Hue branch. All these factors are significant in the model and have a positive impact on the loan quality of the bank, as the regression coefficients are all positive.

The regression equation shows the quality of consumer loans of Vietcombank - Hue Branch as follows:

CL = 3.41 + 0.523STC + 0.31SCT + 0.244NLPV + 0.348KNDU + 0.262SHH

Based on the regression model of factors affecting the quality of consumer loans of Vietcombank - Hue Branch, it can be seen that the coefficient β 1 = 0.523 means that when Factor 1 changes by 1 unit while other factors remain unchanged, the quality of consumer loans of Vietcombank - Hue Branch also fluctuates in the same direction by 0.523 units. For Factor 2, the coefficient β 2 = 0.31 also means that when Factor 2 changes by 1 unit, the quality of consumer loans of the bank also changes in the same direction by 0.31 units. The same explanation applies to the remaining variables (in case the remaining factors remain unchanged).

Thus, based on the regression analysis results that I conducted above, it can be seen that the Trust factor has the greatest impact on the quality of consumer loans of Vietcombank - Hue Branch with coefficient β 1 = 0.523. Commenting on this phenomenon, through the survey, nearly 70% choose banks to borrow consumer loans because of the bank's reputation and interest rates. According to experts, "commercial banks target customers who already have deposits, bank accounts... low risk level, so the lending interest rate is lower than other financial institutions" (Ms. Nguyen Thu Ha, former Deputy General Director of Vietcombank). Moreover, commercial banks always publicly list clear and transparent interest rates to facilitate customers to make accurate decisions, customers will feel confident when using services at the bank.

2.2.2.2.4 Description of customer assessment of service quality at VCB Hue Bank

To know the quality of CVTD of customers, analyze the average value of each group of factors extracted in the above section. The results of the average value assessment are presented in the following table:

Table 2.9: Results describing the assessment of customer service quality at the bank by average value

Types of factors

Central jar | Short best | High best | |

1. Trust | 3,408 | 1,750 | 5 |

2. Empathy | 3,449 | 1,750 | 5 |

3. Service capacity | 3,302 | 1,333 | 5 |

4. Responsiveness | 3,481 | 1,667 | 5 |

5. Tangibility | 3,330 | 1,667 | 5 |

6. Quality | 3,410 | 2 | 5 |

Maybe you are interested!

-

Solutions to improve the quality of consumer lending activities at Vietnam Prosperity Joint Stock Commercial Bank - 2

Solutions to improve the quality of consumer lending activities at Vietnam Prosperity Joint Stock Commercial Bank - 2 -

Consumer lending quality at Vietnam Prosperity Joint Stock Commercial Bank - Northern Consumer Lending Center - 10

Consumer lending quality at Vietnam Prosperity Joint Stock Commercial Bank - Northern Consumer Lending Center - 10 -

Improving the quality of financial appraisal of investment projects in medium and long-term lending at the Military Commercial Joint Stock Bank, Hoang Quoc Viet branch - 14

Improving the quality of financial appraisal of investment projects in medium and long-term lending at the Military Commercial Joint Stock Bank, Hoang Quoc Viet branch - 14 -

Evaluation of the quality of savings deposit services for individual customers at Dong A Commercial Joint Stock Bank - Hue Branch - 14

Evaluation of the quality of savings deposit services for individual customers at Dong A Commercial Joint Stock Bank - Hue Branch - 14 -

Improving the quality of financial appraisal of investment projects in medium and long-term lending at the Military Commercial Joint Stock Bank, Hoang Quoc Viet Branch - 2

Improving the quality of financial appraisal of investment projects in medium and long-term lending at the Military Commercial Joint Stock Bank, Hoang Quoc Viet Branch - 2

(Source: Data processing results on SPSS software )

Looking at the table above, it can be initially observed that the overall customer assessment of the bank's service quality is above average, with the corresponding mean value being 3.410.

However, to have the most detailed and accurate assessment of the quality of CVTD of the bank, it is necessary to rely on the above table to analyze more deeply into the factors affecting the quality of CVTD of the bank. For example, for factors such as Trust , Sympathy , Responsiveness , the general assessment of customers for the quality of CVTD is at the highest level, the average value is 3.408; 3.449; 3.481 respectively. This shows that the bank always puts customers' trust in the bank high, besides that, listening to opinions and sharing with customers to best meet customers' needs is also a top priority for the bank.

