Successfully implement long-term plans in VIB's business strategy and especially improve the quality of Customer Service towards international standards.

2.2.1.2. VIB's vision, mission, core values, and business strategy

VIB Bank's goal is: "VIB becomes one of the three leading joint stock commercial banks in Vietnam by 2013". This is a very clear, specific and bold goal. It demonstrates the determination of the Board of Directors as well as all employees of the bank in a period when other banks are strongly innovating.

As one of the pioneering banks in reforming business operations, VIB always focuses on customers, takes service quality and creative solutions as its business motto with the determination to "become the most creative and customer-oriented bank in Vietnam" . One of the missions identified by VIB's board of directors since its inception is "Excellence in providing creative solutions to satisfy customers' needs to the maximum". Therefore, VIB has been increasing the efficiency of capital use, along with management and operation capacity, continuing to focus on developing the retail banking network and new products through diverse distribution channels to provide comprehensive financial solutions for key customer groups, while improving service quality to serve customers better and better.

VIB International Bank - Hoan Kiem Branch, or VIB Hoan Kiem for short, was established on December 27, 2004, and is one of 35 branches in Hanoi. VIB - Hoan Kiem Branch was established due to VIB's market development needs, to meet the development requirements of a business, and based on the actual needs of the market for the financial products that VIB serves.

2.2.2. Main business performance results of VIB International Bank in recent years

2.2.2.1. General business performance of the bank

After 15 years of operation, Vietnam International Bank (VIB) has achieved many successes and created the image of a modern and professional bank. Through the numbers and growth charts, we can see that. We see that the growth rate of Total Assets, Owner's Equity and Charter Capital all had remarkable growth rates in the period of 2005 and 2007 (average on

330%). It can be seen that the bank's Board of Directors and all employees have successfully grasped and taken advantage of the general development stage of the entire market when the banking and securities markets exploded.

Chart 2.1 Performance of International Bank over the yearsSource: International Bank Annual Report 2011 |

Maybe you are interested!

-

Mission - Vision - Core Values of the Hospital

Mission - Vision - Core Values of the Hospital -

Some recommendations to improve the business strategy of Tay Ho Tourism Service Company - 9

Some recommendations to improve the business strategy of Tay Ho Tourism Service Company - 9 -

Solutions to complete the business strategy of Thu Do Industrial Trading Joint Stock Company - 1

Solutions to complete the business strategy of Thu Do Industrial Trading Joint Stock Company - 1 -

Values, Beliefs and Attitudes of Business Members.

Values, Beliefs and Attitudes of Business Members. -

Some Solutions to Improve the Efficiency of Integrating Human Resources Activities with the Business Strategy of Waterway Construction Joint Stock Company

Some Solutions to Improve the Efficiency of Integrating Human Resources Activities with the Business Strategy of Waterway Construction Joint Stock Company

According to the analysis of Vietcombank Securities Company - Assessment Report of some credit institutions, VIB Bank is ranked in Group 2 (Group of average banks including VIB, SHB and Seabank, Oceanbank, Lien Viet Bank). VIB is the bank with the largest total assets (VND 96,950 billion) and equity (VND 8,160 billion). Not only that, VIB also leads this group in both mobilization and lending, but the mobilization growth rate is low at 4.8%.

Chart 2.2 Comparison chart of credit and mobilization activities of banks

1.85

Report on banking activities 2011 - Vietcombank Securities Company Limited Chart 2.3 Bad debt ratio of VIB bank over the years

Bad debt ratio

3

2.5

2

2.69

1.5

1.59

1

0.5

0

2007.5 2008 2008.5 2009 2009.5 2010 2010.5 2011 2011.5

1.27

Bad debt ratio

Source: Student synthesis

36.37

%

Corporate Debt

63.63

%

Personal Debt

41.90

%

58.10

%

Corporate Debt

Chart 2.4 Debt structure of VIB bank through the years 2010, 2011 Debt structure by customer group

