Assume that there are N MFIs. Each MFI will have m output factors and n input factors. Then, the technical efficiency of each MFI is determined as follows:

∑ 𝑚

𝑢𝑖𝑦𝑖𝑠

𝑇𝐸 =𝑖=1

∑

𝑛

𝑗=1

𝑣𝑗𝑥𝑗𝑠

Where, 𝑦 𝑖𝑠 is the quantity of the i-th output of the s-th MFI, 𝑥 𝑗𝑠 is the quantity of the j-th input of the s-th MFI, u i is the weight of the output and v j is the weight of the input. The technical efficiency TE is maximized to find the output and input weights with the condition

∑ 𝑚

𝑢𝑖𝑦𝑖𝑟

𝑖=1≤ 1, 𝑟 = ̅ 1 ̅ , ̅̅ 𝑁 ̅

∑

𝑛

𝑗=1

𝑣𝑗𝑥𝑗𝑟

𝑢 𝑖 ≥ 0, 𝑣 𝑖 ≥ 0

The conditions are to ensure that the technical efficiency TE does not exceed 1, and at the same time, the input and output weights are non-negative.

However, the above linear programming problem will have multiple solutions. To solve this problem, Chames, Cooper and Rhodes (1978) added the condition:

𝑛

∑ 𝑣 𝑗 𝑥 𝑗𝑠 = 1

𝑗=1

Therefore, the above equation can be transformed into a new linear programming problem as follows:

Provided:

𝑚

𝑀𝑎𝑥 𝑢𝑣 𝑇𝐸 = ∑ 𝑢 𝑖 𝑦 𝑖𝑠

𝑖=1

𝑛

∑ 𝑣 𝑗 𝑥 𝑗𝑠 = 1

𝑗=1

𝑚 𝑛

∑ 𝑢 𝑖𝑦 𝑖 𝑟 − ∑ 𝑣 𝑗 𝑥 𝑗 𝑟 ≤ 0, 𝑟 = 1 ̅ ̅, ̅ ̅𝑁 ̅

𝑖=1

𝑗=1

𝑢 𝑖 ≥ 0, 𝑣 𝑗 ≥ 0; ∀𝑖, 𝑗

The technical efficiency obtained in this case is constant technical efficiency to scale (CRS).

𝑗=1

When the condition ∑ 𝑛 𝑣 𝑗 𝑥 𝑗𝑠 ≠ 1 , the technical efficiency obtained in this case is

is variable technical returns to scale (VRS).

The scale efficiency index to evaluate the performance of MFI is calculated according to the following formula:

𝑆𝐸 =

𝑇𝐸 𝐶𝑅𝑆

𝑇𝐸 𝑉𝑅𝑆

In which, 𝑇𝐸 𝐶𝑅𝑆 is constant technical efficiency with scale, 𝑇𝐸 𝑉𝑅𝑆 is variable technical efficiency with scale.

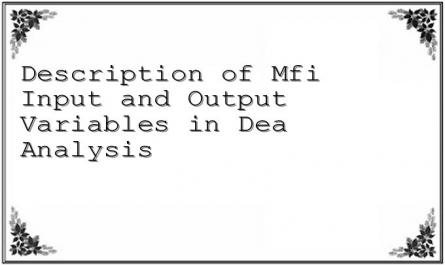

In this study, to evaluate the performance of Vietnamese MFIs, the author selects input factors and output factors of MFIs based on previous studies, specifically:

The input variables selected according to the research of Sufian (2006), Ferdousi (2013), Bolli et al. (2012) include the following 02 variables:

-Operating expenses: include interest expenses on deposits and equivalents, employee salary expenses, and non-interest expenses.

- Number of employees: includes all employees working at MFI.

The output variables selected according to Ferdousi's (2013) study include 2 variables reflecting the performance of MFIs as follows:

- Total outstanding loans: includes all outstanding loans of customers.

- Number of borrowers: includes all customers with outstanding loans at the bank.

MFI.

