Expand credit, grow new loans safely and effectively to offset losses from outstanding debts.

* Debt collection after processing

If setting up and using provisions to handle risks is a very important part of the credit risk management process, it shows the proactiveness in dealing with losses caused by credit risks, then debt recovery after handling proves the business efficiency of a bank, because all the money collected from debts transferred to off-balance sheet accounts is included in the income and increases profits.

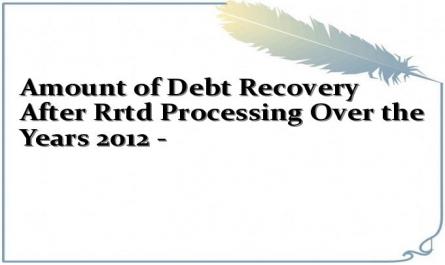

Table 2.7 shows debt collection after handling RRTD of NHNo&PT branch

Phuc Tho district

Table 2.7: Amount of debt recovered after handling RRTD over the years 2012 -

2014

Unit: Billion VND

STT

Target | 2012 | 2013 | 2014 | ||||

KH | TH | KH | TH | KH | TH | ||

1 | Amount of debt collected has been XLRRTD | 1.5 | 3.9 | 0.7 | 1 | 0.6 | 1.4 |

2 | Balance has been XLRR | 8,392 | 4,492 | 3,492 | |||

3 | Revenue rate compared to customer delivery | 260% | 142.8% | 233.3% | |||

4 | Collection to Debt Ratio XLRR | 46.5% | 22.3% | 40% | |||

Maybe you are interested!

-

Basic Issues of Credit, Credit Risk and Bad Debt of Commercial Banks

Basic Issues of Credit, Credit Risk and Bad Debt of Commercial Banks -

Solutions to Improve Credit Risk Management Capacity, Specialize Bad Debt Handling Activities

Solutions to Improve Credit Risk Management Capacity, Specialize Bad Debt Handling Activities -

Credit risk management at Vietnam International Commercial Joint Stock Bank - Hanoi Branch - 12

Credit risk management at Vietnam International Commercial Joint Stock Bank - Hanoi Branch - 12 -

The Impact of Bad Debt on the Operations of Credit Institutions

The Impact of Bad Debt on the Operations of Credit Institutions -

Credit risk management for personal loans at Nam A Commercial Joint Stock Bank - Quang Ninh Branch - 13

Credit risk management for personal loans at Nam A Commercial Joint Stock Bank - Quang Ninh Branch - 13

( Source: Business performance summary report of the branch of NHNo &PTNT Phuc Tho district)

The above table shows that the branch pays great attention to debt collection after handling RRTD, the targets over the years have been completed and exceeded the plan assigned by the Ha Tay Provincial Bank for Agriculture and Rural Development - Hanoi City, in order to increase financial capacity to ensure exceeding the annual financial coefficient with productivity. The above table also shows that over the years, the debt collection rate has been XLRR compared to the actual debt transferred.

Off-balance sheet monitoring at branches has continuously increased. This result is due to the good performance of the bad debt handling and collection team, with many initiatives and measures applied to the CBTDs. For example: Regularly organizing analysis of debt that has been handled at risk to plan for collection at transaction offices and centers; Launching emulation campaigns associated with rewarding individuals and groups with good achievements in reducing off-balance sheet debt monitoring; for debts that have been handled at risk and clearly identified as the cause of the risk as the CBTD's subjective fault, the CBTDs are temporarily not entitled to receive business salary, focusing time on debt collection... etc. All of the above measures have contributed to improving the effectiveness of debt collection in particular and the effectiveness of RRTD management in general.

2.3. ASSESSMENT OF THE CURRENT STATUS OF CREDIT RISK MANAGEMENT AT THE BANK FOR AGRICULTURE AND RURAL DEVELOPMENT OF VIETNAM - PHUC THO DISTRICT BRANCH, HANOI CITY

2.3.1. Results achieved

2.3.1.1. The branch has strictly implemented credit policies and procedures.

Strictly implementing credit policies, debt classification and customer rating policies, and current credit manuals are among the most important issues to prevent and limit credit risks. The branch of the NHNo&PTNT in Phuc Tho district has strictly complied with credit policies. Lending ensures the industry's regulations and rules, from the stage of establishing credit records, disbursing and settling loans are carried out synchronously, the work of prevention, provisioning, and using provisions to handle credit risks is in accordance with Decision 493/QD-NHNN and Decision 469/QD-HDTV-XLRR of the Board of Members of the NHNo&PTNT Vietnam and implementing guidelines. In addition, the branch of the NHNo&PTNT in Phuc Tho district has strictly implemented the provisions of law and the banking industry on lending limits.

