Test: Var(u) = 0

Table 4.6 Breusch-Pagan test

chibar2(01) = 19.75 Prob > chibar2 = 0.0000

Source: Results from STATA software

Based on the test results in table 4.6, we have p-value = 0.0000 < 5% significance level, we have enough evidence to reject H 0 , so there is a difference in error between different subjects, so we choose the RE method.

Thus, after performing model selection tests between OLS, RE and FE, RE is the appropriate model for the research data of the thesis. The regression results using the RE method are as follows:

Table 4.7 Regression results by RE

ROE

Coef. | Std. Err. | z | P>z | |

CAP | -0.330 | 0.082 | -4.030 | 0.000*** |

CR | -1.013 | 0.581 | -1.740 | 0.081* |

OC | -0.247 | 0.022 | -11,250 | 0.000*** |

Size | 0.012 | 0.005 | 2,160 | 0.031* |

GDP | -0.006 | 0.324 | -0.020 | 0.985 |

CPI | 0.174 | 0.046 | 3,780 | 0.000*** |

OWN | -0.005 | 0.018 | -0.290 | 0.768 |

LA | 0.028 | 0.034 | 0.810 | 0.418 |

DOP | -0.009 | 0.025 | -0.360 | 0.721 |

_cons | 0.034 | 0.116 | 0.290 | 0.772 |

Maybe you are interested!

-

Test Results of Optimal Mode Effect on Mechanical Properties

Test Results of Optimal Mode Effect on Mechanical Properties -

Preliminary Test of Reliability of Scale in Research Model

Preliminary Test of Reliability of Scale in Research Model -

Profitability of Long-Term Investment Activities

Profitability of Long-Term Investment Activities -

Frequency Distribution of Test Results No. 2

Frequency Distribution of Test Results No. 2 -

Statistical Table of Test Results of Classes 10A1 and 10A6

Statistical Table of Test Results of Classes 10A1 and 10A6

Note: *, **, *** represent significance levels of 10%, 5% and 1% respectively.

Source: Results from STATA software

Through the regression results on the variables CAP, OC, CPI are significant at the 1% level, Size is significant at the 5% level and CR is significant at the 10% level. Based on the regression coefficient, we see that CAP, CR, OC have an inverse relationship with ROE, meaning that when the equity ratio decreases, other factors remain unchanged, ROE will increase, when the loan risk provision ratio on outstanding loans decreases, other factors remain unchanged, ROE will also increase. The variables Size, and CPI have

positive relationship with ROE. That means when a quantity increases and other factors remain constant, ROE will increase. In addition, the variables OC, OWN, LA are not statistically significant. That means they do not affect the fluctuation of ROE.

However, the expected result of the OWN variable is not statistically significant. When the assumption of no correlation between the independent variable and the error is violated, the endogeneity phenomenon occurs. The independent variable in the model plays both the role of an exogenous variable (due to its impact on Y) and an endogenous variable (due to its impact on error). The model with the independent variable being an endogenous variable is called an endogenous model. The endogenous phenomenon makes the estimates obtained by the classical linear regression method no longer consistent. As argued in the above section, the CAP variable is a suspected endogenous variable (Athanasoglou, 2008), so the following content will present the steps to handle endogeneity using the SGMM method. The results are based on the two-step system GMM model using the xtabond2 command introduced by Roodman (2009) as follows:

Table 4.8 Regression results according to SGMM

ROE

Coef. | Std. Err. | t | P>t | |

OWN | -0.033 | 0.016 | -2.090 | 0.050** |

Size | 0.028 | 0.007 | 3,880 | 0.001*** |

OC | -0.234 | 0.047 | -4.950 | 0.000*** |

CR | -1.070 | 0.869 | -1.230 | 0.233 |

CAP | -0.191 | 0.150 | -1.270 | 0.218 |

LA | 0.033 | 0.043 | 0.770 | 0.450 |

DOP | 0.027 | 0.029 | 0.930 | 0.365 |

GDP | -0.415 | 0.326 | -1.270 | 0.219 |

CPI | 0.105 | 0.056 | 1,860 | 0.079* |

year | -0.007 | 0.002 | -3.120 | 0.006 |

_cons | 13,453 | 4,363 | 3,080 | 0.006 |

Note: *, **, *** represent significance levels of 10%, 5% and 1% respectively.