Table 3.1. Description of MFI input and output variables in DEA analysis

Variable

Define | Unit | |

Input variables | ||

Operating costs | Interest expense on deposits and equivalents, employee salary expenses, non-interest expenses | VND |

Maybe you are interested!

-

Discussion of Quantitative Research Results on the Impact of Control Variables on Financial Performance

Discussion of Quantitative Research Results on the Impact of Control Variables on Financial Performance -

Foreign Exchange Services and Investment Operations of Credit Institutions in the Financial Market

Foreign Exchange Services and Investment Operations of Credit Institutions in the Financial Market -

Assessment of the Reliability of the Scale “Pressure from Government, Importers, Investors, Financial Institutions, Community on Environmental Information”

Assessment of the Reliability of the Scale “Pressure from Government, Importers, Investors, Financial Institutions, Community on Environmental Information” -

Developing rural financial institutions in Vietnam - 1

Developing rural financial institutions in Vietnam - 1 -

Input and Output Nutritional Sources of Nutritional Balance

Input and Output Nutritional Sources of Nutritional Balance

Number of employees

All employees working at MFI | People | |

Output variable | ||

Total outstanding loans | All outstanding customer loans | VND |

Number of borrowers | All customers with outstanding debt at MFI. | People |

Source: author's research

3.2.2. Method of evaluating factors affecting the performance of microfinance institutions in Vietnam

To assess the factors affecting the performance of microfinance institutions in Vietnam, the author builds a research model based on the main research model of Abdulai & Tewari (2017) combined with factors in the research of Dao Lan Phuong & Le Thanh Tam (2017), Ngo (2015) and Ngo et al. (2014). The general research model of the topic is as follows:

Model (1):

OSS it = β 0 + β 1 OSS it-1 + β 2 AGE it + β 3 CPB it + β 4 OEA it + β 5 DER it + β 6 PAR30 it + β 7 NAB it + β 8 GLP it + v i + u it

Model (2):

ROA it = β 0 + β 1 ROA it-1 + β 2 AGE it + β 3 CPB it + β 4 OEA it + β 5 DER it + β 6 PAR30 it

+ β 7 NAB it + β 8 GLP it + v i + u it Model (3):

ROE it = β 0 + β 1 ROE it-1 + β 2 AGE it + β 3 CPB it + β 4 OEA it + β 5 DER it + β 6 PAR30 it

+ β 7 NAB it + β 8 GLP it + v i + u it Model (4):

TE it = β 0 + β 1 TE it-1 + β 2 AGE it + β 3 CPB it + β 4 OEA it + β 5 DER it + β 6 PAR30 it + β 7 NAB it + β 8 GLP it + v i + u it

Model (5):

SE it = β 0 + β 1 SE it-1 + β 2 AGE it + β 3 CPB it + β 4 OEA it + β 5 DER it + β 6 PAR30 it + β 7 NAB it + β 8 GLP it + v i + u it

In there:

Dependent variables: OSS is the level of operational self-sustainability, ROA is the net income on total assets, ROE is the net income on equity, TE is the index of technical efficiency and SE is the index of scale efficiency. These are the indicators used to assess the efficiency of MFIs in this study. The indicators usually refer to the ability of MFIs to continuously implement microfinance programs in pursuit of their regulatory objectives (Abdulai & Tewari, 2017; Dao Lan Phuong & Le Thanh Tam, 2017; Ngo, 2015).

The independent variables include: AGE (MFIs' age) is the age of MFIs, CPB (Cost per borrower) is the cost per borrower, OEA (Operating expense to assets ratio) is the ratio of operating expenses to total assets, DER (Debt to equity ratio) is the ratio of equity to total assets, PAR30 (Portfolio at risk) is the risk ratio of the portfolio, NAB (Number of active borrowers) is the number of real borrowers, GLP (Gross loan portfolio) is the total loan portfolio.

In addition, v i is an unobservable characteristic of MFI, u it is the specific error.

3.2.3. Method of assessing the impact of women's empowerment on the performance of microfinance institutions in Vietnam

To assess the impact of women's empowerment on the performance of microfinance institutions in Vietnam, the author added to the above research models the independent variable PFB representing women's empowerment measured by the total number of women borrowers over the total number of MFI borrowers. The research model has the following form:

Model (6):

OSS it = β 0 + β 1 OSS it-1 + β 2 AGE it + β 3 CPB it + β 4 OEA it + β 5 DER it + β 6 PAR30 it + β 7 NAB it + β 8 GLP it + β 9 PFB it + v i + u it

Model (7):

ROA it = β 0 + β 1 ROA it-1 + β 2 AGE it + β 3 CPB it + β 4 OEA it + β 5 DER it + β 6 PAR30 it

+ β 7 NAB it + β 8 GLP it + β 9 PFB it + v i + u it Model (8):

ROE it = β 0 + β 1 ROE it-1 + β 2 AGE it + β 3 CPB it + β 4 OEA it + β 5 DER it + β 6 PAR30 it

+ β 7 NAB it + β 8 GLP it + β 9 PFB it + v i + u it Model (9):

TE it = β 0 + β 1 TE it-1 + β 2 AGE it + β 3 CPB it + β 4 OEA it + β 5 DER it + β 6 PAR30 it + β 7 NAB it + β 8 GLP it + β 9 PFB it + v i + u it

Model (10):

SE it = β 0 + β 1 SE it-1 + β 2 AGE it + β 3 CPB it + β 4 OEA it + β 5 DER it + β 6 PAR30 it + β 7 NAB it + β 8 GLP it + β 9 PFB it + v i + u it

The way the variables are measured, their sign expectations, and the basis for the proposed variables are presented in the following table:

Table 3.2. Description of variables used in the model

Variable name

Symbol | Measure | Expected sign | Citation basis | |

Dependent variable | ||||

Self-sustainable in operations | OSS | Operating income x100% Total operating costs | Schäfer and Fukasawa (2011), Dissanayake (2014), Ngo (2015), Dao Lan Phuong and Le Thanh Tam (2017), Abdulai and Tewari (2017) | |

Return on assets | ROA | Net income x100% Total assets | Dissanayake (2014), Abdulai and Tewari (2017) | |

Return on equity | ROE | Net income x100% Total equity | Dissanayake (2014), Abdulai and Tewari (2017) | |

Technical efficiency | TE | Calculated from DEA analysis | ||

Efficiency of scale

SE | Calculated from DEA analysis | |||

Independent variable | ||||

Women empowerment | PFB | Total number of women borrowers Total number of borrowers | + | Abdulai & Tewari (2017), Lopatta et al. (2017) |

Equity to total assets ratio | DER | Total equity Total assets | + | Ngo (2015), Dao Lan Phuong and Le Thanh Tam (2017) |

Total loan portfolio | GLP | Ln(Total loan portfolio adjusted for write-offs) | + | Abdulai and Tewari (2017) |

Portfolio risk ratio | PAR30 | Net Losses/Total Loans Outstanding | - | Schäfer and Fukasawa (2011), Dao Lan Phuong and Le Thanh Tam (2017), Abdulai and Tewari (2017) |

Growth in Borrowers | NAB | Ln(Total number of borrowers) | + | Schäfer and Fukasawa (2011), Ngo (2015), Abdulai and Tewari (2017), |

real

Operating Expenses to Total Assets Ratio | OEA | Total operating expenses Total assets | - | Dissanayake (2014), Abdulai and Tewari (2017) |

Cost per Borrower | CPB | Ln(Total operating expenses/Total number of borrowers) | - | Schäfer and Fukasawa (2011), Dissanayake (2014), Ngo (2015), Abdulai and Tewari (2017), |

Age of microfinance institutions | AGE | Number of years of operation of microfinance institutions at the time of study | + | Dao Lan Phuong and Le Thanh Tam (2017), Abdulai and Tewari (2017) |