for a customer; comply with regulations on safety ratios in the operations of credit institutions, including: Minimum capital safety ratio, liquidity ratio, maximum ratio of using short-term capital for medium and long-term lending; deploy and implement Decision No. 1627/2001/QD-NHNN dated December 31, 2001 of the Governor of the State Bank promulgating the Regulations on lending by credit institutions to customers; Decision No. 457/2005/QD-NHNN dated April 19, 2005 of the Governor of the State Bank on safety ratios in the operations of commercial banks; Decision No. 493/2005/QD-NHNN and other implementing documents; Decision No. 115/QD-HDQT-KHTH dated May 19, 2005 of the Board of Directors of the Vietnam Bank for Agriculture and Rural Development on promulgating regulations on developing and organizing the implementation of business plans for transaction offices and branches in the system of the Vietnam Bank for Agriculture and Rural Development...

Good compliance with credit policies and procedures at the district center and transaction offices in the area has maximized the advantages to improve the effectiveness of credit risk management at the branch of the Bank for Agriculture and Rural Development of Phuc Tho district.

2.3.1.2 Implement credit granting and credit risk management within a system of synchronous and tight credit policy and mechanism framework

As a branch in the system of Vietnam Bank for Agriculture and Rural Development - one of the largest banks in Vietnam, Phuc Tho District Branch has a clear strategic orientation and credit policy guidance, reflected in the development strategy of commercial banks until 2020, the annual credit plans of commercial banks and specifically the annual credit plan of the Branch; The Branch applies a fairly synchronous credit policy framework issued by commercial banks, including regulations on granting and managing credit limits, Credit Council regulations, co-financing regulations, debt classification regulations, risk provisioning and risk provisioning and use, lending regulations, loan security regulations, problem debt handling regulations, and guiding documents in each period.

The period ensures the flexibility of the regime documents according to market developments... Credit business processes are standardized according to ISO 9001:2000 standards.

Credit policy always aims to serve the reasonable needs of customers and ensure risk control, which has increased the competitiveness of the Branch compared to other credit institutions in the same area. Credit policy is extended to all customers; customers are treated equally in credit; there are preferential policies for strategic partners and customers who bring great overall benefits to the Branch;

The specific risk management policy ensures control of all risks in over-granting, managing credit limits and specific credit amounts through the credit appraisal process, monitoring the use of capital, collateral, credit contracts and financial capacity of customers.

2.3.1.3 Proactively build and manage the overall loan portfolio at the branch

Based on the credit orientation of the Vietnam Bank for Agriculture and Rural Development, the Phuc Tho District Bank for Agriculture and Rural Development Branch has specified the branch's credit portfolio, ensuring that it is suitable for the characteristics of customers at the branch, suitable for the characteristics of the socio-economic situation in the operating area, while still ensuring compliance with the credit orientation of the Vietnam Bank for Agriculture and Rural Development. From there, identify risks, measure risks, and propose credit response measures for the overall credit portfolio at the branch.

2.3.1.4. Diversify the loan portfolio and customers; strictly implement the lending judgment rights prescribed by the NHNo&PTNT Ha Tay branch and set limits on lending judgment rights for affiliated transaction offices.

In recent years, the activities of the NHNo&PTNT branch in Phuc Tho district have gradually diversified their loan portfolio, not only focusing on

in the main field of rural agriculture but also expanded lending to a number of large projects. The expansion of lending fields and diversification of customers have created a basis for limiting credit risks. In addition, based on the lending decision rights prescribed by the NHNo&PTNT Ha Tay branch for the branch. The Director of the NHNo&PTNT Phuc Tho district directed the strict implementation and limited the lending decision rights for direct transaction offices, thereby contributing to improving the efficiency of credit management work of the entire branch.

2.3.1.5. Do a good job of credit analysis

Credit analysis is a regular task of the CBTD, through the information channels that the CBTD collects. For a branch that operates mainly in rural areas such as Phuc Tho district, the information is mainly collected through sources such as customers, relationships with partners, with residential groups, local authorities, and the State Bank credit information center. The information provided is screened, selected, analyzed and proposed by the CBTD to advise the Director to make credit decisions. Thanks to that, for many years, the branch of the NHNo&PTNT Phuc Tho district has always achieved the criteria for credit efficiency, the ratio of bad debt/total outstanding debt is always at the allowable level (under 3%/total outstanding debt).

2.3.1.6. Expanding secured lending

In accordance with current regulations on loan security, most loans for all types of enterprises and production and business households in the area must be secured by assets. Particularly for farming households that borrow up to 50 million VND, they can borrow without having to mortgage assets, but the bank only holds the assets for them.

