Variable

N | Range | Minimum | Maximum | Sum | Mean | Std. Deviation | Variance | |

B16 | 100 | 2 | 1 | 3 | 263 | 2.63 | 0.661 | 0.437 |

B17 | 100 | 2 | 2 | 4 | 302 | 3.02 | 0.402 | 0.161 |

B18 | 100 | 2 | 3 | 5 | 391 | 3.91 | 0.473 | 0.224 |

B19 | 100 | 1 | 3 | 4 | 369 | 3.69 | 0.465 | 0.216 |

B20 | 100 | 1 | 4 | 5 | 427 | 4.27 | 0.446 | 0.199 |

B21 | 100 | 1 | 4 | 5 | 475 | 4.75 | 0.435 | 0.189 |

B22 | 100 | 2 | 3 | 5 | 406 | 4.06 | 0.422 | 0.178 |

B23 | 100 | 2 | 3 | 5 | 409 | 4.09 | 0.452 | 0.204 |

KN | 100 | 3 | 2 | 5 | 390 | 3.90 | 0.644 | 0.414 |

Valid N (listwise) 100 | ||||||||

Maybe you are interested!

-

Solutions for tourism development in Tien Lang - 10

zt2i3t4l5ee

zt2a3gstourism, tourism development

zt2a3ge

zc2o3n4t5e6n7ts

- District People's Committees and authorities of communes with tourist attractions should support, promote, and provide necessary information to people, helping them improve their knowledge about tourism. Raise tourism awareness for local people.

*

* *

Due to limited knowledge and research time, the thesis inevitably has shortcomings. Therefore, I look forward to receiving guidance from teachers, experts as well as your comments to make the thesis more complete.

Chapter III Conclusion

Through the issues presented in Chapter II, we can come to some conclusions:

Based on the strengths of available tourism resources, the types of tourism in Tien Lang that need to be promoted in the coming time are sightseeing and resort tourism, discovery tourism, weekend tourism. To improve the quality and diversify tourism products, Tien Lang district needs to combine with local cultural tourism resources, at the same time combine with surrounding areas, build rich tourism products. The strengths of Tien Lang tourism are eco-tourism and cultural tourism, so developing Tien Lang tourism must always go hand in hand with restoring and preserving types of cultural tourism resources. Some necessary measures to support and improve the efficiency of exploiting tourism resources in Tien Lang are: strengthening the construction of technical facilities and labor force serving tourism, actively promoting and advertising tourism, and expanding forms of capital mobilization for tourism development.

CONCLUDE

I Conclusion

1. Based on the results achieved within the framework of the thesis's needs, some basic conclusions can be drawn as follows:

Tien Lang is a locality with great potential for tourism development. The relatively abundant cultural tourism resources and ecological tourism resources have great appeal to tourists. Based on this potential, Tien Lang can build a unique tourism industry that is competitive enough with other localities within Hai Phong city and neighboring areas.

In recent years, the exploitation of the advantages of resources to develop tourism and build tourist routes in Tien Lang has not been commensurate with the available potential. In terms of quantity, many resource objects have not been brought into the purpose of tourism development. In terms of time, the regular service time has not been extended to attract more visitors. Infrastructure and technical facilities are still weak. The labor force is still thin and weak in terms of expertise. Tourism programs and routes have not been organized properly, the exploitation content is still monotonous, so it has not attracted many visitors. Although resources have not been mobilized much for tourism development, they are facing the risk of destruction and degradation.

2. Based on the results of investigation, analysis, synthesis, evaluation and selective absorption of research results of related topics, the thesis has proposed a number of necessary solutions to improve the efficiency of exploiting tourism resources in Tien Lang such as: promoting the restoration and conservation of tourism resources, focusing on investment and key exploitation of ecotourism resources, strengthening the construction of infrastructure and tourism workforce. Expanding forms of capital mobilization. In addition, the thesis has built a number of tourist routes of Hai Phong in which Tien Lang tourism resources play an important role.

Exploiting Tien Lang tourism resources for tourism development is currently facing many difficulties. The above measures, if applied synchronously, will likely bring new prospects for the local tourism industry, contributing to making Tien Lang tourism an important economic sector in the district's economic structure.

