55

2.4.2. Data processing and analysis results

The topic uses DEAP 2.1 software by author Tim Coelli to estimate cost efficiency and allocative efficiency. This software is concise, easy to understand, and is a powerful processing tool.

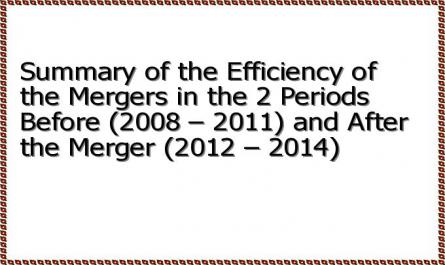

After selecting input and output variables for 5 commercial bank samples in the period 2008-2011 and 4 samples in the period 2012-2014, according to the theoretical basis of the DEA method, through processing by DEAP 2.1 software, the results are as shown in table 2.10:

Table 2.10.: Summary of the efficiency of banks in the two periods before (2008 - 2011) and after the merger (2012 - 2014)

Pre-merge | Post-merge | |||||

TE(CRS) | PE (VRS) | SE(VRS) | TE(CRS) | PE (VRS) | SE(VRS) | |

SHB | 79.30 | 98.50 | 80.50 | 100.00 | 100.00 | 100.00 |

HBB | 67.60 | 100.00 | 67.60 | |||

VPB | 100.00 | 100.00 | 100.00 | 94.30 | 100.00 | 94.30 |

ABB | 100.00 | 100.00 | 100.00 | 89.50 | 100.00 | 89.50 |

NCB | 36.20 | 50.00 | 72.40 | 100.00 | 100.00 | 100.00 |

Average | 76.62 | 89.70 | 84.10 | 95.95 | 100.00 | 95.95 |

Maybe you are interested!

-

Improving business efficiency of Vietnam Technological and Commercial Joint Stock Bank - 2

Improving business efficiency of Vietnam Technological and Commercial Joint Stock Bank - 2 -

Solutions to Improve Business Efficiency of Vietnam Technological and Commercial Joint Stock Bank

Solutions to Improve Business Efficiency of Vietnam Technological and Commercial Joint Stock Bank -

Building a Model of Indicators Affecting the Business Efficiency of the Military Commercial Joint Stock Bank.

Building a Model of Indicators Affecting the Business Efficiency of the Military Commercial Joint Stock Bank. -

Improving the efficiency of consumer lending activities at Southeast Asia Commercial Joint Stock Bank - 9

Improving the efficiency of consumer lending activities at Southeast Asia Commercial Joint Stock Bank - 9 -

Improving the efficiency of international payment activities by credit method at Vietnam Joint Stock Commercial Bank for Investment and Development - Thanh Do Branch - 11

Improving the efficiency of international payment activities by credit method at Vietnam Joint Stock Commercial Bank for Investment and Development - Thanh Do Branch - 11

Source: Author's compilation The overall efficiency estimates presented by pure technical efficiency analysis and economies of scale using DEA model are shown in the table.

2.10. We see that during the pre-merger period (2008-2011), the banks in the group had an average overall efficiency of 76.62%, and the efficiency improved in the post-merger period. The inefficiency of the banks in the pre-merger period was largely attributed to scale efficiency rather than pure technical efficiency. The average overall efficiency of SHB in the pre-merger period was quite good compared to the banks in the same group. The bank operated with an average input loss (interest expense x 1 and non-interest expense x 2 ) of 20.7%, meaning that SHB could reduce input by 20.7% to produce the same amount of output (interest income y 1 and non-interest income y 2 ).

56

The results also show that, in the pre-merger period, SHB's inefficiency was mainly due to scale.

Also according to the results from Table 2.10, after the merger, SHB's overall efficiency has been completely improved (100%) thanks to the increased efficiency due to scale. However, it should be noted that SHB only achieved overall efficiency compared to banks in the same group, and these banks did not carry out merger activities. At the time of 2012, SHB and HBB were both in this group 6 . However, after 2012, commercial banks such as ABB and NCB had lower ratings than SHB.

6 According to the ranking in the "Vietnam Credit Index Annual Report 2012" of the Vietnam Chamber of Commerce and Industry (VCCI)

57

CONCLUSION OF CHAPTER 2

Based on the theoretical basis of business performance presented in chapter 1, the thesis applied the CAMEL model, combined with the DEA model to evaluate the current status of SHB's business performance in the two periods before and after the merger, focusing on changes in business performance after M&A. From there, the thesis gives some comments and assessments of an orientational nature. According to the analysis results of the CAMEL model, it can be seen that restructuring a weak bank like HBB by merging into a bank with strong financial potential like SHB has helped to quickly restore and improve asset quality. After the merger, although there were some difficulties to resolve due to the financial exhaustion left by HBB, SHB is still showing itself to be a bank with a healthy financial situation and good development prospects, as shown through the indicators of operational safety, liquidity safety, and stable credit growth rate over time. The results of the DEA model also show that the merger has helped to completely improve the pure technical efficiency as well as the scale efficiency of SHB compared to banks with the same competitive ability at the time of the merger (2012).

