The bank has brought preferential capital directly to poor households, ensuring the right subjects, collecting debts and interest on time, guiding borrowers to use capital for the right purposes, improving capital efficiency, increasing income, improving life, escaping poverty and getting rich.

Savings and loan groups are a small financial model, which can be considered a microfinance model in rural areas, but under the unified guidance and management of the Vietnam Bank for Social Policies. After a period of operation, this model has really met many requirements for the organization and management of credit in rural areas, especially policy credit. It can be affirmed that the savings and loan group model has a very important position, considered as an extension of the Vietnam Bank for Social Policies in transferring capital directly to poor households. Savings and loan groups also help the Bank in deploying and mobilizing savings from group members, helping households save money to repay debts to the bank when due, at the same time, with the capital mobilized by the savings and loan groups, the Bank deploys it to lend to other subjects with economic difficulties.

Thus, it can be said that credit activities through savings and loan groups have actively supported banks in allocating and recovering capital, saving and initially bringing about encouraging results: Investment capital is preserved and quickly rotated, helping poor farmers increase their income, promoting the spirit of mutual love, mutual assistance, self-reliance to escape poverty, building poor farmers with a sense of credit discipline, enhancing the spirit of volunteerism and self-awareness in credit relations without the need for collateral. The average interest rate of the Bank is very high at over 95%.

2.2.1.3. Business process of lending to poor households of the Social Policy Bank of Thai Nguyen province

To borrow capital from the Social Policy Bank, the borrower must appoint a family representative to represent the family in transactions with the policy bank. The borrower must be considered and accepted into the group by the members of the savings and loan group in the presence of the village chief and the chairman or vice chairman of the commune association.

(2)

(5)

(6)

Organization

Commune level social work

(7)

(8)

(1)

Social Policy Bank

Commune People's Committee

Poor household

TK&VV Group

(3)

(4)

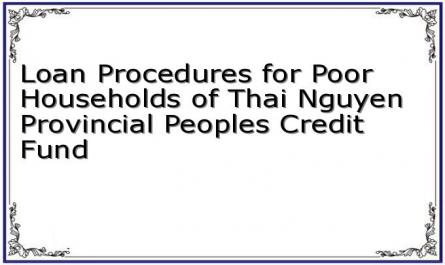

Figure 2.2 Flowchart of lending process for poor households through savings and credit groups

Step 1: When in need of a loan, the borrower writes a Loan Application (Form No. 01/TD) and sends it to the Savings and Credit Group.

Step 2: The Savings and Credit Group, together with the Association and mass organizations, organizes a meeting to publicly review poor households eligible for loans, compiles a list in Form 03/TD and submits it to the Commune People's Committee for confirmation that they are eligible for loans and legally residing in the commune.

Step 3: The Savings and Credit Group sends the loan application to the Bank.

Step 4: The bank approves the loan and notifies the People's Committee at the commune level" (Form 04/TD).

Step 5: The People's Committee at the commune level notifies the commune-level Association and mass organization.

Step 6: Commune-level associations and unions notify the Saving and Credit Group.

Step 7: The Savings and Credit Group notifies the group members/borrowing households of the list of households eligible for loans, time and place of disbursement.

Step 8: The bank disburses directly to the borrower.

2.2.2. Criteria for assessing the quality of loans for poor households of the Social Policy Bank of Thai Nguyen province

2.2.2.1. Quantitative criteria

a) On loan sales for the poor and loan sales growth rate

Loan turnover is an indicator reflecting the credit scale of a bank. Through data on outstanding loans from 2018 to 2020, we will analyze to see more clearly about lending to poor and near-poor households at the branch.

Table 2.4: Loan turnover for poor households in the period 2018–2020

Unit: Million VND

Target

Year 2018 | Year 2019 | Year 2020 | 2019/2018 | 2020/2019 | |

Household loan sales poor | 316,626 | 407,608 | 291,588 | 28.73 | -28.46 |

Tr: Short-term loans | 0 | 0 | 0 | 0 | 0 |

Medium term loans | 316,626 | 407,608 | 291,588 | ||

-Number of customers borrowing capital | 11,102 | 12.121 | 7,633 | 9.18 | -37.03 |

Maybe you are interested!

-

Entrusting loans for poor households between the social policy bank and socio-political organizations in Bang Thanh commune, Pac Nam district, Bac Kan province - 6

Entrusting loans for poor households between the social policy bank and socio-political organizations in Bang Thanh commune, Pac Nam district, Bac Kan province - 6 -

Home business households and preferential loan procedures at banks today - 3

Home business households and preferential loan procedures at banks today - 3 -

Social security policy for poor households in Nghia Hung district, Nam Dinh province - 2

Social security policy for poor households in Nghia Hung district, Nam Dinh province - 2 -

Actual Loan Usage Situation of Surveyed Households

Actual Loan Usage Situation of Surveyed Households -

Factors Affecting Loan Quality for the Poor

Factors Affecting Loan Quality for the Poor

Source: Report of Thai Nguyen Social Policy Bank

The Bank's lending turnover to the poor has increased and decreased unevenly. In 2018, the lending turnover reached 316 billion VND, in 2019, the lending turnover increased to 407 billion VND; in 2020, it decreased to 291 billion VND; the growth rate fluctuated.

Over the years, in 2019/2018 it was 28.73%, the growth rate in 2020/2019 decreased by 2% due to the characteristics of the Social Policy Bank when approving loans, it must be the right target, the poor households whose names are on the list of poor households at the People's Committee of the commune or ward in the area, the number of poor households over the years has gradually decreased, so the growth rate of loan sales tends to decrease, which is inevitable and difficult to avoid. Moreover, poor households borrow capital for production

The business has not escaped poverty and still needs capital, so the Bank extended the loan period.

b) Total outstanding loans and growth rate of outstanding loans for the poor

Outstanding loans are an indicator reflecting the credit scale of a bank. Through data on outstanding loans from 2018 to 2020, we will analyze to see more clearly about loans for poor and near-poor households at the branch.

Table 2.5: Total outstanding loans for poor households in the period 2018 - 2020

Unit: Million VND

Target

2018 | 2019 | 2020 | ||||

Amount | Rate (%) | Amount | Rate (%) | Amount | Rate (%) | |

Total outstanding debt | 1,024,338 | 100 | 1,128,311 | 100 | 1,165,443 | 100 |

Short term | 120 | 0.01 | 60 | 0.005 | 0 | 0 |

Medium term | 1,024,218 | 99.99 | 1,128,251 | 99,995 | 1,165,443 | 100 |

Source: Thai Nguyen Social Policy Bank Report Through the above data table, we can see that although the lending turnover for poor households of Thai Nguyen Provincial Social Policy Bank has decreased, the outstanding debt still tends to increase. The data table shows that the outstanding debt in 2019 increased by 124 billion VND compared to 2018, and in 2020 increased by 3 billion VND compared to 2019. In which, mainly medium-term loans because the Bank's service objects are poor households, near-poor households, the main purpose of capital use is livestock, cultivation and investment in craft villages, so the Bank's medium-term loans account for a large proportion of more than %, while short-term loans only account for a very small proportion.

small, accounting for less than 1% of total outstanding loans to the poor.

The number of poor households has decreased over the years, leading to a decrease in the number of poor households receiving loans, so the growth rate of outstanding loans for poor households in the period 2018 - 2020 of the Social Policy Bank of Thai Nguyen province tends to decrease gradually. Through the above table, we can see that the growth rate

The growth of outstanding short-term loans to poor households has decreased steadily, due to the poor households' need to borrow capital to invest in crops and livestock with long-term capital recovery cycles.

c) Rate of poor households receiving loans

Table 2.6: Rate of poor households receiving loans from the Social Policy Bank of Thai Nguyen province in the period 2018 - 2020

Unit: Million VND

Target

Year 2018 | Year 2019 | Year 2020 | 2019/2018 | 2020/2019 | |

-Number of customers borrowing capital | 11,102 | 12.121 | 7,633 | 9.18 | -37.03 |

Number of poor households | 25,007 | 19,735 | 15,936 | -17.08 | 23.14 |

The rate of poor households is loan | 55.60 | 41.54 | 52.10 | -14.06 | 10.56 |

Source: Report of Thai Nguyen Social Policy Bank Through the above table, it can be seen that the poverty rate of Thai Nguyen province tends to decrease over the years. However, in the period 2018-2020, the rate of poor households receiving loans tends to increase and decrease unevenly over the years. In 2018, 55.60 poor households received loans, in 2018, it accounted for 41.54%, and by 2020, it increased to account for 10.

52.10%.

d) Average loan amount per household

In the process of implementing the poverty reduction policy, the loan amount for poor households has changed over time. In 2003 and 2004, the maximum loan amount for poor households was 5 - 10 million VND/loan, then increased to 10 million VND... and by 2019 the maximum loan amount was 35 million VND (for households raising large livestock, growing perennial crops and lending to craft villages). In 2019, the outstanding loan balance for poor households of the Thai Nguyen Provincial Social Policy Bank was 1,128 billion VND, with an average loan of 28 million VND per household. By the end of 2020, the Thai Nguyen Provincial Social Policy Bank had 36,703 households.

The poor are borrowing capital from poverty reduction funds, with a total outstanding debt of 1,165 billion VND, on average each household can borrow 31.75 million VND/loan.

The number of households escaping poverty in 2019 was 6,995, a decrease of 205 households compared to 2019. By 2020, the number of households escaping poverty had increased to 60 households. This shows that the loan capital has been used effectively, helping households escape poverty to increase.

e) Income indicators from lending activities to the poor

Revenue from lending activities is one of the important indicators to evaluate the quality of lending. If the quality of lending is good, the loans will be paid on time, with low interest debt, contributing greatly to increasing the income of the Bank.

Table 2.7: Interest income from lending activities to poor households in the period 2018–2020

Unit: Million VND

Target

2018 | 2019 | 2020 | ||||

Amount | Rate (%) | Amount | Proportion (%) | Amount | Rate (%) | |

Total profit receivable | 74,728 | 100 | 76,933 | 100 | 79,028 | 100 |

Interest earned | 73,607 | 98.5 | 75,858 | 98.6 | 78,000 | 98.7 |

Remaining interest receivable | 1.121 | 1.5 | 1,077 | 1.4 | 1,028 | 1.3 |

Source: Report of Thai Nguyen Social Policy Bank

The total income of the Bank's lending program for the poor is quite stable, with a stable interest rate of 98% of the total interest receivable. The above results are due to the Bank's strengthening of lending activities in Thai Nguyen province, disbursing all credit plans and making optimal use of capital transferred from superiors to lend to the poor. Moreover, in recent years, most of the poor households borrowing from the Bank have been producing and doing business effectively, with high income, preserving capital and paying interest to the bank as agreed. This proves that the Bank has focused on improving credit quality. However,

In addition, some poor households borrow capital from the Bank and operate ineffectively, leading to failure to repay the principal and interest on time, reducing the Bank's income.

f) Indicator of overdue debt ratio for loans to poor households

Any credit institution must face difficulties in lending and debt collection from customers. The problem that causes lending risk is directly manifested in overdue debt. Overdue debt is also an indicator to evaluate loan quality, it reflects the safety and ability to recover capital of each loan.

Table 2.8: Rate of overdue loans for poor households in the period 2018 - 2020

Unit: Million VND

Target

2018 | 2019 | 2020 | |

Total outstanding loans for the poor | 1,024,338 | 1,128,311 | 1,165,443 |

Overdue debt for poor households | 1,164 | 1,756 | 2,771 |

Overdue debt rate for household loans poor(%) | 0.11 | 0.16 | 0.24 |

Source: Report of Thai Nguyen Social Policy Bank

Through the above table, we can see that the rate of overdue loans for poor households at the Social Policy Bank of Thai Nguyen province, although still low, has tended to increase gradually in the period 2018-2020. That shows that the quality of loans at the Social Policy Bank of Thai Nguyen province is still not high.

2.2.2.2.Qualitative criteria

Regarding consulting information, most of the 90 households surveyed received consulting information from the Bank. This proves that the Bank has been active in propaganda and consulting on issues for poor households.

Table 2.9: Opinions of 90 poor households that received loans surveyed

Total | Vo Nhai | Pho Yen | Defining | |||||

Number household | % | Number household | % | Number household | % | Number household | % | |

1. Number of households borrowing capital | 90 | 100 | 30 | 100 | 30 | 100 | 30 | 100 |

2. Have consulting information | ||||||||

- Have | 90 | 100 | 30 | 100 | 30 | 100 | 30 | 100 |

- Are not | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

3. Loan Procedure Evaluation | ||||||||

- Complicated | 8 | 8.89 | 4 | 13.33 | 1 | 3.33 | 3 | 10 |

- Normal | 23 | 25.56 | 9 | 30 | 7 | 23.33 | 7 | 23.33 |

- Convenient | 41 | 45.55 | 9 | 30 | 18 | 60 | 14 | 46.67 |

- Very convenient | 18 | 20 | 8 | 26.67 | 4 | 13.34 | 6 | 20 |

4. Loan term assessment | ||||||||

- Short | 31 | 34.44 | 11 | 36.67 | 5 | 16.67 | 15 | 50 |

- Fit | 59 | 65.56 | 19 | 63.33 | 25 | 83.33 | 15 | 50 |

5. Interest Rate Assessment | ||||||||

- Short | 24 | 26.67 | 9 | 30 | 7 | 23.33 | 8 | 26.67 |

- Fit | 66 | 73.33 | 21 | 70 | 23 | 76.67 | 22 | 73.33 |

6. Comments on CBTD | ||||||||

- Normal | 24 | 26.67 | 7 | 23.33 | 10 | 33.33 | 7 | 23.33 |

- Enthusiasm | 50 | 55.56 | 11 | 36.67 | 16 | 53.33 | 23 | 76.67 |

- Very enthusiastic | 16 | 17.77 | 12 | 40 | 4 | 13.34 | 0 | 0 |

7. Need to borrow more | ||||||||

- Have | 83 | 92.22 | 28 | 93.33 | 26 | 86.67 | 29 | 96.67 |

- Are not | 7 | 7.78 | 2 | 6.67 | 4 | 13.33 | 1 | 3.33 |

(Source: Actual survey data in 2021) The above survey data table shows:

First, about the lending process and procedures.