REFERENCES

1. Nhuan Ha, Trinh Minh Hien, Tran Phuong, Hai Phong - Historical and cultural relics, Hai Phong Publishing House, 1993

2. Hai Phong City History Council, Hai Phong Gazetteer, Hai Phong Publishing House, 1990.

3. Hai Phong City History Council, History of Tien Lang District Party Committee, Hai Phong Publishing House, 1990.

4. Hai Phong City History Council, University of Social Sciences and Humanities, VNU, Hai Phong Place Names Encyclopedia, Hai Phong Publishing House. 2001.

5. Law on Cultural Heritage and documents guiding its implementation, National Political Publishing House, Hanoi, 2003.

6. Tran Duc Thanh, Lecture on Tourism Geography, Faculty of Tourism, University of Social Sciences and Humanities, VNU, 2006

7. Hai Phong Center for Social Sciences and Humanities, Some typical cultural heritages of Hai Phong, Hai Phong Publishing House, 2001

8. Nguyen Ngoc Thao (editor-in-chief, Tourism Geography, Hai Phong Publishing House, two volumes (2001-2002)

9. Nguyen Minh Tue and group of authors, Hai Phong Tourism Geography, Ho Chi Minh City Publishing House, 1997.

10. Nguyen Thanh Son, Hai Phong Tourism Territory Organization, Associate Doctoral Thesis in Geological Geography, Hanoi, 1996.

11. Decision No. 2033/QD – UB on detailed planning of Tien Lang town, Hai Phong city until 2020.

12. Department of Culture, Information, Hai Phong Museum, Hai Phong relics

- National ranked scenic spot, Hai Phong Publishing House, 2005. 13. Tien Lang District People's Committee, Economic Development Planning -

Culture - Society of Tien Lang district to 2010.

14.Website www.HaiPhong.gov.vn

APPENDIX 1

List of national ranked monuments

STT

Name of the monument

Number, year of decisiondetermine

Location

1

Gam Temple

938 VH/QĐ04/08/1992

Cam Khe Village- Toan Thang commune

2

Doc Hau Temple

9381 VH/QĐ04/08/1992

Doc Hau Village –Toan Thang commune

3

Cuu Doi Communal House

3207 VH/QĐDecember 30, 1991

Zone II of townTien Lang

4

Ha Dai Temple

938 VH/QĐ04/08/1992

Ha Dai Village –Tien Thanh commune

APPENDIX II

STT

Name of the monument

Number, year of decision

Location

1

Phu Ke Pagoda Temple

178/QD-UBJanuary 28, 2005

Zone 1 - townTien Lang

2

Trung Lang Temple

178/QD-UBJanuary 28, 2005

Zone 4 – townTien Lang

3

Bao Khanh Pagoda

1900/QD-UBAugust 24, 2006

Nam Tu Village -Kien Thiet commune

4

Bach Da Pagoda

1792/QD-UB11/11/2002

Hung Thang Commune

5

Ngoc Dong Temple

177/QD-UBNovember 27, 2005

Tien Thanh Commune

6

Tomb of Minister TSNhu Van Lan

2848/QD-UBSeptember 19, 2003

Nam Tu Village -Kien Thiet commune

7

Canh Son Stone Temple

2160/QD-UBSeptember 19, 2003

Van Doi Commune –Doan Lap

8

Meiji Temple

2259/QD-UBSeptember 19, 2002

Toan Thang Commune

9

Tien Doi Noi Temple

477/QD-UBSeptember 19, 2005

Doan Lap Commune

10

Tu Doi Temple

177/QD-UBJanuary 28, 2005

Doan Lap Commune

11

Duyen Lao Temple

177/QD-UBJanuary 28, 2005

Tien Minh Commune

12

Dinh Xuan Uc Pagoda

177/QD-UBJanuary 28, 2005

Bac Hung Commune

13

Chu Khe Pagoda

177/QD-UBJanuary 28, 2005

Hung Thang Commune

14

Dong Dinh

2848/QD-UBNovember 21, 2002

Vinh Quang Commune

15

President's Memorial HouseTon Duc Thang

177/QD-UBJanuary 28, 2005

NT Quy Cao

Ha Dai Temple

Ben Vua Temple

Tien Lang hot spring

div.maincontent .p { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; } div.maincontent p { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; } div.maincontent .s1 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; font-size: 16pt; } div.maincontent .s2 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s3 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s4 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; font-size: 14pt; } div.maincontent .s5 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; font-size: 14pt; } div.maincontent .s6 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s7 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s8 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; vertical-align: 6pt; } div.maincontent .s9 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 12pt; } div.maincontent .s11 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; tex

Solutions for tourism development in Tien Lang - 10

zt2i3t4l5ee

zt2a3gstourism, tourism development

zt2a3ge

zc2o3n4t5e6n7ts

- District People's Committees and authorities of communes with tourist attractions should support, promote, and provide necessary information to people, helping them improve their knowledge about tourism. Raise tourism awareness for local people.

*

* *

Due to limited knowledge and research time, the thesis inevitably has shortcomings. Therefore, I look forward to receiving guidance from teachers, experts as well as your comments to make the thesis more complete.

Chapter III Conclusion

Through the issues presented in Chapter II, we can come to some conclusions:

Based on the strengths of available tourism resources, the types of tourism in Tien Lang that need to be promoted in the coming time are sightseeing and resort tourism, discovery tourism, weekend tourism. To improve the quality and diversify tourism products, Tien Lang district needs to combine with local cultural tourism resources, at the same time combine with surrounding areas, build rich tourism products. The strengths of Tien Lang tourism are eco-tourism and cultural tourism, so developing Tien Lang tourism must always go hand in hand with restoring and preserving types of cultural tourism resources. Some necessary measures to support and improve the efficiency of exploiting tourism resources in Tien Lang are: strengthening the construction of technical facilities and labor force serving tourism, actively promoting and advertising tourism, and expanding forms of capital mobilization for tourism development.

CONCLUDE

I Conclusion

1. Based on the results achieved within the framework of the thesis's needs, some basic conclusions can be drawn as follows:

Tien Lang is a locality with great potential for tourism development. The relatively abundant cultural tourism resources and ecological tourism resources have great appeal to tourists. Based on this potential, Tien Lang can build a unique tourism industry that is competitive enough with other localities within Hai Phong city and neighboring areas.

In recent years, the exploitation of the advantages of resources to develop tourism and build tourist routes in Tien Lang has not been commensurate with the available potential. In terms of quantity, many resource objects have not been brought into the purpose of tourism development. In terms of time, the regular service time has not been extended to attract more visitors. Infrastructure and technical facilities are still weak. The labor force is still thin and weak in terms of expertise. Tourism programs and routes have not been organized properly, the exploitation content is still monotonous, so it has not attracted many visitors. Although resources have not been mobilized much for tourism development, they are facing the risk of destruction and degradation.

2. Based on the results of investigation, analysis, synthesis, evaluation and selective absorption of research results of related topics, the thesis has proposed a number of necessary solutions to improve the efficiency of exploiting tourism resources in Tien Lang such as: promoting the restoration and conservation of tourism resources, focusing on investment and key exploitation of ecotourism resources, strengthening the construction of infrastructure and tourism workforce. Expanding forms of capital mobilization. In addition, the thesis has built a number of tourist routes of Hai Phong in which Tien Lang tourism resources play an important role.

Exploiting Tien Lang tourism resources for tourism development is currently facing many difficulties. The above measures, if applied synchronously, will likely bring new prospects for the local tourism industry, contributing to making Tien Lang tourism an important economic sector in the district's economic structure.

REFERENCES

1. Nhuan Ha, Trinh Minh Hien, Tran Phuong, Hai Phong - Historical and cultural relics, Hai Phong Publishing House, 1993

2. Hai Phong City History Council, Hai Phong Gazetteer, Hai Phong Publishing House, 1990.

3. Hai Phong City History Council, History of Tien Lang District Party Committee, Hai Phong Publishing House, 1990.

4. Hai Phong City History Council, University of Social Sciences and Humanities, VNU, Hai Phong Place Names Encyclopedia, Hai Phong Publishing House. 2001.

5. Law on Cultural Heritage and documents guiding its implementation, National Political Publishing House, Hanoi, 2003.

6. Tran Duc Thanh, Lecture on Tourism Geography, Faculty of Tourism, University of Social Sciences and Humanities, VNU, 2006

7. Hai Phong Center for Social Sciences and Humanities, Some typical cultural heritages of Hai Phong, Hai Phong Publishing House, 2001

8. Nguyen Ngoc Thao (editor-in-chief, Tourism Geography, Hai Phong Publishing House, two volumes (2001-2002)

9. Nguyen Minh Tue and group of authors, Hai Phong Tourism Geography, Ho Chi Minh City Publishing House, 1997.

10. Nguyen Thanh Son, Hai Phong Tourism Territory Organization, Associate Doctoral Thesis in Geological Geography, Hanoi, 1996.

