+ Decide on exchange rates for buying and selling foreign currencies according to regulations of the State Bank and BIDV.

+ Decide on commission rates, fees, bonuses, and penalties in business and service activities within the limits prescribed by the State and BIDV.

+ Sign credit contracts and business cooperation with financial and credit institutions according to regulations of the State Bank and BIDV.

+ File lawsuits on economic and civil disputes, request competent authorities to initiate criminal prosecution when there are signs of crime related to the Branch's operations according to BIDV's regulations.

+ Responsible for business results, capital preservation and development, principal and interest recovery, ensuring growth of branch business activities.

+ When borrowing capital, customers are required to provide documents, records and information on the production, business and financial situation according to credit regulations to decide on lending and providing banking services, check the situation and results of loan use, suspend early collection in cases where the branch checks and finds that the capital is used for the wrong purpose, violates state regulations, credit contracts, credit regulations and customer commitments to the bank.

+ Foreclose mortgaged or pledged assets when customers cannot pay their debts on time.

+ Be responsible for economic and civil obligations and commitments between the Branch and customers, keep confidential customer data and operations.

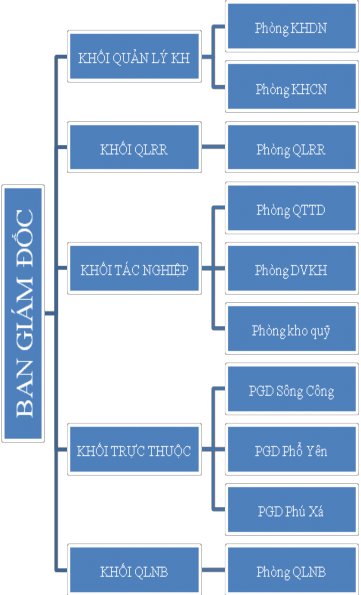

3.1.2. Human resource organization model at BIDV - Nam Thai Nguyen Branch

3.1.2.1. Organizational structure

BIDV - Nam Thai Nguyen Branch has built for itself a reasonable and compact organizational structure but still ensures flexibility and speed in handling work, suitable for the market economy.

The organizational structure of BIDV - Nam Thai Nguyen Branch as of December 31, 2017 includes: Board of Directors (1 Director and 3 Deputy Directors),

operating 5 operating blocks (Customer Management Block, Risk Management Block, Operations Block, Affiliated Block, and Internal Management Block) with small offices.

Figure 3.1: Organizational model diagram of BIDV Nam Thai Nguyen

Source: BIDV Nam Thai Nguyen

3.1.2.2. Human resources

Table 3.1: Human resource structure in the period 2015-2017 of BIDV - Nam Thai Nguyen

Year

2015 | 2016 | 2017 | ||||

People | (%) | People | (%) | People | (%) | |

1. Age | ||||||

Under 30 | 33 | 46.48 | 33 | 44 | 38 | 47.5 |

From 30 - 40 | 29 | 40.85 | 29 | 38.67 | 28 | 35 |

Over 40 | 9 | 12.68 | 13 | 17.33 | 14 | 17.5 |

2. Gender | ||||||

- Male | 31 | 43.66 | 33 | 44 | 36 | 45 |

- Female | 40 | 56.34 | 42 | 56 | 44 | 55 |

3. Level | ||||||

- Postgraduate | 14 | 19.72 | 16 | 21.33 | 19 | 23.75 |

- University | 55 | 77.46 | 57 | 76 | 59 | 73.75 |

-High school, high school, other | 2 | 2.82 | 2 | 2.67 | 2 | 2.5 |

4. Professional Labor (Officer) | 31 | 28 | 30 | |||

- Customer Management Officer | 14 | 45.16 | 16 | 57.14 | 18 | 60 |

- Other professional staff | 17 | 54.84 | 12 | 42.86 | 12 | 40 |

Total number of employees | 71 | 100 | 75 | 100 | 80 | 100 |

Maybe you are interested!

-

Retail credit risk management at Vietnam Joint Stock Commercial Bank for Investment and Development - Nam Thai Nguyen Branch - 2

Retail credit risk management at Vietnam Joint Stock Commercial Bank for Investment and Development - Nam Thai Nguyen Branch - 2 -

Solutions for tourism development in Tien Lang - 10

zt2i3t4l5ee

zt2a3gstourism, tourism development

zt2a3ge

zc2o3n4t5e6n7ts

- District People's Committees and authorities of communes with tourist attractions should support, promote, and provide necessary information to people, helping them improve their knowledge about tourism. Raise tourism awareness for local people.