Debt structure in 2010

Debt structure in 2011

Personal Debt

Debt structure by economic sector

4.70%

Debt structure by industry in 2011

1.55%

Agriculture and forestry

35.06%

47.65%

5.18%

Debt structure by industry in 2010

1.21%

40.13%

43.90%

Agriculture, Forestry, Trade, Manufacturing , Construction

Transport warehouse

Other

Manufacturing trade

Build

Other transportation warehouses

0.81%

0.37%

0.62%

Debt structure by debt group:

Debt structure by debt group in 2010

0.16%

98.04%

Group 1

Group 2

Group 3

Group 4

Group 5

Debt structure by debt group in 2011

0.58%

5.74% 0.95%

1.16%

91.57%

Group 1

Group 2

Group 3

Group 4

Group 5

Source: students self-synthesized from the report of the Board of Supervisors of VIB Bank - 2011

In my opinion, the above results come from a number of objective and subjective reasons such as the impact of the macroeconomic situation and tight monetary policy, plus the fact that business indicators have not been adjusted to suit the practical situation.

According to Ms. Duong Thi Mai Hoa, General Director of VIB Bank, if we analyze the numbers, we will see many positive signs. Although the credit growth rate is only over 4%, this is a number that is consistent with the ability to manage risks and is a safety rate for VIB when many consequences of too fast credit growth are seen after 1-2 years. At the same time, the increase in charter capital and equity along with the additional investment of 1,150 billion VND from Common-wealth Bank of Australia (CBA) - a foreign strategic shareholder, demonstrates the attraction and great potential of VIB in the eyes of foreign investors.

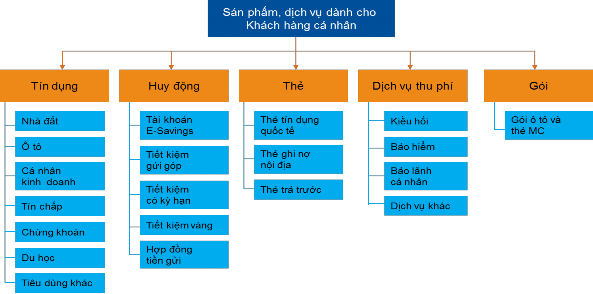

2.2.2.2. Retail banking services

In the general shift of the domestic banking system - that is, making individual customers the target customers of the bank - VIB also makes individual customers its spearhead target . This can be clearly seen when VIB appointed Mr. Richard Harris - a CBA expert to Vietnam under the Capacity Transfer Program (CTP), when CBA became a strategic shareholder of VIB - to take on the position of Director of Retail Banking. This clearly shows VIB's strategy of making retail banking services a focus in the development process and orienting this service towards international standards.

Along with that, VIB has applied many important changes in the organizational structure of the Retail Banking Division to ensure the operational efficiency of the Departments and business units. VIB continues to successfully transform into a new sales and service model and invest heavily in expanding the service network to get closer to customers, improving the ability to serve customers' needs to the maximum. The performance evaluation and management system has been deployed to help employees accurately evaluate the work efficiency they have achieved in order to build a culture that focuses on work efficiency and takes customer satisfaction as a measure of success.

|

Source: Internal training documents and bank website on products and services |

Figure 2.1 Products for individual customers of International Bank

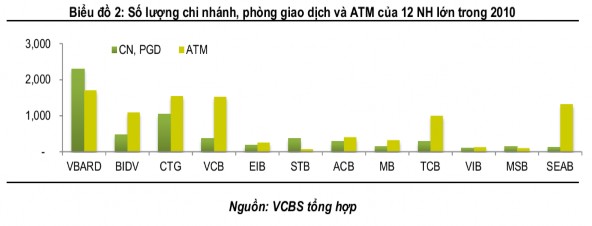

Chart 2.5 Number of branches, transaction offices and ATMs of 12 major banks in 2010

|

Source: Report on banks – Vietcombank Securities Company Limited |

As one of the first joint stock commercial banks to apply the non-physical distribution channel model with the orientation of becoming the leading retail bank in the market and providing services without space and time restrictions for customers, VIB has constantly strived to expand its customer service scope through online transaction channels and ATM network.