Thus, the results of the analysis of the average value of each group of factors partly give us an overall view of the factors affecting the quality of consumer loans at VCB Hue. In general, these results are also quite consistent with the regression model that I analyzed in the above section.

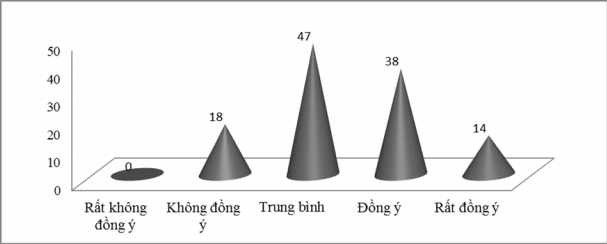

According to statistics on the level of agreement with the quality of consumer loans of banks, 14 customers (equivalent to 11.79%) rated as "Strongly agree" with the quality of CVTD of banks, followed by the level of "Agree" with 38 customers (equivalent to

with 32.48%). The level of “Average” with 47 people (40.17%). This shows that the quality of consumer loans of the Bank for Foreign Trade of Vietnam, Hue Branch, is satisfactory to the majority of customers.

Figure 2.11 Describes customers' assessment of the quality of CVTD at the bank.

However, there are still customers who are not satisfied with the quality of CVTD of the bank, with up to 18 people "Disagree" corresponding to 15.38%, at the same time the number of customers who said they were very satisfied is not higher than this number. Therefore, VCB Hue Bank needs to have appropriate solutions to develop the quality of consumer loans.

CHAPTER 2 SUMMARY

The quality of consumer loans of Joint Stock Commercial Bank for Foreign Trade of Vietnam, Hue Branch in the period 2009-2013 is evaluated from two perspectives:

From the bank's perspective , the quality of CVTD of VCB-Hue is gradually improving. This is clearly shown in the high increase in loan turnover over the past 5 years, the overdue debt ratio except for 2009, the bank has always controlled it at the allowed level, proving that this activity at the bank is always strictly controlled.

Customers rate the quality of the bank's customer service as above average, most customers trust this service of the bank, and highly appreciate the bank's responsiveness and sympathy towards customers.

CHAPTER 3

RECOMMENDATIONS TO IMPROVE THE QUALITY OF CONSUMER LOANS AT THE JOINT STOCK COMMERCIAL BANK FOR FOREIGN TRADE OF VIETNAM, HUE BRANCH

3.1 GROUP OF SOLUTIONS ON CONSUMER LENDING PROCESS

3.1.1 Improve the system of processes, regulations, and CVTD products to suit individual customers.

Competition between commercial banks is fierce, customers have many choices of banks to borrow from. This is very disadvantageous for state-owned banks with many procedures and regulations for lending, while joint-stock banks have very open lending policies, so they have a high proportion of CVTD (over 50% of total outstanding loans). Therefore, in order to compete with joint-stock banks in CVTD products, banks are constantly improving their lending processes and regulations in a direction that is suitable for customers. Meanwhile, for borrowers, especially small businesses, business households and individuals, there are the following characteristics:

Knowledge of law in general and banking in particular is very limited, so when faced with bank requests for information, people often feel hesitant and uncomfortable.

Due to the backward legal system and administrative management system of our country, most businesses declare false taxes and unclear income, so they often have the mentality of concealing personal information and only want the loan procedure to be as simple as possible.

Thus, the gap between the needs of borrowers and banks always exists. Therefore, identifying the factors that affect customers' borrowing decisions is very necessary to approach customers and create a lending process regulation suitable for individual customers, open enough to meet the needs of borrowers but also enough to protect the interests and capital safety of the bank against credit risks.

According to a financial expert, the difference in price (interest rate) of banking services will gradually disappear, instead competition in service quality will be the main focus.

weak. Competition in CVTD products, the issue of interest rates is increasingly not much different between banks and is becoming more and more important in the choice of borrowers, borrowers will choose the service where has the fastest service time, simple procedures, diverse products to choose from and effective financial advice.

In order to speed up customer service time, it is necessary to regulate the time limit for each type of business in each stage of implementation, there must be smooth coordination between departments and divisions involved in credit work, there must be mutual support, all for the development goal of the Bank. Eliminate the idea of passing responsibility or causing conflicts with each other, affecting work efficiency. To do this, the process should have a clear demarcation of the authority and responsibility of each department because the lending process includes many departments involved. Avoid general regulations such as two departments coordinating to handle a certain stage, which will lead to a situation of dependence and passing responsibility.

Simplifying paperwork and speeding up the processing time must go hand in hand with risk management and minimization, so it is necessary to develop a specific and clear method for effective consumer loan management:

Maintain regular contact with customers: The regulation that credit officers must regularly contact customers (on average once a month) is an effective way to get information about the customer's financial situation (such as whether there are any changes in employment, what is their position, work address, etc. in the case of business, how are production and business activities progressing), information about residence, family relationships, etc. When credit officers notice warning signs that are detrimental to the customer's ability to repay debts or may affect the value of collateral, credit officers should report to the Leader to find solutions to prevent the situation of inability to repay bank loans.

Regulations require credit officers to periodically re-evaluate collateral assets every 3, 6 or 12 months depending on the type of collateral. If the asset value decreases, the customer must be required to provide additional collateral or reduce the outstanding loan balance to ensure credit safety for the Bank.

Implement a safe loan management policy, limit risks: for consumer loans with collateral (depending on the product), customers should be asked to buy property damage insurance during the loan period, the beneficiary is the bank. The more the economy develops and becomes more modern, the more attention is paid to the insurance sector. People come to insurance to compensate for future losses when an unfortunate risk occurs. In the banking sector, for deposit activities, credit institutions in general and banks in particular have purchased insurance. However, in the lending sector, there are still limitations, banks need to expand the requirements for customers to participate in insurance. This is also a way for banks to transfer part of the credit risk to the insurance company. For unsecured loans, customers should be encouraged and advised to buy insurance. For example, life insurance: Credit security of Vietcombank Cardif Life Insurance Company Limited. When an insurance risk occurs (the borrower dies), the insurance company will compensate the bank with an insurance amount equal to the debt (including principal and interest) that the customer still owes. If there is any remaining money, it will be returned to the relatives of the borrower (the deceased). This type of insurance product is humane, reducing the debt burden for the family of the victim, and on the other hand, ensuring credit safety for the bank.

Strengthening internal control: In recent times, the bank has effectively overcome lending violations, minimizing risks and losses, ensuring safe operations, with significant contributions from the internal inspection and control department. During the inspection process, shortcomings, loopholes, and irrationalities in the operating mechanism or activities that violate the law and regulations of the industry have been promptly detected, advising leaders to direct the correction of shortcomings and weaknesses, preventing violations and risks of loss, and helping leaders to plan good business strategies, contributing to putting credit activities in order. At the same time, checking the debt classification of the customer department to calculate risk provisions.

3.1.2 Adjusting some regulations of the bank's current CVTD products

Regarding the issue of receiving collateral and valuing collateral:

For real estate assets : it is necessary to create real estate products and services to have a specialized department to perform brokerage and intermediary services in real estate transactions.

Real estate combines specialized appraisal of mortgaged assets to ensure that the valuation is close to the market, ensuring a clear assessment of liquidity and the ability to handle assets in the worst case scenario.

It is recommended to establish an internal information page within the entire bank in parallel with the open information pages to widely publicize in detail the collateral assets that are allowed to be processed for debt recovery. This can be seen as a dual solution, both helping the bank to process bad debt recovery and being the link between supply and demand of assets, prioritizing timely response to the need to find assets for customers of VCB Hue in particular and the Bank for Foreign Trade of Vietnam in general.

For collateral assets being securities: banks need to boldly implement the acceptance of securities as collateral, this type of goods is currently being traded very popularly in the market, many banks have earned a lot of profit from this commodity. Banks have a securities company. Banks are specialized units in securities trading, fully capable of grasping information about securities and being able to quickly react to bad market changes. With a reasonable and safe lending rate, banks can completely implement it and of course this is a type of asset with a strong fluctuating value, affected by many factors, such as financial situation, reputation of the issuing organization, price fluctuations of the stock market, ... requiring the Board of Directors to have a strategic vision of the fluctuations of the stock market, thereby deciding on a reasonable lending level, limiting the risk of difficult debt collection.

For project home loan products:

It is necessary to expand the scope of real estate, not to limit it to lending only to real estate in a planning project where the project investor has signed a business cooperation contract with the Bank while the demand for real estate of the people is diverse in the context of the land of the whole country has not been comprehensively planned. The loan term for this type of product should be extended instead of the current maximum of 15 years because the gap between people's income and real estate prices is too large, so if the loan term is too short, the borrower will not be able to repay a loan large enough to buy a house. While the capital conditions of the Bank are considered one of the strongest banks, the joint stock banks

The non-state sector, with its small capital potential, has home loan products with loan terms of up to 20 years and 25 years.

For auto loan products

It is not advisable to only lend for 100% new cars or used cars that have been imported for less than 2 years and have not been used in Vietnam for a maximum term of 5 years. Used car transactions are much more common than 100% new cars, because used cars will be more affordable for most consumers. And lending for used cars is completely possible if the bank has a specialized valuation department or can request a third party, an independent valuation company, to appraise.

For unsecured loan products to support consumption applicable to employees and managers

No condition is required:

Executive managers must have at least 6 months of experience in an executive management position.

Employees must have at least 12 months of work experience at their current agency.

3.2 GROUP OF SOLUTIONS ON BANKING TECHNOLOGY AND PRODUCTS

3.2.1 Upgrading and developing banking technology

It can be said that in current conditions, technology is the foundation for developing services in general and banking services in particular.

Modern technology today allows commercial banks to develop banking services, modernize and automate operations for banking management and, most importantly, it increases the utility of traditional banking products and services. Technology supports the development of value-added services, thereby rapidly increasing both the number of retail customers and the number of personal accounts. The increase in the number of customers is an important topic for banks to expand their retail banking services and cross-selling services.

Enhanced governance in banking: a centralized governance system will allow data to be accessed anywhere, anytime, accurately and consistently, which is

powerful tool for management to make the right decisions. Particularly in the retail sector, technology supports centralized data processing, increases customer service speed, and facilitates the diversification of banking products and services. Accordingly, with modern management software, customer data will be updated and stored centrally. This feature helps to manage and classify customers in large numbers accurately, saving time and costs, while creating favorable conditions for the development of online banking transactions. With the fast processing speed brought by modern banking technology, it will significantly shorten the time for performing customer service transactions, allowing banks to quickly release customers, and increase the number of customers served to the maximum level within a fixed working period. In addition, the fact that customer accounts are connected to the entire system creates many conveniences for customers, such as customers can make transactions at any transaction location of the system. This feature creates the foundation for the emergence and development of cashless payments (card payments at ATM/POS points, online transactions via the internet, etc.) and is the key to bringing retail products to consumers.

The application of technology also helps banks save on labor costs, office rental costs and other administrative costs. The 24/7 ATM system, Homebanking, Internetbanking, Phonebanking services... and websites are effective support tools in providing information and services anytime, anywhere to customers. In addition, the deployment of technology software applications is having significant impacts on the bank's operating model towards centralized processing and deep specialization (one-stop transaction model, centralized processing model...). In fact, this is an effect with special results, because without the leveraging role of technology, the process of transforming the bank's operating model will be very long and complicated.

Thus, the structure, arrangement, innovation and upgrading of the information technology system to suit the new situation, using information technology as an effective tool to promote retail banking business activities. With the ability to automate operations, build and develop high-tech, breakthrough products and retail banking services, strengthen inspection and supervision,

Modernizing banking information technology is both urgent and a long-term factor ensuring the sustainable development of banks. The bank is a pioneer in developing banking technology. The bank has invested and developed a system data management software based on an American design platform, provided by Siverlake Snd.Bhd Company of Malaysia, built on the principle of providing banking services in accordance with international practices and standards - a strategic part of developing banking technology - put into use since September 1999 at the Transaction Office and has been deployed in the banking system. This can be said to be an extremely advanced technology system that the bank has invested in, creating many new breakthroughs in banking products and services.

However, there are still many features of the program that have not been exploited. The bank needs to quickly improve the program, maximize the application capabilities of the program, continue to develop many other support programs such as a business rating system, fully automated individual customer rating, diverse reporting programs and close to practical requirements to serve the management and operation of the banking system as well as customer appraisal, customer care and scientific research... In addition to strongly developing banking technology and deploying e-banking application solutions, banks need to focus on network security issues, anticipating unexpected events including internal and external attacks that can affect the operation of the e-banking system.

3.2.2 Research and develop new CVTD products to meet diverse customer needs

Financial support service for studying abroad : credit product for individual customers who need financial support to apply for a visa and/or pay for studying abroad and other expenses incurred during the study abroad period.

Financial proof loan: a credit product that proves financial capacity for studying abroad as required by training institutions, foreign Consulates and Embassies that the student's family has enough money to cover all expenses during the study abroad period.

throughout the study process (tuition, accommodation, insurance, books, travel...) for the student and still have enough money to take care of the lives of the remaining family members in Vietnam.

Loans to support small traders: credit products to meet the capital needs of small traders operating in markets within the same area of operation of the bank.

3.2.3 Promote the development of non-credit products to create complete product packages

The current banking products and services are still mainly traditional products, monotonous, lacking connectivity, so banks need to fully recognize the needs of customers to provide a comprehensive service package suitable for each customer. Promoting non-credit products such as payment services, domestic and international money transfers, deposit services, ATM cards, credit cards and other types of cards (Visa, Mastercard, ...), salary payment services through banks, custody services, investment trust, ... The more diverse and convenient non-credit products and services will attract more individual customers, creating cross-support between banking products, customers accessing this product will easily access consumer loan products and vice versa, customers using consumer loan products will access non-credit services, this is also a practical customer care and support while bringing benefits to the bank.

For example: Most CVTD products are related to housing and land transactions. If a bank offers a real estate transaction product, specializing in providing brokerage, intermediary, buying and selling real estate services to customers. Thus, through the bank, customers can come to conduct transactions to buy and sell houses and land and use home loan products safely and conveniently. The bank will both grow CVTD and have a source of fee revenue from the above transactions. It can be said that this is a very convenient all-inclusive support service for both customers and banks.

3.3 ADVERTISING SOLUTION GROUP

According to the recommendations of world banking experts, marketing activities contribute up to 20% to the total profit of retail banks.

To act according to customer desires, commercial banks must understand the customers they serve. However, currently customer information data is incomplete, and annual surveys are not conducted. Only on the basis of complete research and survey data can market segmentation be carried out.

Conducting market segmentation to reasonably determine the market structure and customers, thereby introducing products and promoting services suitable for each customer group, and having an effective approach and service policy for all customer groups, is an extremely necessary task. Banks need to develop a market segmentation policy, including both wholesale and retail markets. Therefore, it is necessary to have a systematic and uniform CVTD market research from top to bottom throughout the entire banking system.

Because retail customers are diverse in terms of social status, education level and economic circumstances, dividing customer groups will help banks have appropriate customer policies as well as preferential interest rates and appropriate service fees. Of course, in the spirit of serving all customers who come to them best, but clearly, each customer group will bring benefits to the bank at different levels due to the demand for products and the need to be served in each customer group. Dividing customer groups must be based on the characteristics of each customer group, so look at classification criteria such as: Financial potential, ability to use banking services, education level, level of use of banking services in the past... and depending on each customer group, the bank has appropriate customer care policies. Banks can divide customers as follows:

Luxury customers (VIP customers): are customers who conduct many transactions at the bank regularly with large transaction values. This is a group of customers who need to be provided with perfect services, to be served with a respectful attitude, in other words, they often have quite strict requirements for the services that need to be provided, they care more about service quality than price. VIP customers often bring high profits to the bank (usually they are the group of 10% of customers that bring the highest profits to that commercial bank).