11. Decision No. 2033/QD – UB on detailed planning of Tien Lang town, Hai Phong city until 2020.

12. Department of Culture, Information, Hai Phong Museum, Hai Phong relics

- National ranked scenic spot, Hai Phong Publishing House, 2005. 13. Tien Lang District People's Committee, Economic Development Planning -

Culture - Society of Tien Lang district to 2010.

14.Website www.HaiPhong.gov.vn

APPENDIX 1

List of national ranked monuments

STT

Name of the monument

Number, year of decisiondetermine

Location

1

Gam Temple

938 VH/QĐ04/08/1992

Cam Khe Village- Toan Thang commune

2

Doc Hau Temple

9381 VH/QĐ04/08/1992

Doc Hau Village –Toan Thang commune

3

Cuu Doi Communal House

3207 VH/QĐDecember 30, 1991

Zone II of townTien Lang

4

Ha Dai Temple

938 VH/QĐ04/08/1992

Ha Dai Village –Tien Thanh commune

APPENDIX II

STT

Name of the monument

Number, year of decision

Location

1

Phu Ke Pagoda Temple

178/QD-UBJanuary 28, 2005

Zone 1 - townTien Lang

2

Trung Lang Temple

178/QD-UBJanuary 28, 2005

Zone 4 – townTien Lang

3

Bao Khanh Pagoda

1900/QD-UBAugust 24, 2006

Nam Tu Village -Kien Thiet commune

4

Bach Da Pagoda

1792/QD-UB11/11/2002

Hung Thang Commune

5

Ngoc Dong Temple

177/QD-UBNovember 27, 2005

Tien Thanh Commune

6

Tomb of Minister TSNhu Van Lan

2848/QD-UBSeptember 19, 2003

Nam Tu Village -Kien Thiet commune

7

Canh Son Stone Temple

2160/QD-UBSeptember 19, 2003

Van Doi Commune –Doan Lap

8

Meiji Temple

2259/QD-UBSeptember 19, 2002

Toan Thang Commune

9

Tien Doi Noi Temple

477/QD-UBSeptember 19, 2005

Doan Lap Commune

10

Tu Doi Temple

177/QD-UBJanuary 28, 2005

Doan Lap Commune

11

Duyen Lao Temple

177/QD-UBJanuary 28, 2005

Tien Minh Commune

12

Dinh Xuan Uc Pagoda

177/QD-UBJanuary 28, 2005

Bac Hung Commune

13

Chu Khe Pagoda

177/QD-UBJanuary 28, 2005

Hung Thang Commune

14

Dong Dinh

2848/QD-UBNovember 21, 2002

Vinh Quang Commune

15

President's Memorial HouseTon Duc Thang

177/QD-UBJanuary 28, 2005

NT Quy Cao

Ha Dai Temple

Ben Vua Temple

Tien Lang hot spring

div.maincontent .p { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; } div.maincontent p { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; } div.maincontent .s1 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; font-size: 16pt; } div.maincontent .s2 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s3 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s4 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; font-size: 14pt; } div.maincontent .s5 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; font-size: 14pt; } div.maincontent .s6 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s7 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s8 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; vertical-align: 6pt; } div.maincontent .s9 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 12pt; } div.maincontent .s11 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; tex -

Summary Table of Exploratory Factor Analysis Results Efa

Summary Table of Exploratory Factor Analysis Results Efa -

Summary Table of Results After Inspecting the Management of Staff, Teachers, and Employees of Public Kindergartens, Primary Schools, and Secondary Schools

Summary Table of Results After Inspecting the Management of Staff, Teachers, and Employees of Public Kindergartens, Primary Schools, and Secondary Schools -

Results of Data Analysis of Interviews with Managers and Experts in the Field of Marine Resources and Environment Management in Korea

Results of Data Analysis of Interviews with Managers and Experts in the Field of Marine Resources and Environment Management in Korea -

Analysis of Credit Situation and Credit Risk Management of Vietnam Bank for Agriculture and Rural Development, Vinh Thuan Branch - Kien Giang

Analysis of Credit Situation and Credit Risk Management of Vietnam Bank for Agriculture and Rural Development, Vinh Thuan Branch - Kien Giang

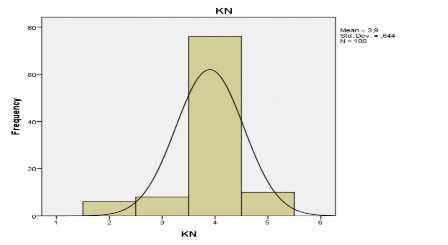

Source: Author's calculation using SPSS 20

Table 2.15 shows that all 24 observed and studied variables are valid and give statistical results on the maximum, minimum, total, mean, deviation, and detailed variance values for each variable;

c. Research results on variables

Figure 2.6 and Table PL11.1 ( see Appendix 11 ) show the detailed research results of the following variables:

- The KN variable's frequency distribution has an average of 3.9 and a deviation of 0.44, and we can conclude that "The possibility of applying the Basel II treaty to the Vietnamese commercial banking system from now until 2020" is quite average.

Source: Author's research results

Figure 2.6: Distribution rule of dependent variable “KN

d. Analyze the relationship between independent and dependent variables

Table PL11.2: Results of testing the scale of aggregate variables ( see details in Appendix 11 ). Shows that the explanatory variables in the author's survey are not meaningful in terms of scale, so they cannot be used in further analysis of the relationships between variables, testing hypotheses and analyzing exploratory factors.

Table PL11.3: Testing the correlation between KN and Bi variables (i = 1÷ 23) ( See details in Appendix 11 ). According to the results, we see that all the values of ig. are greater than the significance level of 0.05 (or 95% confidence level), so we accept the hypothesis Ho: the variable KN and the variables Bi are not correlated with each other.

2.3.2.3. Synthesize analysis results and draw conclusions

Firstly, one of the difficulties affecting the decision to apply Basel II to the risk management and monitoring system of Vietnamese commercial banks is that the operating cost according to the entire Basel II standards is too high. According to estimates, small commercial banks have to spend approximately 10 million USD, equivalent to 10 billion VND, about 5% of the charter capital of joint stock commercial banks. Meanwhile, if it is a large bank, the operating cost of this Basel system can be up to 200 million USD, equivalent to 3,200 billion VND.

Second , information on the stock market and capital market is extremely important if a banking system wants to apply Basel II standards. Meanwhile, in fact, the Vietnamese stock market has been established for just over 11 years, the number of goods on the market has increased significantly compared to the early period, but the transparency issues in information disclosure of listed companies, lax management by authorities, and negative developments in the stock market in recent times have made it difficult for commercial banks to receive information processing support from the stock market to apply to their risk management work.

Other macroeconomic and microeconomic information is still a difficult problem not only for the banking system. The issue of information disclosure has been greatly improved recently through mass media, newspapers, radio, internet, on some official websites of ministries and branches such as the Ministry of Finance, the State Bank of Vietnam, the electronic transaction portals of the Government.

government, city and provincial authorities. However, these reports are usually prepared in the form of annual reports, and have a relatively large delay compared to the time of the events, making it difficult to support banks in forecasting, assessing and preventing risks. Specialized statistical information to create a database for banks is currently very limited, apart from the credit information center CIC, there is almost no organization capable of collecting and providing information.

Third, unlike the “one-size-fits-all” approach to capital standards in Basel I, Basel II relies on a variety of factors to determine the risk weight for each asset class relative to different groups of entities, one of which is the credit rating of an independent agency. As analyzed in chapter 2, most of the risk coefficients of asset groups from deposits to investments or loans are affected by credit ratings, for example, receivables at a commercial bank rated AAA+ have a risk coefficient of only 20% while receivables at a commercial bank but if that bank is rated B-, the risk coefficient can be up to 100% or 150%, including investments in bonds of countries with higher ratings will also have a lower risk coefficient than investments in bonds of countries with average or poor ratings.

Currently, the reality is that each Vietnamese commercial bank is gradually building a credit rating system for each customer group. However, this rating is mainly to serve the appraisal process and make lending decisions of the bank, very little information is shared or widely disseminated outside, which leads to each bank taking care of itself and as a result, sometimes the assessment is more subjective and emotional than objective. In addition, it also leads to inaccurate conclusions simply because of incomplete information.

