The above table shows that the results of other activities of the NHA&PTNT Branch in Phuc Tho district tend to develop well, the total income from service activities increases steadily over the years. The branch has successfully converted and transacted on the IPCAS payment system (the project to modernize the payment system funded by the World Bank for NHA&PTNT Vietnam). Some new banking services have the potential to be applied and exploited well, specifically: the number of ATM cards issued reached 11,213 cards, the card account balance was 33.1 billion VND; Mobile Banking services, VN top up, Atranfer,... It can be said that the above activities, although still new, have proven the inevitable trend of modern banking activities, gradually contributing to the integration of the NHA&PTNT Branch in Phuc Tho district.

d. Business performance in recent years

The NHA&PTNT Phuc Tho District is an effective business unit, the financial results (according to the financial contract mechanism of the NHA&PTNT Vietnam, NHA&PTNT Ha Tay Branch) are always higher year after year, fully fulfilling obligations to the state budget and to the superior bank, ensuring stable jobs and income for officers and employees according to the regulations of the NHA&PTNT Vietnam. The business results under the financial contract mechanism over the years are as follows:

Table 2.4: Business performance results over the years 2012 - 2014

Unit: billion VND

Target

2012 | 2013 | 2014 | Growth (%) | ||

2013 - 2012 | 2014 - 2013 | ||||

1. Total income | 54.8 | 83.8 | 76.9 | 52.9 | -8.2 |

2. Total cost | 37.9 | 49.8 | 54.8 | 31.4 | 10.1 |

3. Total income fund achieved | 16.9 | 33.9 | 22.1 | 100.6 | -34.8 |

4. Salary fund achieved | 5.6 | 10.2 | 8.4 | 82.1 | -17.7 |

Maybe you are interested!

-

Company's Business Performance Results for 3 Years (2018-2020)

Company's Business Performance Results for 3 Years (2018-2020) -

Production and Business Performance Results of La Nga Forestry Company Limited

Production and Business Performance Results of La Nga Forestry Company Limited -

Business Performance Results Over 3 Years 2011-2013

Business Performance Results Over 3 Years 2011-2013 -

Acb's Business Performance Results in 15 Years

Acb's Business Performance Results in 15 Years -

Production and Business Performance Results for the Period 2017 - 2019

Production and Business Performance Results for the Period 2017 - 2019

(Source: annual financial report, NHNo&PTNT Phuc Tho district)

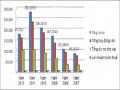

Figure 2.6: Total income fund over the years 2012-2014

35

30

Total income fund achieved

25

20

15

10

5

0

2 0 12 2 0 13 2 0 14

Conclusion: The above table gives us an idea of the annual income fund achieved.

The Branch's revenue fluctuates from year to year, from 2012 to 2013 to 2014 to 22.1 billion VND, in which the profit target from 2012 to 2014 accounts for a large proportion (over 93%) of the total income, which proves that credit activities are still the main activity of the Bank for Agriculture and Rural Development of Phuc Tho district. The indicators on income and salary fund have been stable and growing over the years, showing that the business activities of the Bank for Agriculture and Rural Development of Phuc Tho district are effective, completing the financial targets assigned by the Bank for Agriculture and Rural Development of Ha Tay - Hanoi City, having a stable and strong financial foundation, creating a premise for the following years in the process of regional and international economic integration.

2.3. CURRENT STATUS OF CREDIT EXPANSION FOR PRODUCTION HOUSEHOLDS AT THE BRANCH OF NHNo & PTNT IN PHUC THO DISTRICT

2.3.1. Legal basis for credit activities of production households

Legal basis for credit adjustment for production households at the branch of NHNo & PTNT in Phuc Tho district:

- Joint Resolution No. 2308/NDLT between the Central Committee of the Vietnam Farmers' Union and the Vietnam Bank for Agriculture and Rural Development on the organization and implementation of bank credit policies serving agricultural and rural development issued by the Central Committee of the Vietnam Farmers' Union - the Bank for Agriculture and Rural Development.

Content:

Establish loan groups to expand loans to members.

Encourage professional organizations and Good Farmer clubs to sign contracts to provide loan services according to regulations.

Propagating policies on agriculture and rural areas, policies and measures, lending procedures, good business practices, and effective use of capital.

- Decision 2382/QD-NHNN dated October 19, 2009 on promulgating the List of documents and regulations issued by the State Bank of Vietnam that have expired from January 1, 2009 to June 30, 2009.