*

* *

Due to limited knowledge and research time, the thesis inevitably has shortcomings. Therefore, I look forward to receiving guidance from teachers, experts as well as your comments to make the thesis more complete.

Chapter III Conclusion

Through the issues presented in Chapter II, we can come to some conclusions:

Based on the strengths of available tourism resources, the types of tourism in Tien Lang that need to be promoted in the coming time are sightseeing and resort tourism, discovery tourism, weekend tourism. To improve the quality and diversify tourism products, Tien Lang district needs to combine with local cultural tourism resources, at the same time combine with surrounding areas, build rich tourism products. The strengths of Tien Lang tourism are eco-tourism and cultural tourism, so developing Tien Lang tourism must always go hand in hand with restoring and preserving types of cultural tourism resources. Some necessary measures to support and improve the efficiency of exploiting tourism resources in Tien Lang are: strengthening the construction of technical facilities and labor force serving tourism, actively promoting and advertising tourism, and expanding forms of capital mobilization for tourism development.

CONCLUDE

I Conclusion

1. Based on the results achieved within the framework of the thesis's needs, some basic conclusions can be drawn as follows:

Tien Lang is a locality with great potential for tourism development. The relatively abundant cultural tourism resources and ecological tourism resources have great appeal to tourists. Based on this potential, Tien Lang can build a unique tourism industry that is competitive enough with other localities within Hai Phong city and neighboring areas.

In recent years, the exploitation of the advantages of resources to develop tourism and build tourist routes in Tien Lang has not been commensurate with the available potential. In terms of quantity, many resource objects have not been brought into the purpose of tourism development. In terms of time, the regular service time has not been extended to attract more visitors. Infrastructure and technical facilities are still weak. The labor force is still thin and weak in terms of expertise. Tourism programs and routes have not been organized properly, the exploitation content is still monotonous, so it has not attracted many visitors. Although resources have not been mobilized much for tourism development, they are facing the risk of destruction and degradation.

2. Based on the results of investigation, analysis, synthesis, evaluation and selective absorption of research results of related topics, the thesis has proposed a number of necessary solutions to improve the efficiency of exploiting tourism resources in Tien Lang such as: promoting the restoration and conservation of tourism resources, focusing on investment and key exploitation of ecotourism resources, strengthening the construction of infrastructure and tourism workforce. Expanding forms of capital mobilization. In addition, the thesis has built a number of tourist routes of Hai Phong in which Tien Lang tourism resources play an important role.

Exploiting Tien Lang tourism resources for tourism development is currently facing many difficulties. The above measures, if applied synchronously, will likely bring new prospects for the local tourism industry, contributing to making Tien Lang tourism an important economic sector in the district's economic structure.

REFERENCES

1. Nhuan Ha, Trinh Minh Hien, Tran Phuong, Hai Phong - Historical and cultural relics, Hai Phong Publishing House, 1993

2. Hai Phong City History Council, Hai Phong Gazetteer, Hai Phong Publishing House, 1990.

3. Hai Phong City History Council, History of Tien Lang District Party Committee, Hai Phong Publishing House, 1990.

4. Hai Phong City History Council, University of Social Sciences and Humanities, VNU, Hai Phong Place Names Encyclopedia, Hai Phong Publishing House. 2001.

5. Law on Cultural Heritage and documents guiding its implementation, National Political Publishing House, Hanoi, 2003.

6. Tran Duc Thanh, Lecture on Tourism Geography, Faculty of Tourism, University of Social Sciences and Humanities, VNU, 2006

7. Hai Phong Center for Social Sciences and Humanities, Some typical cultural heritages of Hai Phong, Hai Phong Publishing House, 2001

8. Nguyen Ngoc Thao (editor-in-chief, Tourism Geography, Hai Phong Publishing House, two volumes (2001-2002)

9. Nguyen Minh Tue and group of authors, Hai Phong Tourism Geography, Ho Chi Minh City Publishing House, 1997.

10. Nguyen Thanh Son, Hai Phong Tourism Territory Organization, Associate Doctoral Thesis in Geological Geography, Hanoi, 1996.