Thus, the initial successes of this case are a sign of the success of the SBV's strategy of restructuring weak credit institutions. However, CAMEL analysis shows that SHB needs to improve its business performance, especially its profitability to match its scale of equity and total assets. This is still a challenge for SHB, as shown by the figures on profitability that are still not very positive after nearly 3 years of merger. In the period of increasingly fierce competition in the banking industry and the SBV's regulations on the business activities of commercial banks becoming more stringent, SHB needs to focus on implementing a number of solutions to improve the efficiency of its business activities in order to take full advantage of the strengths that this M&A deal brings. This is also the content presented in Chapter 3.

58

CHAPTER 3. SOLUTIONS TO IMPROVE SHB'S BUSINESS EFFICIENCY AFTER THE MERGER

3.1. Changes in the macroeconomic and industry environment affecting SHB's business operations

To effectively implement the strategic planning to improve business performance, SHB needs to closely follow the content of some important policy changes that have been affecting the banking business sector, as well as the context of the macroeconomic environment in the coming years.

3.1.1. Forecast of the economic situation in the period 2016 - 2020 affecting the banking industry At the end of 2014, our country had a fairly good growth rate (5.98%) along with low inflation (1.84%). This is an opportunity for the Government to implement macroeconomic management policies focusing on economic restructuring - a basic condition for the economy to recover in the long term. In particular, the Government focuses on restructuring and handling bad debt .

At the conference on implementing banking tasks in 2015, Governor of the State Bank of Vietnam Nguyen Van Binh said that, looking at the forecast indicators of the domestic and international economy (such as exports), 2015 is a year of many challenges for the banking sector. This is also the final year in the process of restructuring credit institutions in the period 2011 - 2015. Therefore, the sector focuses on restructuring credit institutions and handling bad debts, and affirms that in general, the monetary policy will be stable, but monetary policy tools will be used more flexibly. To achieve this goal, the State Bank of Vietnam will closely monitor market developments to operate appropriate tools in line with a series of policies such as: maintaining low interest rates; exchange rate fluctuations not exceeding 2%; credit growth target of 13 -15%; bringing the bad debt ratio to 3%...

In fact, after more than 2 years of implementing the Project on restructuring credit institutions, the risk of system collapse has been prevented, the safety of the system has been ensured; bad debts of the system have been clearly identified and there have been initial positive changes in the implementation of handling; the restructuring has been carried out synchronously and drastically with

59

appropriate solutions based on maximizing private resources and minimizing state resources. The State Bank will comply with legal regulations to thoroughly handle weak banks, and major credit institutions will participate in this process. The stable trend of inflation is forecast to continue in 2015. According to experts, the CPI in 2015 may fluctuate between 2 - 3%. This inflation rate is predicted to last for several years, and may remain stable throughout the 2016 - 2020 period.

Thus, with the macroeconomic and industry outlook in the coming time, SHB needs to closely follow the government's orientations and planned growth targets to clearly perceive its role, take advantage of advantages, and adjust its business strategy accordingly.

3.1.2. Changes in the industry affecting business operations in the coming period

3.1.2.1. The banking industry is actively restructuring.

2015 is the year when the banking industry accelerates the restructuring process because the Vietnamese banking system has overcome the most difficult period, the macro-economic situation has many positive changes, production and business activities have recovered clearly. In the first months of 2015, Vietnamese commercial banks held the 2015 annual general meeting of shareholders to evaluate the performance of 2014, orient and develop business plans for the coming time.

At this congress, a number of small commercial banks focused on discussing restructuring measures in the direction of finding strategic partners to increase capital, through the plan of merging with other banks to become a larger commercial bank, both in terms of finance, network, and at the same time improving the bank's management capacity. At the shareholders' meeting held on April 20, 2015, the Board of Directors of Nam A Bank presented a plan to merge with Sacombank. In the operational orientation for the period 2015-2020, National Citizen Bank (NCB) plans to merge with another commercial bank,...

Previously, the State Bank of Vietnam issued Official Dispatch No. 1607/NHNN-TTGSNH dated March 18, 2015 approving in principle the merger plan of Mekong Development Joint Stock Commercial Bank.

60

(MDB) into Maritime Commercial Joint Stock Bank (MSB), the basic goal is to help MDB improve asset quality and minimize future risks. Along with the group of small banks, the merger wave is also positively responded by large commercial banks. At the shareholders' meeting held on April 14, 2015, the leaders of the Vietnam Joint Stock Commercial Bank for Industry and Trade officially asked for shareholders' opinions on the merger plan with the Global Petroleum Bank.