Source: Results from STATA software

Model reliability testing:

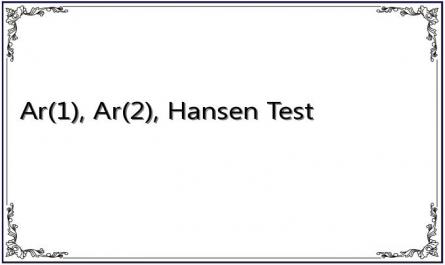

Table 4.9 AR(1), AR(2), Hansen Test

Arellano-Bond test for AR(1) in first differences: z = -2.39 Pr > z = 0.017 Arellano-Bond test for AR(2) in first differences: z = -0.56 Pr > z = 0.578

-------------------------------------------------- ----------------------------

Hansen test of overriding. restrictions: chi2(13) = 9.69 Prob > chi2 = 0.719 (Robust, but weakened by many instruments.)

Source: Results from STATA software

Based on the regression results table, we have p-value AR(1) = 0.017 < 5%. Thus, in this test, we reject H0, which means there is first-order autocorrelation. Testing for second-order autocorrelation AR(2), we have p-value = 0.578 > 5%, which means there is not enough evidence to reject H0, accepting H0 means the model does not have second-order autocorrelation. At the same time, Hansen's test has p-value = 0.719 > 5%, accepting the hypothesis H0. Therefore, the model is valid, the instrumental variable is appropriate. Thus, all results in SGMM are significant.

4.5 Discussion of research results

The study was developed based on empirical evidence related to the impact of state ownership on the profitability of Vietnamese joint stock commercial banks. After using the overall OLS model to test the relationship between state ownership and capital structure, the random effects model was used to handle the problem of heterogeneity and unobserved phenomena. However, the results of the model all showed that the state ownership form had no impact on the profitability of the bank. The reason for the biased results is due to the endogenous factor in the model and according to Athanasoglou (2008), CAP is the endogenous variable and also based on the study of Athanasoglou (2008), the GMM method was used. The GMM dynamic model solves problems related to short time series data. Second, the model

The GMM model will be more accurate in the existence of endogeneity of the CAP variable (equity/total assets ratio) Athanasoglou (2008).

The results of the SGMM model supported the hypothesis that ownership form has a negative correlation with bank profitability, at the 5% significance level. Specifically, with the dummy variable included in the research model 1 being joint-stock commercial banks with the state holding the majority stake and 0 being joint-stock commercial banks, the regression coefficient result = -0.033 means that when all factors remain constant, the profitability of the group of joint-stock commercial banks with the state holding the majority stake is lower than that of the group of joint-stock commercial banks. This result is consistent with the expectation and research of Kieu Huu Thien et al. (2014) and many other countries also gave results that coincide with this research. This result can be explained as follows: the lending objects of State-owned commercial banks are state-owned enterprises, with relatively large outstanding loans, but state-owned enterprises are considered to operate inefficiently, and these loan objects are often applied by the Bank with low interest rates, thereby affecting the Bank's income. Another reason is that State-owned commercial banks are also a channel for managing and implementing State policies, investing in projects with high social value and low yield. This result shows the importance in the restructuring project of the Vietnamese banking system is to reduce the state ownership ratio in joint-stock commercial banks in which the State holds controlling shares so that banks operating under market mechanisms can promote their strengths and maximize profitability.

Bank size has a positive relationship with the profitability of the Bank with a significance level of 1%. This means that the larger the bank size, the higher the profitability of the Bank. The regression results are consistent with the research results of Emery (1971), Akhavein et al. (1997), Bourke (1989), Molyneux and Thornton (1992), Bikker and Hu (2002), Goddard (2004) and expectations. The results are opposite to the research of Stiroh and Rumble (2006). Compared to banks in the world, the scale of Vietnamese commercial banks is still quite modest, so increasing the scale for banks

The current Vietnamese Joint Stock Commercial Bank does not reduce operational efficiency due to administrative costs as the research results of Stiroh and Rumble (2006) but will contribute to increasing the competitive potential of banks. This result is somewhat important in the current period, when merger activities between banks are taking place vigorously. Two or more banks merging together will create a larger scale. From there, it will create a better capital supply capacity to increase the profitability of the bank.

According to the research results with a significance level of 1%, the ratio of operating expenses to total operating income has a negative relationship with the profitability of the Bank. This result is consistent with the arguments of Athanasoglou (2008), Alexiou and Sofoklis (2009) Trujillo-Ponce (2013) and the initial expectation. Operating cost management is an important factor affecting the profitability of Vietnamese joint stock commercial banks. The negative relationship implies that an increase in operating costs will reduce the bank's profits, thereby reducing the bank's profitability. Thus, to increase profitability, joint stock commercial banks need to control their operating costs well and increase operational efficiency.