Fourth, the Standardization Methodology proposed in the Treaty overemphasizes the role of rating agencies in classifying asset risks, while experience shows that large companies in the credit rating industry have a relatively large number of inaccurate ratings.

Fifth, in addition, in many countries around the world, especially in Vietnam, most businesses are not rated. This leads to disadvantages for Vietnamese banks because all unrated customer loans will be subject to

The risk level is 100%. Furthermore, Basel II's assumption that unrated companies are less risky than rated companies is not entirely accurate.

Another problem is that most businesses in developing countries are not rated, which can lead to a situation where rating companies will conduct business rating without the request of the business. In that case, the rating provided by these companies will be inaccurate due to incomplete information about the business, which will be disadvantageous to the business. On the other hand, there are many problems in the method of assessing operational risks, such as the overly complicated self-assessment method of banks, the standardized method with basic indicators not closely linked to risks, and the aggregation of credit risk with operational risk.

Sixth, the Basel II Accord gives the banking regulatory authority the right to consider the applicability of each type of risk assessment system to classify the asset risks of credit institutions. In fact, if the central bank - the agency that manages and supervises banking activities - is not qualified to verify whether the risk assessment system of credit institutions is appropriate or not, it will be very dangerous for the operation of the entire banking system. For example, when using the internal risk assessment system, many credit institutions may be too optimistic about their customers' prospects and do not have appropriate countermeasures and prevention measures, leading to the possibility of customer defaults that can lead to the default of the bank in particular and the entire banking system in general. In the current conditions, whether the State Bank wants it or not, it cannot let commercial banks freely choose their own risk assessment methods, but must strictly manage each regulation of the State Bank, which is reflected in a series of regulations on safety ratios in the operations of credit institutions in Vietnam. Once the State Bank succeeds in improving its supervision level as well as successfully implementing the restructuring process of commercial banks, equipping banks with certain knowledge and skills in the field of risk management, then it can move towards the possibility of applying more modern methods.

Seventh, One of the difficulties when considering the application of Basel II to risk management at Vietnamese commercial banks is the lack of high-quality human resources. This is a common problem for all commercial banks and even for commercial bank supervisory agencies such as

State Bank. Through studying the Basel II standards in Chapter I, it can be seen that in order to master and apply these standards, experts in the field of banking management and supervision and staff in charge must have a certain level of understanding, be good at foreign languages, have mathematical knowledge and management knowledge. In addition, analytical and forecasting skills are also indispensable skills. These are really high requirements for Vietnamese banking experts at this time. Currently, Vietnamese commercial banks are competing fiercely to retain good experts who are knowledgeable in the banking sector through preferential salary, bonuses and other forms such as stock rewards, housing and transportation equipment, etc. However, with the current strong growth rate of the banking system, the number of good experts is still not enough and requires a great deal of training and supplementation. In addition, there are also many good experts who are holding senior positions in commercial banks, but due to lack of conditions or insufficient time to be trained and access this new knowledge, they are not able to apply it to practical work. The cost of courses with foreign experts in the field of finance and banking is usually very high, requiring a lot of time and effort from those who attend the course.

Eighth, Vietnamese commercial banks are confused in implementing Vietnamese accounting standards and international accounting standards. When reporting according to these two standards or hiring domestic and foreign independent credit rating organizations to evaluate, the results are very different.

Ninth, Normally, when banks analyze their operations over a period of time, they will use data on the balance sheet and other financial statements. However, there is an issue of concern here: how should the value of items on the balance sheet be expressed in order to take into account factors that fluctuate in the market affecting the book value of these items, including fluctuations in interest rates, exchange rates, fluctuations in the prices of securities and derivative products according to the remaining maturity period, etc. That is the matter of taking into account market risks in the book value of commercial banks. According to the published balance sheets of a number of commercial banks, including joint-stock commercial banks and state-owned commercial banks, it can be seen that most banks have not taken into account market risks in the value of investments on the books of commercial banks.

CONCLUSION OF CHAPTER 2

Based on the theoretical system in chapter 1, the author has embarked on a study of the current status of Basel II application in Vietnam, the current status of risk management and awareness of Basel II, specifically as follows:

The author described and analyzed the characteristics of Vietnam's economy and analyzed the effects of those characteristics on the commercial banking system and risk management.