2015 is also a good time for the banking sector to accelerate the restructuring process because the Vietnamese banking system has overcome the most difficult period, the macro-economic situation has many positive changes with GDP in the first quarter of 2015 increasing by 6.03% compared to the same period last year and inflation being controlled at a low level, production and business activities have recovered clearly. In particular, the recovery of the real estate market is an important factor helping banks recover outstanding debts, contributing to quickly reducing bad debts to a safe threshold and expanding credit to support economic growth.

After a period of preparation for the necessary initial steps in the restructuring process, the liquidity of Vietnamese credit institutions has improved significantly, the bad debt ratio has decreased sharply, and the banking system has gradually stabilized. The efforts of commercial banks have also received active support from the State Bank, especially in handling bad debts and improving the legal environment to develop the Vietnamese banking system in a more sustainable direction.

3.1.2.2. Implementing Circular 36 - many business objectives must change On November 20, 2014, the State Bank of Vietnam (SBV) issued Circular 36/2014/TT-NHNN regulating limits and safety ratios in the operations of credit institutions and foreign bank branches. This is a legal document that creates a new framework for comprehensive regulation of limits, restrictions, and safety ratios in banking operations. Circular 36 took effect from February 1, 2015, issued to guide the provisions of the Law on Credit Institutions 2010, specifically regulating: (i) Minimum capital safety ratio; (ii) Credit limits and restrictions; (iii) Solvency ratio; (iv) Maximum ratio of short-term capital sources used

61

(v) Limits on capital contribution and share purchase; (vi) Ratio of outstanding loans to total deposits.

Circular 36 has replaced a series of documents previously issued by the State Bank, specifically including: (i) Decision 03/2008/QD-NHNN dated February 1, 2008 of the State Bank on lending and discounting valuable papers for investment and securities trading; (ii) Circular 15/2009/TT-NHNN dated August 10, 2009 of the State Bank promulgating Regulations on the maximum ratio of short-term capital sources used for medium-term and long-term loans; (iii) Circular 13/2010/TT-NHNN dated May 20, 2010 of the State Bank promulgating Regulations on safety ratios in the operations of credit institutions; (iv) Circular 19/2010/TT-NHNN dated September 27, 2010 of the State Bank amending and supplementing a number of articles of Circular 13/2010/TT-NHNN; (v) Circular 22/2011/TT-NHNN dated August 30, 2011 of the State Bank amending and supplementing a number of articles of Circular 13/2010/TT-NHNN; (vi) Article 1 of Circular 33/2011/TT-NHNN dated October 8, 2011 and Clause 2, Article 6 of Circular 28/2012/TT-NHNN dated October 3, 2012 of the State Bank on bank guarantees.

Some impacts of Circular 36 on business activities that commercial banks need to note:

The regulation of CAR ratio at 9% (as per old regulation) while reducing the risk weight for securities lending and real estate lending from 250% to 150% will basically have a positive impact on the market. Credit institutions, especially those with medium and small capital scale, can expand credit activities for real estate, thereby better supporting the recovery of the real estate market, creating liquidity as well as supporting economic recovery and growth.

In addition, changing the structure of determining equity capital, including adding general provisions to the capital calculation component, also contributes to expanding the money creation capacity of commercial banks.

The regulation of some limits and safety ratios in Circular 36 with reference to international standards under Basel II and Basel III Agreements shows that the State Bank has gradually adjusted the operations of the money and banking market towards international integration.

62

At the same time, it enhances the stability and sustainability of the Vietnamese credit institution system, thereby enhancing the competitiveness of credit institutions. However, in the current context, the application of international standards to the practical operations of the Vietnamese banking system may encounter the following difficulties and obstacles:

Firstly, the response of the information technology system, statistics, monitoring, cash flow management, monitoring of limits, and short-term safety ratios can hardly be automated. The reason is that the system, the method of measuring indicators and many data classification criteria for calculating the capital adequacy level of Circular 36 are different from the old regulations. Therefore, controlling indicators and limits to ensure accuracy and compliance with new regulations is very difficult when it has to be done manually. Secondly, to ensure compliance with stricter new standards such as narrowed credit limits (credit balance plus corporate bond balance), government bond investment limits, payment capacity ratios, short-term capital ratio for medium and long-term loans, etc., banks will have to restructure the entire asset and liability portfolio to both comply with regulations and optimize the portfolio's profitability. Portfolio restructuring may impact established business objectives and business strategies.

Third, the new regulations of Circular 36 may lead to changes and additions to the organizational structure and management apparatus that have been established and approved by the bank. Circular 36 has a major impact on all credit institutions, introducing a number of new regulations such as the ratio of payment capacity, the ratio of loans/mobilized capital, the ratio of government bond investment/short-term capital sources; changing the method of determining equity capital, expanding the scope of calculating credit balance when calculating safety limits, adding regulations on calculating medium and long-term debt including short-term overdue debt; stricter regulations on risk management requirements, the system of policies and procedures for governance, credit management, etc.

Circular 36 was issued at the end of 2014 and took effect from February 1, 2015, which will significantly affect the business plans of commercial banks. Many business and credit management goals will have to be changed and adjusted accordingly.