power distance, uncertainty avoidance, and long term orientation.

Individualism is the opposite of collectivism . Individualism is characterized by loose social contracts and a greater emphasis on the role of the individual. On the contrary, in a society that emphasizes the role of the collective, every member is greatly dependent on groups in society.

Power distance is the degree to which hierarchy and unequal distribution of power are accepted in institutions and organizations. This dimension affects the behavior of members with less or more power in a society. In a high power distance society, people are more likely to accept hierarchical arrangements without any justification. These hierarchies are explained by power and tradition.

Uncertainty avoidance is the degree to which an individual feels threatened by unknown situations or risks in life. It is expressed in the need for clear, predictable, and formal rules. Cultures with high uncertainty avoidance tend to develop and maintain rigid rules and tend to resist behaviors and ideas that contradict common norms.

Long-term orientation is a characteristic of cultures that emphasize the adaptation of tradition to modern needs, emphasize social obligations and status within the limits of costs, save resources and thus have enough capital for investment, persevere to achieve results gradually and support individuals to achieve goals. In contrast, short-term oriented cultures respect tradition, emphasize social obligations and status, do not care about costs, save low levels and therefore have insufficient resources for investment, maintain outward appearances. It is easy to see that in long-term oriented societies tend to be more conservative and law-abiding than short-term oriented societies.

Hofstede's research became the foundation for many branches of business science including accounting. Based on cultural aspects, Gray [95] has

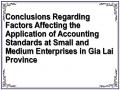

The analysis of the influence of culture on the development of accounting systems in countries is presented in Figure 1.1.

External influences Natural environment Commerce

Invest

Conquest (political)

The importance of institutions

Legal system

Business Ownership Capital Markets

Professional Organizations Education

Religion

Environmental impact

Economic Geography

Demographics Genetics History

Urban Engineering

Social value

Accounting value

Accounting system

Figure 1.1. The influence of culture on accounting ( Source: Gray [95])

The accounting values in the above diagram include four attributes: professionalism, uniformity, prudence and confidentiality. The relationship of each of these aspects has been empirically studied by many scholars in developed countries to examine the correlation between accounting and culture [71] [110] [148]. For example, professionalism is highly promoted when enterprises operate in an environment where individuality is promoted, maintaining self-established regulations of professional organizations instead of following the provisions of the law. The most specific manifestation of this issue is the role of professional accounting organizations in countries following the Anglo-Saxon model. Uniformity over flexibility shows the priority of implementing a unified accounting regime among enterprises and the consistent use of those regimes over time compared to flexibility in applying accounting in specific enterprises and situations. Conservatism versus optimism reflects the measurement of uncertain future events versus a more optimistic, fair-minded, risk-taking approach. Confidentiality versus openness reflects the preference for disclosure of information to

those who have close contact with the manager or tend to disclose transparently and openly to the public about financial figures.

The above theoretical foundations are often used to study the development of accounting systems in countries, but when considering the application of accounting standards from the business side, the cultural factor cannot be ignored because the application of accounting is carried out by people in a specific economic - cultural - social environment. In the context of Vietnam, a country that has long been influenced by Chinese culture, the French colonial process, was a member of the socialist bloc and has implemented economic renovation for more than 40 years, so these factors have a significant impact on the institutional aspects and habits in accounting work. Therefore, the theory of culture to some extent also needs to be used to explain the application of accounting standards in businesses.

1.3. Overview of small and medium enterprises

1.3.1. Concept of small and medium enterprises

Up to now, there is still no consensus in the world on the concept of what is called a small and medium enterprise, but this concept is determined by different criteria according to each country and each different industry. Therefore, the concept of small and medium enterprises in the world can be determined by criteria such as: geographical location, scale, number of years of establishment, enterprise structure, number of employees, revenue, net assets, ownership structure, nnnmbnnb nhbjhjtechnological innovation ... [82]. From a quantitative perspective, the concept of small and medium enterprises implies enterprises that some standards of scale are measured [101]. Standards of scale are often expressed through indicators such as: profit, investment capital, total assets, contributed capital, number of employees, revenue ... Based on this criterion, many countries and associations have issued standards to divide enterprises into large, medium or small enterprises.

In Vietnam, the scale standard is based on a combination of two criteria: capital and number of employees . 2. Small and medium enterprises are business establishments that have registered their business according to the law, divided into three levels: micro, small, and medium.

2 According to Decree 56/2009 dated June 30, 2009, this combination is the basis for dividing into medium-sized enterprises, small enterprises and micro-enterprises.