The thesis did not find any relationship between the ratio of outstanding loans/total assets, the ratio of loan loss provisions/total loans, the ratio of customer deposits/total liabilities, the ratio of equity/total assets with the profitability of the Bank. That means that outstanding loans, loan loss provisions, customer deposits and equity do not affect the profitability of Vietnam Joint Stock Commercial Bank in this period. Due to the current trend of commercial banks expanding to non-credit business and only good credits can increase the profitability of the bank, if the outstanding loans are high and the bad debt ratio is also high, it cannot increase the profitability of the bank, the same result is also found for credit risk provisions. In addition, the results show that customer deposits have no impact on the profitability of Vietnamese commercial banks, contrary to the findings of Athanasoglou et al. (2006), Zhang (2013). This can be explained by the fact that commercial banks are not yet free in deposit interest rates, so almost

The interest rate level mobilized in the market is equal, not creating advantages in terms of scale and reputation of the bank. The equity ratio is not statistically significant for Vietnamese commercial banks, different from the research results of Athanasoglou et al. (2008) and Pasiouras and Kosmidou (2007) when they said that the more equity held, the higher the profitability. This result can be explained by the current situation that the capital structure of banks is a matrix of cross-ownership of investors' capital, thus distorting the nature of equity in the capital sources of Vietnamese commercial banks.

Two factors represent the macroeconomic situation in which CPI is significant at the 10% level and has a positive correlation with profitability. This result is consistent with the research of Alexious and Sofoklis (2009), Kasman (2010), Kunt and HuiZinga (1999). This means that when inflation increases, the profitability of banks will increase. This can be explained by the fact that when inflation increases, lending interest rates increase, but deposit interest rates and other operating costs increase more slowly, so the additional income is greater than the additional cost, which increases the profitability of the bank. On the contrary, the GDP growth rate has not really affected the profitability of banks, this result is similar to Trujillo-Ponce (2013) research on Spanish commercial banks in the period 1999-2009. That is, the economic cycle has no significance for the operations of Vietnamese joint stock commercial banks.

In summary, the model results have answered the research question that the form of state ownership has an impact on the profitability of Vietnamese joint stock commercial banks, and joint stock commercial banks have higher profitability than joint stock commercial banks with state-controlled shares. In addition, the size of total assets and the ratio of operating expenses to total operating income and the inflation rate represented by the CPI variable also affect the profitability of the Bank.

CONCLUSION OF CHAPTER 4

Based on the theoretical foundation, chapter 4 presents an empirical research model to study the relationship between profitability and ownership form of Vietnamese joint stock commercial banks, including the dependent variable measuring the profitability of commercial banks is ROE, independent variables include: Ownership form (OWN), and control variables include: Total asset size (SIZE), Operating expenses (OC), Credit risk (CR), Owner's equity (CAP), Loan outstanding ratio/Total assets (LA), Customer deposit ratio/Total liabilities (DEP), Economic growth rate (GDP), Inflation (CPI). In which the CAP variable is included in the model as an endogenous variable. To handle endogeneity, the regression method used is SGMM, the model results show that the form of state ownership affects the profitability of the Bank, the regression coefficient has a negative value, meaning that the profitability of joint stock commercial banks with the state holding controlling shares is lower than that of joint stock commercial banks. At the same time, it also proves that the larger the total assets and inflation, the higher the profitability, on the contrary, the higher the ratio of operating expenses to total operating income, the lower the profitability.

CHAPTER 5: CONCLUSION AND RECOMMENDATIONS

5.1 Conclusion of model results:

With the aim of measuring the impact of ownership form on bank profitability through experiments, the study used balance sheet data of 20 commercial banks in the period from 2007 - 2014. Based on an overview of issues related to bank profitability, the thesis has built a proposed research model based on theoretical foundations and previous studies.

Through the process of collecting sample data as a basis for testing and explaining the model, the thesis used the following statistical tools:

- Use Hausman Test to choose FE and RE method. The test result has p-value > 5%, so the study chooses RE method. To choose between RE and Pooled OLS method, the thesis uses Breusch-Pagan test and the result has p-value < 5%, supporting the choice of RE method. However, the regression result according to RE does not find the relationship between state ownership form and bank profitability. The reason is due to the endogeneity problem for the explanatory variable CAP.

- To handle endogeneity, the thesis uses a dynamic model in which the dependent variable is lagged for one period as the dependent variable, the regression method used is SGMM.

- Testing the reliability of model results according to SGMM includes: AR (1), AR (2) and Hansen test are all satisfied, proving that the model results obtained are reliable.

The summary of regression results using OLS, RE, SGMM methods is presented in the following table: