- 38 -

- The profit or loss of the joint venture or associate investment is accounted for using the equity method;

- Any income or expense arising from the difference between the carrying amount before reclassification and the fair value at the reclassification date (as defined in IFRS 9- Financial Instruments ) when a financial asset is reclassified to be measured at fair value;

Maybe you are interested!

-

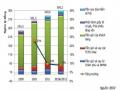

Business Results for the Period 2009-June 30, 2012 According to Consolidated Financial Statements According to Vietnamese Accounting Standards.

Business Results for the Period 2009-June 30, 2012 According to Consolidated Financial Statements According to Vietnamese Accounting Standards. -

Applying international accounting standards to perfect the corporate financial reporting system in Vietnam conditions - 20

Applying international accounting standards to perfect the corporate financial reporting system in Vietnam conditions - 20 -

Completing the work of auditing cash capital in auditing financial statements performed by An Phat Auditing and Accounting Consulting Co., Ltd. - 13

Completing the work of auditing cash capital in auditing financial statements performed by An Phat Auditing and Accounting Consulting Co., Ltd. - 13 -

Presentation of Inventory Accounting Information on Financial Statements

Presentation of Inventory Accounting Information on Financial Statements -

Methods Used In Analyzing Corporate Financial Statements

Methods Used In Analyzing Corporate Financial Statements

- Tax costs; and

- Total value of interrupted business operations.

Information on other comprehensive income , defined in IAS 1 (2012) at paragraph 7, includes:

- Changes in asset revaluation surplus (as defined in IAS 16 -

Property, plant and equipment and IAS 38 - Intangible assets );

- Reassessment of the value of benefit plans (as prescribed in IAS 19-

Employee benefits );

- Gains and losses arising from the translation of financial statements of foreign operations (as prescribed in IAS 21 - Effects of changes in foreign exchange rates );

- Gains and losses from investments in equity instruments are determined at fair value through other comprehensive income (as prescribed in IFRS 9- Financial Instruments );

- The gains and losses recognised for cash flow hedging instruments (as defined in IAS 39 - Financial Instruments: Recognition and Measurement );

- The portion of changes in fair value due to changes in credit risk of debt obligations for specific debt obligations determined at fair value through profit or loss (as prescribed in IFRS 9- Financial Instruments ).

Enterprises should present expenses recognized in the profit and loss statement in a classification based on the nature or function of the expense, so that it provides more reliable and relevant information. Expenses are classified in more detail to clarify the components of business results that may differ in frequency, in expected profit or loss and predictability. Other comprehensive income should be presented in different lines reflecting the value of other comprehensive income earned during the period, which are

- 39 -

Classification based on nature (IASB, 2012a).

(3) Statement of changes in equity

The statement of changes in equity provides information on changes in the enterprise's equity, reflecting the increase or decrease in the value of net assets during the period, including the following information:

- Total consolidated profit for a period, presenting separately the portion attributable to the owners of the parent company and minority shareholders;

- The effect of retrospective application or retrospective adjustment on each component of equity, as required by IAS 8- Accounting Policies, Changes in Accounting Estimates and Errors ; and

- Reconcile the beginning and ending values for each component of equity and separately explain the changes arising from:

+ Profit and loss (business operations);

+ Other comprehensive income; and

+ Transactions with the owners of the enterprise as owners, clearly presenting the value of the owner's contribution and the value distributed to the owners and changes in the ownership ratio of the owner in the subsidiaries that do not lead to loss of control.

An enterprise shall present either in the statement of changes in equity or in the notes to the financial statements the amount of dividends recognised as distributions to owners during the period.

Thus, the change in the owner's equity of an enterprise from the beginning to the end of the reporting period represents the increase or decrease in net assets during the period. Except for changes resulting from transactions with owners in their capacity as owners (such as capital contributions, repurchases of shares of the entity and dividends) and transaction costs directly related to these transactions, the statement of changes in owner's equity during the period presents the total income and expenses, including other income and expenses, generated from the activities of the enterprise during the period (IASB, 2012a).

(4) Cash flow statement

The statement of cash flows provides a basis for users to assess the ability of an enterprise to generate cash and cash equivalents and the need to use them.

- 40 -

use of these cash flows of the enterprise. IAS 7 - Statement of Cash Flows (2012) presents the IASB's regulations on presentation and disclosure of cash flow information.

The statement of cash flows “presents cash flows during a period classified into operating, investing and financing activities” (IASB, 2012b, p.10).

Cash flow from operating activities is the cash flow arising from the main revenue-generating activities of an enterprise or other activities that are not investing or financing activities. Cash flow from operating activities “is an important indicator to determine the level of business activities, assess the ability to generate cash to pay debts, maintain operations, pay dividends, and carry out new investment activities without resorting to external sources of funding” (IASB, 2012b, p.13).

An enterprise can present cash flows from operating activities using one of two methods: the direct method or the indirect method.

Cash flows from investing activities are cash flows arising from the acquisition or disposal of long-term assets and other investments. Disclosure of cash flows from investing activities separately is important because it reflects the size of investments that generate future income and cash flows.

IAS 7 (2012) presents some contents of cash flows from investing activities, including: cash spent on purchasing or cash received from selling fixed assets and other long-term assets; cash spent on lending and purchasing debt instruments; cash recovered from loans or selling debt instruments; cash received and paid from futures contracts, forward contracts, option contracts (except contracts for commercial purposes)...

Cash flows from financing activities are cash flows arising from activities that change the size and composition of equity and debt capital, related to the mobilization and repayment of external resources. The separate disclosure of cash flows from financing activities is important because it is useful for assessing the trend of funding cash flows from capital providers to the enterprise.

IAS 7 (2012) covers some aspects of cash flows from operating activities.

- 41 -

finance, including:

- Proceeds from the issuance of shares or other equity instruments;

- Payments to owners;

- Proceeds from issuance of bonds, debentures and other short-term or long-term loans;

- Payment of debts; and

- Payment of financial lease debt.

(5) Notes to financial statements

According to IAS 1 (2012), paragraph 112, Notes to financial statements aim at the following objectives:

- Present information on the basis for preparing the financial statements and the accounting policies used;

- Disclose any information required by international financial reporting standards that is not presented in the financial statements; and

- Provide additional information that is not presented in the financial statements but is considered relevant for a better understanding of them.

The notes to the financial statements should be presented in a systematic manner. Each item in the Statement of Financial Position, Statement of Comprehensive Income, Statement of Changes in Equity and Statement of Cash Flows should be marked to refer to the relevant information in the Notes to the Financial Statements (IASB, 2012a).

According to IAS 1 (2012), paragraph 114, in order to assist users in comparing with the reports of other enterprises, the notes to the financial statements should be presented in the following order:

- Report on compliance with international financial reporting standards;

- Summarize the significant accounting policies applied, including: the valuation basis used in preparing the financial statements and other accounting policies that are considered appropriate for understanding the financial statements;

- Details of the items presented in the Statement of Financial Position, Statement of Profit and Loss and Other Comprehensive Income, Statement of Changes in Equity, and Statement of Cash Flows, in the order in which they are presented in the statements; and

- Other announcements, including:

- 42 -

+ Contingent liabilities, contractual commitments not yet recorded; and

+ Non-financial disclosures, for example, the enterprise's financial risk management objectives and policies...

In addition, according to paragraphs 125 to 138 of IAS 1 (2012), the following contents must also be disclosed in the notes to the financial statements: information about assumptions about the future and the main basis for the uncertainty of the estimates made at the end of the reporting period when these assumptions or estimates have a high risk of causing material adjustments to the recorded value of assets and liabilities in the next financial year; information that allows users of the financial statements to evaluate the enterprise's capital management objectives, policies and processes; financial instruments with repurchase rights classified as equity instruments; detailed information about dividends.

1.3.2.2. Corporate financial statements in the US, France and China

(1) Financial statements of enterprises in the US

The United States is a country with a high level of economic development, the main source of financial supply is from the stock market, and the legal system is based on common law (Choi and Meek, 2011).

The US accounting system is based on a theoretical framework issued in the form of financial accounting concepts (SFAC) and financial accounting standards (SFAS). Financial accounting concepts and standards are issued by FASB (Financial Accounting Standards Board ), an independent private organization established in 1973, recognized and supported by SEC ( Securities and Exchange Commission ). As of June 2012, FASB has issued 8 financial accounting concepts and 9 sets of accounting standards (summarized by topic on the basis of 168 financial accounting standards) ( Appendix 03 ) .

The Sarbanes-Oxley Act (2002) of the United States significantly expanded the requirements for corporate governance, the regulations of the accounting and auditing profession, information disclosure and reporting, in which, compliance with generally accepted accounting principles (GAAP) is considered the "test" of fair presentation . GAAP includes all accounting standards, laws and regulations to be respected when drafting financial statements. FASB and SEC are also considering moving from rules-based standards to principles-based standards.

- 43 -

in presenting and publishing financial statements (Choi and Meek, 2011).

FASB identifies seven elements to be presented on the financial statements of both for-profit and non-profit organizations: “assets, liabilities, equity/net assets, revenues, expenses, other income, and other expenses” and three elements for for-profit organizations only: “owners' investments, distributions to owners, and comprehensive income” (FASB, 2008).

The US annual financial statements system (for large enterprises) includes:

- Management report;

- Independent auditor's report;

- Basic financial statements: Balance sheet, Income statement, Comprehensive income statement, Cash flow statement, Statement of changes in equity...;

- Report discussing and analyzing performance and financial situation;

- Announce accounting policies that have significant impact on financial statements;

- Financial statement explanation;

- Comparative financial data report (selected) for 5 or 10 years;

- Quarterly reports (selected).

Consolidated financial statements are mandatory, the consolidation rules require that all subsidiaries are fully consolidated. Quarterly financial statements are mandatory for listed companies but audits are not required for these reports.

(2) French corporate financial statements

At the heart of the French accounting system is the General Accounting Scheme (PCG), a unified accounting system that includes accounting principles, a chart of accounts, financial statement templates, special cases, consolidated reporting methods, and management accounting guidelines. The French National Council of Accountancy (CNC) and the Accounting Regulation Committee (CRC) are tasked with overseeing the implementation and proposing improvements to the PCG. In 2009, the French Accounting Standards Authority (ANC) was created, replacing the CNC and CRC, with the main function of setting accounting standards in the form of regulations for the private sector.

The French financial reporting system includes:

- Balance sheet ;

- Income statement ;

- 44 -

- Notes to financial statements ;

- Directors' report ;

- Auditor 's report .

French commercial law allows for simplified financial reporting for small and medium-sized enterprises; there are no mandatory requirements for the Statement of Changes in Financial Position and the Statement of Cash Flows. However, the CNC requires large enterprises to prepare four additional reports: Statement of Cash Position, Statement of Cash Flows, Income Statement, and Business Plan. Listed enterprises must prepare interim reports and Environmental Performance Reports (Choi and Meek, 2011).

A characteristic of French corporate financial statements is the requirement for extensive and detailed disclosure of notes and notes… Another important feature is that the French corporate financial reporting system places great importance on environmental reporting and social responsibility. A social responsibility report is a requirement for all companies with 300 or more employees. This report describes, analyzes, and reports on training issues, labor relations, health and safety conditions, wages and other job benefits, working environment… Listed companies also prepare environmental reports (on consumption, saving of raw materials, water, energy; waste treatment, noise, and related costs; provisions for environmental risks, etc.) (Choi and Meek, 2011).

(3) Financial statements of Chinese enterprises

The Chinese Accounting Law assigns the Ministry of Finance the responsibility for setting accounting standards and related accounting regulations. In 1992, the Ministry of Finance issued the Accounting Standards for Enterprises (ASBE). In 1998, the Accounting Standards Committee (CASC) was established under the Ministry of Finance to develop standards. In 2003, the CASC was restructured to include 26 members appointed by the Ministry of Finance from government agencies, academia, professional organizations, and the business community. However, the decision to issue accounting standards still rests with the Ministry of Finance. To date, the Chinese Accounting Standards for Enterprises (ASBE) system includes one basic standard and 38 accounting standards that apply to all listed companies in China.

- 45 -

China's periodic financial reporting system is implemented according to the calendar year, including:

- Balance sheet;

- Profit report;

- Cash flow statement;

- Report on changes in equity;

- Financial statement explanation.

Notes to financial statements are required to disclose information on asset depreciation; changes in capital structure; profit allocation; business segments; accounting policies; provisions, important events after the end of the fiscal year, etc.

Financial statements must be expressed in Chinese yuan. Annual financial statements must be audited. Quarterly financial statements are required for listed companies. Listed companies must assess their internal controls and hire external auditors to assess the control system and provide an opinion on the report.

1.3.3. Comments on the Content of Financial Reports

After studying the general content of the financial statement system according to the regulations of IASB and some countries representing some accounting schools in the world, the thesis draws some comments as follows:

First, there is a certain similarity in the structure of financial reporting systems in general.

Accordingly, the financial reporting system is based on 5 basic reporting forms, including: Balance Sheet, Profit and Loss Report, Equity Change Report, Cash Flow Report and Notes to Financial Statements, to provide information to users, in accordance with national characteristics and in harmony with the international integration trend.

Second, there are differences in information provision trends and differences in the depth and breadth of information among countries of different schools.

- IASB: does not impose a fixed format for reports; reports are aimed at investors, lenders, and other creditors.

- US: In addition to not imposing a fixed format for reports, the report