11. Decision No. 2033/QD – UB on detailed planning of Tien Lang town, Hai Phong city until 2020.

12. Department of Culture, Information, Hai Phong Museum, Hai Phong relics

- National ranked scenic spot, Hai Phong Publishing House, 2005. 13. Tien Lang District People's Committee, Economic Development Planning -

Culture - Society of Tien Lang district to 2010.

14.Website www.HaiPhong.gov.vn

APPENDIX 1

List of national ranked monuments

STT

Name of the monument

Number, year of decisiondetermine

Location

1

Gam Temple

938 VH/QĐ04/08/1992

Cam Khe Village- Toan Thang commune

2

Doc Hau Temple

9381 VH/QĐ04/08/1992

Doc Hau Village –Toan Thang commune

3

Cuu Doi Communal House

3207 VH/QĐDecember 30, 1991

Zone II of townTien Lang

4

Ha Dai Temple

938 VH/QĐ04/08/1992

Ha Dai Village –Tien Thanh commune

APPENDIX II

STT

Name of the monument

Number, year of decision

Location

1

Phu Ke Pagoda Temple

178/QD-UBJanuary 28, 2005

Zone 1 - townTien Lang

2

Trung Lang Temple

178/QD-UBJanuary 28, 2005

Zone 4 – townTien Lang

3

Bao Khanh Pagoda

1900/QD-UBAugust 24, 2006

Nam Tu Village -Kien Thiet commune

4

Bach Da Pagoda

1792/QD-UB11/11/2002

Hung Thang Commune

5

Ngoc Dong Temple

177/QD-UBNovember 27, 2005

Tien Thanh Commune

6

Tomb of Minister TSNhu Van Lan

2848/QD-UBSeptember 19, 2003

Nam Tu Village -Kien Thiet commune

7

Canh Son Stone Temple

2160/QD-UBSeptember 19, 2003

Van Doi Commune –Doan Lap

8

Meiji Temple

2259/QD-UBSeptember 19, 2002

Toan Thang Commune

9

Tien Doi Noi Temple

477/QD-UBSeptember 19, 2005

Doan Lap Commune

10

Tu Doi Temple

177/QD-UBJanuary 28, 2005

Doan Lap Commune

11

Duyen Lao Temple

177/QD-UBJanuary 28, 2005

Tien Minh Commune

12

Dinh Xuan Uc Pagoda

177/QD-UBJanuary 28, 2005

Bac Hung Commune

13

Chu Khe Pagoda

177/QD-UBJanuary 28, 2005

Hung Thang Commune

14

Dong Dinh

2848/QD-UBNovember 21, 2002

Vinh Quang Commune

15

President's Memorial HouseTon Duc Thang

177/QD-UBJanuary 28, 2005

NT Quy Cao

Ha Dai Temple

Ben Vua Temple

Tien Lang hot spring

div.maincontent .p { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; } div.maincontent p { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; } div.maincontent .s1 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; font-size: 16pt; } div.maincontent .s2 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s3 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s4 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; font-size: 14pt; } div.maincontent .s5 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; font-size: 14pt; } div.maincontent .s6 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s7 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s8 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; vertical-align: 6pt; } div.maincontent .s9 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 12pt; } div.maincontent .s11 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; tex

Solutions for tourism development in Tien Lang - 10

zt2i3t4l5ee

zt2a3gstourism, tourism development

zt2a3ge

zc2o3n4t5e6n7ts

- District People's Committees and authorities of communes with tourist attractions should support, promote, and provide necessary information to people, helping them improve their knowledge about tourism. Raise tourism awareness for local people.

*

* *

Due to limited knowledge and research time, the thesis inevitably has shortcomings. Therefore, I look forward to receiving guidance from teachers, experts as well as your comments to make the thesis more complete.

Chapter III Conclusion

Through the issues presented in Chapter II, we can come to some conclusions:

Based on the strengths of available tourism resources, the types of tourism in Tien Lang that need to be promoted in the coming time are sightseeing and resort tourism, discovery tourism, weekend tourism. To improve the quality and diversify tourism products, Tien Lang district needs to combine with local cultural tourism resources, at the same time combine with surrounding areas, build rich tourism products. The strengths of Tien Lang tourism are eco-tourism and cultural tourism, so developing Tien Lang tourism must always go hand in hand with restoring and preserving types of cultural tourism resources. Some necessary measures to support and improve the efficiency of exploiting tourism resources in Tien Lang are: strengthening the construction of technical facilities and labor force serving tourism, actively promoting and advertising tourism, and expanding forms of capital mobilization for tourism development.

CONCLUDE

I Conclusion

1. Based on the results achieved within the framework of the thesis's needs, some basic conclusions can be drawn as follows:

Tien Lang is a locality with great potential for tourism development. The relatively abundant cultural tourism resources and ecological tourism resources have great appeal to tourists. Based on this potential, Tien Lang can build a unique tourism industry that is competitive enough with other localities within Hai Phong city and neighboring areas.

In recent years, the exploitation of the advantages of resources to develop tourism and build tourist routes in Tien Lang has not been commensurate with the available potential. In terms of quantity, many resource objects have not been brought into the purpose of tourism development. In terms of time, the regular service time has not been extended to attract more visitors. Infrastructure and technical facilities are still weak. The labor force is still thin and weak in terms of expertise. Tourism programs and routes have not been organized properly, the exploitation content is still monotonous, so it has not attracted many visitors. Although resources have not been mobilized much for tourism development, they are facing the risk of destruction and degradation.

2. Based on the results of investigation, analysis, synthesis, evaluation and selective absorption of research results of related topics, the thesis has proposed a number of necessary solutions to improve the efficiency of exploiting tourism resources in Tien Lang such as: promoting the restoration and conservation of tourism resources, focusing on investment and key exploitation of ecotourism resources, strengthening the construction of infrastructure and tourism workforce. Expanding forms of capital mobilization. In addition, the thesis has built a number of tourist routes of Hai Phong in which Tien Lang tourism resources play an important role.

Exploiting Tien Lang tourism resources for tourism development is currently facing many difficulties. The above measures, if applied synchronously, will likely bring new prospects for the local tourism industry, contributing to making Tien Lang tourism an important economic sector in the district's economic structure.

REFERENCES

1. Nhuan Ha, Trinh Minh Hien, Tran Phuong, Hai Phong - Historical and cultural relics, Hai Phong Publishing House, 1993

2. Hai Phong City History Council, Hai Phong Gazetteer, Hai Phong Publishing House, 1990.

3. Hai Phong City History Council, History of Tien Lang District Party Committee, Hai Phong Publishing House, 1990.

4. Hai Phong City History Council, University of Social Sciences and Humanities, VNU, Hai Phong Place Names Encyclopedia, Hai Phong Publishing House. 2001.

5. Law on Cultural Heritage and documents guiding its implementation, National Political Publishing House, Hanoi, 2003.

6. Tran Duc Thanh, Lecture on Tourism Geography, Faculty of Tourism, University of Social Sciences and Humanities, VNU, 2006

7. Hai Phong Center for Social Sciences and Humanities, Some typical cultural heritages of Hai Phong, Hai Phong Publishing House, 2001

8. Nguyen Ngoc Thao (editor-in-chief, Tourism Geography, Hai Phong Publishing House, two volumes (2001-2002)

9. Nguyen Minh Tue and group of authors, Hai Phong Tourism Geography, Ho Chi Minh City Publishing House, 1997.

10. Nguyen Thanh Son, Hai Phong Tourism Territory Organization, Associate Doctoral Thesis in Geological Geography, Hanoi, 1996.

11. Decision No. 2033/QD – UB on detailed planning of Tien Lang town, Hai Phong city until 2020.

12. Department of Culture, Information, Hai Phong Museum, Hai Phong relics

- National ranked scenic spot, Hai Phong Publishing House, 2005. 13. Tien Lang District People's Committee, Economic Development Planning -

Culture - Society of Tien Lang district to 2010.