Outstanding loans secured by assets of the NHNo&PTNT Phuc Tho district as of December 31, 2014 were 420.4 billion VND, accounting for 99.85% of total outstanding loans. The types of assets commonly accepted as collateral for loans are: land use right certificates, houses, and architectural structures attached to residential land;

Factory systems, machinery and equipment; means of transport such as cars, boats; valuable papers such as savings books, promissory notes; ... The increase in secured loans of the Bank for Agriculture and Rural Development of Phuc Tho district in recent times has contributed to stabilizing credit activities and limiting possible risks.

2.3.1.6. Strengthening inspection and control of TD

The NHA&PTNT Phuc Tho District conducts pre-, during- and post-lending inspections in accordance with the regulations issued by the NHA&PTNT Vietnam, in conjunction with the appraisal, disbursement, and cash flow monitoring and management processes after lending. Periodically or unexpectedly, the internal inspection department conducts inspections and monitors compliance with regulations and procedures, detects errors in the lending and debt collection process, and makes appropriate recommendations for corrections, in order to prevent and handle credit risks. Some measures applied at the branch such as sending open letters to solicit customer opinions, periodically organizing loan reconciliation, and changing locations for CBTDs who have a period of time in charge of the location according to regulations have brought about clear results.

2.3.1.7. Improve professional capacity and ethics of CBTD

Professional competence and professional ethics of staff are indispensable conditions for the work of preventing and handling credit risks. The branch of the Bank for Agriculture and Rural Development in Phuc Tho district has conducted professional training sessions, regularly sent staff to attend courses to improve their professional qualifications, appraisal courses, and equip them with legal knowledge and foreign knowledge related to credit work organized by the Bank for Agriculture and Rural Development in Ha Tay branch.

In addition, the Branch Management Board always pays attention to education, improving professional ethics for staff, timely rewards and discipline. Thereby, the staff's qualifications are increasingly improved, there are no ethical risks in credit work, ensuring the safety of capital, assets and people.

2.3.2 Limitations and causes

2.3.2.1 Limitations

Although achieving significant results, the Branch's credit risk management still does not meet requirements, credit risks still occur:

The ratio of overdue debt/bad debt is high and tends to increase. Credit activities with the main investment direction on households and individuals are mainly, this shows that the shift in the structure of lending towards diversification is not positive; there are no appropriate credit policies and mechanisms for each customer area. Therefore, the volume of bad debt concentrated in the customer group of households and individuals in previous years is still high.

The increase in overdue debt ratio in all debt groups shows that: in addition to old overdue debts that customers continue to default on, leading to a jump to a higher debt group, the loan portfolio at the branch continues to generate new overdue debts, which shows that loans at the bank are potentially risky.

The bank uses risk handling measures to transfer off-balance sheet irrecoverable debts with balances that increase steadily over the years. Although this reflects proactive response to credit risk, it also reflects the high state of credit risk at the branch of the Bank for Agriculture and Rural Development in Phuc Tho district. Risk handling with increased risk provisions over the years increases capital costs and reduces bank profits.

- Bad debt ratio is low but does not ensure stability and solidity.

- There is still a phenomenon that, in order to ensure the financial plan, bad debts that are not really recoverable are not handled, but those that are recoverable are handled and then debt collection is focused on to clean up off-balance sheet debt . If this measure is abused for a long time, it will create a bad precedent, not reflecting the true nature of RRTD and risk handling.

2.3.2.3. Causes

* Subjective causes

First, the content of risk management is not comprehensive.

The content of credit risk management only focuses on measuring risks, not on detecting and warning about potential risks. The branch has many risk control tools. But it has not yet fully utilized the tools and policies of risk management.

Credit risk identification content at branches is still limited.

The awareness of the staff at the branch about credit risk management is still limited, they underestimate the assessment and recognition of risk signs in the pre-credit and credit granting stages, mainly waiting until credit risks have occurred to find solutions to resolve and handle risks.

In many cases, credit officers have not strictly complied with the regulations in credit appraisal, leading to inaccurate appraisal results. The Vietnam Bank for Agriculture and Rural Development and its branches have specific instructions on selecting customers' financial reports for analysis. In cases where the financial reports provided by customers are not reputable (such as not being independently audited, or the auditing organization is not reputable...), the appraisal officer must check and verify the accuracy of the data, make adjustments to the financial reports to suit the customer's reality and the regulations of the Ministry of Finance; then analyze the production and business situation and the financial situation of the customer based on the adjusted financial reports. However, many appraisal officers have skipped this step or are not qualified enough to detect unreasonable points in the financial reports provided by customers for adjustment, leading to inaccurate appraisal results and proposed credit decisions.

Customer relations officers have not seriously carried out the inspection, evaluation/re-evaluation of collateral assets. This is extremely dangerous because most of the collateral assets at the branch are real estate, during the period when the real estate market was frozen, the value of collateral assets has decreased sharply compared to the time.