Next, the author described and analyzed the entire Vietnamese commercial banking system through a study of the 14 largest commercial banks (G14) in terms of charter capital, mobilization activities, lending activities, investment activities, and bad debt developments. At the same time, the author also analyzed and pointed out the types of risks that are occurring in the current commercial banking system.

Finally, the author analyzed the current status of Basel II application in the Vietnamese commercial banking system, including: the legal document system, the Capital Adequacy Ratio (CAR), the credit rating system, and the information system. To clarify the issues, the author conducted a survey of bank officials' awareness of Basel II and the possibility of applying Basel II. Detailed conclusions are presented in section 2.3.2.3.

In summary, these research results are sufficient conditions for proposing solutions to apply Basel II to the Vietnamese commercial banking system in the period from now to 2020.

CHAPTER 3: SOLUTIONS TO APPLY THE BASEL II AGREEMENT TO THE RISK MANAGEMENT SYSTEM AT THE

VIETNAM COMMERCIAL BANK

3.1. Development orientation of Vietnam's commercial banking system in the period 2015 - 2020

After Vietnam joined the World Trade Organization (WTO) and implemented the roadmap of commitments to open the financial market, banking activities have undergone profound changes in both quantity and quality: the number of branches, capital scale, securities-banking, insurance-banking transactions, and international transactions have increased. These changes have brought both positive impacts and many risks and require banks themselves to effectively manage risks.

The author proposes a number of orientations to determine the overall development direction of the financial and banking system, focusing on the main contents:

3.1.1. General development orientation

Firstly , reorganize the State Bank (SBV) with the structure and nature of operations as a modern Central Bank, increasingly operating under a full market mechanism, being given more independence and autonomy in making policy decisions, and the right to take initiative in budget matters; at the same time, being given the right to control all tools that affect the goals of monetary policy, especially in the fight against inflation, limiting direct financing of the Government's budget deficit.

Second , strengthen the restructuring of commercial banks and credit institutions according to modern and sustainable requirements in the direction of: diversifying ownership, types, and products; rationalizing scale, rapidly reducing the number of weak banks and credit institutions. Improve the quality of human resources, risk management capacity, strictly control bad debts, ensure liquidity and safety of the commercial banking system according to increasingly high international standards; encourage banks with conditions to develop, merge, expand their scope of operations, diversify and improve the quality of banking products and services to be competitive domestically and internationally; establish order and discipline in the management and use of foreign exchange; gradually reduce the rate of

Provide capital for development investment from the commercial banking system, increase the proportion of capital mobilization from the stock market and corporate bonds.

Third , perfect the financial and banking supervision and stability mechanism. Strengthen specialized supervision and comprehensive supervision, cross-supervision as required to ensure the safety of the national financial and banking system; clearly stipulate the coordination relationship between relevant agencies, ensure the consistency of the legal basis and practical effectiveness of the Budget Law, the State Bank Law, the Credit Institution Law, the Deposit Insurance Law, the Safety Supervision Law, the Securities Trading Law, closely following the above general orientation. In particular, it is necessary to strengthen the capacity and effectiveness of the system of institutions, rules and activities of financial safety supervision at all levels.

Fourth, adjusting the ceiling on deposit interest rates. Reality also shows that, in the process of restructuring and innovating the management of the banking system, it is necessary to soon soften the ceiling on deposit interest rates and control the ceiling on lending interest rates to limit the circular capital trading and minimize risky lending to speculative sectors, thereby helping to improve capital sources for production investment, as well as minimizing the risk of instability in the banking system; it is necessary to use more economic tools, along with administrative tools to direct banks to credit activities that bring high efficiency to the economy.

3.1.2. Orientation of applying Basel II Agreement to risk management system

The current system of supervisory and regulatory agencies in Vietnam still has many limitations, which strongly affect the safety of the financial system in general and the commercial banking system in particular. Supervisory activities have not focused on early warning and currently focus mainly on compliance monitoring of individual institutions. Therefore, restructuring commercial banks towards financial health, restructuring operations, restructuring the governance system, and restructuring legal entities and ownership must be carried out together with reaching the effectiveness of supervision according to Basel II standards as soon as possible.

The new Basel Accord sets out the basic pillars of minimum capital requirements, inspection and supervision assessment procedures and market discipline. The process of international financial and banking system integration requires the need to improve information transparency to control risks in the banking system. In order to control risks and increase the transparency of the Vietnamese banking system based on the spirit of the new Basel Accord, there are some following orientations: