014 | |

Mobilize | 13,647 | 14,500 | 13,163 | 12,358 | 13,699 |

Loan | 7,247 | 8,272 | 8,728 | 7,563 | 7,752 |

Income | 2,435 | 4,961 | 4,133 | 4,079 | 2,873 |

Expense | 2,368 | 4,566 | 4,109 | 4,043 | 2,796 |

Profit | 67 | 395 | 24 | 36 | 77 |

(Source: Report on general operations of VIETBANK from 2010 to September 2014)

Figure 2.1: General performance of VIETBANK over the years from 2010 to September 2014

(Source: Report on general operations of VIETBANK from 2010 to September 2014)