According to the scale of total capital (total capital is equivalent to total assets determined in the balance sheet of the enterprise) or the average number of employees per year (total capital is the priority criterion), specifically: According to Decree No. 56/2009/ND-CP of the Government issued on June 30, 2009 [27], SMEs are divided by industry, including: agriculture, forestry and fishery; industry and construction; trade and services. In addition, the main criteria for classifying SMEs in Vietnam are the number of employees and capital, but it is not clear whether it is the average number of employees or the number of employees at the time of classification (because this is a criterion that almost continuously fluctuates during the business year); nor is it clear whether the capital is the registered business capital on the license or the average operating capital of the enterprise.

According to Circular No. 16/2013/TT-BTC dated February 8, 2013 of the Ministry of Finance, SMEs are identified as follows: SMEs include branches, affiliated units but with independent accounting, cooperatives (using less than 200 employees, working full-time and having annual revenue not exceeding 20 billion VND).

According to Article 6 - Decree No. 39/2018/ND-CP issued on March 11, 2018 detailing a number of articles of the Law on Support for Small and Medium Enterprises, the criteria for determining small and medium enterprises according to the table are determined as follows:

Table 1.1. Criteria for determining small and medium enterprises according to Decree No. 39/2018/ND-CP

Area

Scale – Criteria

Industry, agriculture, forestry industry and construction | Trade and service | ||

Business microscopic | Number of employees | 10 people or less | 10 people or less |

Or capital | 3 billion VND or less | 3 billion VND or less | |

Or revenue | 3 billion VND or less | 10 billion VND or less | |

Business small | Number of employees | 100 people or less | 50 people or less |

Or capital | 20 billion VND or less | 50 billion VND or less | |

Or revenue | 50 billion VND or less | 100 billion VND or less | |

Business medium sized enterprise | Number of employees | 200 people or less | 100 people or less |

Or capital | 100 billion VND or less | 100 billion VND or less | |

Or revenue | 200 billion VND or less | 300 billion VND or less |

Maybe you are interested!

-

Theoretical and Practical Basis of Applying Accounting Standards in Small and Medium Enterprises

Theoretical and Practical Basis of Applying Accounting Standards in Small and Medium Enterprises -

Factors affecting the application of management accounting in small and medium enterprises in Vietnam - 4

Factors affecting the application of management accounting in small and medium enterprises in Vietnam - 4 -

Conclusions Regarding Factors Affecting the Application of Accounting Standards at Small and Medium Enterprises in Gia Lai Province

Conclusions Regarding Factors Affecting the Application of Accounting Standards at Small and Medium Enterprises in Gia Lai Province -

Problems and Limitations of Cost Management Accounting in Small and Medium-sized Commercial Enterprises in Vietnam

Problems and Limitations of Cost Management Accounting in Small and Medium-sized Commercial Enterprises in Vietnam -

Research on the application of accounting standards - the case of small and medium enterprises in Gia Lai province - 21

Research on the application of accounting standards - the case of small and medium enterprises in Gia Lai province - 21

![The Influence of Culture on Accounting (Source: Gray [95])](https://tailieuthamkhao.com/en/uploads/2025/01/12/the-influence-of-culture-on-accounting-source-gray-95-445x306.jpg)

Source: Decree No. 39/2018 – ND/CP

Although quantitative criteria differ between countries and regions around the world, considering the correlation with the business environment of economies, SMEs have the following characteristics that influence the issuance of accounting regulations:

Firstly , SMEs are usually closed enterprises (Non-public). Securities or financial instruments issued by these enterprises are often not widely traded in the market. The users of accounting information of SMEs focus on owners, current and potential creditors. Therefore, the legal obligation to disclose financial information of these enterprises has certain limitations and is simpler than that of large-scale public enterprises.

Second , the business activities of small and medium enterprises often focus on the main business lines. The economic activities arising in these enterprises are often basic activities related to the main production and business activities. Complicated economic and financial relations rarely occur. Therefore, the accounting work of these enterprises mainly focuses on the basic issues in the production and business process.

Third , due to limited resources and requirements for accounting work, investment in equipment and human resources for accounting work in small and medium enterprises is limited.

From a qualitative point of view, the standard for classifying SMEs is based on a number of criteria, such as: the separation between management and production functions in an organization; characteristics of the market (local, regional, national); or characteristics of technology and equipment used. Although there are many different views, the above methods of classifying enterprises have pointed out some characteristics of SMEs in the following aspects.

Narrow market and simple organizational structure . Small scale (capital, labor) is the origin of this characteristic. SMEs are often opened to meet the demand for goods and services of a community in a region. Therefore, the operating market of this type of enterprise is small, the products and services of the enterprises are not as diverse as large-scale enterprises. This characteristic makes the management structure of SMEs very simple, not divided into many levels like large enterprises, and does not have many units.

members, or not reaching out to localities at home and abroad.