- Law on the State Bank of Vietnam No. 01/1997/QH10 aims to build and effectively implement the national monetary policy; strengthen state management of currency and banking activities; contribute to the development of a multi-sector commodity economy under a market mechanism with state management, following a socialist orientation; protect the interests of the State, the legitimate rights and interests of organizations and individuals;

- Law on credit institutions No. 47/2010/QH12:

The Law on Credit Institutions was passed by the 12th National Assembly at the 7th session on June 16, 2010, effective from January 1, 2011 and replacing the Law on Credit Institutions No. 02/1997/QH10 and the Law amending and supplementing a number of articles of the Law on Credit Institutions No. 20/2004/QH11.

The Law on Credit Institutions regulates the establishment, organization, operation, special control, reorganization, and dissolution of credit institutions; the establishment, organization, and operation of foreign bank branches and representative offices of foreign credit institutions and other foreign organizations with banking activities.

The subjects of application of the Law are credit institutions; foreign bank branches; representative offices of foreign credit institutions, foreign organizations.

Other foreign organizations with banking activities; organizations and individuals related to the establishment, organization, operation, special control, reorganization, and dissolution of credit institutions; the establishment, organization, and operation of foreign bank branches and representative offices of foreign credit institutions and other foreign organizations with banking activities.

- Decision No. 666/QD-HDQT-TDTHo dated June 15, 2010 on promulgating the Regulations on lending to customers in the system of the Bank for Agriculture and Rural Development of Vietnam.

- Decision No. 1300/QD-HDQT-TDHo dated December 3, 2007 on promulgating the Regulation on implementing loan security measures in the system of the Bank for Agriculture and Rural Development of Vietnam.

- Decision No. 1627/2001/QD-NHNN dated December 31, 2001 on promulgating the Regulations on lending by credit institutions to customers.

- Decision No. 571/2002/QD-NHNN dated June 5, 2002 on approving the Charter on organization and operation of the Bank for Agriculture and Rural Development of Vietnam.

- Decision No. 28/2002/QD-NHNN dated January 11, 2002 amending Article 2 of Decision No. 1627/2001/QD-NHNN dated December 31, 2000 of the Governor of the State Bank on promulgating regulations on lending by credit institutions to customers.

- Decision No. 127/2005/QD-NHNN on amending and supplementing a number of articles of the Regulations on lending by credit institutions to customers issued under Resolution 1627/2001/QD-NHNN dated December 31, 2001 of the Governor of the State Bank.

- Decree 41/2010/ND-CP dated April 12, 2010 on credit policies for agricultural and rural development

- Resolution 30a/2008/NQ-CP on the new rural construction program investing in lending for large-scale fields and converting land for gardens, ponds and barns of the Vietnam National Bank for Agriculture and Rural Development.

2.3.2. Current status of credit expansion for production households

2.3.2.1. Number of production households receiving loans

The expansion of credit for production households is reflected in many aspects such as: increasing loan turnover, outstanding debt, debt collection, expanding the network and lending methods and forms, and also reflected in the increase in the number of households receiving loans and the average outstanding debt per household. The number of production households borrowing capital and the average outstanding debt per household of the Branch of the Bank for Agriculture and Rural Development of Phuc Tho district are shown in the following data table:

Table 2.5: Number of production households receiving loans and average outstanding loans per household

Unit: Billion VND, household

Target

2012 | 2013 | 2014 | |

Total outstanding debt of production households | 283.2 | 313.8 | 338.3 |

Number of production households receiving loans | 13,485 | 13,075 | 9,665 |

Average outstanding debt/household | 0.021 | 0.024 | 0.035 |

(Source: Statistics of the Branch of the Bank for Agriculture and Rural Development of Phuc Tho district 2012 - 2014)

The total outstanding loans of production households have continuously increased over the years, thanks to which the average outstanding loans per household also tend to increase. In 2013, the average outstanding loans per household were 24 million VND/household, an increase of 3 million VND, in 2014 it was 35 million VND/household, an increase of 11 million VND. This is a good sign in the bank's capital investment work.

However, the number of production households borrowing capital from banks has decreased. The reason is that some production households use capital ineffectively and do not pay back.

are owed to the bank, so the bank only focuses on production households with effective production and business plans and projects. On the other hand, in the area, some commercial banks have initially focused on households, moreover, for poor or near-poor households, they are the subjects served by the Social Policy Bank, so they have switched to lending relationships with this bank, which has significantly reduced the number of customers of the branch.