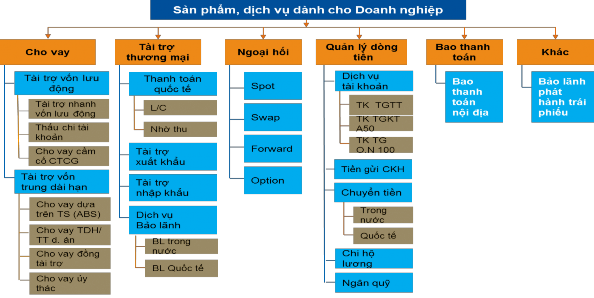

2.2.2.3. Wholesale banking services – Corporate Banking:

The corporate customer service segment has always been a strength and has contributed a very important part to VIB's business activities. Along with the strong development of the country's economy, at the same time, to meet the increasing demands of Vietnamese enterprises as well as foreign-invested enterprises (FDI) operating in Vietnam.

|

Source: Internal training documents and bank website on products and services |

Figure 2.2 Products for corporate customers of International Bank

FDI and small and medium enterprises (SME) customer groups: The two customer groups that VIB has been particularly targeting in recent years are foreign-invested enterprises and small and medium enterprises (SMEs). With efforts, in just 3 years 2009, 2010 and 2011, VIB has begun to break through and affirm its position in the market by serving more than 5,000 new small and medium enterprises (SMEs), increasing the total number of VIB's corporate customers to more than 20,000 enterprises. In addition, VIB has continuously improved its capacity in serving selected large corporate customers. Product and service policies are developed and designed to suit the specific needs of enterprises, in which service quality is given top priority.

Modern international payment services: With a modern centralized payment model, VIB continuously improves the quality of international payment services to meet the needs of import-export enterprises. Especially in 2011, VIB continued to invest in technology, equipment and experienced staff with a reputable correspondent banking network worldwide. With abundant foreign currency capital, VIB has provided high-quality international payment services to enterprises such as: fast international money transfer, issuance and payment of export letters of credit, export collection and issuance of foreign counter-guarantees...

Cash flow management is increasingly effective for businesses:

Cash flow management solution packages including receivables management, payables management and centralized account management are designed by VIB to serve the specific characteristics of each business with the motto: Customers only need to transact with a single bank for all liquidity management requirements.

In addition to efforts to serve businesses better, VIB also builds policies and incentives to provide a comprehensive service for corporate employees with the Payroll Multi-utility Salary Package Service. By the end of 2011, more than 600 new businesses had used this service, bringing the total number of businesses using Payroll to 2,000.

VIB4U Online Banking: The number of businesses using VIB4u Online Banking service is increasing. In 2011, there were nearly 1,000 new businesses using it, bringing the total number of businesses using this service at VIB to

5,000 enterprises. In addition to the continuous efforts to improve quality and technology to serve SME customers, 2011 marked a big step forward for VIB4U Online Banking service with the successful deployment of services for large corporate customers, such as: AAA Insurance Corporation, HPT Information Technology Corporation, Parkson Vietnam. At the same time, VIB also offers synchronous, integrated solutions to manage cash flow and liquidity of enterprises in the form of product packages, meeting the models of Parent - Subsidiary companies, Corporations - Member companies.

2.2.2.4. Risk management:

In the context of rapidly increasing bad debts of Vietnamese banks affecting the safe operation of the system, the issue of Risk Management has been given top priority by VIB's Board of Directors. Maintaining good credit quality, controlling bad debts and preventing operational risks due to fraud, deceit, violations of professional ethics, etc., VIB will become safer to ensure sustainable development in recent years. With support through the transfer of capacity from strategic shareholder CBA - one of the world's leading safe banks - VIB is increasingly perfecting its structure, framework and risk management policies.

Credit risk management : Recognizing risks and threats from the market that can directly and indirectly affect credit granting activities and cause losses to VIB, the Board of Directors and the Executive Board of VIB have focused on promoting credit risk management throughout the system. Project Review of the Portfolio