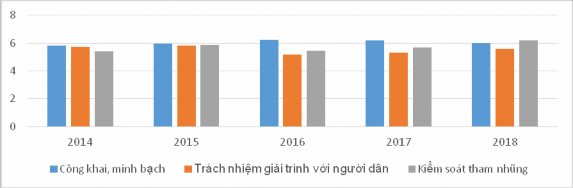

Source: Provincial Governance and Public Administration Performance Index (PAPI) Report: Measured from people's practical experience in the period 2014 - 2018 According to chart 3.6, it can be seen that in the period 2014 - 2018, the performance index

Thai Nguyen province's governance and public administration have achieved certain results based on people's experiences and assessments when interacting with local authorities. The overall assessment results show that in 2018, Thai Nguyen's PAPI index reached 45.66 points, an increase of 8.13 points compared to 2017 and ranked 12th out of 63 provinces and cities, among the top localities in the country, up 5 places compared to 2017, with high-ranking indicators such as: People's participation at the grassroots level; transparency at the provincial level; accountability of people at the provincial level; public administrative procedures; e-governance efficiency. This is the result of the direction, leadership, efforts and attempts of all levels, sectors and localities in implementing solutions to improve the quality of criteria, creating conditions for people to improve their quality of life.

Maybe you are interested!

-

State management of transport infrastructure construction from the State budget of Nghe An province - 13

State management of transport infrastructure construction from the State budget of Nghe An province - 13 -

Perfecting state management of tourism in Lam Dong province - 9

Perfecting state management of tourism in Lam Dong province - 9 -

State Budget Management in Ea Sup District, Dak Lak Province - 1

State Budget Management in Ea Sup District, Dak Lak Province - 1 -

Viewpoints on Perfecting State Management of Business Activities of Non-Life Insurance Enterprises in Vietnam

Viewpoints on Perfecting State Management of Business Activities of Non-Life Insurance Enterprises in Vietnam -

Perfecting the state capital management policy in state-owned enterprises after equitization in Vietnam - 22

Perfecting the state capital management policy in state-owned enterprises after equitization in Vietnam - 22

Seventh, inspection and examination of the use of the state budget and handling of violations have been carried out more regularly.

Every year, the provincial State Inspectorate, the Department of Finance Inspectorate, and the inspectorates of departments and branches develop inspection plans for the field of management and use of the State budget with the aim of: detecting loopholes in the State's financial management mechanism to recommend to competent authorities measures to overcome and amend them to suit the reality and handle violations of the law in financial management and compliance with the Accounting Law of the State budget-using units, promptly detecting and correcting existing problems and violations of the State budget-using units that have not strictly complied with the provisions of the law, promoting positive factors; contributing to

Improve the effectiveness and efficiency of using the state budget, while strengthening financial management discipline at units.

3.3.2. Limitations and causes

3.3.2.1. Limitations

First, the existence of mechanisms and policies

Thai Nguyen is still managing state budget expenditures in the traditional way, mainly focusing on input control, and managing each year. Practice shows that the traditional method of managing public expenditures and controlling inputs is subjective, arbitrary, and imposed by the agencies providing resources. This often leads to the following results:

The link between the allocated funds and the goals to be achieved is not high.

The current management of state budget expenditures in Thai Nguyen province is still carried out in a traditional manner, so there is no connection between the allocation of financial resources and the implementation of political and socio-economic goals, leading to unclear accountability in the management and use of the budget. It has not been evaluated and highlighted how the allocation and use of resources have brought about specific results and effects on socio-economic life.

Right from the planning stage as well as at the end of the management of state budget expenditures in Thai Nguyen province, there was no specific connection, no indication of the quantitative relationship between the allocated funds and the implementation (level, results and effectiveness) of the political - socio-economic tasks that the unit receiving the funds must complete. Therefore, all levels and sectors can only announce the total state budget expenditures in a discrete manner, unable to be linked to the set development goals as well as evaluate the implementation results compared to the original plan. All levels and sectors cannot clearly announce that in year N, how many resources were used, how they were used and how many poor households were eliminated? How many resources were used to improve people's quality of life and to what extent? How many resources were used for investment in infrastructure construction and what were the implementation results?......

This is one of the biggest shortcomings requiring innovation in the management of state budget expenditures in Thai Nguyen province to connect and create a link between planning and implementation results as well as promote socio-economic development in Thai Nguyen province.

There are still some shortcomings in the preparation of budget estimates.

When building a budget, using existing resources as a basis for budgeting, although financially realistic, easy to do, and consistent with current management style and thinking, also reveals many shortcomings. Negotiations right from the preparation, drafting, to approval and adjustment of the budget are often complicated and lengthy between the parties because the resource management side - always under pressure because the total budget revenue is limited while the spending tasks are large and many other units also have corresponding necessary spending needs, and the spending side - always has many financial needs to ensure the completion of assigned tasks. Therefore, right from the stage of discussing the budget estimate, the time is often long, difficult to convince and often ends with compromise between the parties. Not only that, a current reality is that such budget allocation also bears the mark of the "ask - give" mechanism, not based on actual needs as well as available resources. This limitation partly requires re-evaluation of the capacity of leaders as well as the organization and management of state budget expenditures. That is the biggest shortcoming of the traditional budget management process.

When building the State budget expenditure estimate, based on the regime, standards and norms that have been specifically prescribed, the Department of Finance has submitted to the Provincial People's Committee to build a system of budget expenditure norms, which is changed annually based on the specific situation. In the condition that financial resources are limited and cannot fully meet the needs, expenditure norms are a very good basis for allocating financial resources. However, the mechanism of allocating financial resources based on norms has also revealed shortcomings:

- When making a budget in the traditional way, it means relying mainly on input resources, so there is no connection between the planning and budgeting process and the evaluation of efficiency and spending results.

- Short-term budgeting, mainly annual budgeting, therefore does not evaluate or consider resource allocation linked to development programs.

Annual socio-economic development. When establishing short-term budgets, allocating budgets based on input factors without evaluating spending efficiency and linking them to the unit's responsibilities creates a fundamental weakness that discourages units from spending budget economically, because it does not set a reasonable and tight requirement between the allocated budget and the output achieved from using that budget.

Second: exists in the process of organizing and implementing state budget expenditure management

* Allocation of public financial resources is spread out, lacking focus and key points, and low efficiency in resource use.

Budgets are mainly short-term, based on input norms, thus not creating conditions for evaluating and considering resource allocation in conjunction with the 5-year plan and the 10-year socio-economic development strategy of the province, because these plans often focus on output targets. Output parameters as well as the results of using the budget have not been given attention, so there is a lack of motivation to build budget estimates in conjunction with reality. The mentality of relying too much on budget adjustments does not encourage budget beneficiaries to invest properly in establishing the basis and scientific budgeting methods. Currently, budgeting contains many subjective factors (desire to be allocated a lot so the budget is high, based on input norms so there is a tendency to propose many unnecessary tasks leading to waste, not encouraging economical use of the budget because items cannot be transferred, not being creative in using the budget, etc.). The annual budget is not only time-consuming, labor-intensive and costly, but also does not anticipate all medium-term events that may affect the budget. In some units, the budget for the following year is based on a slightly increased budget for the previous year. The fact that the construction budget is separate from the investment expenditure budget also causes duplicate expenditures, such as management fees. The budget also lacks a system of appropriate criteria to determine the order of priority in allocating local budget expenditures.

Normally, arranging state budget expenditures on the basis of existing resources cannot really implement the strategic intention of allocating sufficient financial resources for the selected key spending priorities.

Due to the lack of medium-term vision, not only are the financial agencies and the provincial People's Committee passive in terms of revenue, but the agencies, localities and units are also passive in terms of resources. Spending units cannot and do not have the right to be proactive.

The allocation of spending priorities according to key points and focal points. The efficiency of using public resources is therefore significantly reduced.

The traditional process of budgeting and managing state budget expenditures seems to only be concerned with immediate benefits, year by year, without a medium-term vision, and the budget is only built for a period of one year. At the end of each budget year, the budget estimate will expire, and people will continue to make a budget plan for the next (one) year. At the end of the year, the allocated funds that have not been fully used (even though there is still a need for spending) must be canceled. Budget settlement reports often only focus on whether the budget expenditures are fully budgeted or not? Inspections and controls only consider whether the spending is within the norm or not? Are there any violations of the financial regime? But they have not paid attention to evaluating the results achieved compared to the plan, as well as what results those expenditures have created to serve the socio-economic development process?

In the process of implementing state budget expenditure tasks, most activities continue from year to year, many tasks require more than a year to complete, many expenditure items are extended beyond a budget year. Therefore, if state budget expenditure tasks are only implemented in one year, management agencies cannot predict revenue sources and do not have appropriate medium-term budget arrangements. Management agencies as well as budget-using units are passive in the face of economic and financial developments, in the face of total revenue and expenditure in annual estimates, the implementation process is passive in terms of resources, and is even suspended due to the lack of medium-term budget arrangements.

Often due to lack of resources but high demand, resources are forced to be spread out, many items are spent "moderately", public financial resources are not allocated to the necessary threshold. Therefore, investment time is extended beyond necessary, projects are slow to develop effectively, many fields due to lack of capital cannot invest "to the fullest", cannot create the necessary "strategic punches" to develop a certain industry or field... In other words, funding sources for the above plans are not given due attention, leading to financial shortages.

As a result, many projects are either waiting for funding or abandoned. In addition, investment costs are spread across many projects, causing local priorities to not be funded commensurate with their importance.

Furthermore, coordination at the macro level also has many shortcomings when public resources are always limited. In a certain period, the connection between sector strategies and the development of specific financial plans is often not tight. Therefore, it is necessary to change the mindset so that it can connect the resources to be allocated and the expected results to be achieved. It is necessary to allocate limited resources in a more practical way, with more practical measures, ensuring allocation to the necessary threshold, for necessary tasks, implementing decisive, focused, and key investments. If so, public resources will definitely be used reasonably, optimally, and will bring about certain results. The method of budget planning according to a medium-term framework linked to output results will allow to implement those requirements.

* Poor public sector performance

In the implementation organization, many agencies and units cite many reasons to increase the payroll before accepting the contract, then find ways to claim the budget for this increased payroll. And even in the contract mechanism, there is no specific final product, only the general product of completing the assigned functions and tasks, which cannot demonstrate the effectiveness and impact of the results of the contract...

Sectors and levels have not really paid attention to directing, operating and implementing the mechanism of autonomy in apparatus, staffing and finance, especially at the district level. Some policy mechanisms have not been specified and completed, so agencies are passive in the implementation process.

The establishment of criteria to evaluate the level of completion of assigned tasks such as volume and quality of work of the unit has not been implemented, so the payment of additional income is still equal and average.

The central allocation norms are still low and stable over a long period of time, while market prices fluctuate strongly, so many units cannot save money or save insignificantly, which has limited the meaning of autonomy and increased income for cadres and civil servants.

Existing budget resources are not sufficient for public activities, even after the budget is approved. Managers are always passive, not sure of resources to proactively balance short-term and long-term needs.

Legally, budget control is established in a highly centralized manner with many detailed regulations on asset purchases, spending norms, etc. However, in reality, official control is not effectively implemented due to lack of information on management organization.

* Discipline in implementing NS is not really strict, still applying "soft NS" plan

The management and control of expenditures are not strict enough, so there is still a situation of loss and waste of State budget funds, especially expenditures for infrastructure repair. The situation of spending incorrectly on regimes and policies has not ended. Instead of reducing the payroll and managing in a streamlined manner, in the past 3 years, Thai Nguyen province has established Pho Yen town and 4 wards in Pho Yen town and established Luong Son ward in Song Cong town and Song Cong city. The establishment of towns and cities increases the scale of public funding and the number of state employees, while efficiency in the public sector does not increase and civil servants have no motivation to try.

There are still cases of unplanned spending according to the request-grant mechanism. Some units that receive the State budget have not properly implemented the State budget expenditure management process, such as having CTX items that are not according to the budget estimate, not requesting timely budget adjustment, and having a large difference between the budget estimate and the budget implementation, but the State budget management agency still accepts the final settlement...

Some units lack initiative in managing expenditures according to assigned budgets and allowable revenue sources, and expenditures without guaranteed sources lead to an increasing trend in state debt. The distinction between investment expenditures and CTX expenditures of some departments and branches is not clear, leading to a prolonged capital allocation period.

* Management of investment capital from the state budget still has many shortcomings.

There are still some mistakes in the management of capital for construction investment that make the investment results not as expected. Specifically:

- The process of investment project preparation still has many shortcomings, leading to some projects having scale and functions exceeding the demand for use, while some other investment projects are not invested synchronously, so they cannot fully promote their functions and efficiency after completion and put into use; some projects are designed with low quality, during the construction process, they have to stop for adjustment, leading to the total investment increasing many times, making management agencies passive in balancing annual capital, slow construction progress. Some investment projects have not been carefully prepared, the quality of documents is low, the calculation of investment needs is not close to reality, when implemented, new costs arise, making the investment capital larger than the estimate, causing difficulties for both the capital approval agency and the construction unit. The quality of examination and approval of technical design, construction drawings, and total estimates carried out by some investors has not met the requirements.

- The investment capital plan is still spread out and dispersed beyond the maximum time limit prescribed by the Government, which prolongs the project implementation time, increases investment costs, delays putting the project into operation and use, and reduces the socio-economic efficiency of the investment capital. When developing the investment plan, the investor has not proactively arranged enough resources to pay off due loans, resulting in overdue interest costs and bad debts. The allocation of the capital plan is not reasonable: The Central Government assigns detailed capital plans from the Central budget to support each project category throughout the medium term. During the implementation process, if there are problems that arise that require adjustment and capital coordination, the locality must submit them to the Central Government for consideration and decision, which takes a lot of time. Some capital sources that the Central Government has assigned are slow to guide implementation, affecting the progress of capital allocation and capital accumulation at the end of the year. Therefore, there is always a situation where the annual investment capital plan is not fully disbursed and must be transferred to the following year. Some projects and works have been appraised, settled, and have completed volume, but capital has not been allocated for final payment. The situation of implementing construction investment exceeding the state budget's capacity is still happening, leading to a tendency for public debt to increase.

- There are still some violations in the implementation of investment projects, causing waste and loss of investment capital. The use of NS in some projects is still wasteful, and there are hidden costs. The progress of some key projects does not meet requirements due to the low capital mobilization capacity of investors. Some contractors committed to investing capital for construction when bidding, but when implementing, there is not enough capital according to the committed progress, leading to delays.