14.Website www.HaiPhong.gov.vn

APPENDIX 1

List of national ranked monuments

STT

Name of the monument

Number, year of decisiondetermine

Location

1

Gam Temple

938 VH/QĐ04/08/1992

Cam Khe Village- Toan Thang commune

2

Doc Hau Temple

9381 VH/QĐ04/08/1992

Doc Hau Village –Toan Thang commune

3

Cuu Doi Communal House

3207 VH/QĐDecember 30, 1991

Zone II of townTien Lang

4

Ha Dai Temple

938 VH/QĐ04/08/1992

Ha Dai Village –Tien Thanh commune

APPENDIX II

STT

Name of the monument

Number, year of decision

Location

1

Phu Ke Pagoda Temple

178/QD-UBJanuary 28, 2005

Zone 1 - townTien Lang

2

Trung Lang Temple

178/QD-UBJanuary 28, 2005

Zone 4 – townTien Lang

3

Bao Khanh Pagoda

1900/QD-UBAugust 24, 2006

Nam Tu Village -Kien Thiet commune

4

Bach Da Pagoda

1792/QD-UB11/11/2002

Hung Thang Commune

5

Ngoc Dong Temple

177/QD-UBNovember 27, 2005

Tien Thanh Commune

6

Tomb of Minister TSNhu Van Lan

2848/QD-UBSeptember 19, 2003

Nam Tu Village -Kien Thiet commune

7

Canh Son Stone Temple

2160/QD-UBSeptember 19, 2003

Van Doi Commune –Doan Lap

8

Meiji Temple

2259/QD-UBSeptember 19, 2002

Toan Thang Commune

9

Tien Doi Noi Temple

477/QD-UBSeptember 19, 2005

Doan Lap Commune

10

Tu Doi Temple

177/QD-UBJanuary 28, 2005

Doan Lap Commune

11

Duyen Lao Temple

177/QD-UBJanuary 28, 2005

Tien Minh Commune

12

Dinh Xuan Uc Pagoda

177/QD-UBJanuary 28, 2005

Bac Hung Commune

13

Chu Khe Pagoda

177/QD-UBJanuary 28, 2005

Hung Thang Commune

14

Dong Dinh

2848/QD-UBNovember 21, 2002

Vinh Quang Commune

15

President's Memorial HouseTon Duc Thang

177/QD-UBJanuary 28, 2005

NT Quy Cao

Ha Dai Temple

Ben Vua Temple

Tien Lang hot spring

div.maincontent .p { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; } div.maincontent p { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; } div.maincontent .s1 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; font-size: 16pt; } div.maincontent .s2 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s3 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s4 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; font-size: 14pt; } div.maincontent .s5 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; font-size: 14pt; } div.maincontent .s6 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s7 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s8 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; vertical-align: 6pt; } div.maincontent .s9 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 12pt; } div.maincontent .s11 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; tex -

Credit risk management for personal loans at Nam A Commercial Joint Stock Bank - Quang Ninh Branch - 13

Credit risk management for personal loans at Nam A Commercial Joint Stock Bank - Quang Ninh Branch - 13 -

Swedish Short-Term Human Resource Forecasting Model

Swedish Short-Term Human Resource Forecasting Model -

Current Status of Credit Risk Management for Individual Customers at Vietnam Technological and Commercial Joint Stock Bank - Thai Nguyen Branch

Current Status of Credit Risk Management for Individual Customers at Vietnam Technological and Commercial Joint Stock Bank - Thai Nguyen Branch

(Source: BIDV Internal Management Department - Nam Thai Nguyen)

The professional quality at the branch is relatively good, the proportion of employees with university and postgraduate degrees always accounts for over 90%. With the characteristics of the industry that always requires highly qualified human resources, BIDV branch - Nam Thai Nguyen branch always constantly improves the qualifications of officers and employees to serve the work well. In allocating human resources to the blocks (excluding department leaders), the number of customer management officers in the business block (working directly in credit development, capital mobilization, customer base growth, etc.) accounts for a gradually increasing proportion over the years, out of the total number of officers working.

The branch's expertise, by the end of 2016, had reached >50%, demonstrating the branch's focus and attention on business human resources.

On the other hand, the very young staff is also the strength of the branch. By the end of 2017, the workforce under 30 years old accounted for 47.5%; from 30 to 40 years old accounted for 35%, from 41 years old and up accounted for only 17.5% - this is a small proportion.

Thus, recruiting young staff and focusing on the quality of human resources for the sales team is one of the top concerns in the bank's strategy. This proves that human resource management activities at the branch are highly focused.

3.1.3. Results of main business activities of BIDV - Nam Thai Nguyen Branch in the period of 2015 - 2017

3.1.3.1. Business environment

The period of 2015-2017 was a period of economic difficulties, the Government directed the implementation of solutions to control inflation, stabilize the macro economy, and ensure social security. The reason must be mentioned that in 2014, the liquidity of the economy was low, leading to many industries being heavily affected, the stock market declined, real estate prices decreased... so although lending interest rates continuously decreased in the last months of the year, financial costs were still relatively high, causing low credit growth and increasing bad debt. By 2015, the world economy had recovered but not sustainably and evenly, inflation tended to decrease. Domestically, the macro economy developed in a positive direction, exchange rates and the foreign exchange market were basically stable, the gold market was stable. Entering the implementation of the 2016 plan, although the province's socio-economic situation has seen significant improvements and changes, there are still shortcomings and difficulties arising from previous years that have not been resolved, causing pressure on production and business such as: inventory, weak purchasing power, high debt ratio, slow recovery of the real estate market, many manufacturing industries facing difficulties due to the impact of the world market, especially the deep decline in oil prices and increasingly fierce domestic competition, causing production and business activities of many enterprises to continue to face difficulties. The output market still faces many difficulties, especially in some industries such as construction materials, real estate, etc. In addition, competition between banks is increasingly fierce.

3.1.3.1. Business performance results

As a new branch operating for more than 4 years in a completely new location, with many difficulties, the initial period was mainly market penetration and customer base design. Moreover, the business environment from 2014 to present has been unfavorable, the financial and monetary market has fluctuated in a complicated and negative direction. However, with the efforts of all officers and employees of the branch together to overcome difficulties, after more than 4 years of operation, the branch has achieved relatively positive results in business activities in general and retail activities of BIDV - Nam Thai Nguyen Branch in particular. The indicators of scale and efficiency all have a good growth rate, basically completing the plan, the indicators of structure and quality have all been achieved and shifted in the right direction of BIDV.

Table 3.2. Business results of BIDV - Nam Thai Nguyen Branch in the period 2015 - 2017

Unit: billion VND

TT

Target | 2015 | 2016 | 2017 | Compare(%) | ||

2016/2015 | 2017/2016 | |||||

1 | Stock capital mobilization | 2410 | 2280 | 2306 | 94,606 | 101,140 |

2 | Loan Sales | 1692 | 2785 | 3050 | 164.6 | 109,515 |

3 | Debt collection turnover | 815 | 2448 | 2591 | 300.4 | 105,842 |

4 | Outstanding loans of securities | 2990 | 3327 | 3786 | 111,271 | 113,796 |

Retail | 743 | 890 | 1086 | 119,785 | 122,022 | |

5 | Profit after tax | 65.44 | 79.05 | 96.13 | 120,798 | 121,607 |

6 | Number of staff | 71 | 75 | 80 | 105,634 | 106,667 |

7 | Average profit per capita | 0.9216 | 1,054 | 1,202 | 114,366 | 114,042 |

8 | Net retail income | 32.64 | 41.83 | 55.21 | 128,156 | 131,987 |

(Source: BIDV - Nam Thai Nguyen Branch Summary Report 2015-2017)

Table 3.3. Proportion of retail credit balance in total outstanding balance in the period 2015 - 2017

Content | Value (billion VND) | Rate (%) | |

2015 | Total credit balance at the end of the period | 2990 | 100 |

Retail debt | 743 | 24.85 | |

2016 | Total credit balance at the end of the period | 3327 | 100 |

Retail debt | 890 | 26.75 | |

2017 | Total credit balance at the end of the period | 3786 | 100 |

Retail debt | 1086 | 28.68 |

Looking at table 3.2, the % comparison column shows the good growth in business results of BIDV - Nam Thai Nguyen Branch. Although only counting from 2015 to now, important indicators such as capital mobilization and outstanding credit have all grown remarkably, bringing stable income to employees. Specifically:

Capital mobilization is the first indicator when considering operating results, and is the premise of the banking business process. Specifically, by the end of 2015, capital mobilization reached 2,410 billion VND. Although 2016 recorded a slight decrease in this indicator, down 5.4% compared to 2015, it still achieved a good capital mobilization level of 2,280 billion VND. At the end of 2017, the total capital mobilization reached an absolute number of 2,306 billion VND, equivalent to a growth of 1.14% compared to 2016. This shows that although there are still many difficulties in building the image and attracting customers because it is a new branch in operation, thanks to the good implementation and diversification of capital mobilization forms such as cumulative deposits, ladders, bonus savings, deposit certificates, flexible interest payment methods... along with the implementation of promotional programs according to BIDV's instructions for depositing customers such as giving insurance cards, gifts, doing well in consulting services and taking care of deposit customers; implementing communication forms to introduce capital mobilization programs and products to organizations and people. Therefore, the capital mobilization results of the branch also achieved relatively good results.

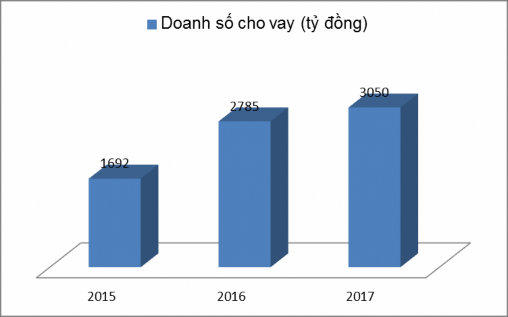

Regarding credit indicators, BIDV - Nam Thai Nguyen Branch has focused on and invested heavily since the establishment of the branch. Sales activities have been focused on and promoted, especially retail credit. Specifically: In general, the loan turnover results after one year of operation increased from 1,692 billion VND in 2015 to 2,785 billion VND in 2016, equivalent to a growth of 64.6%. At the end of 2017, this target reached 3,050 billion VND, equivalent to a growth of 9.5% compared to 2016 and 80.26% compared to 2015.

Figure 3.2: Loan sales chart for the period 2015 - 2017

(Source: Summary report of BIDV - Nam Thai Nguyen Branch, period 2015 - 2017)

Debt collection revenue also recorded a sharp increase in 2016 with a growth rate of over 200% compared to 2015. And by 2017, this indicator also achieved a slight increase (up 5.84%) compared to 2016.

Proportional to the growth in loan sales, the outstanding credit balance at the end of the period also recorded good growth over 3 years, specifically at the end of 2016, it grew by 11.27% compared to 2015, raising the outstanding credit balance target to 3,327 billion VND, in 2017 it grew by 13.79% compared to 2016, officially reaching 3,786 billion VND. Contributing to that growth is the growth in retail outstanding balance. Specifically, as follows:

After one year of operation, this target reached 890 billion VND in 2016, equivalent to a growth of 19.78% compared to 2015. By the end of 2017, this target reached 1,086 billion VND, equivalent to a growth of 22.02% compared to 2016 and 46.16% compared to 2015. On the other hand, according to table 3.3, the proportion of retail debt in total credit balance increased from 24.85% in 2015 to 26.75% in 2016 and reached 28.68% in 2017. The increase in both absolute and relative numbers shows that the positive development direction of retail credit products in the area has initially helped banks expand the market. In addition, the increased demand for capital of economic sectors in the region shows that BIDV - Nam Thai Nguyen Branch has favorable and flexible policies on interest rates, collateral conditions, loan procedures, etc., helping the branch to increasingly expand its credit scale.

Pre-tax profit has continuously increased over the years, reaching 96.13 billion VND in 2017, equivalent to an increase of 21.6% compared to 2016, showing that labor productivity has always improved over the years. An important indicator to evaluate the life and income of officers and employees is the average pre-tax profit per capita, this indicator at the branch has always achieved significant growth, reaching 1.2 billion VND at the end of 2017, an impressive figure, contributing to BIDV - Nam Thai Nguyen Branch being in the top of the most effective branches in the Northern mountainous region according to BIDV's ranking results (2017). The above indicator also contributes to showing that the life of officers and employees of the branch is cared for and taken care of carefully, which will help motivate officers to work with peace of mind and contribute more to the agency.

Despite the difficult business environment, with the synchronous implementation of solutions from the State Bank of Vietnam and the economic development policy of Thai Nguyen province, closely following the business orientation of the Joint Stock Commercial Bank for Investment and Development of Vietnam, Nam Thai Nguyen branch has continued to maintain growth momentum, achieved encouraging results, increasingly affirmed its position and created a premise for the branch's business activities in the following years.