The above situation shows that although there is a reduction in the number of borrowers, it does not mean that the Phuc Tho District Branch of the Bank for Agriculture and Rural Development has reduced credit for production households, but rather a shift from expanding credit in breadth to expanding credit in depth. The bank has reduced small, ineffective loans, and loans that are not eligible, both reducing the workload for credit officers and creating conditions to focus capital on households with effective production and business plans and projects, promptly meeting the needs of production and business activities of households that are increasingly expanding.

2.3.2.2. Forms and methods of credit for production households

In recent years, to meet the capital demand for production and business in agriculture and rural areas, mainly production households, with increasingly diverse and rich subjects. The Vietnam Bank for Agriculture and Rural Development issued Decision 72/QD-HDQT-TD, dated March 31, 2002 on lending to customers in the Vietnam Bank for Agriculture and Rural Development system and on June 15, 2010, Decision 666/QD-HDQT-TDHo replaced it. The Phuc Tho District Bank for Agriculture and Rural Development Branch has applied many forms of capital transfer to production households. The main forms that the Phuc Tho District Bank for Agriculture and Rural Development Branch is currently applying for production household credit are: Loans with collateral and loans without collateral.

According to the first type of loan, which is a form of loan with collateral, the bank will carry out procedures for collateral to lend according to the law. When completing the documents on collateral, the branch encountered some difficulties because some households have not been granted land use right certificates. This has caused the bank to be hesitant when granting credit to production households, because when customers cannot repay the bank loan, there is no property to process to recover the debt, the possibility of risk is high.

In the case of unsecured loans, the bank will have to establish a relationship with the local government to confirm the borrower. Before the Government's Decree 41/ND-CP was issued, the NHA&PTNT Phuc Tho district still followed Decision 67/1999/QD-TTg on unsecured loans to farming households, which is no more than 10 million VND. In many cases, households with large and effective production and business plans and projects, but without collateral, still cannot borrow in this form. Until April 12, 2010, Decree 41/ND-CP of the Government was issued, increasing the loan limit for farmers without collateral to 50 million VND, removing and overcoming the limitations of Decision 67/1999/QD-TTg, thus creating conditions for households to access bank capital more easily, and have conditions to expand the scale of production and business.

Regarding the process, the lending procedures are relatively strict, the bank has implemented the lending process for Production Households of the Vietnam Bank for Agriculture and Rural Development. With a team of enthusiastic and experienced staff, they have guided Production Households to quickly complete the loan application, creating conditions for households to borrow capital conveniently and quickly.

In credit for production households, branches often apply the following 3 main forms:

+ Direct loan form at the bank

Customers proactively go directly to the bank to borrow capital, repay debt, and pay interest. This transfer has had an effect, reducing intermediary levels, bringing capital to producers faster, reducing hassles, creating initiative for producers, and using capital more effectively. At the same time, banks also expand credit more effectively, enhancing the bank's reputation.

To apply this form, ensuring convenience for customers, the branch of the NHNo&PTNT Phuc Tho district has actively expanded its network. Up to now, there have been 4 inter-commune transaction offices established in residential areas and towns. This network has been and is promoting good efficiency.

Because agricultural production is seasonal, the demand for loans from each household is small, credit officers are in charge of a large area, have to manage a large number of customers, appraisal work takes a lot of time, so sometimes it is not timely. If the credit scale increases, it will cause customer overload.

+ Mobile lending form, rural mobile banking

The bank organizes a group of 3-5 people (Credit, Accounting and Cashier) to go to the commune to disburse, collect debts and interest according to a pre-announced schedule or a three-way lending group in coordination with companies supplying materials and purchasing agricultural products. This form is mainly applied in large areas of operation, sparsely populated, underdeveloped commodity economy, and not yet qualified to establish a transaction office. This form is very convenient for customers, reducing the cost of having to travel far to the district bank to make transactions.

This form requires arranging many workers for accounting and fund operations, operating according to a schedule, so checking and urging each borrower is limited.

+ Direct lending through groups (credit groups)

Credit organizations include: Farmers' Association, Women's Association, Veterans' Association... Credit officers and volunteer groups carry out 8 stages, dividing responsibilities: