Treasury department: Implement cash collection and payment regime, keep money in the warehouse on schedule...

Customer Relations Department

Customer Relations Department – Corporate Customers:

- Maintain, develop and expand business relationships with corporate customers.

- Customer assessment; guide and advise customers on how to use banking products and services; propose plans to provide products and services.

- Check and monitor before, during and after the process of providing products and services.

- Cross-sell products.

- Liaise with financial institutions to arrange syndicated loans and manage co-financing for the entire Branch.

- Coordinate with relevant departments to perform assigned tasks well.

Customer Relations Department – Individual Customers:

- Develop business activities of banking products and services and risk management of the Branch for individual customers according to the orientation and policies prescribed by the Bank.

- Perform other tasks as directed by the individual customer segment at the headquarters and the Branch Director regarding plans related to the individual customer segment such as network development, distribution channels, marketing, etc.

- Coordinate with other departments of the Branch and other Branches to ensure the implementation of set goals.

Card department:

Organize, deploy and develop the Branch's card business activities according to the annual targets and plans assigned by the General Director. Manage and supervise the Branch's card business activities.

Credit Management Department

- Advise the Director on credit management: mechanisms, policies, regulations, credit procedures, guarantees, credit limits; management and handling of bad debts.

- Monitor credit performance at the Branch.

- Assist the Director, Customer Relations Department in legal issues related to credit activities.

- Collect and prepare reports for management and operations.

- Develop strategies, structures, credit limits; develop monthly business plans and assign plans to departments.

Dong Ba Transaction Office and Ba Trieu Transaction Office

Business activities in the assigned area are subject to business management by the Branch Director and carry out assigned targets by the Bank's leadership.

Each transaction office has 2 departments:

- Treasury Accounting

- Customer Relations.

2.1.2.4. Branch's labor structure

Hue Branch of An Binh Commercial Joint Stock Bank is a unit operating in the service business sector, so the human factor plays a very important role. The qualifications, abilities and professional skills of the staff directly affect the quality of the Bank's services, affect customer relationships and affect the business results of the Branch. In monetary business activities, the Bank often faces risks from many sides, of which the risks from the staff are very large. Violations caused by an individual have a much greater level of damage than other business sectors. Recognizing that problem, ABBANK Hue in recent years has continuously supplemented and developed its human resources to better meet the needs of customers.

To better understand the human resources of ABBANK Hue, we study Table 1, statistics on the Branch's labor structure over the years 2011 - 2013 below.

Along with the development and expansion of operations, the number of employees working at ABBANK Hue Branch has continuously increased over the years and has increased quite steadily in terms of quantity. In 2011, the total number of employees of the Branch was 27 people; by 2012, along with the upgrading and establishment of Dong Ba Transaction Office and the decision to change the location of the main transaction office, this number was 40 people, an increase of 13 people (equivalent to an increase of 48.15%). 2013 continued to witness the strong development of ABBANK Hue when the

The transaction branch relocation from 100 Nguyen Hue to 17 Hanoi was completed, the number of employees working in the entire branch increased to 45 people, an increase of 13 people compared to 2012 (equivalent to an increase of 12.50%). Thus, it can be said that ABBANK Hue has quite stable growth in terms of labor scale.

Table 1: Labor structure of ABBANK - Hue Branch

Division criteria

2011 | 2012 | 2013 | Compare | ||||||||

2012/2011 | 2012/2013 | ||||||||||

SL (People) | Structure (%) | SL (People) | Structure (%) | SL (People) | Structure (%) | +/- | % | +/- | % | ||

Total number of workers | 27 | 100 | 40 | 100 | 45 | 100 | 13 | 48.15 | 5 | 12.50 | |

1. Classification by gender | |||||||||||

Male | 9 | 33.33 | 15 | 37.50 | 19 | 42.22 | 6 | 66.67 | 4 | 26.67 | |

Female | 18 | 66.67 | 25 | 62.50 | 26 | 57.78 | 7 | 38.89 | 1 | 4.00 | |

2. Classified by level | |||||||||||

Grand study or more | 19 | 77.37 | 33 | 82.50 | 41 | 91.11 | 14 | 73.68 | 8 | 24.24 | |

Intermediate, High class | 6 | 22.22 | 5 | 12.50 | 2 | 4.44 | (1) | (16.67) | (3) | (60) | |

General labor information | 2 | 7.41 | 2 | 5.00 | 2 | 4.44 | 0 | 0.00 | 0 | 0.00 | |

Maybe you are interested!

-

Company's Business Performance Results for 3 Years (2018-2020)

Company's Business Performance Results for 3 Years (2018-2020) -

Acb's Business Performance Results in 15 Years

Acb's Business Performance Results in 15 Years -

Business Performance Results Over the Years 2012 – 2014

Business Performance Results Over the Years 2012 – 2014 -

Business Performance of the Company in the Period 2009–2011 Table 2.1. Business Results of Viet Holiday Travel Company

Business Performance of the Company in the Period 2009–2011 Table 2.1. Business Results of Viet Holiday Travel Company -

Production and Business Performance Results of La Nga Forestry Company Limited

Production and Business Performance Results of La Nga Forestry Company Limited

(Source: Administration Department - General ABBANK Hue)

In terms of gender, the labor structure at the Bank has a large difference and remains quite stable over the years. In 2011, ABBANK Hue had 9 male employees (accounting for 33.33 %) and 18 female employees (accounting for 66.67 %). In 2012, the number of male employees increased by 6 people (equivalent to an increase of 66.67%) and female employees increased by 7 people (equivalent to an increase of 38.89 %). By 2013, the number of employees increased by 4 men and 1 woman (equivalent to an increase of 926.67% and 4% compared to 2012), at this time the Branch had 19 men (accounting for 42.22%) and 26 women (accounting for 57.78 %).

By level, it can be seen that the majority of employees at the Bank are university and post-graduate graduates. In 2011, out of a total of 27 employees, 19 were university-graduated (accounting for 77.38%), only 6 were college-graduated (accounting for 22.22%) and 2 were unskilled workers (accounting for 7.41%). By 2012, the number of employees with university-graduated training increased by 14 (equivalent to an increase of 73.68%), the number of employees with college-graduate degrees decreased by 1 person and the number of unskilled workers remained unchanged. In 2013, along with the increase in quantity, the labor structure in terms of qualifications remained stable: The number of employees with university and post-graduate degrees was 41 (accounting for 91.11%), an increase of 8 people compared to 2012 (equivalent to an increase of 24.24%); the number of employees with college and intermediate degrees was 2 people (accounting for 4.44%), a decrease of 3 people; and the number of unskilled workers was 2 people (accounting for 4.44%). A highly qualified workforce is an advantage that helps the Branch achieve optimal work efficiency and sustainable development.

Thus, it can be seen that the labor force working at ABBANK Hue is increasing and increasing steadily, the labor structure is also always stable in terms of both gender and training level.

2.1.2.5. Business performance results over 3 years 2011-2013

The business activities of An Binh Commercial Joint Stock Bank - Hue Branch have increasingly achieved great results, not only reflected in the increase in scale but also in financial indicators such as revenue and profit.

To better understand the business performance of the Branch, we study Table 2, business data of ABBANK - Thua Thien Hue through the years 2011-2013 below.

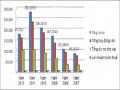

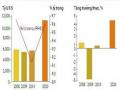

Table 2: Business data of ABBANK – Thua Thien Hue Branch

Unit: Million VND

Target

2011 | 2012 | 2013 | Compare | ||||

Value | Value | Value | 2012/2011 | 2013/2012 | |||

+/- | % | +/- | % | ||||

I. Income | 6250 | 9250 | 12200 | 3000 | 48.00 | 2950 | 31.89 |

II. Cost | 3700 | 5150 | 6660 | 1450 | 39.19 | 1510 | 29.32 |

III. Profit | 2550 | 4100 | 5540 | 1550 | 60.78 | 1440 | 35.12 |

(Source: Accounting Department - Customer Service ABBANK Hue) Looking at the data table, we can see that along with the development of the scale of the location, the profit of the Branch has always increased at a high level over the years. Specifically: In 2011, the profit reached 2,550 million VND, then in 2012 this figure increased to 4,100 million VND, an increase of 1,550 million VND (equivalent to an increase of 60.78%). 2013 continued to record great success when the profit reached 5,540 million VND, an increase of 1,440 million VND compared to 2012 (equivalent to an increase of 35.12%). Ignoring the impacts of the macro economy, it can be said that these are positive growth figures, promising increasingly stable development of the Branch.

ABBANK – Thua Thien Hue Branch.

However, one issue that ABBANK Hue needs to pay attention to in order to further improve the Bank's profit and operational efficiency is cost. In 2011, the cost was 3,700 million VND, but in 2012 it increased to 5,150 million VND (an increase of 39.19%). More notably, in 2013, this figure reached 6,660 million VND, an increase of 1,510 million VND compared to 2012 (an increase of 29.32%).

This high increase in costs is caused by many reasons: the increase in the number of employees over the years (increased employee salary costs), the increase in employee training costs (especially for new employees) and the increase in recruitment costs,...

2.1.3.6. Capital mobilization activities

Capital mobilization activities at the bank show the scale of deposits, specifically the amount mobilized from 2011 to 2013 was 215 billion VND, 317 billion VND and 470 billion VND. We can see that the capital mobilization of the branch has a good trend: In 2012, it increased by 47.4% compared to

In 2011, the amount increased by 102 billion VND; in 2013, the amount increased to 470 billion VND, an increase of 48.3% compared to 2012. The capital mobilization results increased over the past 3 years, showing that customers' trust in ABBANK is increasing, and the ABBANK brand is increasingly spreading in the Hue market.

Table 3: Capital mobilization scale at branches over 3 years

Target

2011 | 2012 | 2013 | 2012/2011 | 2013/2012 | ||||||

Value (percent) copper) | Structure (%) | Value (percent) copper) | Structure (%) | Value (percent) copper) | Structure (%) | +/- (billion VND) | % | +/- (billion VND) | % | |

215 | 100 | 317 | 100 | 470 | 100 | 102 | 47.4 | 153 | 48.7 | |

1. Classify by term | ||||||||||

KKH | 10 | 4.7 | 50 | 15.8 | 78 | 16.6 | 40 | 400 | 28 | 56 |

Short term | 202 | 94 | 263 | 83 | 386 | 82.1 | 61 | 30.2 | 123 | 46.8 |

Medium long limit | 3 | 1.4 | 4 | 1.3 | 6 | 1.3 | 1 | 33.3 | 2 | 50 |

2. According to the form of mobilization | ||||||||||

Deposit pay | 10 | 4.7 | 50 | 15.8 | 78 | 16.6 | 40 | 400 | 28 | 56 |

Deposit save | 205 | 95.3 | 267 | 84.2 | 392 | 83.4 | 62 | 30.2 | 125 | 46.8 |

3.By customer target | ||||||||||

Science and Technology | 170 | 79.1 | 240 | 75.7 | 350 | 74.5 | 70 | 14.2 | 110 | 45.8 |

Business | 45 | 20 | 77 | 24.3 | 120 | 25.5 | (68) | (46.9) | 43 | 55.8 |

4.By type of mobilized currency | ||||||||||

VND | 212 | 98.6 | 308 | 97.2 | 459 | 97.7 | 96 | 45.3 | 151 | 49 |

Foreign currency | 3 | 1.4 | 9 | 2.8 | 11 | 2.3 | 6 | 200 | 2 | 22.2 |

(Source: Accounting Department - Customer Service ABBANK Hue)

2.1.2.7. Lending activities

Through the table above, we can see that the branch's loan sales over the past 3 years have achieved an increase.

quite sustainable growth, specifically: in 2012 it increased by 43.0%, equivalent to 116 billion VND; in 2013 it increased by 19.2%, equivalent to 74 billion VND. Although the increase in 2 years is not too high, this is also a positive signal for the development of the branch.

Lending activities for corporate customers account for a larger proportion. The reason is that businesses have a greater need to borrow for business purposes, while individual customers borrow mainly for consumption purposes. This is also consistent with the proportion of consumer and business loan purposes shown in the table.

In general, the branch's lending activities are developing in a positive direction, which also contributes to demonstrating the effectiveness of ABBANK's brand building in general and the effectiveness of the personal sales team in particular.

Table 4: Branch loan structure scale over 3 years

Target

2011 | 2012 | 2013 | 2012/2011 | 2013/2012 | ||||||

Value (percent) copper) | Structure (%) | Value (percent) copper) | Structure (%) | Value (percent) copper) | Structure (%) | +/- (billion VND) | % | +/- (billion VND) | % | |

Sales loan | 270 | 100 | 386 | 100 | 460 | 100 | 116 | 43 | 74 | 19.2 |

Science and Technology | 115 | 42.6 | 171 | 44.3 | 210 | 45.7 | 56 | 48.7 | 39 | 22.8 |

Business | 155 | 57.4 | 215 | 55.7 | 250 | 54.3 | 60 | 38.7 | 35 | 16.3 |

(Source: Accounting Department - Customer Service ABBANK Hue)

2.2. Brand value assessment of An Binh Commercial Joint Stock Bank - Thua Thien Hue branch

2.2.1. Descriptive statistics of the research sample

Through the investigation process, 130 questionnaires were distributed and 130 questionnaires were collected. After checking, all 130 questionnaires collected were valid. The study collected primary data from 130 individual customer samples at An Binh Commercial Joint Stock Bank - Thua Thien Hue branch. The survey sample has the following characteristics:

Table 5: Characteristics of the study sample

Criteria

Frequency | Rate (%) | |

1. Gender | ||

Male | 68 | 52.3 |

Female | 62 | 47.7 |

Total | 130 | 100 |

2. Age | ||

18 to 22 years old | 6 | 4.6 |

23 to 30 years old | 33 | 25.4 |

31 to 45 years old | 60 | 46.2 |

46 to 55 years old | 21 | 16.2 |

Over 55 years old | 10 | 7.7 |

Total | 130 | 100 |

3. Income | ||

Under 5 million | 17 | 13.1 |

5 to under 10 million | 75 | 57.7 |

10 to 15 million | 34 | 26.2 |

Over 15 million | 4 | 3.1 |

Total | 130 | 100 |

(Source: SPSS processing results)

-Sample characteristics by gender

Through the table above, it can be easily seen that the percentage of customers coming to transact at ABBANK Thua Thien Hue branch, if compared by gender, there is not too big a difference. The percentage of men is slightly higher with 52.3% of customers, the remaining 47.7% of customers are women.

-Sample characteristics by age

The characteristics of the survey sample begin to have certain differences through age statistics.

The age structure of the 130 samples collected showed that more than 46% of the interviewed customers were between the ages of 31 and 45, followed by the age group from 23 to 30 years old accounting for 25.4% and more than 16% for the age group from 46 to 55 years old. The 2 age groups of 18-22 years old and over 55 years old accounted for only low proportions of 4.6% and 7.7% respectively.

The group of middle-aged customers from 31 to 45 years old accounts for the majority, because at this age, people have achieved success or are more or less stable in their work, so it is understandable that they need to contact the bank in many forms (savings, money transfer, using ATM cards, etc.). The group from 23 to 30 years old accounts for a high proportion, which also contributes to explaining the working relationship between this group and customers. The group from 18 to 22 years old has little need or no need to use, so the proportion of people in this age group contacting the bank is quite low. As for the age group over 55, this is the retirement age, so the main trend is consumption and saving, saving is mainly for periodic periods, so the frequency of this group of customers is not high. On the other hand, going to the bank to make transactions is not easy, often authorizing relatives to do transactions.

-Sample characteristics by income

Among the interviewed customers, more than 57% of customers have an income of 5-10 million VND/month, 26.2% have an income of 10-15 million VND/month, the remaining 16.2% include two groups of customers with an income of less than 5 million (13.1% - most of whom are retired customers or students) and over 15 million VND (accounting for the smallest proportion - 3.1%). This is also an income level suitable for the economic situation of Hue city in general, most customers still have a good income to be able to

both living expenses and investment in different channels to make profits.

2.2.2. Testing the reliability of the scale

As presented above, in order to conduct exploratory factor analysis - EFA and regression, the component variables in the factors of brand value will be assessed for reliability through the variable correlation coefficient and Cronbach' Alpha coefficient. Variables are assessed as sufficiently reliable when the total variable correlation coefficient is >0.3 and the Cronbach' Alpha coefficient is >0.6. Variables that do not meet the above two conditions, i.e. are not sufficiently reliable, cannot be included in the EFA analysis and will be eliminated from the model.

During the reliability test, two observed variables were eliminated because their total correlation coefficient was less than 0.3. The two eliminated variables are:

- Variable "Do you know ABBANK branches in Thua Thien Hue province" (Variable total correlation coefficient is 0.208)

- Variable "Do you often follow information about bank products and services" (Has a total variable correlation coefficient of 0.298)

Table 6: Assessment of scale reliability before conducting the test

VARIABLE

Scale mean if variable excluded | Scale variance if variable is excluded | Total correlation | Cronbach's Alpha coefficient if variable is excluded | |

1. Brand awareness: Cronbach's Alpha = 0.805 | ||||

Do you know that ABBANK provides deposit, loan, money transfer, and e-banking services? | 7.2 | 2,109 | 0.589 | 0.795 |

Can you distinguish ABBANK from other competing brands? | 7.53 | 1,936 | 0.677 | 0.706 |

Do you know the logo of ABBANK? | 7.52 | 1,889 | 0.692 | 0.689 |

2. Perceived quality: Cronbach's Alpha = 0.908 | ||||

The bank quickly resolves when you encounter problems. | 45.50 | 7,902 | 0.693 | 0.899 |

ABBANK staff make transactions correctly the first time. | 45.48 | 73,016 | 0.593 | 0.903 |

Bank staff provide timely services

45.44 | 73,176 | 0.606 | 0.902 | |

Banks always pay attention to avoid errors. | 45.60 | 74,924 | 0.501 | 0.906 |

Staff provide full transaction information to customers | 45.62 | 72,465 | 0.587 | 0.903 |

Transactions are made quickly | 45.62 | 73,310 | 0.602 | 0.902 |

Bank staff are ready to help you. | 45.52 | 73,617 | 0.719 | 0.899 |

Do you feel safe when transacting at ABBANK? | 46.00 | 72,445 | 0.553 | 0.904 |

Bank staff have enough knowledge to solve your questions. | 46.13 | 70,975 | 0.681 | 0.899 |

The staff has a warm and friendly attitude towards you. | 46.36 | 70,461 | 0.676 | 0.899 |

Bank staff attentively serve you | 45.93 | 71,580 | 0.623 | 0.901 |

ABBANK has convenient transaction locations. | 46.13 | 71,512 | 0.659 | 0.900 |

Modern banking facilities and equipment | 46.38 | 71,636 | 0.507 | 0.908 |

Staff uniform is very neat and polite | 46.00 | 71,886 | 0.660 | 0.900 |

3. Brand desire: Cronbach's Alpha = 0.647 | ||||

Do you like ABBANK? | 7.83 | 1,739 | 0.442 | 0.583 |

When you have a need to use banking services, you will choose to transact at ABBANK. | 7.52 | 1,833 | 0.534 | 0.411 |

Are you willing to introduce friends and relatives to do transactions at ABBANK? | 7.38 | 2,270 | 0.411 | 0.612 |

4. Brand loyalty: Cronbach's Alpha = 0.747 | ||||

ABBANK is your first choice when using banking services. | 11.13 | 3,969 | 0.538 | 0.690 |

I do not use any other bank's services even if they offer them. | 11.33 | 3,876 | 0.581 | 0.666 |

You are willing to wait to use ABBANK's services rather than switch to another bank. | 11.41 | 3,851 | 0.498 | 0.718 |

You are a loyal customer of ABBANK. | 11.13 | 4,289 | 0.565 | 0.681 |

(Source: SPSS processing results)

Removing these two observed variables helps to increase the Cronbach's Alpha coefficient of the research concepts containing the removed variables significantly, as well as ensuring reliability for conducting EFA exploratory factor analysis.

In addition, all remaining observed variables have total correlation coefficients greater than 0.3. Therefore, it can be concluded that the scale used in the study after removing variables is appropriate and reliable, ensuring the EFA exploratory factor analysis.

2.2.3. Exploratory Factor Analysis (EFA) on factors affecting brand loyalty

Exploratory factor analysis is used to reduce and summarize research variables into concepts. Through factor analysis, the relationship between many identified variables is determined and the factors representing the observed variables are found.

2.2.3.1. KMO test

Before conducting exploratory factor analysis to extract factors affecting individual customer loyalty at An Binh Bank, Thua Thien Hue Branch from observed variables, I tested the suitability of the data through two parameters: Kaiser - Meyer - Olkin (KMO) index and Barlett's test. The condition for the data to be suitable for exploratory factor analysis is that the KMO value is 0.5 or higher and the Barlett's test gives a p-value result less than the significance level of 0.05.

Table 7: KMO test results

KMO and Bartlett test

KMO coefficient. | 0.888 | |

Bartlett's Test of Sphericity | Approx. Chi-Square | 1328,490 |

Df | 190 | |

Sig. | 0.000 | |

(Source: SPSS processing results)

In order to check whether the research sample is large enough and qualified to conduct factor analysis, I conducted the Kaiser – Meyer – Olkin test and the Bartlett test. With the KMO test result of 0.888, greater than 0.5 and the p – value of the Bartlett test less than 0.05, we can conclude that the survey data is