Less complicated in economic transactions . With the characteristics of a narrow operating market and small capital, economic transactions in SMEs are also simpler. Of course, this issue also depends on the economic development characteristics of each country. Most SMEs in Europe operate in the service sector, based on knowledge and little use of tangible assets, but in the ASEAN region, they are basically commercial and production activities. At the basic level, economic transactions focus mainly on production activities or providing and selling goods and services to the outside. Due to capital limitations, external investment activities have certain limitations compared to large enterprises. The management ability to participate in specific commodity markets and participate in risk prevention activities is also limited compared to large-scale enterprises.

High business risk . Normally, SMEs operate in a narrow market with highly specialized services and goods, and limited worker skills, so investing in machinery and equipment and improving competitiveness is extremely difficult. Therefore, the ability to negotiate with suppliers of goods and services is also weaker than that of large enterprises. As a result, revenue and input prices are volatile, causing business profits to often change according to market conditions.

Management skills . Management experience is considered one of the most important factors affecting the success or failure of an organization. Normally, managers in SMEs lack leadership skills, management experience and operational operations. Small business owners are often experts in many areas of business operations, so they cannot operate the business effectively.

Flexibility in management . Due to the impact of management skills, SMEs have high flexibility in the decision-making process. Specifically, there are few internal rules and procedures and few barriers when changing jobs or implementing a new strategy. Communication between owners and employees when performing business tasks is more convenient, with fewer barriers than in large-scale enterprises. SMEs have relative freedom when entering and exiting.

from a market. The relative flexibility of SMEs allows them to adapt quickly to environmental changes.

Poor access to capital. Normally, SMEs start their business with personal savings or loans from friends, so their financial resources are limited. Regarding this issue, Dr. Cao Si Kiem - Chairman of the Association of SMEs [14] assessed that "SMEs with charter capital under 1 billion VND account for 42%, from 1-5 billion VND account for 37%, from 5-10 billion VND account for 8% and the remaining is over 10 billion VND. The majority of enterprises mobilize their own capital from sources for production and business, of which only about 20% of SMEs access loans from commercial banks and financial institutions". Due to their small scale and risky nature, SMEs often face many difficulties in accessing credit from commercial banks or other financial institutions, which often require collateral. In addition, poor accounting systems in SMEs also affect the behavior of commercial banks when providing credit. The reporting system is limited, not really transparent and complete. Legal documents, financial documents do not really meet the requirements of standards, lack of assets to secure loans when borrowing short-term capital. Therefore, the debts of SMEs often have high capital costs, or lack of capital to finance new business opportunities.

The level of workers . Due to the small scale, narrow market, less complex technology, and streamlined management and control procedures, this also affects the level of workers and their ability to improve their learning in their work. The level of workers is assessed lower not only in direct production work but also in operations and management.

Thus, the above characteristics of SMEs have significantly affected the way of managing enterprises, not only from the perspective of the owner and manager but also from the perspective of macro management and the control of other organizations. In terms of accounting, it raises many questions about how to organize accounting and how to apply accounting regulations to suit the characteristics of the enterprise. In terms of state management, what must be the requirements for information disclosure to satisfy the appropriate needs of users of accounting information, while taking into account the ability of SMEs to implement legal regulations on accounting. These issues are always

considered in each historical period and development conditions of each country.

1.3.2. Information needs of small and medium enterprises

Due to the characteristics of SMEs, accounting work in this type of enterprise also has many differences from that of large enterprises. In SMEs, the target audience for information is quite narrow compared to large enterprises. The need for information of SMEs is focused on the enterprise itself and on some subjects interested in the enterprise's activities such as credit institutions and tax authorities. However, due to the variety of scales, it is necessary to have different sets of financial statements depending on the enterprise's scale [165]. The survey results of Dang Duc Son [17] [18] and colleagues show that external subjects are concerned about the truthfulness of information provided by SMEs. In addition, information on cash flow as well as forecasting information is also considered quite important, but this information is not provided or is provided in a sketchy manner. Tran Thi Thanh Hai [41] after conducting a survey with two groups of subjects, information providers and information users, confirmed that accounting information provided by SMEs is used for decision making by business managers.

However, SMEs prepare financial statements based on accounting standards for large enterprises. Based on the view that SMEs are not miniature versions of large enterprises [157], studies agree that this point of view causes certain burdens for SMEs and does not ensure the usefulness of accounting information. Thus, it can be seen that SMEs' application of accounting standards for large enterprises is still a matter of concern when users of financial statements are not provided with information according to their needs and it is necessary to issue a set of accounting standards for SMEs to keep up with the trend of modern economic development that needs to be paid attention to by relevant agencies.

1.4. Overview of studies related to the application of accounting standards in small and medium enterprises

1.4.1. Overview of research in the world

Applying accounting standards is a broad concept, so there are many branches of research on applying accounting standards in practice, which are summarized through branches such as: the branch of research on the disclosure of accounting information according to the requirements of standards.